How and when to report changes of income, address, etc. to Covered CA and/or Medi Cal

Try turning your phone sideways to see the graphs & pdf's?

You report must notify Covered CA and/or Medi-Cal any changes, higher or lower in:

-

your Estimated * MAGI Modified Adjusted Gross income for the-upcoming taxable year,

- If nothing else, don’t take APTC subsidy and just get it when you file taxes Form 8962,

- note the penalties if you under pay your estimated tax under form 2210 – instructions.

- marriage or divorce

- the birth or adoption of a child — number of people in your household,

- starting a job with health insurance

- gaining or losing your eligibility for other health care coverage

- Health Coverage Options for Individuals & Families if you lost job – CoronaVirus

- changing your residence – Address

- losing a job & income FAQ’s

- Suggestions on keeping health coverage when you lose a job FAQ

- Affidavit – Attestation of Income for Covered CA

- Proof of Unemployment?

- Reporting these changes will help individuals avoid large differences between the advance credit payments and the amount of the premium tax credit allowed on their tax return, which may affect their refund or balance due.

- Covered CA has asked agents not to give tax advice. Here’s their suggestions.

- Pros – Cons – Complicated FAQ’s Research on staying with under 65 plan? Covered CA? vs Medicare

- Medi-Cal process to handle reported changes.

- Be CAREFUL when you update income… It could cause your coverage to be cancelled!!! InsureMeKevin.com detailed Analysis

- Covered California’s Problems with Updating Income and Calculating Subsidies Insure Me Kevin .com

Deadlines to get your information in, namely new enrollment or annual renewal

- ROP Reasonable Opportunity Period to send Covered CA what they need or else you get cancelled Toolkit

- Covered California is required to check federal records several times each year to confirm eligibility

Jump to section on:

#Report changes as they happen - within 30 days! 10 CCR California Code of Regulations § 6496

10 days for Medi Cal 22 CCR § 50185

Our webpage on ARPA & Unemployment Benefits - Silver 94

IRS Form 5152 - Report Changes

- Our VIDEO on how to report changes to Covered CA

- Lost your job? How to keep your Health Insurance. Shelter at Home VIDEO

- References & Links

- Here's instructions, job aid, reporting change in income

- Our webpage on the exact definition of MAGI Income

- If you've appointed us - instructions - as your broker, no extra charge, we can do it for you.

- Voter Registration

- Denial of benefits and possible criminal charges if you don't report changes in income!

- When Increasing Your Covered California Income Estimate Creates an Ethical Dilemma Insure Me Kevin.com

- Fudging Income?

- Western Poverty Law on reporting changes

- How to cancel coverage.

- Visit our webpage on how to report changes

Covered CA Member’s #Duty to Report Changes in Circumstances

An enrollee, or application filer on behalf of an enrollee, must report any change of circumstances with respect to the eligibility standards within 30 days of such change. An enrollee, however, who has a change in income that does not impact the amount of the enrollee’s Advance Payments of Premium Tax Credit (APTC) or the level of Cost-Sharing Reduction (CSR) (See income chart or get a quote) is not required to report such a change. cdss.ca.gov/shd/res/htm/ParaRegs-Covered-California.htm * (45 C.F.R. § 155.330(b); * 10 CCR California Code of Regulations § 6496

§ 6496. Eligibility Redetermination During a Benefit Year.

(a) The Exchange shall redetermine the eligibility of an enrollee in a QHP through the Exchange during the benefit year if it receives and verifies new information reported by an enrollee or identifies updated information through the data matching described in subdivision (g) of this section.

(b) Except as specified in subdivisions (c) and (d) of this section, an enrollee, or an application filer on behalf of the enrollee, shall report any change of circumstances with respect to the eligibility standards specified in Sections 6472 and 6474 within 30 days of such change. Changes shall be reported through any of the channels available for the submission of an application, as described in Section 6470(j).

(c) An enrollee who has not requested an eligibility determination for IAPs shall not be required to report changes that affect eligibility for IAPs.

(d) An enrollee who experiences a change in income that does not impact the amount of the enrollee’s APTC or the level of CSR for which he or she is eligible shall not be required to report such a change.

(e) The Exchange shall verify any reported changes in accordance with the process specified in Sections 6478 through 6492 before using such information in an eligibility determination. Cal. Code Regs., tit. 10, § 6496, subds. (b), (d).)

Definition of change

1a: to make different in some particular : ALTER never bothered to change the will

b: to make radically different : TRANSFORM can’t change human nature

c: to give a different position, course, or direction to changed his residence from Ohio to California Webster

Learn More about Medi Cal Fraud

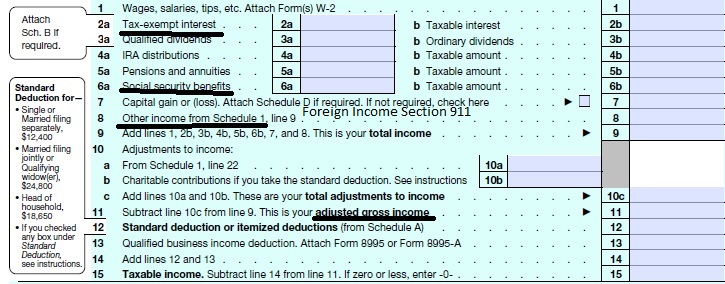

Calculate your Covered CA MAGI Income

take #Line8b 11 Adjusted Gross income then add line 2a, 6a & 8 (Foreign Income)

- 1040 IRS Annual Tax Form

- Schedule 1 Additional Income & Adjustments to Lower your MAGI Income

- Estimate next years MAGI Income?

- Get instant quotes, subsidy calculation and coverages

- NO ASSET TEST for MAGI based subsidies in Covered CA or MAGI Medi Cal Qualification. VIDEO

- Nor is there a lien against your estate for Covered CA or MAGI Medi Cal

Estimating Income

How to #Estimate MAGI Income for Covered CA?

Covered CA bases your subsidies on what you expect your household income will be for the upcoming coverage year, not last year’s income. When you calculate your income, you’ll need to include the incomes of you, your spouse, and anyone you claim as a dependent when you file taxes.

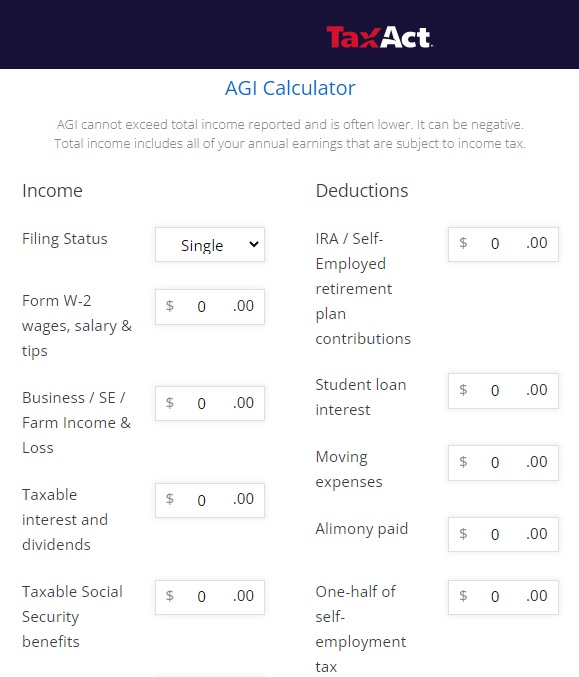

You can start by using your adjusted gross income (AGI) from your most recent federal income tax return, located on line 11 on the Form 1040.

taxact.com/adjusted-gross-income-calculator

- From the AGI above, Add back in any foreign income, Social Security benefits and interest that are tax-exempt. Then, add or subtract any income changes you expect in the next year.

- Health Care. Gov on estimating income

- Scroll down for more information on estimating income.

More on estimating Income

If you are self-employed or unemployed, you might have an unpredictable income. If so, just estimate as best you can, Covered CA and the IRS don’t think that you have a crystal ball, then just report changes in income throughout the year in your account.

IMHO all these estimates are just Hocus Pocus. It all comes out in the wash when you file your Tax Subsidy Reconciliation form form 8962 with your tax return. Covered CA *

Self Employed, Free Lancers & 1099?

The amount of your Advance Premium Subsidies APTC go by estimated net income for the year you’ll be covered, not the previous year. Estimating your income to find out how much financial help you’ll get can be tricky for self-employed people. It can be difficult to know how much you’ll make in the coming year, which is information you need to find out your monthly premiums. Estimate your income and expenses as best as you can, using industry trends and past experience as a guide.

If your yearly net income looks like it will be higher or lower than what you estimated, log in to your account, or email us [email protected], if we are you broker and update what you previously reported. If you end up making more than what you estimated, at tax time you may have to pay some or all of the financial help (in the form of Advanced Premium Tax Credits) you received. Conversely, you could get money back if you end up making less. Covered CA *

Resources & Links

- Oscar Insurance – Tips on estimating income

- Explaining Health Care Reform: Questions About Health Insurance Subsidies Kaiser Foundation *

- Try some of the tax estimators…

- MAGI – Modified Adjusted Gross Income – Line 11

- APTC Advance Premium Tax Credit – Subsidies – Introduction

FAQ’s on Estimating Income

#caca1

- Question I’m applying for insurance on the Covered California website. While registering it asks how much I anticipate my income to be.

I’m currently unemployed but looking for a job.

Should I put the number I anticipate to make or $0.00 since I’m unemployed?

If I put a number in, the next question it asks is who employs me.

Should I type “unemployed” even though I typed in a dollar amount for “Anticipated Income”?

- Answer How much do you expect to earn in the upcoming current coverage tax year?

Why?

How much did you earn last year?

How long have you been unemployed?

- If you put zero, you’ll qualify for no premium Medi-Cal.If your MAGI Income estimate changes, you’re mandated to report to Covered CA within 30 days. If you’re on Medi-Cal 10 days.How about appointing us as your agent, no extra charge, so that we get paid for helping you?

Advocacy Tip: Enrollees who are uncertain about their income estimate may be well served by taking a smaller amount of premium tax credits each month in advance so they are not at risk of owing money come tax time. The Covered California website includes a sliding bar that allows enrollees to choose how much of the tax credit to take ahead of time.

individuals who enroll in a plan through Covered California without premium tax credits and realize later that they were eligible can claim those premium tax credits when they file at tax time.

- So, if you just pay “full price,” (get quote) then you shouldn’t have to put in an employer. When you do get employed, you can change your estimate. This way you don’t have to have Medi Cal.

- If you put zero, you’ll qualify for no premium Medi-Cal.If your MAGI Income estimate changes, you’re mandated to report to Covered CA within 30 days. If you’re on Medi-Cal 10 days.How about appointing us as your agent, no extra charge, so that we get paid for helping you?

Tons of FAQ’s #about estimating Income

- Our combined household income will put us over the limit to qualify for any subsidy. I’m ok with paying out of pocket full premium but this article seems to make even that impossible.

california healthline.org/this-family-says-no-to-medi-cal-but-a-computer-wont-listen/ - Is this still an issue since the article is from 2016 ? Or do I need to buy insurance directly from insurers rather than on covered CA. Would that fix the problem?

- Did you check the income chart? Two people would be $100K

- Please use our quote engine cited above.

- What Special Enrollment Reason will we use?

- There is a Special Enrollment for those who don’t have coverage due to COVID 19. We might be able to do that.

- It’s my understanding only Covered CA has the Special Enrollment for COVID 19. I can double check.

- Our webpage on Insurance and COVID 19.

- Our webpage for Health Net PPO & HMO Individual

- Our webpage on dual coverage.

- Yes income is much higher than that so I’m sure we won’t qualify for subsidies.

- When I enter our ZIP code on covered CA the health net plan doesn’t show up. So I believe I’ll have to buy it outside covered CA.

- Does special enrollment apply to health net plan purchased directly through them as well?

- Please use OUR quote engine, so that we can follow what you are doing. Also, we only get compensated if you purchase through our affiliate link, no extra charge.

- We do not accept hearsay. We need to see the exact stuff!

- Covered CA not Health Net pay us for our second to none website. Nor for the time it saves their personnel on the phone.

- Here’s our online enrollment link and quoter for Health Net.

- Yes, since everything under ACA/Health Care Reform/Obamacare is guaranteed issue, no pre-x, you can only buy at Open or Special Enrollment. Not when you get diagnosed with cancer and have MAJOR bills ahead!

- If you can get Medi-Cal to disenroll you, that would be a special enrollment for loss of coverage.

- Here’s an excerpt of Health Net’s bulletin about the COVID 19 special enrollment

- Here’s what you need to know about the SEP:

• Any uninsured individual or family can use this SEP to apply for 2020 health coverage.

• This SEP is for new enrollment only and not available for plan changes.

• To enroll in one of our off-exchange plans, go to http://www.myhealthnetca.com. Proof of a qualifying event is not needed to enroll under this SEP. You may also use the existing 2020 IFP enrollment forms to apply by mail.

• Effective dates of coverage are:

Enroll by Effective date

May 31 June 1, 2020

June 30 July 1, 2020 - • After June 30, 2020, the regular special enrollment period qualifying events apply.

• First month’s premium payment is required to activate coverage.

• The impact of COVID-19 on small businesses may be causing some people to lose employer based health coverage. Individuals can use this SEP to enroll with Health Net to regain health coverage. - So, it looks like, if you take your Mom as a dependent, Medi-Cal will kick you out.

- Then you would have a special enrollment period for loss of coverage.

- Here’s a list on Stanford’s website of the plans they take.

- Please use OUR quote engine so we can properly consult with you.

- Medi Cal Plans

- Santa Clara Family Health Plan

- Stanford Health Care is in-network for hospital and specialist physician services only. You would not be able to select a Stanford Health Care physician as your primary care physician.

- In order to be seen at Stanford Health Care, your primary care physician would need to refer you and your medical group or health plan would need to authorize all services provided at Stanford Health Care or by Stanford Health Care physicians.

- Our webpage on appeals & grievances

- Santa Clara Family Health Plan Medi Cal Website

- Member Handbook

- See page 36 for information on getting a second opinion

- I have been looking online for some answers and I hope that you guys can help

- I live far away from town and have not yet filed for a 1040 Tax return I never filed a tax return last year either

- I do not work I haven’t for quite some time but I am on record the secretary for a non-profit company I’m not too sure if he has filed anything.

- Will not filing a tax return affect my Medi Cal application for claiming my daughter as a dependent.

- I am not married I am single. I have enrolled into medi-cal when I was pregnant

- I had gotten food stamps and CalWORKs 4 maybe 5 months

- I do not get that anymore.

- Does that affect my tax return as well.

- I have a daughter and people were telling me that I should have filed for a return for a dependent for this year and last year

- I do not know the process and how this works

- so please give me a call or email at your earliest convenience

- hopefully you guys can help thank you have a good night

- It sounds to me like you have zero income. Thus there is no mandate to file a return. Here’s the IRS tool to determine if you need to file a return. Here’s a website that says if you are head of household, you don’t need to file a return if you earn less than $18k.

- I’m not authorized to give you tax advice. Try VITA.

- I don’t listen to “what other people say.” Yes, it’s cost me friendships and people in charge or think they are in charge don’t like it, but the law is the law and what is right is right, not just because something was given some authority somewhere or they were told by an expert…. One needs to actually read the law 3x, then when you think you understand it, read it again.

- Medi-Cal beneficiaries are not required to file a federal income tax return and many Medi-Cal beneficiaries have household income well below the minimum income level at which a U.S. citizen or resident must file an income tax return. Some beneficiaries may still choose to file taxes to collect other federal tax credits. With the implementation of the Modified Adjusted Gross Income (MAGI) income counting methodology, this has been a source of confusion for some county eligibility workers.

- However, Medi-Cal does not require applicants or beneficiaries to file taxes and, in fact, has special “non-filer” rules for determining the household size for those who do not file taxes. Copied from Western Poverty Law

- Did you need term life insurance, see above for quotes.

- Are you getting alimony or child support?

- Have you been asked to Redetermine?

- If one no longer has his job and expects his income for this year to be low (pursuing a new self-employment business) and thus qualify for Medi-Cal, how can one prove this in applying in order to be accepted for Medi-Cal. (The tax returns would show too much income from the previous year in order to qualify.)

-

See our web pages on

-

accepted proofs of income

proof-income-accepted-documents/ -

Then scroll down and get more details on:

-

Business records such as profit and loss statements

- Excel Template

- Quicken Software

- Your Bank’s ONLINE Spending Reports

-

Bank Statement Review

-

Self employed Health Insurance Deduction

-

Home Office Deduction

-

Computing Subsidies and Health Insurance Deduction

-

Premium Subsidy reconciliation – it’s not what you made in 2019, it’s what do you expect to make in 2020!

-

Be sure to report changes in income within 10 days.

-

There might be criminal penalties if you don’t!

-

- I have a part time job and earn less than $2k/month, do I still qualify for Medi-Cal? I have over $3k in assets, is that relevant to getting Medi-Cal?

- See our income chart or use the instant quote calculator.

- We need an actual # for your income. If you are single, if you earn over $17k gets you Covered CA subsidies. Medi Cal is if you are less than $17k. So, telling us under $2k means nothing.

- There is NO Asset test for MAGI Income Medi-Cal qualification.

- If you earn more than Medi Cal Limits 138% of income, do you have to repay the premiums that Medi Cal paid to the HMO, if you didn’t tell Medi Cal that you were earning more?

- Usually no. Learn More @ Insure Me Kevin.com

- Can I get Medi-Cal if I get unemployment?

- Qualifying for MAGI Medi-Cal a function of the number of people in your family – tax return and your expected MAGI income for the current tax year.

- Please use our complementary subsidy, premium and benefits calculator and then we can help you better.

- Medi-Cal has year around enrollment.

- Please review the special enrollment qualifications.

- There used to be temporary plans and Mr. Mip, which is minimum essential coverage and covers pre-existing conditions.

- I’m on Medi-Cal as I have no income. I just turned 65.

- Did I have to apply for Medicare A Hospital?

- Part B Doctor Visits?

- I can’t afford the $135/month premium.

- Yes, I believe so. Please note that I’m not an authorized Medi Cal agent or employee. Contact Medi Cal to double check, they make excellent salaries with benefits and vacations and are paid to help you.

- adults aged 19 through 64, who are not pregnant, not eligible for Medicare, and with incomes below 138% of the FPL became eligible for Medi-Cal as of January 1, 2014 – the start of ACA/Obamacare.

- Here’s my research:

- Beneficiaries who turn 65 while they are enrolled in Medi-Cal as an Expansion Adult must be evaluated for eligibility in all other Medi-Cal programs, i.e., non-MAGI programs such as for the aged, blind or disabled, before they are disenrolled. Citation Western Poverty Law Page 2.36

- Here’s the link to Enroll in Medicare

- Once you get Medicare A & B we can set you up with a Medicare Advantage Plan with Blue Shield, AARP or Blue Cross. Most of these plans have ZERO premium and all include Part D Rx.

- You can pay your Part B Hospital premium of $135 from Medicare from your Social Security check.

- Yes, I believe so. Please note that I’m not an authorized Medi Cal agent or employee. Contact Medi Cal to double check, they make excellent salaries with benefits and vacations and are paid to help you.

- I got a new job in April. My company will be offering me health benefits starting in June. But job is not certain, they might let me go anytime. 1. What do you recommend regarding Medi-Cal? 2. can i continue with Medi cal? 3. if i cancel medi cal do you think if i loose my job i will be again eligible for the medi cal?

- Glad to hear you got a new job with benefits.

- 1. Medi-Cal and Covered CA require that you report changes within 30 days, here’s the instructions. Do you have a Medi Cal ONLINE account?

- 2. If your income is below 138% of poverty level, I guess you could have both Medi Cal and your Group Coverage. Here’s information on dual coverage.

- 3. Yes, depending on your income. If you lose your job, report that to Medi-Cal.

- I don’t get paid to help the public with Medi-Cal. Here’s their contact page.

- If the Company you worked at got bought out by another company, and your status changes from contractor to full time employee, are you still eligible for Medical [Medi-Cal] if you can’t afford the premiums or out of pocket [deductibles, co-pays] insurance plans they offer, based on your annual [MAGI} income?

- My position is outside sales, with a home office, now I am having even more expenses than before, due to the new company’s contract. I can not afford what they offer in regards to healthcare coverage.

- If you qualify for Medi-Cal is based on your MAGI income being above or below 138% of Federal Poverty Level FPL. In 2018 for a single person that would be $16,644, see chart.

- If your income is between 138 and 400% of FPL, you can probably get Covered CA subsidies to help pay your premium. Use our complementary instant quote engine to find out.

- Your statement about affordability of health insurance premiums for your employers plan has to do with getting Covered CA subsidies, not Medi-Cal. Basically, it depends on if the premiums are more or less than 9.66% of income. We deal with the affordability issue for Covered CA subsidies on this page.

- Kentucky Gets exemptions so that they can require Medicaid recipients to work modern health care.com La times latimes.com/

- I am 70 years of age and have been on medi cal due to low income. I recently applied for my ex husbands social security and my income increased to $1379.10. Can I still qualify for medi cal?

- ***We are setting up a new page to discuss Medi-Cal Qualification for Seniors. Please click and visit us there.

- I am single, and unemployed. In January 2021, I made over $100k from a stock sale. For the rest of the year, I will make around $1,200/mo. Question: Is it my annual income or my current monthly income ($1,200/mo) that determines Medi-Cal eligibility? My annual income will be large because of the stock sale in January 2021. However, my current monthly income is low. Am I eligible for Medi-Cal?

- That’s what our webpage and citations say. I’m not an authorized Medi Cal agent, nor am I compensated to help people with Medi-Cal. So, just enroll online here.

- Check back around April 14, when we have all the information on ARPA COVID Stimulus... things might change?

- Did you want to look at Long Term Care, Life Insurance, Medicare, etc?

- FAQ’s on Premium Subsidy & Projected Income

- I am not getting APTC, and will get PTC next year, at tax time, does it matter what I make monthly; in other words, if one month I make under $1,833, is that relevant?

- ***I understand how confusing it is, especially when Covered CA asks so many questions about monthly income. The point is when you file your taxes, what goes on line 37* Magi Income.

- Although, Medi-Cal wants to write everyone and their calculations are based on monthly. only the annual sum is important.

- ***Right. See MAGI Definition monthly under 1833 for the month.

- ***Please talk to me in the bottom line MAGI income for the end of the year. I don’t know how many are in your household. Now I have to multiply 12 x $1,833 = $21,996 if you have a household of 2 it’s borderline, but you are right, that would put you in Medi-Cal.

- Should we make it a point to have at least that much monthly income for the remainder of the year?

- ***The monthly amounts are all hocus – pocus with smoke and mirrors. What counts is the annual. Please use our quote engine and see what happens with your income on an annual basis. Some people at Medi Cal might disagree.

- Did you want to look at getting Enhanced Silver – Cost Sharing Reductions?

- Do you sell health insurance not run through covered california?

- ***Yes. Get quotes here. If you want the subsidy though, you must have Covered CA. Click here for instructions on how to appoint us as your agent, no extra charge. Did you like our answer better than calling Covered CA?

- income from the IRA – Annuity,

- ***Line 15 A of the 1040

- Are you saying that I would drop into Medical [Medi-Cal] if the monthly income dropped below $1,833 for the next month or even four months, despite the fact that the annual quota has already been surpassed.

- ***No, not at all. It’s all annual MAGI. This monthly is for people who want subsidies and can’t figure out the annual amount they will put on line 37* Medi-Cal does want to write everyone and not let them out.

- You said the annual income is what matters,

- ***Right. But please do not quote me. I only read the official IRS publications, namely publication 974 and Covered CA bulletins.

- but the part I described above and your response confused me. Are you saying that the annual is what matters as long as you make a minimum of 1833 for each month of the year?

- ***Yes. Please, forget the monthly amount. It’s just crap for those who can’t figure out what their MAGI* incomewill be on line 37.

- How about appointing us as your agent so that we can get paid to help you. Sure, Covered CA says find free help, but it’s not free. It’s slave labor until I get appointed. There is no extra cost to you.

- Since you are not taking the advance premium tax credit and if I understand you correctly, are not taking it in advance next year, just put that down and you shouldn’t have to enter an income amount.

- ***Please use our quote and subsidy calculator. You will note, it only asks for annual income.

- As I understand it, insurance sign up starts in November.

- ***Right, now it’s October for a January effective date.

- I have not gotten a subsidy this year, because my projected income is above 63k.

- ***That’s what the chart shows for a household of two, but it’s best to get a complementary quote and subsidy calculation.

- I did not want to drop into medicare [Medi-Cal] if I made less than $1,833 in a month).

- ***MAGI Income is ANNUAL – what shows on line 37 of your 1040.

- MAGI Income – Medi-Cal Qualification? However, I definitely do not want APTC. [Advance Premium Tax Credit]

- ***That’s what the brochures on the above right and on this page talk about. Take the credit now or later? If your income drops below $34k you may qualify for Enhanced Silver Cost Sharing Reductions.

- If I renew for CC in November and I indicate that I don’t want APTC, would I still have to provide a breakdown of projected income, along with documentation?

- ***No, note the new rule I just found that says Covered CA – the Exchanges MUST vette everyone who asks for Premium Credits. (42 U.S. Code § 18081 * CFR § 155.320)

- When you asked if I would give up the subsidy, did you mean APTC, or do you mean the PTC that one gets as a refund on taxes.

- ***You have to stay in Covered CA to get either subsidy.

- Does one have to fill out the financial part of the [Covered CA] application for next year in order to get the PTC on the tax refund following the benefit year?

- ***Yes, as Covered CA must vette everyone under 42 U.S. Code § 18081 * CFR § 155.320

- Again, I have heard different opinions on this.

- ***That’s because very few people actually read the CFR’s, actual IRS documents and the documents don’t always refer to the other relevant rules, codes & laws. Check our main page on take it (APTC or PTC) now or later.

- I was temporarily laid off on March 30. My income is low and I might be eligible for Medi-cal. Could you look into it for me, please.

- We had a question just like this a week ago. Please click on the following link, review that and if you have any further questions, ask on the relevant page.

- If you want us to put in into Medi Cal, where we don’t get paid to help you, we will do that, as you’ve been a client. Please send us a “clear” email as to what your income is, and what you want us to report to Covered CA, under penalty of perjury.

- Don’t forget, unemployment is taxable.

- The Feds have a bill pending to pay 100%!

- As, you’ll see on the Q & A for the other similar question, once you get into Medi Cal, it’s very difficult to get out.

- I’m a real estate agent and my income fluctuates. So, I read the above, but didn’t click on the links – citations. Are you sure the law says monthly?

- Monthly vs. Annual income: MAGI Medi-Cal rules allow counties to base eligibility on monthly rather than annual income. If an applicant provides both monthly and annual income, counties are instructed to divide the annual income by 12, compare it to the monthly amount also provided, and use the lower of the two amounts Western Poverty Law

- if the individual’s current monthly income is lower than the projected annual income divided by 12, counties should enter the current monthly income.dhcs

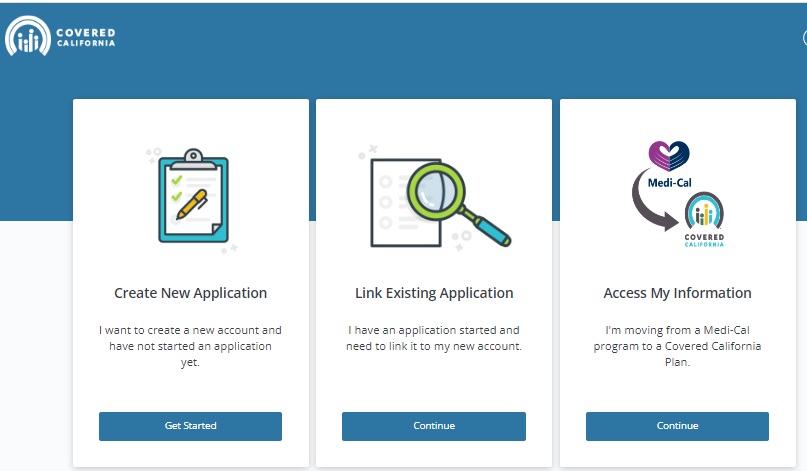

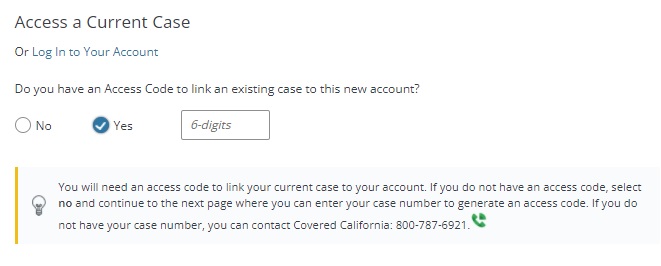

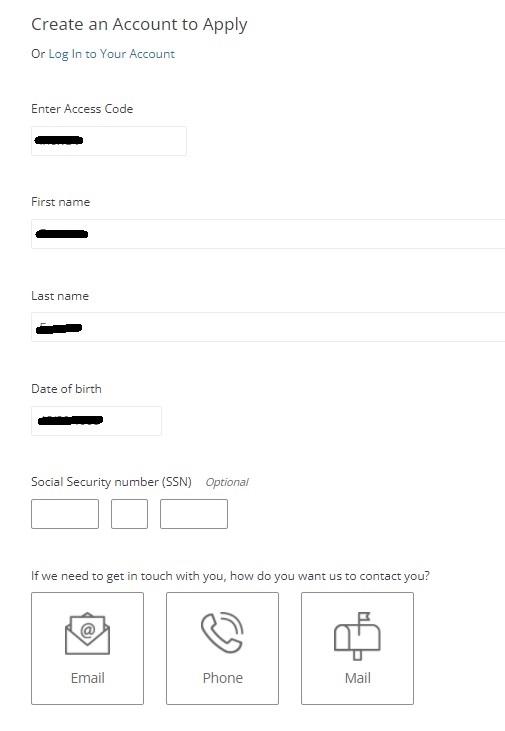

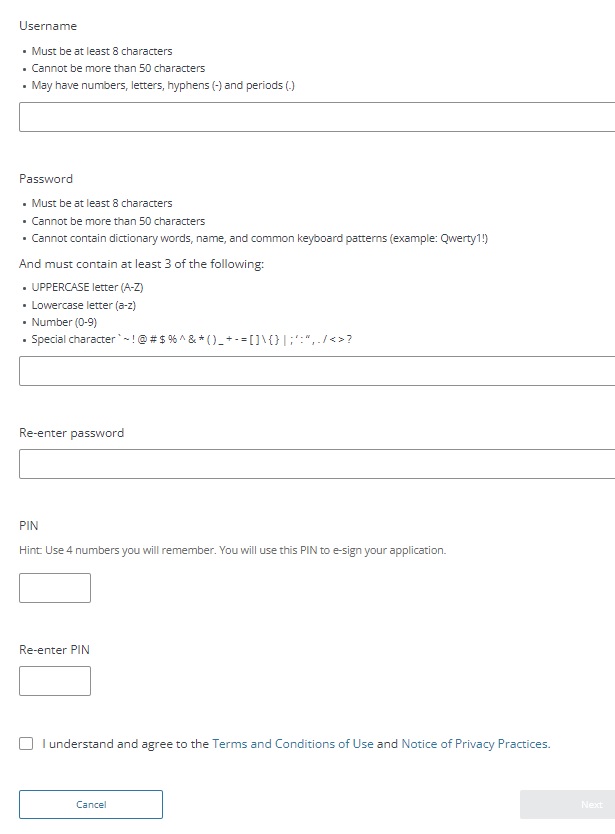

How to #create your Covered CA online account

Login

Here’s instructions and/or See video‘s on the right or scroll down, to create and gain access to your account on Covered CA’s website creating-an-online-account

Other ways to pay your premium?

If all else fails, we can set a Zoom Meeting to do it together.

Steps to Create an Online Account for Existing Members

|

|

||

|

|

||

|

|

||

|

|||

|

|||

|

|||

|

|||

|

|||

Forgotten User Name or Password

- If you have forgotten your user name or password after setting up a Covered California online account, visit Covered CA’s Frequently Asked Questions page to learn how to change them.

- Copied from coveredca.com/creating-an-online-account We added the pictures

- coveredca.com/no-delegation-access-code

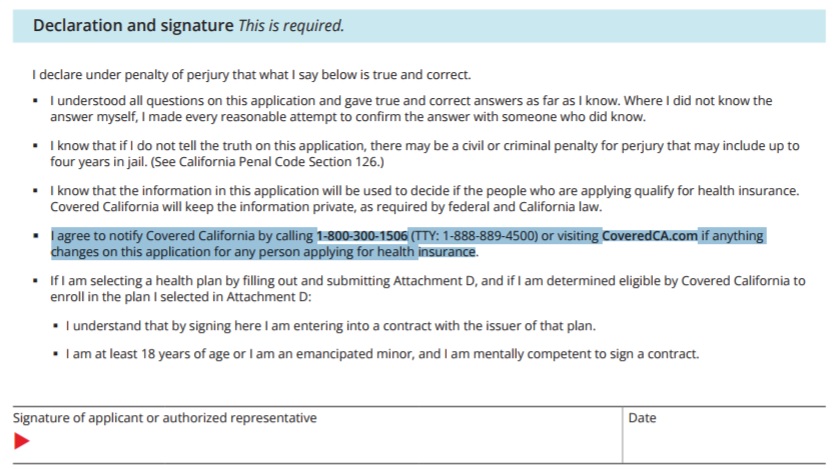

Perjury Declaration - Signature - Agree to notify changes

and that the application is correct in the first place

Mandate to File Tax Return

& Form 8962

Etc. Copied from Covered CA ONLINE application 11.26.2014 – Paper Application Rights & Responsibilities Page 16

I agree to file a tax return before (April 15, ) to claim the Premium Tax Credit. I understand that I am required to submit changes that affect my eligibility, including income, dependency changes, address, and incarceration. These changes could affect the plans I can be enrolled.

I cannot change plans unless I have a life triggering event. Life Events include lost or will soon lose my health insurance, permanently moved to/within California, had a baby or adopted a child, got married or entered into domestic partnership, returned from active duty military service, gained citizenship/lawful presence, Federally recognized American Indian/ Alaska Native, released from jail, and other qualifying life events.

#Withholding W 4

IRS Withholding Calculator

Here’s tools to make sure the right amount is withheld, either for tax refund purposes or to avoid an unexpected tax bill next year.

“It’s a personal choice if you want to have extra money withheld to get a bigger tax refund, but you have options available if you prefer to have a smaller refund next year and more take-home money now.” Advance Premium Tax Credit now or later?

By adjusting your Form W-4, Employee’s Withholding Allowance Certificate, taxpayers can ensure that the right amount is taken out of their pay throughout the year so that they don’t pay too much tax and have to wait until they file their tax return to get any refund. Employers use the form to figure the amount of federal income tax to be withheld from pay. IRS Tax Withholding Calculator

People Working in the Shared Economy

Covered CA Consent for Verification – Income, etc.

Review the Consent for Verification Notice that Covered California sent to consumers last week and the Consent for Verification Quick Guide for more information.

Also, watch the How to Update Consent VIDEO for instructions on updating consumer consent.

Consumers are at risk of losing their Advanced Premium Tax Credit (APTC) and/or cost-sharing reductions for health insurance coverage if their consent form is out of date.

A consumer’s financial assistance may end because of one or more of the following reasons:

- The consumer’s consent to allow Covered California to use computer sources to check their income and family size, including information from tax returns, has expired.

- The consumer may not have filed afederal income tax return for their household to reconcile the Advanced Premium Tax Credit (APTC) used to lower plan premium costs

- The consumer’s household income may be too high.

Covered CA

Right to change plans when there is a #SilverChange due to higher or lower Estimated MAGI Income

One way to to make a change in your Covered CA coverage when it’s not Annual Open Enrollment is if your income changes, so that you qualify for a new or different level of Enhanced Silver Subsidies or income change makes you newly eligible for subsidies. Covered CA’s interpretation of the law is that you must already have coverage through Covered CA, to do this. FN 1

CA CCR Code of Regulations (7)

An enrollee Definition, or his or her dependent enrolled in the same QHP – Qualified Health Plan, is determined newly eligible or ineligible for APTC (Subsidies) or has a change in eligibility for CSR. [Cost Sharing Reductions – Enhanced Silver]

See more detail and discussion in footnotes below.

It just doesn’t seem “Fair” that if someone makes $100k as a single and then loses his job, can’t enroll when that happens.

Yes, I’ve been told that if you want Fair, you have to go to Pomona.

Response By Email (Argelia) (03/26/2018 11:57 AM) Good day Steve Shorr, Thank you for contacting Covered California™. A change in income is not a Qualifying life event. If you select “other qualifying life event,” it puts a hold on the account. In the future, for income changes you need to select “none of the above.”

CFR §156.425 Changes in eligibility for cost-sharing reductions. (Enhanced Silver)

Please start your research into Special Enrollment Periods by reviewing our main page of California Code of Regulations on Qualifying Events

See Full FPL Federal Poverty Level Chart – Income vs Plan and Program you and your family qualify for

(a) Effective date of change in assignment. If the Exchange notifies a QHP issuer of a change in an enrollee’s def eligibility for cost-sharing reductions (including a change in the individual’s eligibility under the special rule for family policies set forth in §155.305(g)(3) of this subchapter due to a change in eligibility of another individual on the same policy), then the QHP issuer must change the individual’s assignment such that the individual is assigned to the applicable standard plan or plan variation of the QHP as required under §156.410(b) as of the effective date of eligibility required by the Exchange.

(b) Continuity of deductible and out-of-pocket amounts. In the case of a change in assignment to a different plan variation (or standard plan without cost-sharing reductions) of the same QHP in the course of a benefit year under this section, the QHP issuer must ensure that any cost sharing paid by the applicable individual under previous plan variations (or standard plan without cost-sharing reductions) for that benefit year is taken into account in the new plan variation (or standard plan without cost-sharing reductions) for purposes of calculating cost sharing based on aggregate spending by the individual, such as for deductibles or for the annual limitations on cost sharing ECFR.Gov

(6) Newly eligible or ineligible for advance payments of the premium tax credit, or change in eligibility for cost-sharing reductions.

(i) The enrollee is determined newly eligible or newly ineligible for advance payments of the premium tax credit or has a change in eligibility for cost-sharing reductions; [Enhanced-Silver]

advance payments of the premium tax credit (subsidies) or is experiencing a change in eligibility for Enhanced Silver – cost-sharing reductions CA Agent Training Page 9 or premiums become unaffordable 155.420 156.425 156.410

premium tax credit

determined newly eligible or newly ineligible for advance payments of the premium tax credit or has a change in eligibility for cost-sharing reductions [enhanced silver],

Special enrollment periods no longer will be available for:

Consumers who had signed up for exchange plans with too much in advance payments of tax credits because of redundant or duplicate coverage;

Consumers who were affected by Social Security income tax errors; (Counihan, CMS blog, 1/19). Learn More ⇒CA Health Line – Health Affairs.org 1.20.2016

(ii) The enrollee’s dependent enrolled in the same QHP is determined newly eligible or newly ineligible for advance payments of the premium tax credit or has a change in eligibility for cost-sharing reductions; or

(iii) A qualified individual or his or her dependent who is enrolled in an eligible employer-sponsored plan is determined newly eligible for advance payments of the premium tax credit based in part on a finding that such individual is ineligible for qualifying coverage in an eligible-employer sponsored plan in accordance with 26 CFR 1.36B-2(c)(3), including as a result of his or her employer discontinuing or changing available coverage within the next 60 days, provided that such individual is allowed to terminate existing coverage.

affordable or provide minimum value [bronze plan] for his or her employer’s upcoming plan year to access this special enrollment period prior to the end of his or her coverage through such eligible employer-sponsored plan; Learn More⇒Change Enhanced Silver

(iv) A qualified individual in a non-Medicaid expansion State who was previously ineligible for advance payments of the premium tax credit solely because of a household income below 100 percent of the FPL, who was ineligible for Medicaid during that same timeframe, and who has experienced a change in household income that makes the qualified individual newly eligible for advance payments of the premium tax credit.

Footnotes

1. Covered CA cites their webpage and says change in income is only if you are already enrolled in a Covered CA plan. Email dated 11.14.2016 3:35 PM 45 CFR §155.420(d)(6); 10 CCR – CA Code of Regulations – Special Enrollment Periods § 6504(a)(6). Note that Covered California interprets this to only allow for changes in plan, not to newly enroll based on language in the state and federal regulations referring to the enrollee rather than the individual as in other sections. Thus, if you are already in a plan you can change to a new plan but you can’t newly enroll in a plan when your income decreases. Western Poverty Page 5.215

45 CFR §155.420(d)(6) Newly eligible or ineligible for advance payments of the premium tax credit, or change in eligibility for cost-sharing reductions.

(i) The enrollee is determined newly eligible or newly ineligible for advance payments of the premium tax credit or has a change in eligibility for cost-sharing reductions;

(ii) The enrollee‘s dependent enrolled in the same QHP is determined newly eligible or newly ineligible for advance payments of the premium tax credit or has a change in eligibility for cost-sharing reductions; or

(iii) A qualified individual or his or her dependent who is enrolled in an eligible employer-sponsored plan is determined newly eligible for advance payments of the premium tax credit based in part on a finding that such individual is ineligible for qualifying coverage in an eligible-employer sponsored plan in accordance with 26 CFR 1.36B-2(c)(3), including as a result of his or her employer discontinuing or changing available coverage within the next 60 days, provided that such individual is allowed to terminate existing coverage.

(iv) A qualified individual who was previously ineligible for advance payments of the premium tax credit solely because of a household income below 100 percent of the FPL and who, during the same timeframe, was ineligible for Medicaid because he or she was living in a non-Medicaid expansion State, who either experiences a change in household income or moves to a different State resulting in the qualified individual becoming newly eligible for advance payments of the premium tax credit;

Enrollee means a qualified individual

or qualified employee enrolled in a QHP. Enrollee also means the dependent of a qualified employee enrolled in a QHP through the SHOP, and any other person who is enrolled in a QHP through the SHOP, consistent with applicable law and the terms of the group health plan. Provided that at least one employee enrolls in a QHP through the SHOP, enrollee also means a business owner enrolled in a QHP through the SHOP, or the dependent of a business owner enrolled in a QHP through the SHOP. Qualified individual means, with respect to an Exchange, an individual who has been determined eligible to enroll through the Exchange in a QHP in the individual market. Definitions 155.20 You can completely forget about what federal law has to say when it comes to Covered CA. Since Day 1, they have been making up their own rules without regard to the law when it suits their fancy. So, to Covered CA, decrease in income only allows a change of health plan if already enrolled through Covered CA despite the fact that in just about any other state, it triggers an SEP. MAX Herr Response from Covered CA Income changes so much that a current Covered California enrollee becomes newly eligible or ineligible for help paying for their insurance. For example, if a consumer is already getting help paying for their insurance premium, and their income goes down, they may be able to get extra help. coveredca.com/special-enrollment

This is what it states in Healthcare.gov.If you’re enrolled in a Marketplace plan and your income or household change, you should report the changes as soon as possible. These changes — like higher or lower income, adding or losing household members, or getting offers of other health coverage — may affect the coverage or savings you’re eligible for.

Why it’s important to update your application immediately

If your income estimate goes up or you lose a household member: You may qualify for less savings than you’re getting now. If you don’t report the change, you could have to pay money back when you file your federal tax return. If your income estimate goes down or you gain a household member: You could qualify for more savings than you’re getting now. This could lower what you pay in monthly premiums. You could qualify for free or low-cost coverage through Medicaid or the Children’s Health Insurance Program (CHIP). healthcare.gov/why-report-changes/

More Info

• Income and Reconciliation Notice

• APTC & Income Talking Points

If you haven’t given Covered CA permission to verify income, you will be renewed, but without the advance premium tax credit and risk cancellation Insure Me Kevin.com

- VIDEO What is APTC Advance Premium Tax Credit

- Health Net VIDEO How to get subsidies – pay less for coverage

- Interactive Tax Assistant (ITA)

- Am I eligible to claim the Premium Tax Credit?

- IRS FAQ on Premium Tax Credit

Tax #Estimators

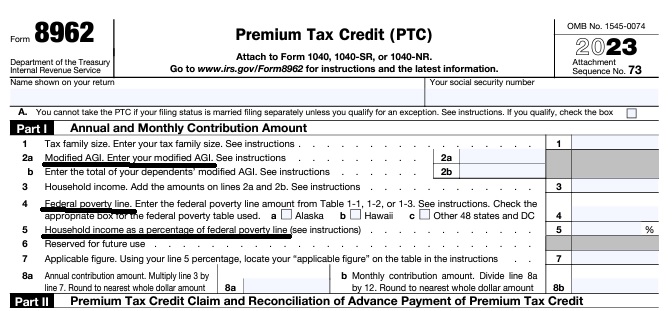

Federal IRS #Form8962 Instructions Premium Tax Credit

Reconciliation Form for Covered CA Subsidies attaches to 1040

Subsidy is IMHO hocus pocus - smoke & mirrors

it all comes out when you file taxes!

-

Introduction

-

If you got too high a subsidy or too low, it gets reconciled at tax time on form 8962. If your subsidies were too high you may have to pay the excess back and maybe penalties, if too low, you can get a tax refund or lower the amount you have to pay. In a lot of ways, IMHO subsidies are hocus pocus, jiggery pokery - smoke and mirrors as it's all guesswork and promises. Be sure to report income and household changes within 30 days.

- Instructions for IRS Form #8962 Subsidy Reconcilation

- ARPA & Inflation Reduction Act of 2022

- Instead of increasing taxpayer audits, policymakers should simplify taxes across the board. That way, it would be easier for everyone to pay the correct amount to the government. heritage.org/who-those-87000-new-irs-agents-would-audit

- That 87,000 new tax agents estimate represents everything from IT techs to customer service people who answer the phone and help you file your return. Second, it includes attrition. So, the actual enforcement personnel is 5,000 LA Times * Mother Jones

- IRS backlog hits nearly 24 million returns, further imperiling the 2022 tax filing season

- ARPA Stimulus - you don't have to pay back 2020 overage on subsidies IRS.Gov *

- InsureMeKevin.com on subsidies & pay backs... 1.25.2022 update ARPA and 600% CA

- 1040 Instructions

- Overview FTB site

- How to Reconcile Subsidies FTB

- Calculate Pay Back

- Assistance Repaying California Subsidies

- covered ca.com/the most you might have to pay back

- 2022 Insure Me Kevin.com

- Our webpage on Form 8962 - Premium Tax Credit Subsidy Reconciliation

#Lose a job? How to keep coverage?

- I have lost my job at the xxx Club, and am unemployed for now. What can I do regarding my health insurance?

- Are you 1099 or W 2?

- You could apply for unemployment benefits. The Governor is waiving the one week waiting period.

- The benefits are taxable, so that would raise your expected annual MAGI income.

- Under the CARES act, unemployment pays 100% of lost wages!

- /cares-act/

- Flow Chart courtesy of Naked Capitalism

- Our page on 1099 workers

- Our webpage on PPP Loans

- Unemployment Page

- Under the new CARES Act responding to the COVID-19 pandemic, all states will be allowed to provide up to 13 additional weeks of federally funded extended benefits to people who exhaust their regular state benefits.

- Under the Act, through the end of this year, people who exhaust both regular and extended benefits, and many others who have lost their jobs for reasons arising from the pandemic but who are not normally eligible for UI in their state, are eligible for Pandemic Unemployment Assistance. People can receive a maximum of 39 weeks of benefits this year from all three sources combined. CBPP.org

- If you want to go for broke you probably could qualify for Medi Cal under the monthly income rule. We don’t get paid to help you with Medi Cal, so you can either go into your Covered CA Account and change your annual income… If it’s less than 138% and that would be about $18k for a single, Covered CA would get you into Medi Cal. Or, you can apply directly with Medi Cal.

- One downside is, that you may have a difficult time getting out of Medi – Cal. They want to grow and write everyone. IMHO it won’t be Medicare for All, but Medi Cal for all. They already write 1/2 of Californian’s. Medi Cal has a “secret” buzzword called Soft Pause, that no one seems to be able to hurdle!

- Here’s our quote engine to calculate FPL and subsidies.

- We currently have you down for $45k in annual income or let’s just say $4k/month. So, if you drop your annual income to say $40k, that would change your subsidy from $419/month to $468/month.

- If you think things will get real tough, you could drop your estimated income lower… When this tragedy is over and you’re earning $$$ again, you have to report to Medi Cal within 10 days or Covered CA within 30.

- I recently had someone tell me through their employer (hearsay) that Medi Cal may file criminal charges as they didn’t report the wife got a job. See more on that Q & A

- Some people did not take the full amount of the subsidy available, so they wouldn’t have a problem at tax time. One could change that.

- The tool to adjust the subsidy can be found my starting at the Enrollment Dashboard page.

- Then you would select My Eligibility History on the left hand side.

- On this page you will find the Plan Summary button once you select it the next page will display the Adjust Premium Tax Credit button.

- Since you are getting subsidies, there is technically a 90 day grace period.

- I am NOT in any way shape or form suggesting that you attempt to use it!!! If you get cancelled for non-pay, there is virtually NO F**ing way that you can get coverage till next January. I will NOT be responsible for anyone attempting to do that. IMHO Moses parting the Red Sea was easier than getting someone reinstated who has cancelled non pay.

- Sure, I’ve had people claim they just called the Insurance Company and it was no problem, but I don’t listen to hearsay.

- If you are not currently getting subsidies or don’t have insurance, check out all the new rules from Covered CA on special enrollment

- If you prefer to listen rather than read, scroll to the top of the page and watch the video.

- youtube.com

- Here’s another top rated well known experienced agent and his explanation

- youtu.be

- If you had coverage on the job, you could check out california-cal-cobra/If you are Medicare Eligible check our main webpage on Employer vs Medicare and the sub – child pages underneath.

Brother - Sister - Sibling Side Pages Subpages

View our website with your Desktop or Tablet for the most information

I was just approved to covered california.

However, the address on my file is completely wrong (completely different area of Cali).

I cannot figure out how to fix this on the website and their number doesnt work until Tuesday, which is another month!

What am I missing?

IMHO the Covered CA website is not intuitive…

Did Covered CA let you know that you can have a Professional, College & Industry Educated, Licensed Broker help you at no charge?

There are several ways on our appoint us as your agent page to do that. Then we can fix the problem right away. Just let us know the correct address. We will also check if it changes your premiums.

Considering it’s Memorial Day weekend, try appointing us as your broker by using the option of doing it through your Covered CA account

We spent several hours/days on the phone with them. It was extremely complicated and I’m not sure any insurance expert would even have expected or understood the insanity of covered ca’s process.

If you enjoy waiting on the phone for hours/days rather than just send us an email and we’ll take care of it, then we are probably not the agent for you.

Take a look at the Q & A on this page along with the resources on this website.

See the Q & A above about simplifying income when reporting a change to Covered CA

I’d don’t like the word “expert” but I love complicated stuff and I probably know more about Covered CA, than Covered CA does.

See our webpages on:

MAGI Income

IRS Form 8962 Tax Reconcilation at the end of the year

IMHO it doesn’t matter what Covered CA tells you now about your Income. It’s what the IRS says at the end of the year when you file taxes.

FAQ on how to avoid the trap of answering every question on calculating your income

Details of every kind of income & deduction, on our website including official IRS publications!

See our reference materials:

IRS Publication 974

Western Poverty Law

Don’t forget – Covered CA cannot give you legal or tax advice and even issued a memo on that

Please note too, that even if you prove in Court that Covered CA gave you the wrong tax advice, too much or too little subsidy or told you Social Security Income doesn’t count – Covered CA doesn’t have to reimburse you! Ask the Polk Family!

Thus, I won’t give you tax advice either, but I will show you were it says it in the tax code or an actual Covered CA or Insurance Company brochure

If you find ANY page on any other website that explains something better with a citation to the law or actual regulation than my page, just link to it in the comments are we have a bounty of $5/link!

Check our testimonials where numerous people that we’ve helped with Covered CA intricacies have THANKED us.

I probably understand Covered CA’s process than anyone there! Check out the appeal we just won!

Our son has obtained a Anthem policy through his employer with an 11/01 effective date. Seems as if it does not make sense to keep him on our policy and pay both premiums for next two months.

However, you never know with Covered CA-they may charge more with my son off and just my wife on the policy.

Are you able to check this without making a change?

The Tax Subsidy Calculation is a very complicated algebraic formula explained in Section 1.36 b. So, I just use the quote engine that I pay around $175/month for.

CCA [Covered CA] already informed me we can either

1. leave it as is or

2. drop him for Dec only.

Nov premium already paid.

Did the Phone Representative:

ever read the material above about the mandate to report changes within 30 days?

Tell you, that you should check out the tax consequences? free-help-vita/

Tell you that the Administrative Law Judge wanted to make Covered CA pay damages when they provided the WRONG advise?

Since your son has MEC Minimum Essential Coverage, sure he can have two policies, he won’t collect twice though there will NO LONGER BE SUBSIDIES FOR HIS PREMIUM and you will have to pay those back when you file taxes – Form 8962

You or a tax family member enrolled in health insurance coverage through Covered CA … not eligible for affordable coverage through an eligible employer-sponsored plan that provides minimum value or eligible to enroll in government health coverage – like Medicare, Medicaid, or TRICARE irs.gov/eligibility-for-the-premium-tax-credit

Hi,

I have been on the Covered California insurance (HealthNet) for the last several years.

However, my income level has increased some. So, the premium amounts forecasted through them for 2021 all appear quite high.

Is it less expensive to separate out from Covered California and just find health insurance directly?

Going from paying $187 per month to paying over $400 per month sounds a little steep.

I am not sure that my budget can afford it.

First thing to do is, use our quote engine, put in your income, age & zip code and then you can compare rates in Covered CA with possible subsidies or outside of Covered CA.

When the ACA passed, rates were supposed to be exactly the same in or out of Covered CA, with or without an agent.

Silver Level is different

Due to one of the many lawsuits on the constitutionality of ACA, the funding subsidies for Enhanced Silver went away.

What is your income now?

Are you self employed, it’s a tax deduction!

There is no extra charge for us to be your agent, if you stay with Covered CA see the link above to get instructions to appoint us. If you want Silver Benefits and go direct, just use OUR links on our website or the “add to cart” button in our quote engine.

I went on the Covered CA website the other day and tried to update things, but it would not let me.

My husband who was covered by Medicare passed away in April. Should I keep him on still because of tax filing for 2020? 2021,

I will be filing single vs. married, filing jointly.

If he should be removed because of a “qualifying event” and it might change my premium for 2021 for the better, please tell me how to remove him, and I will.

Also, my MAGI for 2020 will be significantly less (probably around $35,000 or maybe less) when I file taxes.

Whatever you think is best.

Thank you again,

Covered CA requires that changes be reported within 30 days See above for rules, documentation, etc.

When you file taxes, the subsidy gets reconciled. You might get back $$$ or you might have to pay back subsidies, if you were not entitled. https://individuals.healthreformquotes.com/covered-ca-tax-credits-subsidies-aptc/intro/premium-tax-credit-8962/

It’s difficult to tell someone how to do something in the Covered CA portal. Instructions are above. I can do it for you. I can do a video and show you want I did.

I’ll send you quotes privately for the premiums currently and next year with lower income and just one person in the household.

Here’s where web visitors can get quotes http://www.quotit.net/eproIFP/webPages/infoEntry/InfoEntryZip.asp?license_no=0596610

Here’s the income chart https://individuals.healthreformquotes.com/covered-ca-tax-credits-subsidies-aptc/magi/income-chart/

Here’s your current premium at $45k married filing jointly

Here’s premium and subsidy at #35k single

Email me privately if you want me to make the changes for you in your account.

I changed employers, can I switch from Bronze to Silver?

**********

Only if there is a change in income, that changes subsidies or silver level. See explanation above and the main special enrollment page.

Please explain the 30 day requirement to notify Covered CA of a change in income. 30 days from what?

See excerpt of law above. Enrollee’s Duty to Report Changes in Circumstances