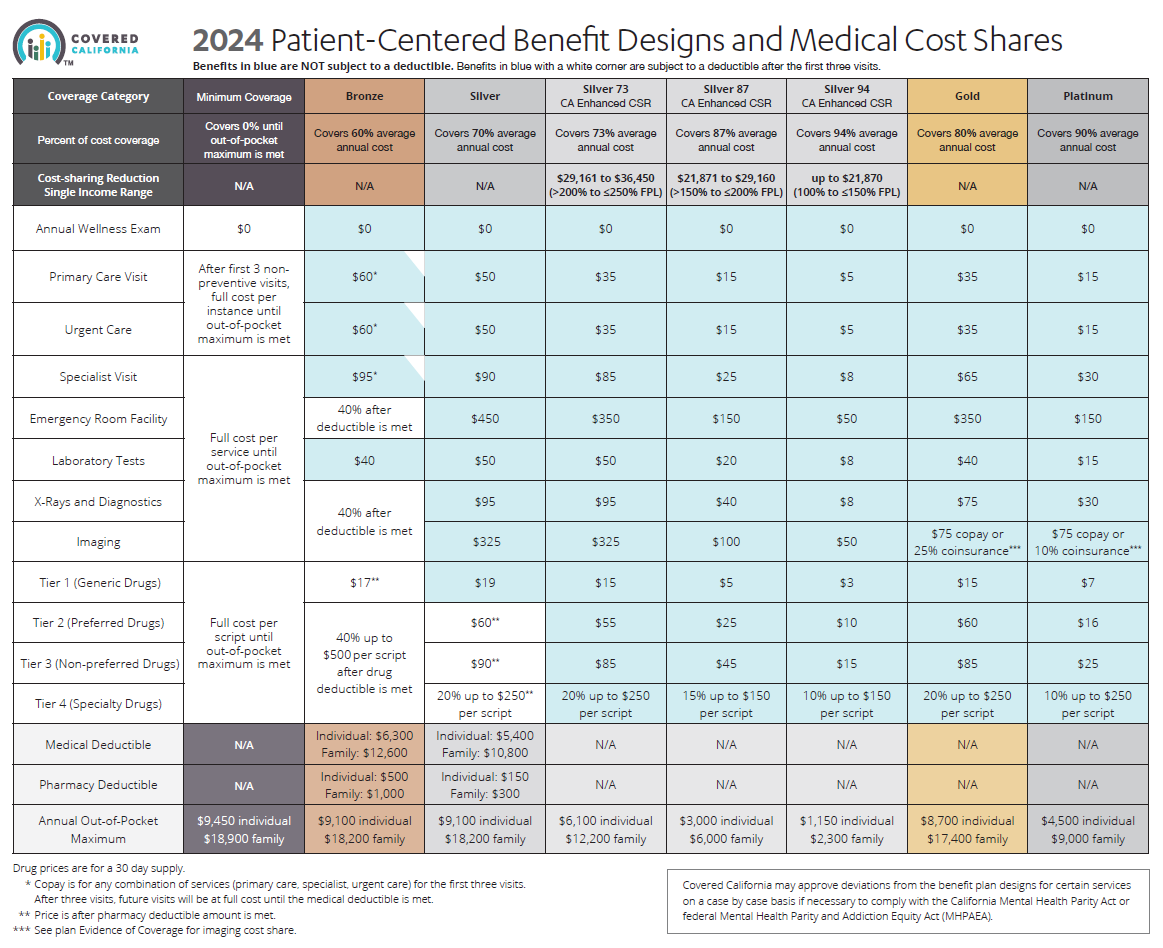

- Source and see a sharper image 2024 Patient Centered Designs * *

- Covered CA bulletin on new and improved Enhanced Silver CSR Cost Sharing Reduction

- Do you think your medical bills will be higher or lower than average for your age & zip code?

- Expected Payout (AV) MLR Medical Loss Ratio

- Bronze 60%

- Enhanced Silver 70% - 94% Gold 80% Platinum 90%

- Metal Levels are based on Expected Claims Payment - that is the actuarial value (AV).

- Did you notice LOWER deductibles & Co Pays???

- This is one way Health Care Reform hopes to make shopping and comparing easier. So, if you get a lower priced plan with less or fewer benefits, co-pays, deductibles you simply pay more when you have a claim. Don't worry, there is a stop loss - maximum out of pocket OOP, of say $7k so that you won't break the bank.

- All plans cover the 10 Federal essential benefits and CA mandated benefits.

- Our main webpage on Metal Levels

#Examples of how claims get paid by Metal Level

- Heart Attack or Stroke,

- Pregnancy

- Back Injury

- Breast Cancer – Essential Benefits by Metal Level FAQ

There is no free lunch, it’s all a function of the Medical Los Ratio.

- What is your ability to pay a higher deductible or any deductible and co pay?

- Get a quote http://www.quotit.net/

Video’s

- What are the four metal levels? VIDEO

- Steve Explains Enhanced Silver – CSR Cost Sharing Reductions VIDEO

- Explanation of the Rate Difference for Silver between Covered CA and direct – Plain English

- Summary of the litigation

- How to find plan that fits budget VIDEO

- what plan to take if you know you will have a BIG surgery or expense coming up VIDEO

- Maximum OOP Out of Pocket? VIDEO

- View our webpage on OOP Maximum Out of Pocket

- Understanding Health Care Costs Health Net VIDEO

FAQ

Differences in Metal Levels

- I’m paying the highest possible premium with a Platinum Plan, why aren’t they covering everything my doctor prescribes or test I need for cancer?

- Take a look at the Metal Level Chart above and you’ll see that the differences in Platinum, Bronze, Silver & Gold are in the deductibles & co-pays. The metal levels have nothing to do with the quality of care! https://www.healthcare.gov/glossary/health-plan-categories/ See above about CA Standard Benefits Designs. Pretty much, everything maxes out at $7,800 the OOP Out of Pocket Maximum, see definitions and videos ablove. Thus, if you have a $1,000,000 claim, whether you have Bronze, Silver or Platinum the most you pay is $7,800.

- The Law requires that Insurance Companies pay out 80% on Individual Plans and 85% in claims on group plans, see MLR-Medical Loss Ratio above. Thus, the Insurance Companies, don’t really care if you take Bronze or Platinum, they still keep 20% for their overhead and profits.

- The definition for Medical Necessity and Clinical Bulletins are the same for all 4 metal levels.

- The formularies the list of Rx the Insurance Company will cover, are the same. See the formulary page about getting exceptions if you really need the higher cost Rx. The difference is the co pays and deductibles. At least when one turns 65 and goes on Medicare, Part D has an Rx finder when you can put in your Rx Prescriptions and get a side by side comparison.

- Here’s more information on price of Rx, getting exceptions, etc. from a similar prior question.

- If you feel an Insurance Company isn’t paying what they should, here’s our Appeals & Grievance Page.

- Check out HSA – Health Savings Accounts – the definition of Medical Necessity isn’t regulated by and Insurance Company having to pay out claims…

- This way you get a High Deductible Bronze Plan and fund yourself any claims before you meet the deductible.

- How do mental health therapist benefits vary amongst the four metal levels?

- Unfortunately, almost 1/2 of therapists don’t take any Insurance. Thus, you’ll have to check the out of network provisions in the Summary of Benefits or EOC Evidence of Coverage.

- See the Metal Level Chart above and note the difference in co-pay between the metal levels under Primary Care and Specialist Visits.

- HDHP so you can get an HSA Health Savings Account and pay the bills tax preferred!

- Did you just get a big rate increase on your Silver Plan with Covered CA and you make too much $$$ to get subsidies?

- See our webpage on Silver Loading

#Report changes as they happen - within 30 days! 10 CCR California Code of Regulations § 6496

10 days for Medi Cal 22 CCR § 50185

Our webpage on ARPA & Unemployment Benefits - Silver 94

IRS Form 5152 - Report Changes

- Our VIDEO on how to report changes to Covered CA

- Lost your job? How to keep your Health Insurance. Shelter at Home VIDEO

- References & Links

- Here's instructions, job aid, reporting change in income

- Our webpage on the exact definition of MAGI Income

- If you've appointed us - instructions - as your broker, no extra charge, we can do it for you.

- Voter Registration

- Denial of benefits and possible criminal charges if you don't report changes in income!

- When Increasing Your Covered California Income Estimate Creates an Ethical Dilemma Insure Me Kevin.com

- Fudging Income?

- Western Poverty Law on reporting changes

- How to cancel coverage.

- Visit our webpage on how to report changes

All our plans are Guaranteed Issue with No Pre X Clause

Quote & Subsidy #Calculation

There is No charge for our complementary services

Watch our 10 minute VIDEO

that explains everything about getting a quote

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- Get more detail on the Individual & Family Carriers available in CA

![]()

#Covered CA Certified Agent

No extra charge for complementary assistance

- Appoint us as your broker

- Get Instant Health Quotes, Subsidy Calculation & Enroll

- Videos on how great agents are

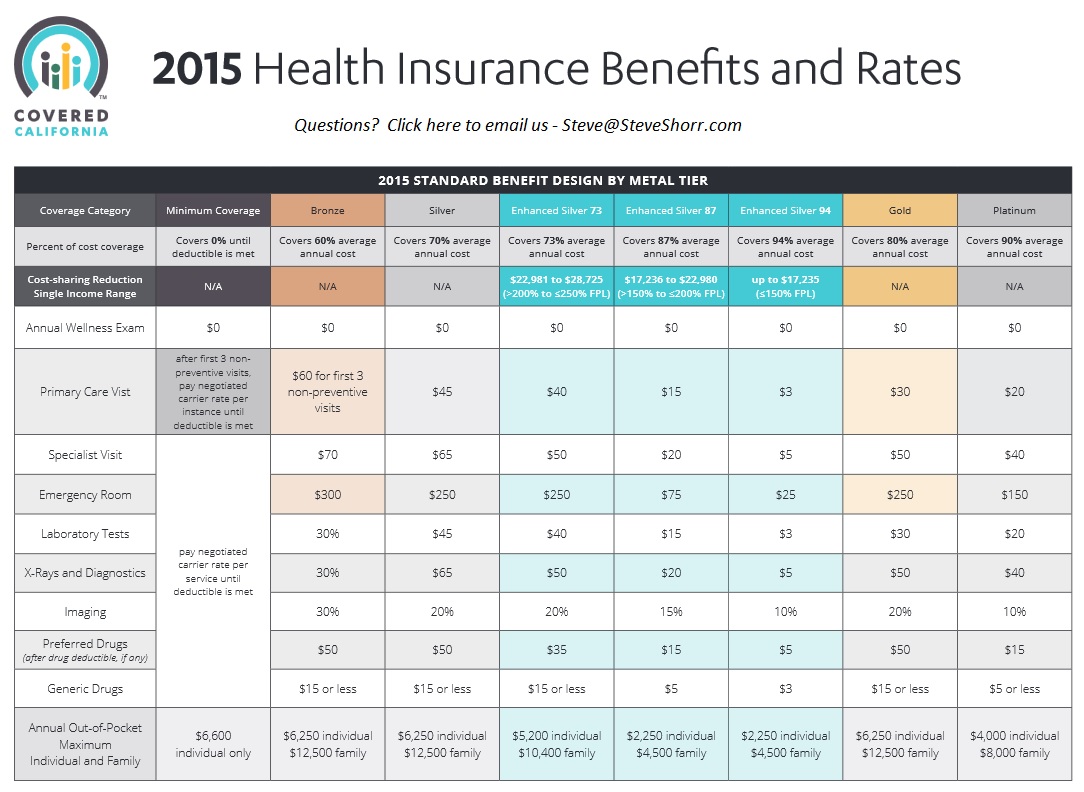

What are Covered California standard benefit designs?

- Health insurance plans must follow Covered California’s standard benefit designs.

- With standardized benefits, consumers can accurately compare health insurance plans, because the benefits are the same for all plans offered in the Covered California marketplace. Additionally, standardizing benefits ensures that the selected health insurance plans define what the consumers get and limit the consumer’s out-of-pocket costs by type of service.

- There is also a Catastrophic level, (high deductible) that one can qualify for, if they are under 30 or the premium is unaffordable as being more than 8% of income. Open Congress.org Blue Cross Blue Shield Blue Shield Catastrophic plan Email us for rates. [email protected]

- AB 639 (Chaptered) would Prohibit any [Insurance] product from being offered other than those with a standardized product design [metal level] in the family market. Sounds like what we have with Medi Gap policies. Get the most recent status at http://leginfo.legislature.ca.gov/

- I agree it will stifle innovation, so do you want same o same o or to be able to get a plan that fits your needs. On the other hand isn’t it just a mathematical calculation to see what the actuarial value and essential benefits is?

§156.140 Metal Levels of coverage.

- (a) General requirement for levels of coverage. AV, calculated as described in §156.135 of this subpart, and within a de minimis variation as defined in paragraph (c) of this section, determines whether a health plan offers a bronze, silver, gold, or platinum level of coverage.

- (b) The levels of coverage are:

- (1) A bronze health plan is a health plan that has an AV of 60 percent.

- (2) A silver health plan is a health plan that has an AV of 70 percent.

- (3) A gold health plan is a health plan that has an AV of 80 percent.

- (4) A platinum health plan is a health plan that has as an AV of 90 percent.

- (c) De minimis variation. The allowable variation in the AV of a health plan that does not result in a material difference in the true dollar value of the health plan is ±2 percentage points, except if a health plan under paragraph (b)(1) of this section (a bronze health plan) either covers and pays for at least one major service, other than preventive services, before the deductible or meets the requirements to be a high deductible health plan within the meaning of 26 U.S.C. 223(c)(2), in which case the allowable variation in AV for such plan is −2 percentage points and +5 percentage points.

- New Amendment 4.18.2017

- (c) De minimis variation. For plan years beginning on or after January 1, 2018, the allowable variation in the AV of a health plan that does not result in a material difference in the true dollar value of the health plan is −4 percentage points and +2 percentage points, except if a health plan under paragraph (b)(1) of this section (a bronze health plan) either covers and pays for at least one major service, other than preventive services, before the deductible or meets the requirements to be a high deductible health plan within the meaning of 26 U.S.C. 223(c)(2), in which case the allowable variation in AV for such plan is −4 percentage points and +5 percentage points.

- [78 FR 12866, Feb. 25, 2013, as amended at 81 FR 94180, Dec. 22, 2016] ECFR.Gov

- Final Rule CMS 9929 F comments & discussion – Page 85

- Link to an amendment published at 82 FR 18382, Apr. 18, 2017.

- get quotes

What is #Catastrophic Coverage

less benefits than Bronze

- One can qualify for the Catastrophic level, Health Care.gov (high deductible) if they are under 30 or the premium is unaffordable as being more than 8% of income, or possibly a hardship exemption. Blue Cross Blue Shield . See the Federal Hardship Exemption Form for more information.

- Check our Quotit Calculator for rates and benefits. Very few people bother with Catastrophic – Especially if they qualify for enhanced silver.

- Learn more on HealthCare.gov

- Exemption Forms

- https://www.healthcare.gov/exemption-form-instructions/

- Right-click this exemption application form (PDF) link for hardship exemptions, like homelessness, bankruptcy, eviction, or foreclosure.

- Right-click this exemption application form (PDF) for affordability exemptions AND residency in:

- California, Colorado, District of Columbia, Idaho, Maryland, Massachusetts, Minnesota, New York, Rhode Island, Vermont, Washington

- Comparison to Bronze & Rates

- FAQ’s

- When/if you think it appropriate I am ready to file a complaint with the state insurance board. Oscar shouldn’t have such a problem selling a policy to someone with an ECN in hand.

- 1st of all, this website is probably the most authoritative site for Catastrophic Coverage in California. We’ve only had two visitors in the past 30 days. Generally, Catastrophic isn’t any less premium than Bronze and there are no subsidies. Finding any information about these plans, without getting into “bogus” plans is difficult. If you’ve found anything authoritative on catastrophic or minimum coverage plans, please post those links in comments below.

- That said, I’m not surprised that the Insurance Companies are having difficulty finding a procedure to sell you a plan. What kind of crazy thing is this, the “family glitch?”

- I don’t think that a week for an Insurance Company to research something is all that long. I just sent a follow up email.

- I seriously doubt that the DOI Department of Insurance or Managed Health Care would even know what you’re talking about if you made a complaint.

- Please, when referring to other website, provide the exact URL. I don’t see why anyone would want the catastrophic – minimum coverage plan. The rate isn’t much less than Bronze.Please advise what hardship you qualify for and why. We must have facts & proof, before making determinations and recommendations.

- Please get a quote, use the icon in the upper right and then we can better discuss what best fits your needs & wants.

Resources & Links

- Insure Me Kevin.com How 2020 plans work deductibles, etc. * Video *

- Covered CA on Metal Levels

- Covered CA now allows different metal levels for each member of family – Learn More CA Health Line 8.15.2016 * Insure Me Kevin.com 8.2.2016

- Affordable Care Act’s cap on annual out-of-pocket health care spending for individuals, regardless of whether consumers have an individual or family health plan. Final Market Rules 45 CFR Parts 144, 147, 153, 154, 155, 156 and 158

- Bronze – Co Insurance after Deductible?

- Covering Costs of High Deductible Plan?

Copied from Facebook Post

Rick Sanders

I had quadruple bypass in 2014 had a covered California bronze plan it cost me 6200.00 I picked my doctor and hospital, Best system in the world by far