Medi Gap Plan F vs Plan G

The ONLY real difference is the $283 Medicare Part B deductible.

Which is the better value for you?

$250/month = $3,000/year

$300/month = $3,600/year

Get current Plan G quotes and compare them with what you are paying now for Plan F.

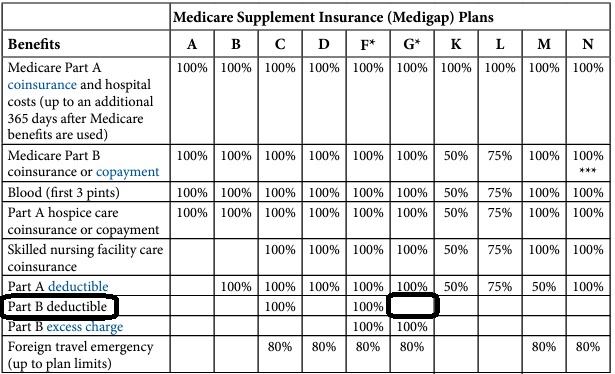

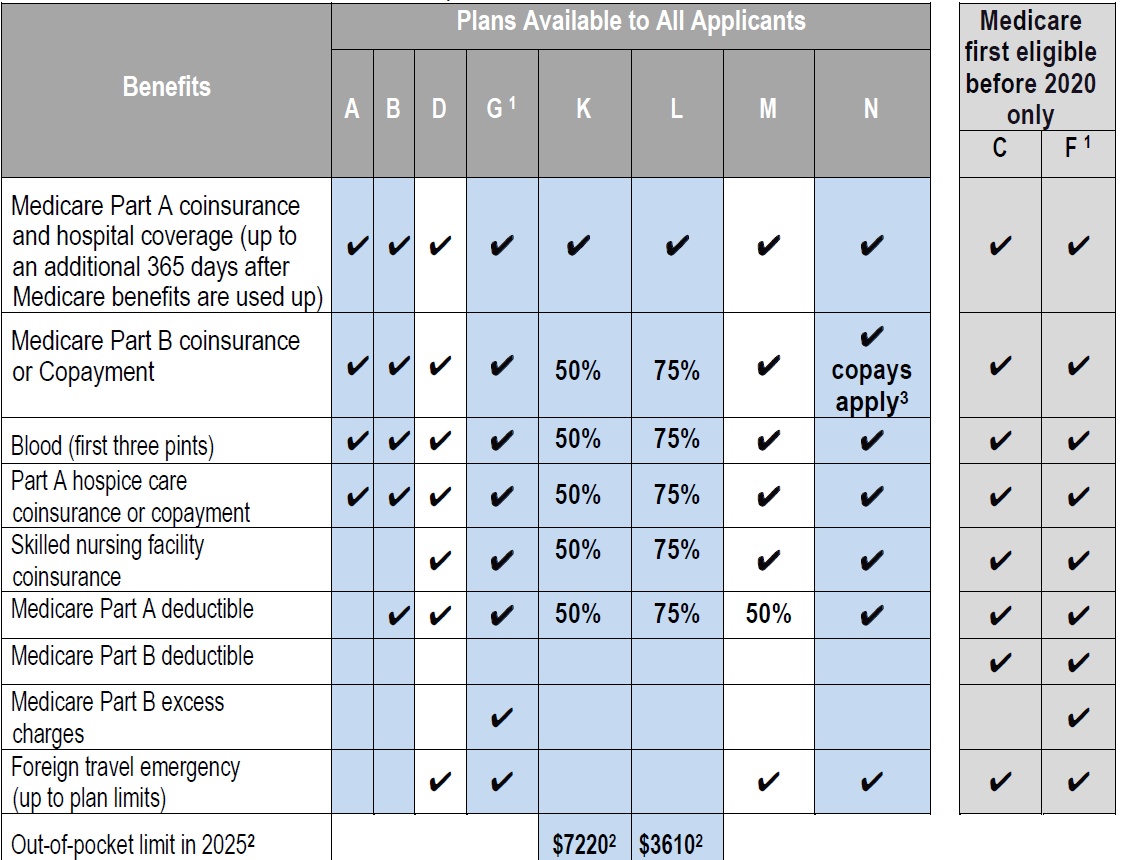

What Medicare A & B Pay, then what Medi Gap Pays

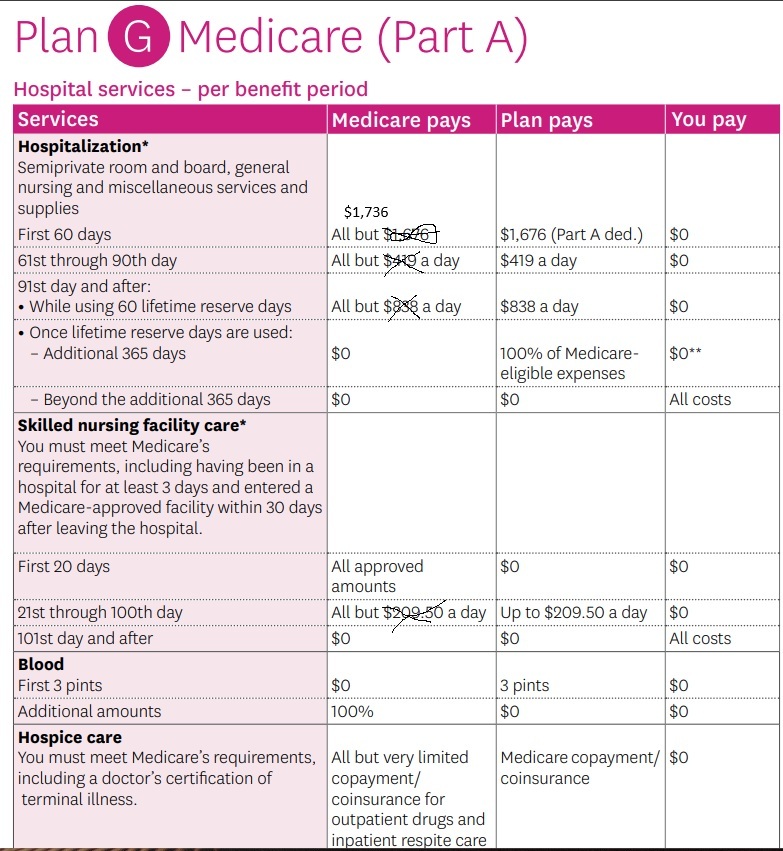

Medicare Part A

(#Hospital Insurance)

- Medicare Part A Hospital coverage helps pay for care in hospitals as an inpatient,... skilled nursing facilities, hospice care, and some home health care (see publication # 10969) but not Long Term Care.

- Most people get Part A automatically when they turn age 65 at no charge, since they or a spouse paid Medicare taxes while they were working. You need to sign up close to your 65th birthday, even if you will not be retired by that time. (If you are getting Social Security benefits when you turn 65, your Medicare Hospital Benefits - Part A - start automatically.)

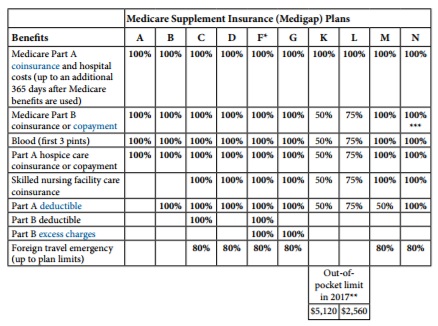

- Here's a chart it's just a illustration and is NOT official that shows what Medicare pays, the gaps in Medicare and what you may get when you add a Medi Gap Plan or Medicare Advantage to cover those gaps

- Chart Updates 2026 Fact Sheet Medicare Costs Publication 11579

- . standard Part B monthly premium amount ($202.90 in 2026)

- Steve's VIDEO Explanation Comparing what Medicare pays and what you get extra with MAPD or Medi Gap

-

See full brochure I cut and pasted this from

-

- "Hospital at Home" Programs Improve Outcomes, Lower Costs But Face Resistance from Providers and Payers Commonwealth Fund

- Explanation from Fortune Magazine

- Price lookup from Medicare.gov on what you pay with Original Medicare without a Medi Gap plan

-

Pays on top of Medicare Parts A & B – Any Medicare Provider

- Steve's YouTube Video

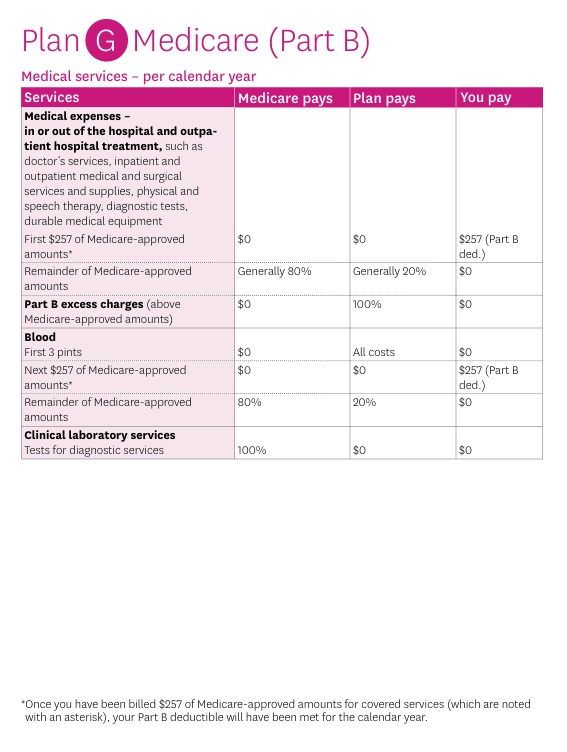

Part B - Outpatient helps Pay For Doctors' services, outpatient hospital care, and some other medical services that Part A does not cover, such as the services of physical and occupational therapists, and some home health care see publication 10969, but not Long Term Care. Part B helps pay for these covered services and supplies when they are medically necessary.

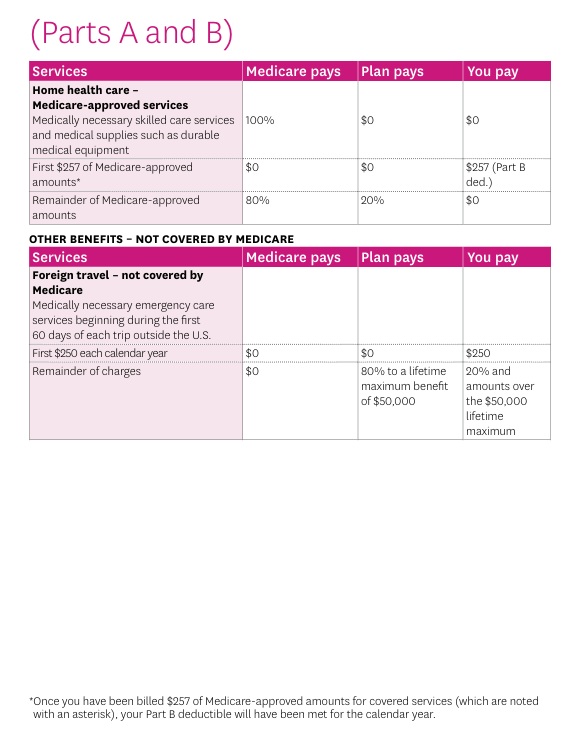

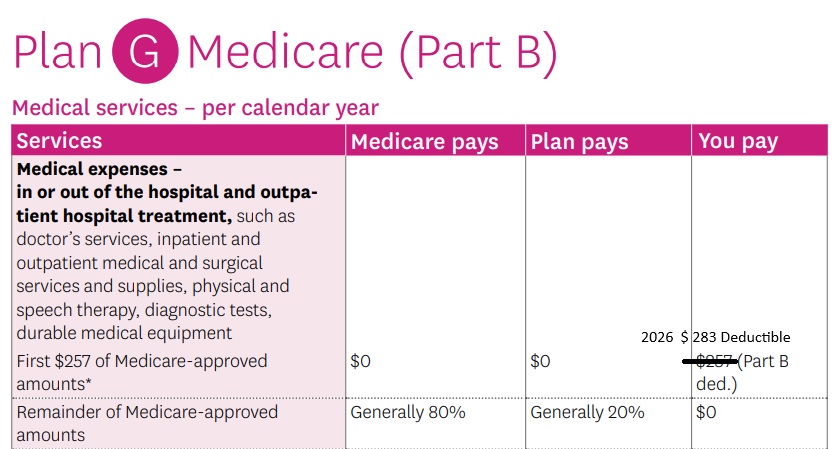

The chart below is a very brief summary. Check the actual Evidence of Coverage for the plan you want to enroll in, Medicare & You or actual Medicare documents.

2026 Part B deductible—$283 before Original Medicare starts to pay You pay this deductible once each year CMS.gov

Our Webpages with more detail:

- Coverage in Part A Hospital & B Doctor Visits? Part D Rx

- Chiropractic – Medicare A & B – MAPD

- Diabetes – Prevention & Coverage under Medicare & ACA

- Durable Medical Equipment

- End Stage Renal – Kidney Failure

- Hearing Aids

- Physical therapy – occupational speech

- Skilled Nursing SNF & Home Health What Medicare Pays

- Togetherness – Loneliness Social Determinants of Health

- Mental Health

- Blue Shield Mental Health Resource Hub >>> Visit *

- How to sign up for Medicare?

- FAQ Medical Necessity our Medical Necessity Webpage

- Original Medicare & Medi-Gap – Supplement vs Medicare Advantage MAPD

- Medicare Beneficiaries’ Out-of-Pocket Spending for Health Care

|

|

|

|

Compare Coverage Plan F to G

The ONLY difference is the Part B (Doctor Visits – Out of Hospital) Deductible 2026 $283 Medicare Fact Sheet Publication # 11579

Source Page 11 of Medi Gap Manual

- Seniors Find Medicare Enrollment Confusing, Avoid Changing Plans

- How does that compare to the premium?

Does it make sense to pay the extra monthly premium when the only difference is the

annual $283 for 2026 of the Part B Medical Insurance Deductible?

Here’s rules on changing from F to G for lower premiums. Our Webpage

Reference Medicare.gov Choosing a Medi Gap policy

- Our webpage on F vs G

- Fact Sheet Medicare Costs

- Fact Sheet Innovative Benefits Hi Cap

FAQ’s & Technical Details

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

Introduction to #MediGap

Publication 02110

- 2025 Official Medicare Guide to choosing a Medi Gap Policy # 02110

- MORE Information and Links

- Matrix - Spreadsheet of what Medicare Pays, Medi Gap pays and what little you pay

Medi-gap Plans C and F

Medi-gap Plans C and F will no longer be available to newly eligible Medicare beneficiaries beginning in January 2020.This is because CMS-Medicare decided they want those on Medicare to have more at stake when using benefits, so the Part B Deductible is no longer covered. Those who have previously purchase or were able to purchase Plan F, Innovative F, High F or F Extra, prior to January 1, 2020 can keep (Grandfathered) or enroll in the older plans!

For new enrollees, Plan G has same comprehensive benefits as Medicare Supplement Plan F, but Plan G does not cover the Part B deductible amount. Medicare now requires new people to pay the Part B deductible. Blue Shield Email dated 9.20.2017 * Choosing a Medi Gap Policy # 02110 * CA Health Advocates * AAFP.org * CMS.gov * CMS FAQ’s * AHCA of 2017 §102 would add $422,000,000 for 2017 * Small practices to be exempt? Modern Health Care 6.20.2017

Here’s rules on changing from F to G for lower premiums.

Medicare Access and CHIP Reauthorization Act of 2015 (MACRA),

(H.R. 2, Pub.L. 114–10)

commonly called the Permanent Doc Fix,

- MACRA establishes a new way to pay doctors who treat Medicare patients, revising the Balanced Budget Act of 1997.

- The reform is the largest in scale on the American health care system since the Affordable Care Act in 2010.

- It fixes the way Medicare doctors are reimbursed, fills in a funding gap and extends a popular children’s insurance program, CHIP.[1]

- There MACRA related regulations also address incentives for use of health IT by physicians. Wikipedia

Resources & Links

- CMS.gov MACRA

- CA Health Care Advocates 2020 Changes

- Section 401 of MACRA – Sec. 1882. [42 U.S.C. 1395ss] (z) prohibits the sale of Medigap policies that cover Part B deductibles to “newly eligible” Medicare beneficiaries defined as those individuals who:

- (a) have attained age 65 on or after January 1, 2020; or

- (b) first become eligible for Medicare due to age, disability or end-stage renal disease, on or after January 1, 2020. NAIC * SSA.gov *