What What does OOP Out of Pocket Maximum, Calendar Year Deductible, co payment, co-insurance, mean in Health Insurance?

Try turning your phone sideways to see the graphs & pdf's?

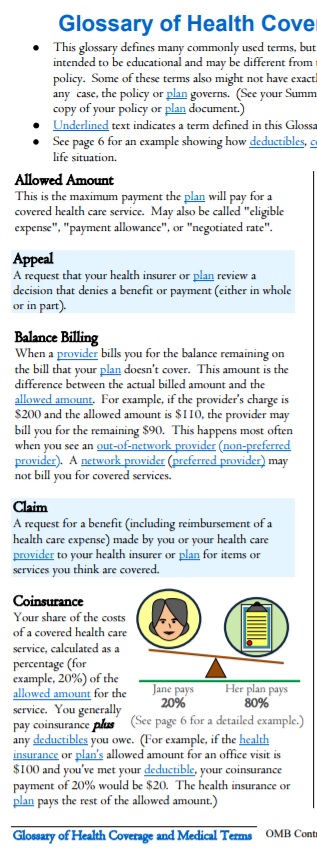

#OOPChart

How the Out of Pocket Maximum Works in Health Insurance

Video On Maximum OOP Out of Pocket

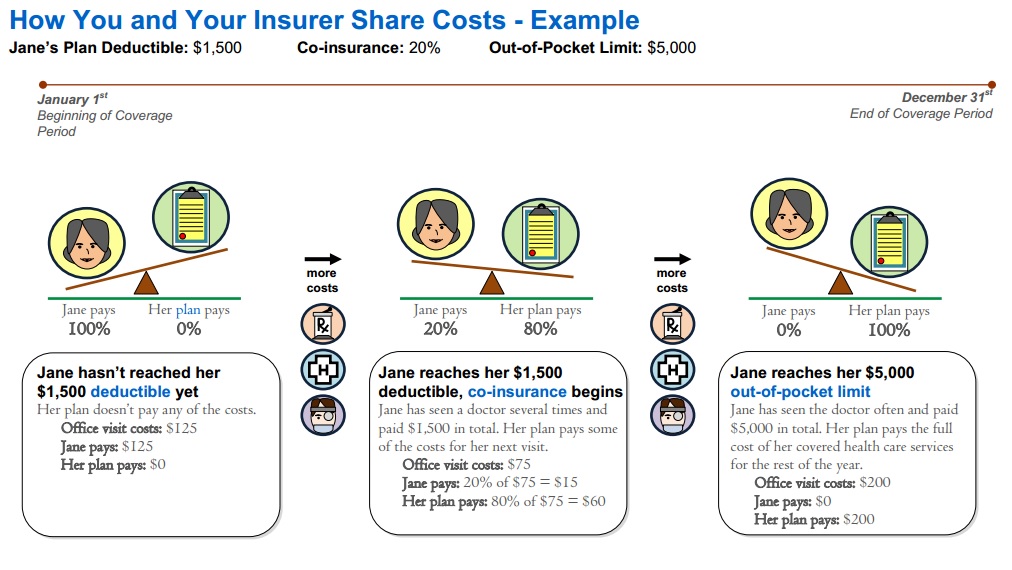

- Graph Source Health Net Glossary Page 6

- Get quotes, subsidies, net premium, deductibles, co-pays, OOP Out of Pocket maximum from all Individual companies * Employer Group

- Provider Finder See also our Site Map for instructions & details on each companies provider finder

- Glossaries – Dictionaries

-

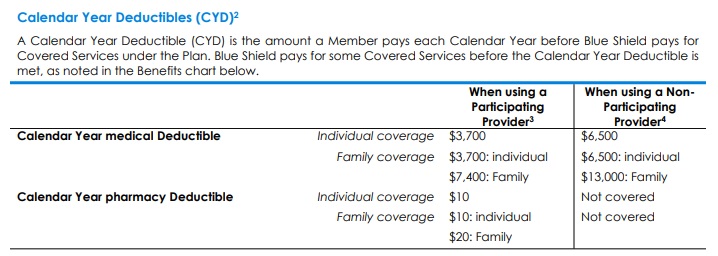

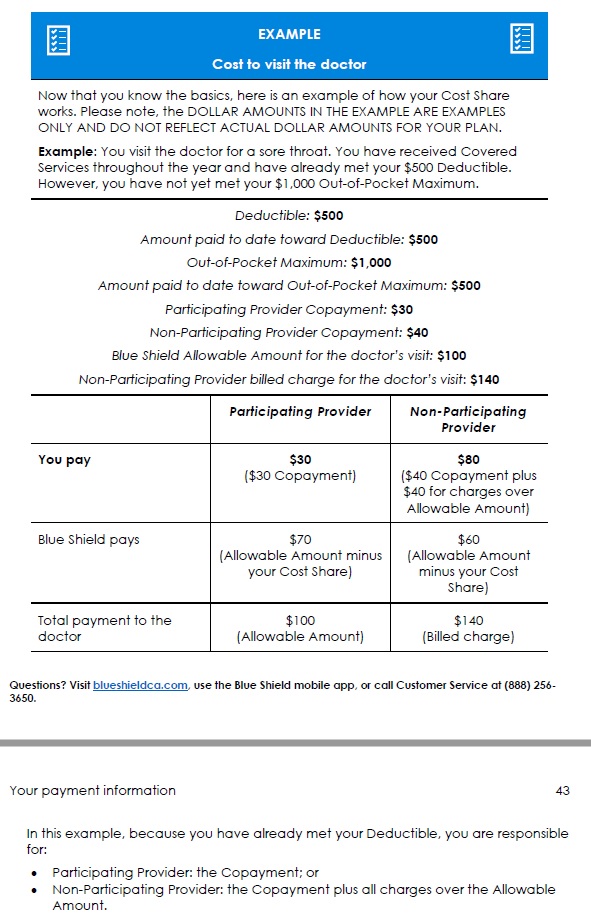

Calendar Year Deductible

- amount you must pay for specific Covered Services before the plan pays for Covered Services pursuant to this [policy] Agreement. Learn more Deductible & Co Pay

- Copayment The specific dollar amount that a Member is required to pay for Covered Services after meeting any applicable Deductible.

- Learn more Co Pays

- Coinsurance The percentage amount that a Member is required to pay for Covered Services after meeting any applicable Deductible.

- Learn more Co-insurance

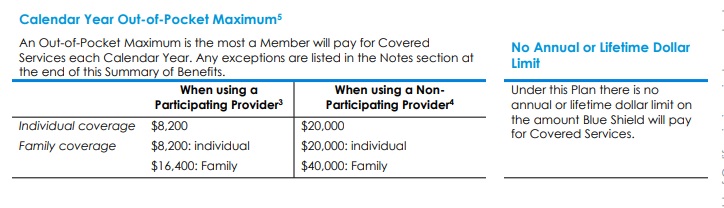

- Out-of-Pocket Maximum OOP The highest Deductible, Copayment, and Coinsurance amount an individual or Family is required to pay for designated Covered Services each year as indicated in the Summary of Benefits section. Charges for services that are not covered, charges in excess of the Allowable Amount or contracted rate do not accrue to the Calendar Year Out-of-Pocket Maximum. Sample EOC Page 107

- Maximum Out of Pocket OOP will go down in 2022 Learn More: AARP * Mercer *

- Video On Maximum Out of Pocket

- ACA’s Maximum Out-of-Pocket Limit Is Growing Faster Than Wages KFf

- Patients often can’t afford to pay off what their insurance leaves behind

- Definitions Health Insurance Terms VIDEO

- Breaking Down Covered California Health Plans By Coverage Sections Insure Me Kevin . com

- FAQs / Ask Us a Question

-

#Deductible s Calendar Year & Co Pays

Deductible – The Calendar Year amount you must pay for specific Covered Services before the plan pays for Covered Services pursuant to this [policy] Agreement. Sample EOC Page 107

Example from 2022 Silver 70 PPO

See evidence of coverage – Cost concepts in action 2024 Page 42

- Deductibles in ACA Marketplace Plans, 2014-2024

- FAQs / Ask Us a Question

#Co-Payments – Specific Covered Services

Footnote #2 Calendar Year Deductible (CYD):

Calendar Year Deductible explained. A Calendar Year Deductible is the amount you pay each Calendar Year before Blue Shield pays for Covered Services under the Plan.

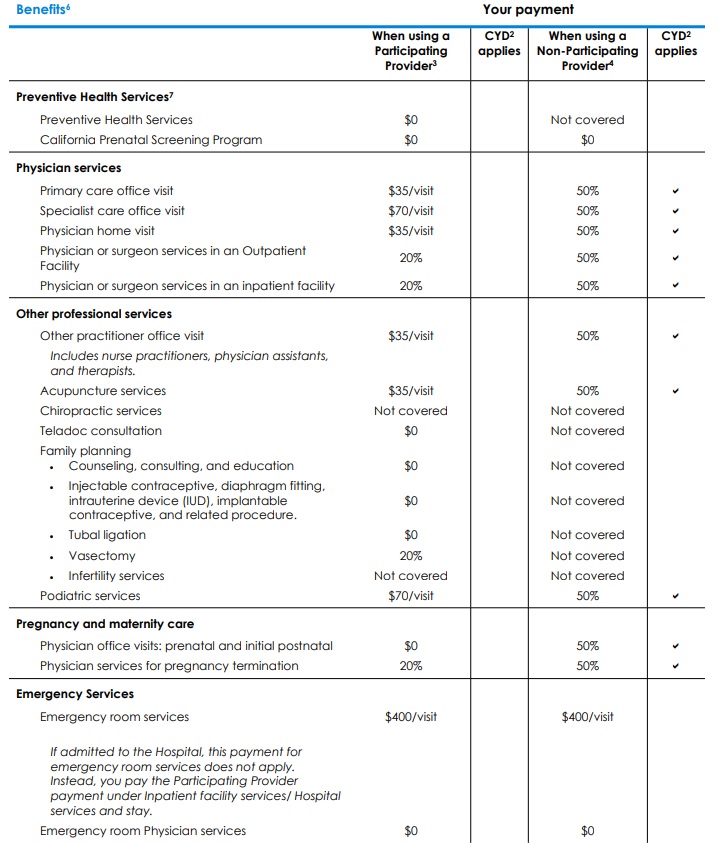

If this Plan has any Calendar Year Deductible(s), Covered Services subject to that Deductible are identified with a check mark () in the Benefits chart above.

Covered Services not subject to the Calendar Year medical Deductible. Some Covered Services received from Participating Providers are paid by Blue Shield before you meet any Calendar Year medical Deductible. These Covered Services do not have a check mark () next to them in the “CYD applies” column in the Benefits chart above.

This Plan has a separate medical Deductible and pharmacy Deductible.

This Plan has a separate Participating Provider Deductible and Non-Participating Provider Deductible.

Family coverage has an individual Deductible within the Family Deductible. This means that the Deductible will be met for an individual with Family coverage who meets the individual Deductible prior to the Family meeting the Family Deductible within a Calendar Year. Any amount you have paid toward the individual Deductible will be applied to both the individual Deductible and the Family Deductible. Once the individual Deductible or Family Deductible is reached, cost sharing applies until the Out-of-Pocket Maximum is reached.

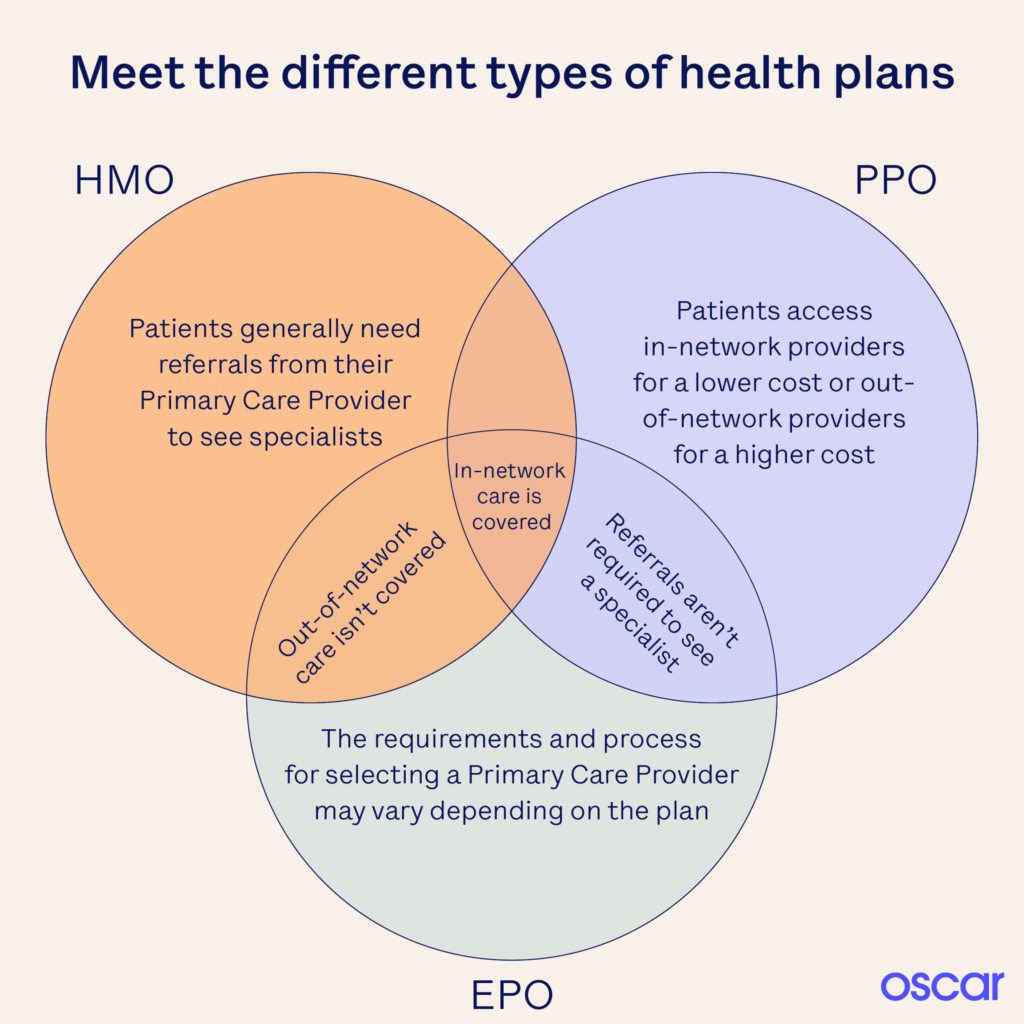

HMO – PPO – EPO

- Learn More – Oscar Explanation

- Provider Finder See also our Site Map for instructions & details on each companies provider finder

- ‘Father Of The HMO’ Dies At 95; Idea Didn’t Turn Out Like He Envisioned KFF

#CoInsurance

Coinsurance The percentage amount that a Member is required to pay for Covered Services after meeting any applicable Deductible. VIDEO

Out-of-Pocket Maximum

The OOP Out of Pocket Maximum is The highest Deductible, Copayment, and Coinsurance amount an individual or Family is required to pay for designated Covered Services each year as indicated in the Summary of Benefits section.

Charges for services that are not covered, charges in excess of the Allowable Amount or [negotiated] contracted rate do not accrue to the Calendar Year Out-of-Pocket Maximum.

Allowable Amount – See page 105 of Specimen Policy

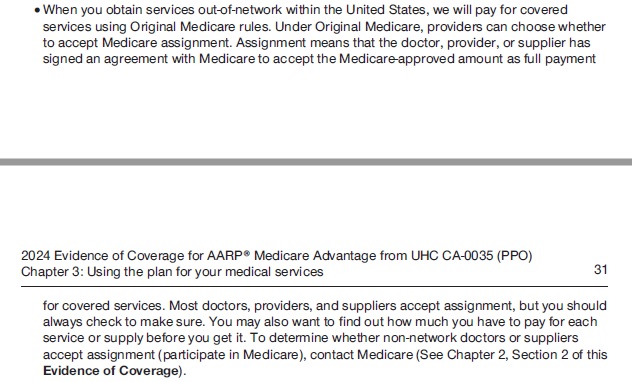

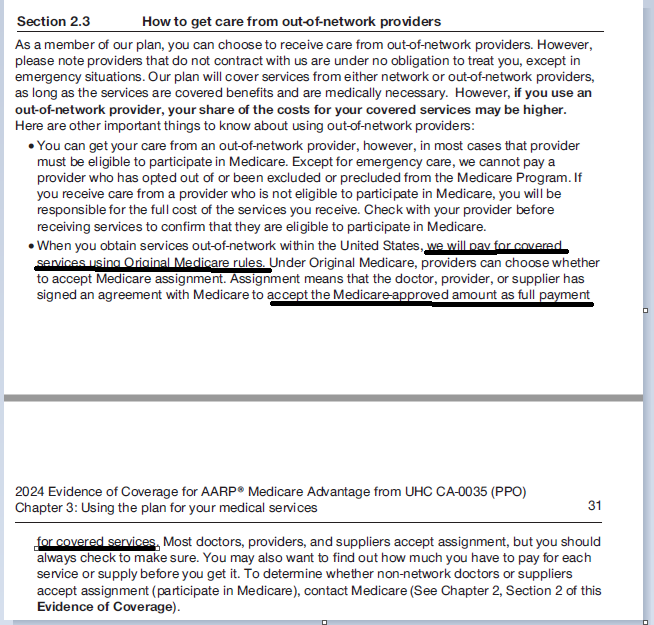

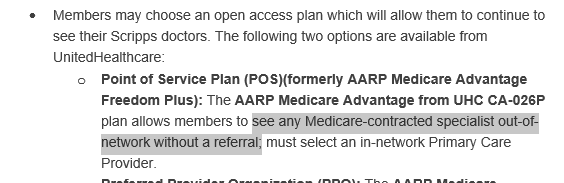

How much gets #paid to an out of network provider?

How Your In-Network Health Coverage Can Vanish Before You Know It CA Health Line

Question? Scripps is no longer taking Medicare Advantage Plans, per their website. If you have a Medicare Advantage Plan MAPD PPO, will the PPO pay, how much and will Scripps take it?

Answer – Scripts states they take Medicare A & B on their website. The PPO pays the same benefits as A & B, thus it looks to me like the PPO will pay and Scripps should take it. Call to double check

800-727-4777. I’d email them, but I don’t find an email address. I don’t post or listen to hearsay. If you call, PLEASE get it in writing!

- See our webpage on Medicare Assignment.

- Sample MAPD Advantage EOC Evidence of Coverage.

- Email us about the Broker only explanation from UHC on options.

![]()

Specimen Individual Policy #EOC with Definitions

Employer Group Sample Policy

It's often so much easier and simpler to just read your Evidence of Coverage EOC-policy, then look all over for the codes, laws, regulations etc! Plus, EOC's are mandated to be written in PLAIN ENGLISH!

- Find your own Individual EOC Evidence of Coverage

- It' important to use YOUR EOC not just stuff in general!

- Obligation to READ your EOC

- Plain Meaning Rule - Plain Writing Act

- Our Webpage on Evidence of Coverage

- OOP Out of Pocket Maximum - Many definitions are explained there.

VIDEO Steve Explains how to read EOC

Insurance #definitions & glossary

- The best place to look for Insurance definitions & glossary is in an actual EOC – Evidence of Coverage (specimen – Platinum) – Policy. Be sure to check your ACTUAL EOC for your specific question.

- CA Dept of Insurance Glossary

- CMS – Medicare

- Medicare Part D Rx Guide Definitions # 11109

- CA Health Care Advocates Glossary

- Health Net 6 page glossary

- aw.com

- CA Court Site Glossary

- Medi-Cal – Helpful words to know

- Texas DOI Glossary

- Glossary of Employee Benefit Terms See the Benefits.com

- FAQs / Ask Us a Question

(Chinese)

(Chinese)

Notification of OOP Out of Pocket Maximum

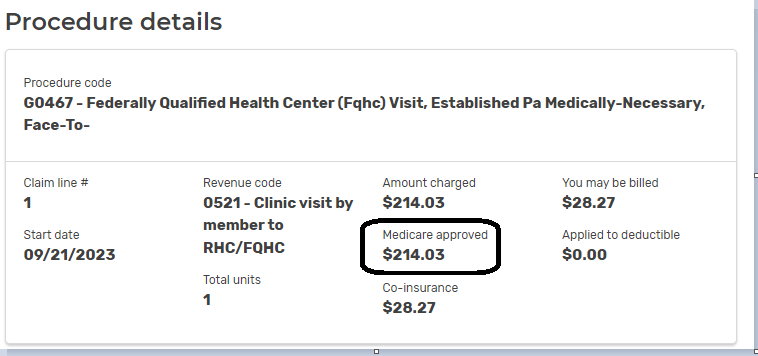

Explanation of Benefits

- SB 368, requires most state-regulated private-sector health plans to send enrollees updates, an EOB Explanation of Benefits for every month in which they received care, showing how much they have paid toward their annual deductible — the amount a person must shell out before insurance begins to cover most of their care — and how close they are to reaching out-of-pocket limits, the amount after which the insurer pays for 100% of care. CA Health Line.org *

Our Webpage on

#Advocates Guide to Surprise Medical Bills

- Hidden Cost of Surprise Medical Bills 3.3.2016 Time Magazine

- heart bypass surgery, replacement of one valve and repair of another. raging infection that required powerful IV antibiotics to treat. spent a month in the hospital, some of it in intensive care, before she was discharged home.

- surprise: Bills totaling more than $454,000 for the medical miracle that saved her life. Of that stunning amount, officials said, she owed nearly $227,000 after her health insurance paid its part. Time.com 3.21.2019 *

- heart bypass surgery, replacement of one valve and repair of another. raging infection that required powerful IV antibiotics to treat. spent a month in the hospital, some of it in intensive care, before she was discharged home.

- true cost of healthcare.org 82 pages pdf

- Newscast about Hospitals being required to post rates - charges VIDEO

- PBS Trump Price Transparency Executive Order VIDEO

- Our webpage on Balance Billing & No Surprises

- Americans often "forced" to pay medical bills they don't owe, feds say CBS News

- Colorado's Supreme Court has ruled in favor of a woman who expected to pay about $1,300 for spinal fusion surgery but was billed more than $300,000 by a suburban Denver hospital that allegedly included charges it never disclosed she might be liable for. Read more: CBS News 5.19.2022

- What the Federal ‘No Surprises Act’ Means in California

- CA Department of Insurance Summary

Prior #Authorization

Preauthorization is A decision by your health insurer or plan that a health care service, treatment plan, prescription drug or durable medical equipment (DME) is medically necessary. Sometimes called prior authorization, prior approval or precertification.

Your health insurance or plan may require preauthorization for certain services before you receive them, except in an emergency. Preauthorization isn’t a promise your health insurance or plan will cover the cost. Health Net Glossary * See also YOUR EOC, Evidence of Coverage!

IMHO Insurance Companies are not doctors and a lot of people and reglators agree, thus the pending laws and investigations.

- Prior Authorization – Regulatory Investigation aka “preauthorization” and “precertification” KFF.org 5.20.2022

- AMA: Insurers not sticking to prior authorizations deal from 2018 Modern Health Care 5.24.2022

- California Senate Bill 250 * Senator Pan would require that insurers consult with doctors on which services require authorizations, streamline the process, less paperwork and allow patients to get the care they need faster.

- SB 250 would require health plans to exempt physicians from prior authorization rules if they have practiced within the plan’s criteria 80% of the time. CMA.Docs.org

- PRIOR AUTHORIZATION REQUIREMENTS HALTED FOR CERTAIN SERVICES

- Parody If Health Care was honest

Resources, Links & Bibliography

- cal matters.org/new-bill-pushes-insurers-to-stop-playing-doctor

- Payer Denial Tactics — How to Confront a $20 Billion Problem

- cal matters.org/richard-pan

- cma docs.org/prior-authorization-bill

- Plaintiff whose insurer delayed surgery is awarded $14 million over opioid dependency

Prior Authorization in Medicare Advantage Plans: How Often Is It Used?

Independent Medical #Review (IMR) Program

VIDEO's

DMHC Help Center & Independent Medical Review VIDEO

An Independent Medical Review (IMR) is where expert independent medical professionals review specific medical decisions made by the insurance company. The California Department of Insurance (CDI) administers an Independent Medical Review program that enables you, the insured, to request an impartial appraisal of medical decisions within certain guidelines as specified by the law.

Health insurer delayed her MRI. Meanwhile, the cancer that would kill her was growing.

An IMR can be requested only if the insurance company’s decision involves:

- The medical necessity of a treatment,

- An experimental or investigational therapy for certain medical conditions, or

- A claims denial for emergency or urgent medical services.

It is important to note that the IMR process cannot be used for an insurance company decision that is based on a coverage issue. Only decisions regarding a disputed health care service, as it relates to the practice of medicine, that do not involve a coverage issue are qualified for the IMR program.

You are required to exhaust the internal appeals/grievance process of your particular insurance company before applying for an IMR with the CDI. Click here to read full article on Department of Insurance Website

- IMR on CA Department of Insurance Website

- What Is an Independent Medical Review?

- Who Can Request an Independent Medical Review?

- When Can an Independent Medical Review Be Requested?

- What Issues Are Eligible for an Independent Medical Review?

- What Issues Are Not Eligible for an Independent Medical Review?

- How Does the Independent Medical Review Program Work?

- What Are the Criteria Used in an Independent Medical Review Determination?

- Is There a Way to Process an Independent Medical Review More Quickly in Extraordinary Circumstances?

- Will an Independent Medical Review be Costly?

- Does Independent Medical Review Participation Prevent Future Legal Action?

- Are Medical Records Kept Confidential in the Independent Medical Review Process?

- How Do I Request an Independent Medical Review from the California Department of Insurance?

- Health Insurance Terms and Phrases

- The California Department of Managed Health Care (DMHC) The DMHC regulates HMOs and some PPOs in California – Try using the Insurance Company procedure first

- Complaint Form & IMR

- 1-888-HMO-2219

- [email protected]

- Contact Form

- CA Department of Insurance

- IMR – Independent Medical Review

- ONLINE complaint form insurance.ca.gov/complain

- Magellan Mental Health

- Policy Statement

- Magellan* provides procedures for the expeditious processing of requests for external appeal of adverse determinations through an Independent Review Organization as required by applicable law or customer contract.

- Purpose

- To establish standards to assure independent and timely review of disputed health care services to assure that appropriate, beneficial treatment interventions are made available to members. Magellan Mental Health

- National Health Law Program 12 page pdf on Internal Grievances & External Review in Service Denials in Covered CA Plans

- Milliman Waste Study

- Sections 10169 through 10169.5 of the California Insurance Code (CIC), which became effective January 1, 2001, explain the IMR process in detail. In addition, Section 10145.3 explains the IMR process as it relates to experimental or investigational therapies.

Our Web Pages on

- Medical Necessity – reasonable and necessary Independent Medical Review

- Appeal & Grievances? Medicare – Medi Cal – Covered CA

Brother - Sister - Sibling Side Pages Subpages

View our website with your Desktop or Tablet for the most information

UCR Reasonable and customary amount

“the UCR usual, customary, and reasonable amount,” and “the prevailing rate” are among the standards that various health care benefit plans may use to pay out-of-network benefits. Before ACA/Obamacare and the rise of HMO’s UCR was quite common.

Please review this page more details and explanations of each of the key terms as they are interrelated.

Comments FAQ’s

Ask Us a Question

News reports about how high deductibles leave people effectively without medical care as people are living on the edge – paycheck to paycheck.

- Los Angeles Times May 2, 2019 * May 2 3 Kids $15k Medical Debt *

- NPR May 3, 2019

- New York Magazine.com 5.3.2019

- North County Public Radio 5.3.2019

- How to figure out the Family Deductible & OOP? Insure Me Kevin.com

- Soaring insurance deductibles and high drug prices hit sick Americans with a ‘double whammy’ LA Times

- Learn about Embedded vs aggregate deductible

- How might an HSA Health Savings Account help you save up to pay the deductible?

- FAQs / Ask Us a Question

Deductible #Carryover.

Many plans used to offer a provision called a deductible carryover. However, Last quarter deductible carry over has gone by way of the dinosaurs – carriers no longer offer this.

This provision allows you to carry over to the next year any unmet portion of the deductible that you, or your family, run up in October, November and December. For example, assume you had no medical claims in the first part of the year. In November, you run up $350 worth of claims. If your deductible was $500, you would start the next year with $350 of your $500 deductible already meet. Example

However, there is no deductible credit for PPO plans since all plans are set up for Calendar Year and a renewal won’t effect this nor a carrier change in the middle of the year since deductible credit for the yearly medical deductible is given by the new carrier (client has to submit EOBs) 9.11.2015 email from Heide Definition – Investopedia LISA Broker Wholesaler – How and what you need to do to get credit when moving from one insurance company to the other.

Benefit Period

The length of time we will cover benefits for Covered Services. For Calendar Year plans, the Benefit Period starts on January 1st and ends on December 31st. For Plan Year plans, the Benefit Period starts on your Group’s effective or renewal date and lasts for 12 months. (See your Group for details.) The “Schedule of Benefits” shows if your Plan’s Benefit Period is a Calendar Year or a Plan Year. If your coverage ends before the end of the year, then your Benefit Period also ends. EOC

Crediting Prior Employer Group Plan Coverage

If you were covered by the Group’s prior carrier / plan immediately before the Group signs up with us, with no break in coverage, then you will get credit for any accrued Deductible, if applicable and approved by us, under that other plan. This does not apply to people who were not covered by the prior carrier or plan on the day before the Group’s coverage with us began, or to people who join the Group later. If your Group moves from one of our plans to another (for example, changes its coverage from HMO to PPO), and you were covered by the other product immediately before enrolling in this product with no break in coverage, then you may get credit for any accrued Deductible, if applicable and approved by us. If your Group offers more than one of our products, and you change from one product to another with no break in coverage, you will get credit for any accrued Deductible, if applicable. This Section Does Not Apply To You If:

· Your Group moves to this Plan at the beginning of a Benefit Period; · You change from one of our individual policies to a group plan; · You change employers; or · You are a new Member of the Group who joins the Group after the Group’s initial enrollment with us.

What’s this about #embedded & aggregate deductibles?

Individual vs Family Deductibles?

Under family coverage, an embedded deductible is the individual deductible for each covered person, embedded in the family deductible. While it might not sound like a good thing to have two deductibles, it actually works to provide better coverage for individual members because once each family member meets his or her embedded deductible, health insurance begins paying for covered services, regardless of whether the larger family deductible is met.

Contrast this to a non-embedded deductible, also referred to as an aggregate deductible. Under an aggregate deductible, the total family deductible must be paid out-of-pocket before health insurance starts paying for the health care services incurred by any family member. While family coverage with an aggregate deductible may have a lower monthly premium, coverage won’t kick in until the total family deductible is met. In contrast, family health plans with an embedded deductible may help ensure that there is coverage for individual family members once they meet their embedded deductible, regardless of whether the family deductible is met. Unfortunately, the Summary of Benefits and Coverage won’t necessarily tell you if the deductible is embedded or not; you may have to call the plan to learn how the deductible will be applied for your coverage. Learn More⇒ Center on Health Insurance Reforms AB 1305

If two or more on a policy it’s the Family Deductible NOT individual, with a family max?

See excerpt of Blue Cross Bronze HSA Page 55 on Family or Individual Deductible

NEW for 2016!!! Embedded – HSA plans had an aggregate deductible where one person could meet the entire family deductible. Now a family member will not be charge more than the individual deductible and be able to receive benefits sooner. BC RSM Email 9.29.2015 SHRM.org AB 1305 2015 Bonta

2017 NEW Laws & Regulations effective 1.1.2017 AB 1305, 339 & 1954 SB 999 – Deductible & OOP Maximums FAQ’s

What is the Maximum that can be contributed to an HSA – Health Savings Account?

ACA Obamacare Essential (Mandatory) Benefits

and #CA California Essential Health Benefits

- CHCF Comparison of CA and Federal Essential Health Benefits

- (A) Ambulatory patient services.

- (B) Emergency services.

- Emergency response ambulance or ambulance transport services

- (C) Hospitalization.

- (D) Maternity [but not infertility - CA Law? ] and newborn care.

- §146.130 Standards relating to benefits for mothers and newborns.

- Maternity: Inpatient hospital and ambulatory

- Prescription drug coverage for contraceptives

- Maternity hospital stay

- Sterilization operations and procedures View the Affordable health ca.com page Assembly Bill 1453 (Monning) and Senate Bill 951 (Hernandez). View the California Health and Safety Code, section 1367.005

- Abortion G-d forbid

- (E) Mental health and substance use disorder services, including behavioral health treatment.

- California Mental health parity

- Autism care (FAQ) including behavioral health treatment

- autism learning partners.com/medi-cal

- insurance.ca.gov/autism

- Sample Policy - use ctrl f to search for autism

- Medi Cal FAQ's

- Autism care (FAQ) including behavioral health treatment

- California Mental health parity

- (F) Prescription drugs. CFR 156.122

- (G) Rehabilitative and habilitative [learn or improve skills for daily living] services and devices.

- (H) Laboratory services.

- (I) Preventive and wellness services and chronic disease management.

- Diabetes education, management and treatment

- (J) Pediatric services, including Dental - oral and vision care. Blue Shield Individual Flyer Essential Health Benefits 5.2013 Group Essential Health Benefits (EBH) 42 USC 18022 SB 951

- (H?) Cancer and other life threatening disease - clinical trials

- AIDS vaccine

- HIV testing

- Organ transplants for HIV

- Alpha feto protein testing

- Prosthetics for laryngectomy

- Reconstructive surgery

- Mastectomies and lymph node dissections

- Cervical cancer treatment

- Osteoporosis treatment

- Surgical procedures for jaw bones

- Anesthesia for dental

- Conditions attributable to diethylstilbestrol

- Hospice (end of life) care

- Pain management medication for terminally ill

- Phenylketonuria treatment

- Health Care.Gov

- CMS.gov very detailed

-

White House.Gov Affordable Health Care Act YouTube Channel

- Here's the Feb. 20, 2013 final.rule establishing the essential health benefits (EHBs) for 10 categories of care, including basic services such as hospitalization and emergency care, as well as mental health and maternity care. In addition, the plans must cover a minimum of 60 percent of the actuarial value of covered medical services.

-

No more Annual & Lifetime Limits under Health Care Reform Aetna's Explanation

- § 1300.67.005. Essential Health Benefits Westlaw Barclays California Code of Regulations

- CHCF Comparison of CA and Federal Essential Health Benefits

- CA Department of Insurance

- Covered CA

- Medi Cal Listing

- California Benchmarks Kaiser Small Group HMO 30 ♦ CA SB 43 effective 1.1.2016 makes this the benchmark for individual plans too.

- CHCF Comparison of CA vs Federal Rules as of 2014

- Frequently Asked Questions on Essential Health Benefits Bulletin from the Department of Health and Human Services (PDF)

- Essential Health Benefits Bulletin from the Department of Health and Human Services, Dec. 16, 2011 (PDF)

-

No more Annual & Lifetime Limits under Health Care Reform Aetna's Explanation

- Short Term Policies that don't have essential benefits have been banned in CA for a long time. Now the Feds are doing it. Kff.org

- Our main webpage on California & Federal Essential Health Benefits