Long Term Care, Nursing & Home Health Care

Start Here for Medicare Skilled Care, Medi-Cal, Home Care, Nursing Homes, and Long-Term Support

Families are often suddenly faced with confusing questions after an illness, injury, hospital stay, memory decline, or aging-related problem. People may hear terms like

skilled nursing facility,

home health care,

hospice,

activities of daily living,

Medi-Cal nursing home benefits,

or estate recovery — and not understand how they fit together.

Medicare is usually limited when it comes to long-term care. Medicare is generally strongest when the care is skilled, medical, rehabilitation-oriented, and temporary. Long-term custodial care — such as ongoing help with bathing, dressing, supervision, meals, dementia support, or permanent nursing home residence — is different.

Choose the Section That Best Fits Your Situation

Medicare Skilled Nursing & Home Health Care

Start here for hospital discharge, rehab, Medicare skilled nursing, home health, hospice, sub-acute care, and the 100-day skilled nursing question.

Medi-Cal Nursing Home & Estate Recovery

Start here for Medi-Cal nursing home eligibility, IHSS caregiving, home care help, paying for care, and estate recovery concerns.

Long-Term Care & Senior Support

Start here for aging parents, senior housing, ADLs, loneliness, social support, caregiving, and supportive living decisions.

Common Questions Families Ask

- Does Medicare pay for a nursing home?

See Long Term Care vs Medicare and

Skilled Nursing SNF & Home Health What Medicare Pays. - How long does Medicare pay for skilled nursing?

See Over 100 Days of Skilled Nursing?. - How do I find or compare a nursing home?

See Find and Pick a Medicare Nursing Home. - What is the difference between skilled nursing and sub-acute care?

See Skilled Nursing vs Sub Acute Care. - Does Medicare pay for home health care?

See Home Health Care – Medicare Coverage. - What about hospice?

See Hospice Coverage – Medicare. - What if dementia or Alzheimer’s is involved?

See Dementia & Alzheimer’s Medicare & ACA/ObamaCare Coverage. - Can Medi-Cal help pay for nursing home care?

See How to Qualify for Medi-Cal Nursing Home Benefits. - Can Medi-Cal help pay for a caregiver at home?

See Medi-Cal Can Pay for Home Caregiver IHSS. - Will Medi-Cal recover from the estate?

See Medi-Cal Nursing Home & Estate Recovery. - What are Activities of Daily Living?

See ADL Activities of Daily Living. - What if the real issue is senior housing or social support?

See Senior Housing Support and Finding a Place and

Togetherness, Loneliness & Social Determinants of Health.

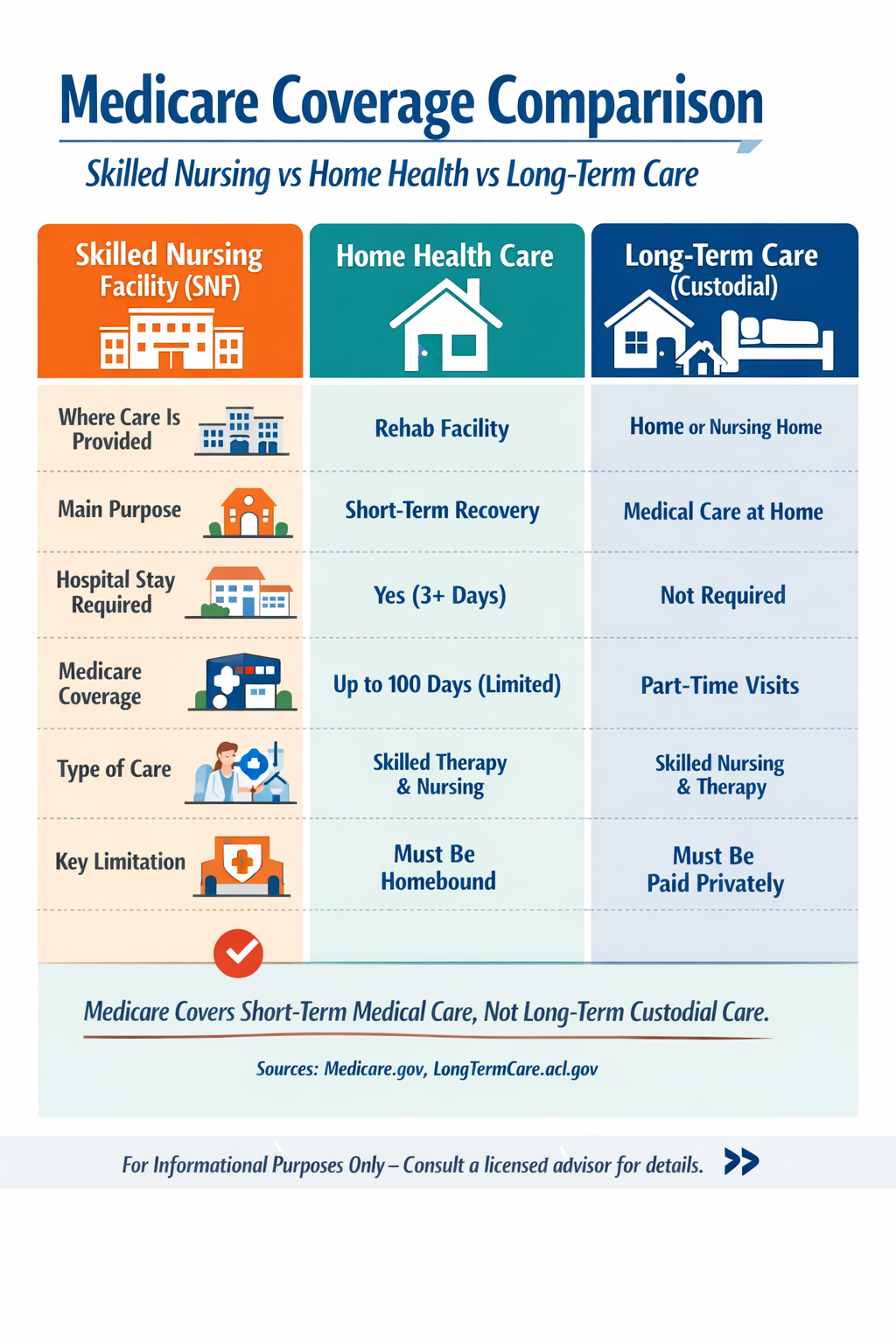

Medicare Coverage Comparison: Skilled Nursing vs Home Health vs Long-Term Care

| Type of Care | Skilled Nursing Facility (SNF) | Home Health Care | Long-Term Care (Custodial) |

|---|---|---|---|

| Where Care is Provided | Nursing facility / rehab center | Your home | Home, assisted living, or nursing home |

| Main Purpose | Short-term recovery after hospital stay | Medical care at home (nurse or therapy) | Help with daily living over time |

| Requires Hospital Stay? | Yes (typically 3+ inpatient days) | No (in many cases) | No |

| Type of Care | Skilled (therapy, IV meds, wound care) | Skilled (nurse visits, therapy) | Custodial (bathing, dressing, eating) |

| Medicare Coverage | Days 1–20: 100% Days 21–100: Copay After 100: Not covered |

Usually covered if medically necessary and homebound | Not covered by Medicare |

| Length of Coverage | Up to 100 days per benefit period | Intermittent / part-time visits | Ongoing / long-term |

| Key Limitation | Stops when skilled care is no longer needed | Must meet “homebound” and medical criteria | Must be paid out-of-pocket or insured |

| Common Misunderstanding | People think it covers long-term stays | People think it includes full-time caregivers | People think Medicare will pay — it won’t |

Bottom line: Medicare is designed for short-term medical care, not long-term living assistance.

Not sure which type of care applies to your situation?

✔ Get help understanding Medicare coverage

✔ Review long-term care planning options

✔ Compare Medicare Supplement plans

Long Term Care Brochures

- What’s on this page?

- CA Dept of Aging – Taking Care of Tomorrow

- Tax Qualified Premiums?

- Medi Cal no $$$ take your home…

- True Freedom Plans – Low Premium Home Health Care only

- 1035 Exchange

- ADL’s Activities of Daily Living

- Medicare Home Health Care Pamphlet

- Employer Groups

- Hospice

- Medicare Coverage for Skilled Nursing

- Low Budget – No money for premiums?

Links & Resources

- CA Health Care Advocates

- Dave Ramsey on when you need Long Term Care

- Rate Increases? Calif. Health Line 3.16.2016

- How will we pay for LTC? CA Health Line 3.16.2016

- Asset & Income Questionnaires? Do you have too much $$$ so you don't need LTC or so little it's Medi-Cal?

- Will annuities take care of your planning needs?

- Long Term Care.Gov

- Genworth - What is long Term Care?

- Total Living Coverage Brochure 20 pages Rev 11.2013

- Privileged Choice Flex Rev 6.2015

- the long term care guy.com

- Life Happens.Org - Long Term Care

- AHIP Who buys Long Term Care Insurance?

- Medicare Website on what Medicare Covers

- American Assoc. for Long Term Care Insurance

- Long Term Care.gov

- Sample Long Term Care Policy

- Genworth - Care & Support for your family

- Long Term Care Fact Sheet

- Veteran's Administration on Long Term Care

- Long Beach Breakers Hotel may lose license

- California Health Insurance Counseling and Advocacy Program (HICAP)

- LTC Consultant’s

- Long Term Care Glossary

- Home Health Care in CA

- long term care.gov

- California Department on Aging

- cal medicare.org/

- Steve Shorr’s Fraud Website

- care giver.org

- CHFC Reports 7.2013

- d i law Group.com/

- You Tube Video's on Mutual of Omaha Long Term Care....

- Borden Hamman Broker Training Video's

Elimination Period Explanation

LTC proposals usually show a 90 day wait for reimbursement. Cash benefits don’t have a waiting period. If you want a lower premium, you can have a longer wait.

Calendar Day Elimination Period –

Your policy has a waiting period before policy benefits begin. The elimination period starts on the first day you are chronically ill and you receive a covered service. Once the elimination period has been satisfied, benefits for covered services are paid to you each month, up to the maximum monthly benefit you select. Your options include:

• 90, 180 or 365 calendar days

On LTC policies, you only have to show you can’t do two of these 7 things (Activities of Daily Living).

What Is Long-Term Care?

Long-term care is the kind of personal care needed for tasks like bathing, dressing, eating, continence, toileting, and transferring (getting in or out of a bed or chair). These six basic needs are commonly referred to as Activities of Daily Living or ADLs. You might need help with one or more of these tasks because of a chronic medical or physical condition, or for an injury like Martha had. Frequently, people with Alzheimer’s disease or other dementias, also referred to as a cognitive impairment, need ongoing supervision. People who can no longer drive, manage their medications, or their finances need help with these tasks, which are referred to as Instrumental Activities of Daily Living or IADLs. These needs often occur first, before someone needs formal long-term care services.

Long-term care covers a broad range of needs and related services people receive in several

types of places. Services may include care at home or in a community program like adult day care, as well as care in an Assisted Living Facility (also known as a Residential Care Facility) or in a nursing home (also known as a Skilled Nursing Facility). Because long-term care is provided through a wide variety of services, it is also known as long-term services and supports, or LTSS. Taking Care of Tomorrow

Benefit Eligibility Triggers

Eligibility for accessing the benefits of a longterm care insurance policy depends on your inability to perform two “activities of daily living” (ADLs) out of a list of six, or when your cognitive ability is impaired. These are referred to as “benefit eligibility triggers.”

To be eligible for benefits you generally have to meet one of the two benefit eligibility triggers listed below. In addition, your doctor or other health care professional must draw up a Plan of Care, and certify that you are expected to need care for 90 days or more.

ADL’s – See above

Impairment of Cognitive Ability This is another benefit eligibility trigger that causes a person to need substantial supervision because of a severe cognitive impairment. People with Alzheimer’s disease or other types of dementia often need substantial supervision to protect themselves or others around them. Taking Care of Tomorrow

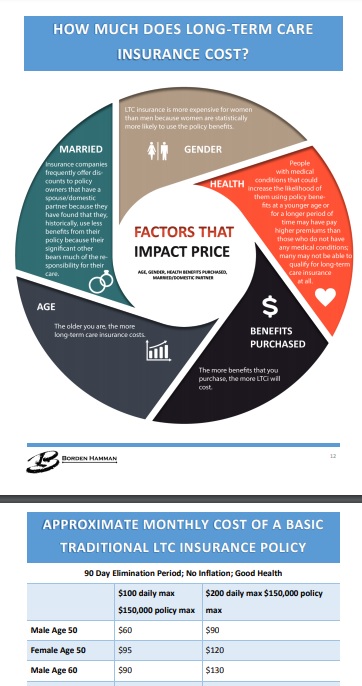

Ball Park Premiums

How much does Home & Long Term Care (Planning Guide) Coverage Cost?

proposal and needs assessment forms

The California Partnership for Long-Term Care

The California Partnership for Long-Term Care (Partnership) is dedicated to educating Californians on the need to plan ahead for their future long-term care and to consider private insurance as a vehicle to fund that care. The California Partnership for Long-Term Care is an innovative program of the State of California, Department of Health Care Services in cooperation with a select number of private insurance companies. These companies have agreed to offer high quality policies that must meet stringent requirements set by the Partnership and the State of California. These special policies are commonly called “Partnership policies”. Partnership policies take the guesswork out of ensuring you purchased a quality policy. In addition to many other consumer protection features, Partnership policies offer the special benefit of Medi-Cal Asset Protection.

WHAT’S NEW!

The Partnership has launched www.RUReadyCA.org an independent, easy-to-use website that offers a host of tools, information and calculators to help each Californian plan for their individually unique long-term care needs.

Learn more about the California Partnership for Long-Term Care on Facebook

Miscellaneous Information

- Children can pay the premium on their parents policy.

- Double check that your Long Term Carrier remains solvent and can hold their prices & promises Cal Broker Magazine *

- Husband & Wife Planning – 2 page brochure

- Benefits are generally income tax free, see the Taking Care of Tomorrow brochure for more details.

- Premium Tax deduction if medical expenses exceed 10% or 7.5% if over 65 Mutual of Omaha

- If your employer pays, it’s no income to you and the employer gets a deduction.

- Medi-cal (Medicaid) Welfare, might pay, however if you have $$$ or Property, they might put a lien on your home.

- The average cost for a private room in a nursing home in Los Angeles is $175/day. Average hourly home heath care is $15.

- Genworth Calculator

- Please email us [email protected] for more details.

FAQ’s

More and ask your own question

Can I be denied because of genetic testing?

No.

The Genetic Information Nondiscrimination Act of 2008 (Pub.L. 110–233, 122 Stat. 881, prohibits the use of genetic information in health insurance and employment. The Act prohibits group health plans and health insurers from denying coverage to a healthy individual or charging that person higher premiums based solely on a genetic predisposition to developing a disease in the future. The legislation also bars employers from using individuals’ genetic information when making hiring, firing, job placement, or promotion decisions.[1] The Act contains amendments to the Employee Retirement Income Security Act of 1974[3] and the Internal Revenue Code of 1986.[4]

CA Law – genomics law report.com * SB 559 – 2011 Padilla

Employer Groups

Long Term Care Plans for #Employer Groups

- Long Term Care for Employer Groups is a business expense deduction and the benefits are received tax free. bjfim.bordenhamman.com ♦ §7702 B ♦ §104 * IRC §104 (a) (3) (a) * IRS Publication 502 Medical & Dental Expenses * Internal Revenue Code §7702 b Long Term Care treated as Accident & Health, just like Section 106 * Bulletin 97-31

- Email us [email protected] for complementary quotes & information.

- C-Corps can benefit from complete (100%) deductibility of the tax-qualified long term care insurance premiums as a business expense. Long Term Care Insurance (LTCi) can be purchased for employees and owners.

- Premiums are not included as part of the employees gross income

- Coverage can be offered to spouses/domestic partners and retirees

- Payroll taxes are not required for premiums paid

- Executive carve-outs may be established to pay all or a portion of the premium for key employees

- S-Corps Partners or More Than 2% Shareholders

- Premiums paid for an owner are included in individual gross income.

- A self-employed health insurance deduction can be taken for tax-qualified LTCi premiums paid. LTCi premiums are considered a medical expense and are subject to the IRS age-based limits found in the first chart on the previous page.

- Self employed individuals can deduct tax-qualified LTCi premiums as a trade or business expense similar to traditional health and accident insurance premiums. A tax deduction is allowed for the self employed individual, for his or her spouse and other tax dependents. The annual deductible maximum for each covered individual is subject to the IRS age – based limits found in this chart. (Agent Manual)

- Technical Links & Resources

- 26 U.S. Code § 7702 B – Treatment of qualified long-term care insurance

- (a) (3) any plan of an employer providing coverage under a qualified long-term care insurance contract shall be treated as an accident and health plan with respect to such coverage [Section 106 tax deductibility of Medical Insurance Premiums]

- b (1) The term “qualified long-term care insurance contract” means – click on link above to view full code & definition.

- Revenue Procedure 2013 – 35 Maximum Contribution

- IRS Publication 502 Medical & Dental Expenses

Tax Incentives – Maximum Deduction For Individuals – Click to ENLARGE – from Agent Manual

Tax Incentives – Maximum Deduction For Individuals – Click to ENLARGE – from Agent Manual

Tax Qualified

WHAT IS A TAX #QUALIFIED LONG-TERM CARE POLICY?

Premiums may be tax deductible

Long-term care policies that use the federal standards to cover benefits are labeled as “Federally Tax Qualified”. Some or all of the premiums for these federally tax qualified policies may be deductible as a medical expense (over 7 or 10% of income & a maximum schedule for individuals) Medical expenses also include amounts paid for qualified long-term care services and limited amounts paid for any qualified long-term care insurance contract. Publication 502 on your federal and California income tax returns (depending on your age and the amount of annual premium). Health Insurance Portability and Accountability Act or HIPAA

Policies sold as federally tax qualified long-term care insurance use a standard of eligibility for benefits that may be stricter than the standards established in California for non-qualified policies. It may be easier to qualify for benefits from non-tax qualified policies that use the standards established by California. insurance.ca.gov *

Benefits are not taxable as income

Since the benefits – claims payments are treated the same as accident & health insurance Taking Care of Tomorrow Pages 29-31, 37-40 * Indiana.Gov * * our webpage * Indiana.Gov

Qualified Long-Term Care Services

Qualified long-term care services are necessary diagnostic, preventive, therapeutic, curing, treating, mitigating, rehabilitative services, and maintenance and personal care services (defined later) that are:

1. Required by a chronically ill individual, and

2. Provided pursuant to a plan of care prescribed by a licensed health care practitioner.

Chronically ill individual.

An individual is chronically ill if, within the previous 12 months, a licensed health care practitioner has certified that the individual meets either of the following descriptions.

1. He or she is unable to perform at least two activities of daily living without substantial assistance from another individual for at least 90 days, due to a loss of functional capacity. Activities of daily living are eating, toileting, transferring, bathing, dressing, and continence.

2. He or she requires substantial supervision to be protected from threats to health and safety due to severe cognitive impairment.

Maintenance and personal care services.

Maintenance or personal care services is care which has as its primary purpose the providing of a chronically ill individual with needed assistance with his or her disabilities (including protection from threats to health and safety due to severe cognitive impairment).

Qualified Long-Term Care Insurance Contracts

A qualified long-term care insurance contract is an insurance contract that provides only coverage of qualified long-term care services.

The contract must:

1. Be guaranteed renewable,

2. Not provide for a cash surrender value or other money that can be paid, assigned, pledged, or borrowed,

3. Provide that refunds, other than refunds on the death of the insured or complete surrender or cancellation of the contract, and dividends under the contract must be used only to reduce future premiums or increase future benefits, and

4. Generally not pay or reimburse expenses incurred for services or items that would be reimbursed under Medicare, except where Medicare is a secondary payer, or the contract makes per diem or other periodic payments without regard to expenses.

The amount of qualified long-term care premiums you can include is limited. You can include the following as medical expenses on Schedule A (Form 1040).

1. Qualified long-term care premiums up to the following amounts.

a. Age 40 or under – $410.

b. Age 41 to 50 – $770.

c. Age 51 to 60 – $1,530.

d. Age 61 to 70 – $4,090.

e. Age 71 or over – $5,110.

2. Unreimbursed expenses for qualified long-term care services.

Note. The limit on premiums is for each person.

Also, if you are an eligible retired public safety officer, you can’t include premiums for long-term care insurance if you elected to pay these premiums with tax-free distributions from a qualified retirement plan made directly to the insurance provider and these distributions would otherwise have been included in your income.

Resources & Links

- Taking Care of Tomorrow Pages 29-31, 37-40

- Wikipedia

- IRS Publication 502 Medical & Dental Expenses

Tax Incentives – Maximum Deduction For Individuals –

Click image to ENLARGE

1035 Exchange

Long Term Care Planning using 1035 #Exchange

United States Code §1035 Exchange – Long Term Care Planning

Broker ONLY

Asset-Care in California

Care Solutions Whole Life Core Brochure I-27754 (CA)

Asset-Care I I-28644 (CA)

Asset-Care II/III I-29681 (CA)

Asset Care IV I-29508 (CA)

Care Solutions Materials

The OneAmerica Difference (I-33305)

Care Solutions Process Guide (I-32803)

Claims 3-Step Process Flyer (I-27660)

Claims Concierge Brochure (I-27661)

Asset Care 2019

Care Solutions Product Guide (I-31591)

Asset Care Core Brochure (I-32407)

Care Solutions Product Overview (I-32414)

Plan for Care (I-36333)