S Corporations

IRS Tax Forms for S. Corp and 2% + plus owners to file for tax deductibility of Group Health Insurance

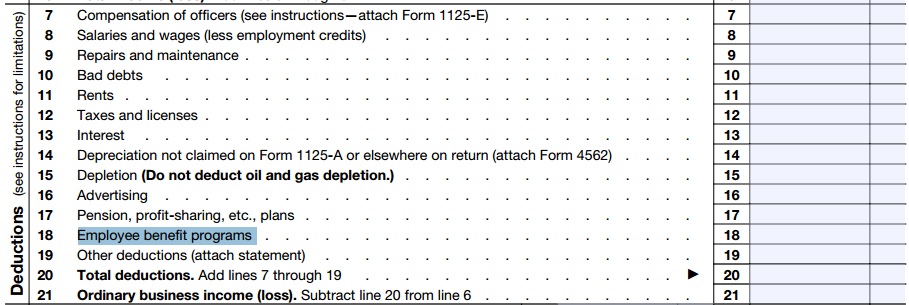

Tax Return for S Corp # 1120 S – Health Insurance Deduction

Section 106 tax deduction for #SCorp Owners?

- The employee premium for S Corporation is not an issue for being tax deductible business expense. See IRS Section 106 above.

- For 2-percent S corporation shareholder-employee it gets complicated and confusing. Check our bibliography belong and competent tax counsel, group health premiums are deductible by the S corporation and reportable as wages on the shareholder– on the employee’s Form W-2, subject to income tax withholding.

- However, these additional wages are not subject to:

- Social Security, or

- Medicare (FICA), or

- Unemployment (FUTA) taxes

- However, these additional wages are not subject to:

- The owner and 2% + shareholders may be able to use the Self-Employed Health Insurance (SEHI) deduction if you’re at least a 2% shareholder in an S Corporation. To claim this deduction, the health insurance premiums must be paid or reimbursed by the S corporation and reported as taxable compensation in box 1 of your W-2. The S Corporation can either purchase the policy in your name or reimburse you for the premiums you paid. The policy can also cover your spouse, dependents, and any nondependent children under the age of 27. See Section 162 IRS Code * (152(f)(1)) * (HR 4872 – Obama Care §162(l)(1)§401(c)(1))

- Claiming the SEHI deduction is generally more advantageous than claiming an itemized deduction. The SEHI deduction will appear on line 17 of Schedule 1 of your federal income tax return, Form 1040 (as part of Line 10), and is limited to the amount in Box 5 (FICA wages by the corporation) of your W-2.W-2 and the K-1 that the S corporation sent to you.

- A 2-percent shareholder-employee is eligible for an above-the-line deduction See Schedule 1 and is able to lower his Adjusted Gross Income (AGI) irs.gov/s-corporation-compensation-and-medical-insurance-issues

- The insurance plan must be established, or considered to be established, under the business. IRS Publication 535 pdf page 18 * If only one employee it can be in employees name IRS.gov * This includes Individual Medicare Plans Journal of Accountancy Check with your CPA.

Links, Bibliography & Resources

-

-

- Source – loop hole lewy.com/health-insurance-deduction

- irs.gov/s-corporation-compensation-and-medical-insurance-issues

- nolo.com/deducting-health-insurance-with-s-corporation

- intuit.com/deduct-health-insurance-premiums-corporation

- S Corporation Compensation and Medical Insurance Issues IRS.gov

- Publication 15B Employer’s Guide to Fringe Benefits..

- IRS Publication 535 Guide to business expense resources

- 26 U.S. Code § 162 – Trade or business expenses

- (a)In general

There shall be allowed as a deduction all the ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business, including—

(1)a reasonable allowance for salaries or other compensation for personal services actually rendered; - Federal Tax Treatment of Health Insurance Expenditures by the Self-Employed: Current Law and Issues for Congress 2009

- (a)In general

- check out Publication #974 Premium Tax Credit,

- If you receive Obamacare Tax Credits, here’s more detail

- Withholding W 4

- Form 1120 US Corp Tax Return

-