Evidence of Coverage EOC

The FULL Policy in PLAIN English!

Introduction

So many questions are answered right in the Full Policy the evidence of coverage – EOC, in

- PLAIN English, as mandated by law.

- Along with your duty to read the policy!

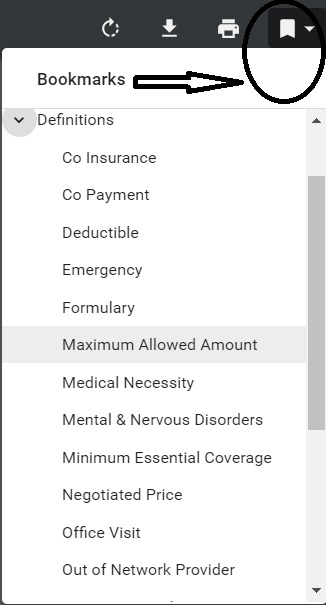

Sure beats reading the law and then trying to see for sure if the law applies to you. When you have your actual EOC, a couple of easy ways to find stuff in the policy is the bookmarks, table of contents and the search feature.

The Evidence of Coverage (EOC) is a document that describes in detail the health care benefits covered by the health plan. It provides documentation of what that plan covers and how it works, including how much you pay. The EOC can also refer to a certificate or contract provided to a health plan member that contains information about coverage and other rights. National Disability Rights *

Here’s where to find your EOC Evidence of Coverage for:

- Individual & Family Plans

- Employer Group Plans

- Medi-Cal

- Medicare Advantage Co Ordination Plan –

- Email us if you are in CA and have any questions.

- JUMP TO SECTION ON:

Specimen Individual Policy #EOC with Definitions

Employer Group Sample Policy

It's often so much easier and simpler to just read your Evidence of Coverage EOC-policy, then look all over for the codes, laws, regulations etc! Plus, EOC's are mandated to be written in PLAIN ENGLISH!

- Find your own Individual EOC Evidence of Coverage

- It' important to use YOUR EOC not just stuff in general!

- Obligation to READ your EOC

- Plain Meaning Rule - Plain Writing Act

- Our Webpage on Evidence of Coverage

- OOP Out of Pocket Maximum - Many definitions are explained there.

VIDEO Steve Explains how to read EOC

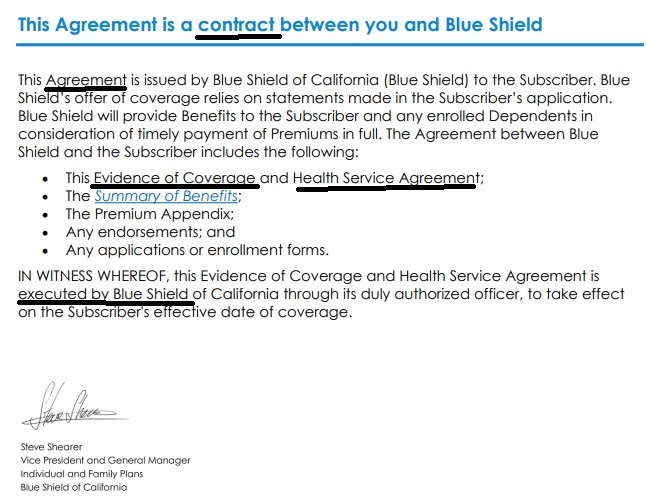

The EOC Evidence of Coverage is the CONTRACT #between you and the Insurance Company

Every policy has a written Evidence of Coverage (EOC). The EOC is your guide to what is covered and what is excluded, how much you will pay depending on the circumstances, what your cost sharing will be, and other information about using your coverage. Keep this document handy for when you have questions about your policy. Insurance.CA.Gov *

![]()

#Covered CA Certified Agent

No extra charge for complementary assistance

- Appoint us as your broker

- Get Instant Health Quotes, Subsidy Calculation & Enroll

- Videos on how great agents are

Must #read your policy

A court “must hold the insured bound by clear and conspicuous provisions in the policy even if evidence suggests that the insured did not read or understand them.”

- property casualty 360.com/is-there-a-duty-to-read-insurance-contracts

- IRMI duty to read

- Is there a duty to read? Hastings College of Law

- Fordham Law Review Duty to read a changing concept 1974

- Kenny & Sams Law Firm

The Hadlands, having failed to read the policy and having accepted it without objection, cannot be heard to complain it was not what they expected. Their reliance on representations about what they were getting for their money was unjustified as a matter of law.Sarchett v. Blue Shield of California (1987) 43 Cal.3d 1, 15, 233 Cal.Rptr. 76, 729 P.2d 267

Hadland v. NN Investors Life Ins. Co. (1994) 24 Cal.App.4th 1578 , 30 Cal.Rptr.2d 88(Findlaw.com requires free registration)

STORY of what happened in this lawsuit

In the fall of 1985, the Hadland’s were notified of a 10 percent increase in the premiums for their health insurance under a policy with Reliance Standard Life Insurance Company. The Reliance major medical policy paid 80 percent of medical and hospital expenses, subject to a $250 deductible. The Hadland’s began to look for less expensive coverage. When they received a mailing from NASE describing low-cost group hospital insurance available to NASE members through NN, they sent in a postcard asking for further information. Kevin Winn, associated with NASE, NN and United Group Association (UGA) (a company that markets NN insurance), contacted the Hadland’s and, on December 5, came to their place of business to make a sales presentation. According to the Hadland’s, Winn told them coverage under the NN policy was “as good if not better” than coverage under the Reliance policy, at half the premium cost. Promotional materials described the policy as offering major hospital benefits. The Hadland’s joined NASE and applied for NN coverage. As it turned out, the NN policy was, as Winn had stated, half as expensive as the Reliance policy, but it did not cover most outpatient medical expenses. Moreover, NN’s benefits were paid according to a maximum benefit schedule which, in some cases, covered less than 50 percent of the actual charge for a surgical procedure. For instance, the maximum surgical benefit available under the policy was $6,000, regardless of the actual cost, and the maximum hospital room and board benefit for nonintensive care was $300 a day.

In January 1986, the Hadland’s received a certificate of insurance indicating their coverage benefits under the NASE group policy. In an attached letter, they were asked to read the certificate and call the NN office if they had any questions. The first page of the certificate advised them that if the policy did not meet their needs, they could return it within 10 days for a full refund. fn. 1 NN sent the Hadland’s a second letter to confirm their receipt of the certificate and to ask them to contact the insurer if they had any questions concerning coverage. The Hadland’s did not read the insurance contract. In November, Mary Jane Hadland was hospitalized for a surgical procedure. She incurred nearly $26,000 in medical and hospital bills. NN paid less than one-half, which, the Hadland’s concede, was the total of benefits due under the policy.

To take their fraud cause of action to the jury, the Hadland’s had to prove not only defendants’ false representations, but their own justifiable reliance

‘A reasonable person will read the coverage provisions of an insurance policy to ascertain the scope of what is covered. [Citation.]’ … Generally the insured is ‘bound by clear and conspicuous provisions in the policy even if evidence suggests that the insured did not read or understand them.’

NN (NASE prior Insurance Company) policy’s schedule of benefits expressly provided, for instance: an entirely unambiguous maximum surgical benefit of $6,000, regardless of whether the surgery consisted of an organ transplant, a partial or radical mastectomy or the amputation of a toe; [FN12] a maximum nonintensive care hospital room and board benefit of $300 a day; and a maximum benefit of **95$300 a day for outpatient hospital charges. The Reliance (the company the Hadland’s had before NASE) policy provided unqualified benefits of 80 *1589 percent of covered expenses. Thus, any representations by defendants of “full protection” under the NN policy, or coverage “as good or better” as the Reliance policy, were patently at odds with the express provisions of the written contract. If the Hadland’s had read it, they would have discovered its limitations, rejected it, and continued to pay the higher premium for the increased security of Reliance’s more comprehensive coverage.

View Entire Case on Findlaw.com Hadland v. NN Investors Life Ins. Co.

(NASE’s prior Carrier, as pointed out by UICI’s 4/6/2006 letter) This case shows that one must read the ACTUAL policy and can’t rely on Agent’s statements or brochures. There are some exceptions… This doesn’t just apply to NASE, but to ANY Insurance Contract. See attorney Keler.com for more explanation.

Plain Language – Read Policy THREE times

Guide to #Contract Interpretation

- Read the Statute – Policy

- Read the Statute – Policy

- Read the Statute – Policy

- Then when you think you understand it, read it again

- Plain Language Video

- Tools to Read a Statute VIDEO

- Contract Interpretation in California: Plain Meaning, Parol Evidence and Use of the Just Result Principle

Our webpage on

- jiggery pokery and contract interpretation

- Evidence of Coverage EOC

- Plain Meaning Rule - How to read Policy - Contract

Major Insurance Company

Asserting the #Wrong Answer!

I just let my contract go with a certain well know and respected Insurance Company, as their RSM Regional Sales Manager told me THREE times, that I couldn’t write a medi-gap plan for someone whose MAPD plan non renewed. Even though I emailed her the official proofs. She even kept this up at a sales meeting and told the other agents there the same thing.

When my client complained as I suggested to the CA Department of Insurance, the Insurance Company denied responsibility as they said they never received an application. They didn’t mention anything about telling their agent that he would be wasting his time sending it in.

Email chain available on request. I have this posted as I’m mandated to report ethical issues.

#Advocates Guide to Surprise Medical Bills

- Hidden Cost of Surprise Medical Bills 3.3.2016 Time Magazine

- heart bypass surgery, replacement of one valve and repair of another. raging infection that required powerful IV antibiotics to treat. spent a month in the hospital, some of it in intensive care, before she was discharged home.

- surprise: Bills totaling more than $454,000 for the medical miracle that saved her life. Of that stunning amount, officials said, she owed nearly $227,000 after her health insurance paid its part. Time.com 3.21.2019 *

- heart bypass surgery, replacement of one valve and repair of another. raging infection that required powerful IV antibiotics to treat. spent a month in the hospital, some of it in intensive care, before she was discharged home.

- true cost of healthcare.org 82 pages pdf

- Newscast about Hospitals being required to post rates - charges VIDEO

- PBS Trump Price Transparency Executive Order VIDEO

- Our webpage on Balance Billing & No Surprises

- Americans often "forced" to pay medical bills they don't owe, feds say CBS News

- Colorado's Supreme Court has ruled in favor of a woman who expected to pay about $1,300 for spinal fusion surgery but was billed more than $300,000 by a suburban Denver hospital that allegedly included charges it never disclosed she might be liable for. Read more: CBS News 5.19.2022

- What the Federal ‘No Surprises Act’ Means in California

- CA Department of Insurance Summary

Term Life Quote #naaipquote

- Set up Schedule a phone, skype or face to face consultation

- Tools - Calculator to help you figure out how much you should get

Life Insurance Buyers Guide

How much life insurance you really need?

Please complete & return

- Short ONE page form - CPS

and we'll search and consult for you.

Free Look Period #view FULL Policy – E O C (Evidence of Coverage) when you purchase Health Insurance and full return privileges’

California Insurance Code §10276.

Every individual accident and health policy or contract, except single premium nonrenewable policies or contracts, issued for delivery in this state on or after July 1, 1962, by an insurance company, nonprofit hospital service plan or medical service corporation, shall have printed thereon or attached thereto a notice stating that the person to whom the policy or contract is issued shall be permitted to return the policy or contract after its delivery to the purchaser and to have the premium paid refunded if, after examination of the policy or contract, the purchaser is not satisfied with it for any reason.

The period time set forth by the insurer, nonprofit hospital service plan or medical service corporation for return of the policy or contract shall be clearly stated on the notice and such period shall not be less than 10 days nor more than 30 days. The policyholder or purchaser may return the policy or contract to the insurer, plan or corporation at any time during the period specified in the notice. If a policyholder or purchaser pursuant to such notice, returns the policy or contract to the company or association at its home or branch office or to the agent through whom it was purchased, it shall be void from the beginning and the parties shall be in the same position as if no policy or contract had been issued. California Insurance Code §10276.

Check your evidence of coverage for the exact provisions!

Covered CA has a different Opinion. IMHO they are in violation of law!

See § 155.430 * Termination of Exchange enrollment or coverage

(b)Termination events –

(1)Enrollee-initiated terminations.

(i) The Exchange must permit an enrollee to terminate his or her coverage or enrollment in a QHP through the Exchange, including as a result of the enrollee obtaining other minimum essential coverage. To the extent the enrollee has the right to terminate the coverage under applicable State laws, including “free look” cancellation laws, the enrollee may do so, in accordance with such laws.

FAQs “30 Day Free Look – Right to view EOC”

The law says to return the policy.

They never sent one. I didn’t get any. They play a game that they sent it. I can’t review it. Its been 21 days. They say I will now get a refund less 150.

That is not the same position I was in when I started.

Why do you publish the 1962 law.

It’s not just the law, but the EOC Evidence of Coverage should state the same provision, in plain English.

Who is “They?”

We don’t like hearsay evidence!

You might want to file a grievance.

Are “They” subject to the provisions of this law?

Did you have a special enrollment period?

I’m curious, paid for Cobra on for May on 6/30 and was told I cannot get a refund because its past 7 days. There was a holiday and the weekend, so I called today 7/8 twice to speak with a supervisor and was told “They didn’t have one available” .

Is there not a 30 day free look period?

3rd How about getting an individual plan with us. Get quotes here.

4th The free look from my reading and you’re welcome to check with legal counsel says it’s only for INDIVIDUAL plans. COBRA and Cal COBRA are group plans, as best I can determine.

Do you have a copy of your Evidence of Coverage?

When did you receive your policy?

Why did it take so long for you to pay your May premium?

InsuBuy International Medical Coverage –

Instant Quotes & Enrollment

I had some doubts regarding the policy details, whom should i contact ?

Are you talking about the actual policy itself or some aspect of Covered CA subsidies?

Which policy? What Insurance Company? What details? What doubts? See links above to find the EOC Evidence of Coverage for each company.

Are you willing to appoint us as your Covered CA broker, no additional charge? We only get compensated when a web visitor appoints us. Covered CA doesn’t pay us unless we do.

Take a look at our website, use the google search feature above. We believe with 20 years working on this website, everything one could ever ask is here.

If you find something on another website that should be here… Post it on the relevant page and we pay $5/relevant useful post.

Hello Steve,

Under our current plan, the co-pay is separated into two categories for the benefits:

1) Facility $50/visit

2) Professional $25/visit

Can you pls [please] advise/explain what is considered facility & professional?

We’ve called Anthem direct, however, all the reps seem to have different understandings for both.

Best Regards,

Justine H

This type of technical question is the very reason we’ve posted a sample copy of the full EOC – Evidence of Coverage. It’s the full contract between the insurance company and you. In addition to the bookmarks, use the search feature, to look for your keywords, like facility, professional & visit.