Medicare Supplement Insurance, also called Medi gap, is private insurance that helps pay some of your share of out-of-pocket costs in Original Medicare, such as copayments, coinsurance, and deductibles. You generally need Medicare Part A and Part B before you can buy a Medigap policy. Medicare.gov explains Medigap basics here.

This page is your starting point for California Medigap choices. From here, you can compare Plan G, review Blue Shield and other carrier options, learn when health questions may apply, and understand California-specific rules like community rating and the birthday rule.

What Does Medigap Add to Medicare A and B?

Original Medicare gives you broad access to doctors and hospitals that accept Medicare, but it does not pay every cost. A Medi gap plan can help reduce your exposure to Medicare deductibles, copays, and coinsurance. It is different from Medicare Advantage: Medi gap works with Original Medicare, while Medicare Advantage is a separate way to receive Medicare benefits.

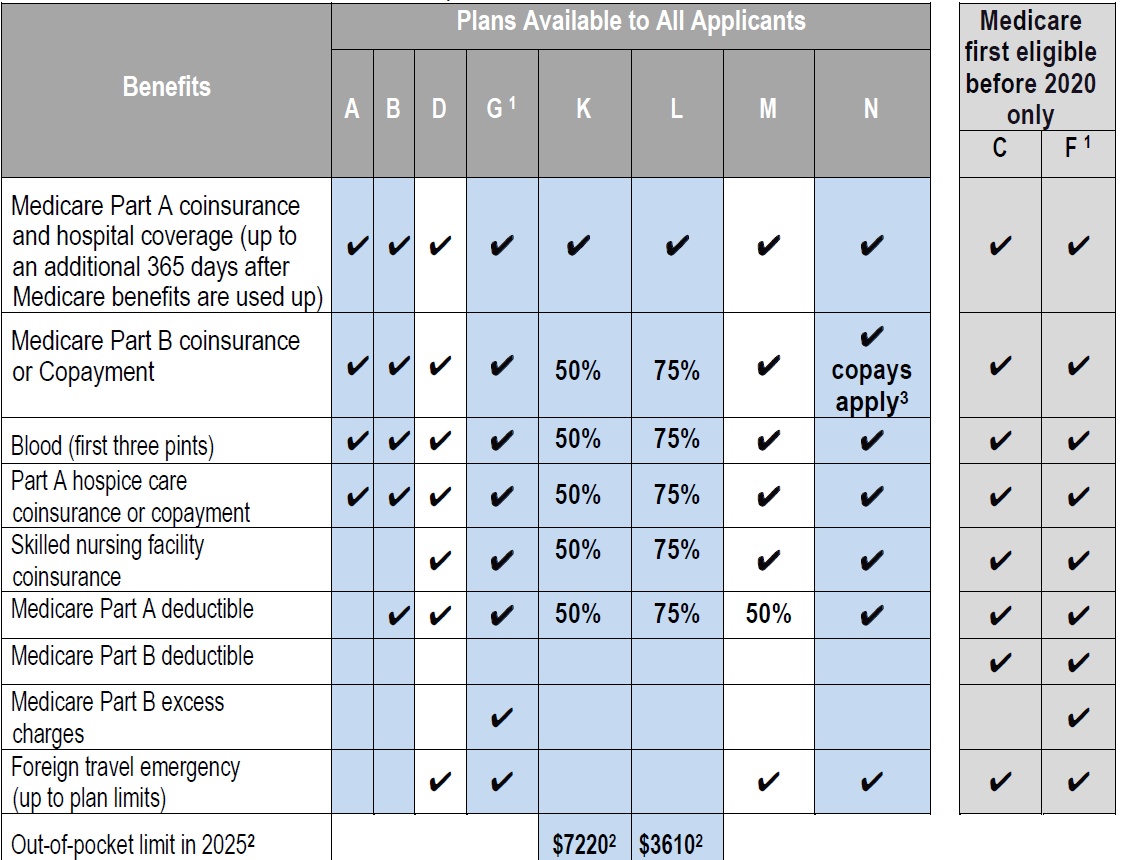

Medi gap plans are standardized by plan letter in most states, so a Plan G from one company has the same basic medical benefits as a Plan G from another company. The differences are usually the premium, rate history, household discounts, customer service, and underwriting rules.

The plan letter determines the benefits. The company determines the price, service, and long-term value.

Why Plan G Is Often the Main Comparison

For many people new to Medicare today, Plan G is the most common Medi gap comparison because it covers many of the gaps left by Original Medicare, except for the Medicare Part B deductible. That makes the real comparison less about benefits and more about price, company stability, rate increases, and whether you can qualify.

If you are mainly shopping for Plan G, compare actual rates first. Then review whether a company such as Blue Shield, Anthem, United Healthcare®, or another carrier makes the most sense for your ZIP code and situation.

California Rules Matter

California has Medi gap rules that can affect when and how you shop. The California Department of Insurance explains that the birthday rule gives Medi gap policyholders a 60-day open enrollment period following their birthday each year to buy a new Medi gap policy without medical screening, (Health Questions) if the new policy has the same or lesser benefits. See the California Department of Insurance explanation.

California Medi gap rates are community-rated, so premiums are not based on gender. Premiums may still vary by ZIP code, age, tobacco use, plan letter, company, and household discounts.

Common California Medigap Questions

When is the easiest time to buy Medigap?

Usually when you are first eligible for your Medigap open enrollment period, or when you have a guaranteed issue right. Outside protected periods, health questions may apply.

Can I switch Medigap plans later?

Sometimes. California’s birthday rule may help if you already have Medi gap and want to move to a plan with the same or lesser benefits. Other guaranteed issue situations may also apply.

Should I pick the cheapest company?

Not always. Price matters, but so do household discounts, rate history, service, and whether the company is a good fit long-term.

Ready to Compare Medigap Rates?

Introduction to #MediGap

Publication 02110

- 2025 Official Medicare Guide to choosing a Medi Gap Policy # 02110

- MORE Information and Links

- Matrix - Spreadsheet of what Medicare Pays, Medi Gap pays and what little you pay

Medicare Part A

(#Hospital Insurance)

- Medicare Part A Hospital coverage helps pay for care in hospitals as an inpatient,... skilled nursing facilities, hospice care, and some home health care (see publication # 10969) but not Long Term Care.

- Most people get Part A automatically when they turn age 65 at no charge, since they or a spouse paid Medicare taxes while they were working. You need to sign up close to your 65th birthday, even if you will not be retired by that time. (If you are getting Social Security benefits when you turn 65, your Medicare Hospital Benefits - Part A - start automatically.)

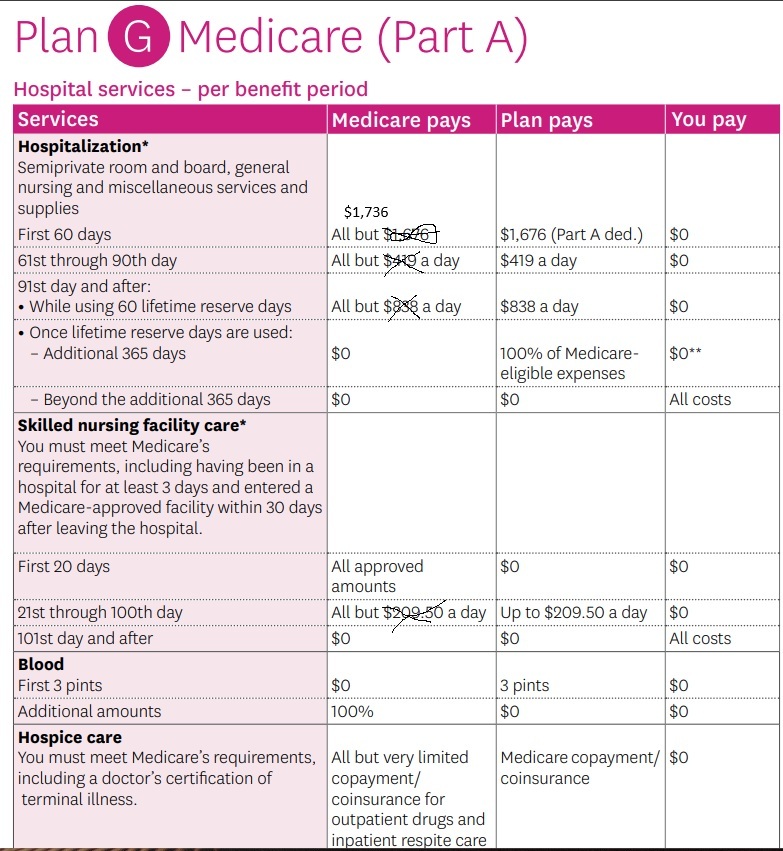

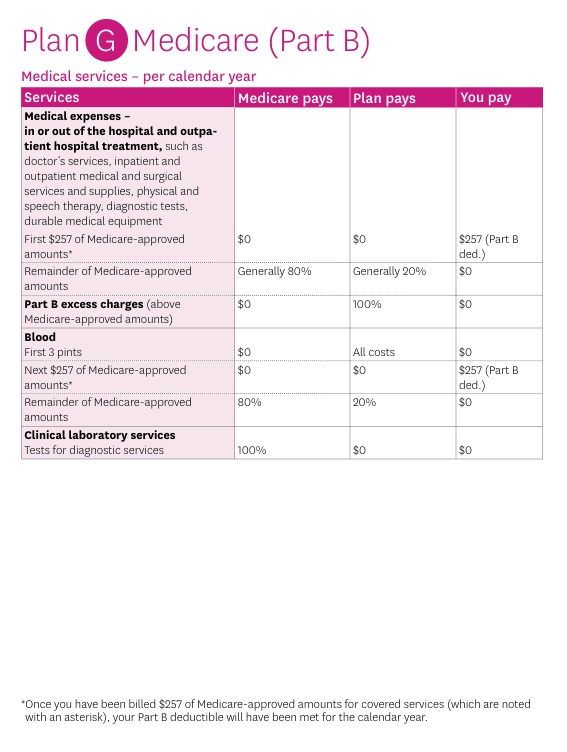

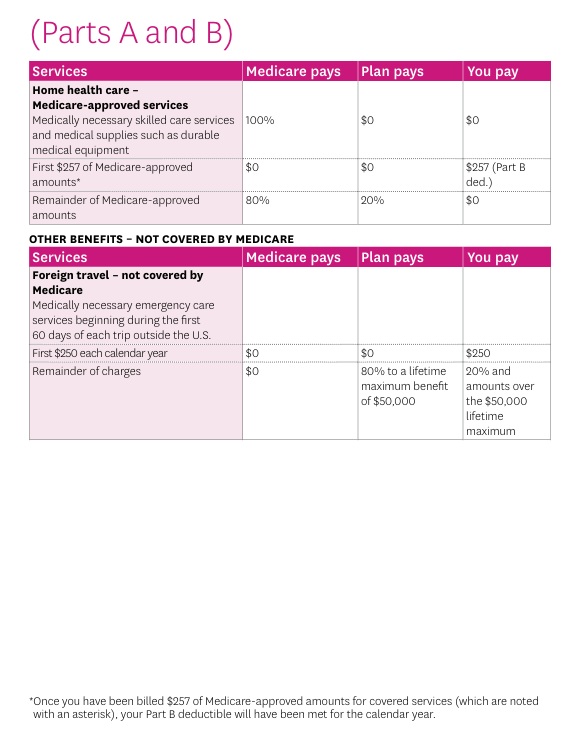

- Here's a chart it's just a illustration and is NOT official that shows what Medicare pays, the gaps in Medicare and what you may get when you add a Medi Gap Plan or Medicare Advantage to cover those gaps

- Chart Updates 2026 Fact Sheet Medicare Costs Publication 11579

- . standard Part B monthly premium amount ($202.90 in 2026)

- Steve's VIDEO Explanation Comparing what Medicare pays and what you get extra with MAPD or Medi Gap

-

See full brochure I cut and pasted this from

-

- "Hospital at Home" Programs Improve Outcomes, Lower Costs But Face Resistance from Providers and Payers Commonwealth Fund

- Explanation from Fortune Magazine

- Price lookup from Medicare.gov on what you pay with Original Medicare without a Medi Gap plan

-

Pays on top of Medicare Parts A & B – Any Medicare Provider

- Steve's YouTube Video

Part B - Outpatient helps Pay For Doctors' services, outpatient hospital care, and some other medical services that Part A does not cover, such as the services of physical and occupational therapists, and some home health care see publication 10969, but not Long Term Care. Part B helps pay for these covered services and supplies when they are medically necessary.

The chart below is a very brief summary. Check the actual Evidence of Coverage for the plan you want to enroll in, Medicare & You or actual Medicare documents.

2026 Part B deductible—$283 before Original Medicare starts to pay You pay this deductible once each year CMS.gov

Our Webpages with more detail:

- Coverage in Part A Hospital & B Doctor Visits? Part D Rx

- Chiropractic – Medicare A & B – MAPD

- Diabetes – Prevention & Coverage under Medicare & ACA

- Durable Medical Equipment

- End Stage Renal – Kidney Failure

- Hearing Aids

- Physical therapy – occupational speech

- Skilled Nursing SNF & Home Health What Medicare Pays

- Togetherness – Loneliness Social Determinants of Health

- Mental Health

- Blue Shield Mental Health Resource Hub >>> Visit *

- How to sign up for Medicare?

- FAQ Medical Necessity our Medical Necessity Webpage

- Original Medicare & Medi-Gap – Supplement vs Medicare Advantage MAPD

- Medicare Beneficiaries’ Out-of-Pocket Spending for Health Care

Reference Medicare.gov Choosing a Medi Gap policy

- Our webpage on F vs G

- Fact Sheet Medicare Costs

- Fact Sheet Innovative Benefits Hi Cap

Medicare Advantage (MAPD) and Medigap are two fundamentally different ways to manage your out-of-pocket costs in addition to Original Medicare. MAPD replaces Original Medicare with a private plan, while Medigap (Medicare Supplement) works alongside Original Medicare. [1, 2, 3]

Comparing these options at a glance:

| Feature [2, 3, 4, 5, 6, 7, 8, 9] | MAPD (Medicare Advantage) | Medigap (Medicare Supplement) |

| — | — | — |

| How it Works | Replaces Original Medicare. You get Part A & B benefits through a private insurer. | Supplements Original Medicare. Original Medicare pays first, then Medigap covers the rest. |

| Monthly Premium | Often $0 or very low, but you still must pay your standard Medicare Part B premium. | Usually higher than MAPD, depending on your age, location, and health. |

| Network & Flexibility | Restrictive networks like HMOs and PPOs. You must use plan-approved doctors. | High flexibility. See any doctor across the country that accepts Original Medicare. |

| Referrals & Pre-auth | Often requires referrals for specialists and pre-authorizations for major procedures. | No referrals needed and almost no pre-authorization required. |

| Drug Coverage (Part D) | Included in most MAPD plans. | Usually not included; you must purchase a separate Part D plan. |

| Out-of-Pocket Limit | Set yearly out-of-pocket maximums. | No yearly out-of-pocket limit, because the plan covers nearly all gaps. |

| Health Questions | No health underwriting. Guaranteed acceptance when you are first eligible. | Requires health underwriting (except during initial open enrollment periods). |

Which route should you choose?

• Choose MAPD if you prefer lower upfront monthly premiums, want additional benefits (like dental and vision) included, and don’t mind staying within specific doctor/hospital networks.

• Choose Medigap if you want the freedom to see any doctor, predictable out-of-pocket costs, and the flexibility to avoid navigating restrictive network rules or prior authorizations. [1, 4, 5, 6, 10]

Because dropping a Medigap plan for MAPD can make it difficult or impossible to switch back to Medigap later (due to health underwriting), it is highly recommended to speak with a licensed agent. To explore your options and get customized rate comparisons, visit the Health Reform Quotes

platform.

AI responses may include mistakes.

[1] https://individuals.healthreformquotes.com/sign-medicare/enrollment-tools-and-decisions-for-medicare/va-compared-to-medicare-a-b-c-d-medi-gap/

[2] https://www.medicare.gov/health-drug-plans/medigap/basics/how-medigap-works

[3] https://individuals.healthreformquotes.com/sign-medicare/medi-gap/blue-shield/

[4] https://www.youtube.com/watch?v=MaLW9Vd-eKk

[5] https://www.youtube.com/watch?v=Tw4kB5z548Q

[6] https://www.youtube.com/watch?v=07MJB5DgLKw

[7] https://individuals.healthreformquotes.com/sign-medicare/medi-gap/

[8] https://www.medicare.org/medicare-supplement-plans/disadvantages-of-medigap-plans-what-you-need-to-know/

[9] https://www.healthline.com/health/medicare/mapd-medicare

[10] https://www.cbsnews.com/news/why-do-some-seniors-choose-medigap-over-medicare-advantage/

[11] https://individuals.healthreformquotes.com/sign-medicare/medi-gap/guaranteed-acceptance/

More #Information on Medicare & You booklet

Our video explaining the Governments brochure on choosing a Medi Gap Policy. Click the little square on the right, to enlarge the video.

- Medicare Supplement Policies CA Insurance Code §§10192.1 – 10192.24

- CA Health Care Advocates HI CAP Fact Sheet

- If you have a Medigap policy and get care, Medicare will pay its share of the Medicare-approved amount for covered health care costs. In most Medigap policies, you agree to have the Medigap insurance company get your Part B claim information directly from Medicare. Then, your Medigap policy will pay your doctor whatever amount you owe under your policy and you’re responsible for any costs that are left. Learn More >>> Medicare.Gov

- Prior Authorization NOT Required! Askchapter.org *

- Supplementing Medicare: An Overview 10-30-20 Hi Cap

- Supplementing Medicare: Medigap Plans 12-14-23 Hi Cap

- Your Rights to Purchase a Medigap 12-14-23 HI Cap

- Search for Participating Doctors & Hospitals – Just about ALL of them!

- medicare.gov/coverage

- What’s Covered App for Smartphones

- Medicare Coverage Database Search

- medicare.gov/procedure-price-lookup

- MLN Items & Services Not Covered Under Medicare

- An Overview-05-19-23 CA Health Care Advocates Hi Cap

- Original Medicare: An Overview CA Health Care Advocates Hi Cap

- 2024 Premiums, Coinsurance & Deductibles – 10-19-23 CA Health Care Advocates Hi Cap

- Supplementing Medicare: An Overview 10-30-20 CA Health Care Advocates Hi Cap

- Enroll in Blue Cross

- Learn about UHC United Health Care

- Enroll in Blue Shield

- SCAN

- Use our scheduler to Set a phone, Skype or Face to Face meeting

- #Intake Form – We can better prepare for the meeting (National Contracting Center)

- TITLE XVIII—HEALTH INSURANCE FOR THE AGED – Medicare AND DISABLE

-

- Welcome to Medicare 2022 Publication # 11095

- Our webpage on Enrolling ONLINE for Medicare Part A Hospital & B Doctor Visits

- Part A Hospital rules for zero premium

- Part B – Doctors – How to sign up – Benefits

- How to apply for Part B when you lose employer coverage – during your special enrollment period # 10012

- Fact Sheet Deciding Whether to Enroll in Medicare Part A and Part B When You Turn 65 CMS.gov 15 pages

- Medicare & You: Deciding to Sign Up for Medicare Part B VIDEO

- CMS form to fill out L 564 E to prove you had Employer Coverage and get a special enrollment period, when you retire. VIDEO

- HI CAP CA Health Care Advocates Medicare Enrollment Periods

FAQ’s from Medicare.Gov

#Should I get Parts A & B?

Most people should enroll in Medicare Part A (Hospital Insurance) when they’re first eligible, but certain people may choose to delay Medicare Part B (Medical Insurance). In most cases, #How

It depends on the type of health coverage you may have.

- Deciding to Sign Up for Medicare Part B VIDEO

- You must pay your Part B premium every month for as long as you have Part B (even if you don’t use it).

- If I’m low income – are there any breaks?

- Interactive Q & A from IRS on when to sign up for Medicare

- I have coverage through my spouse who is currently working.

- I have retiree coverage (from my former employer or my spouse’s former employer) or COBRA coverage.

- I have TRICARE, and I’m a retired service member.

- I have TRICARE, and I’m an active-duty service member.

- I have CHAMPVA.

- I have End-Stage Renal Disease (ESRD).

- I have Marketplace Covered CA or other private insurance.

- I don’t have any of these.

- medicare.gov/should-i-get-parts-a-b

- How to apply for Part B during your special enrollment period # 10012

- Fact Sheet Deciding Whether to Enroll in Medicare Part A and Part B When You Turn 65 15 pages

- FAQ’s that we did

-

Medi Gap pays the medical expenses that Original Medicare Part A (Hospital) and Part B (Doctor) doesn’t. Check out the chart on this page to see what Medicare Pays, what you pay and what a Medi Gap plan pays.

- If you have a Medigap policy and get care, Medicare will pay its share of the Medicare-approved amount for covered health care costs. Then, your Medi-gap policy will pay its share. You’re responsible for any costs that are left. Medicare.Gov *

- More than half of all fee-for-service Medicare enrollees without any additional coverage chose a Medicare Supplement plan in 2021 Health Care Finance *

-

Original Medicare, Medicare Advantage nor Medi Gap pay for long term care either in a nursing home or at home care. Get more information on Long Term Care here.

-

Even if you think you can’t afford any extra premiums, there’s a lot of valuable information to help with planning.

-

- A Medicare Medi Gap – Supplemental plan will pick up most of the deductibles and co pays 20% that Medicare Parts A (Hospital) and B (Doctor Visits) do not.

- Virtually EVERY licensed MD and Hospital accept Medicare and thus any Medi-Gap Plan!

- When you purchase a Medi-Gap plan, rather than a Medicare Advantage Plan MAPD, you will also need to get Part D Rx Prescription Coverage.

- Please review the pages below for more information on Medi-Gap.

-

- Anthem Blue Cross

- Blue Shield – Medi-Gap – Any Medicare Provider

- Guaranteed Acceptance – Medi-Gap – Supplemental Plans

- No more plan F? Only G? MACRA