CalSavers – California Small Business Retirement Savings Plans

Introduction

California law now requires that workers be automatically enrolled in a retirement savings account. Cal Savers – Secure Choice in an attempt to address growing fears that many workers will be financially unprepared to retire.

Cal Savers provides employees access to a retirement savings program without the administrative complexity, fees, or fiduciary liability of existing options for employers. Any employer with at least five employees that doesn’t already offer a workplace retirement savings vehicle

Email us [email protected] to set a time

to discuss your companies retirement needs and plans to offer

like one of these in IRS Publications 3998 or 560 will be required to either begin offering one via the private market or provide their employees access to CalSavers, by June 30, 2022. Eligible employers can register for CalSavers or opt out, if they have a retirement plan in force.

The CalSavers program ensures nearly all Californians have access to a workplace retirement savings program. CalSavers offers employees a completely voluntary, low cost, portable retirement savings vehicle with professionally managed investments and oversight from a public, transparent board of directors, chaired by the State Treasurer.

FAQ’s

- How do I certify that our business already has a retirement plan?

- You have to register and tell Cal Savers on their website.

- a listing of your employees including:

Name, Social Security Number, Birth date, email, mailing address, phone number

- a listing of your employees including:

- You have to register and tell Cal Savers on their website.

- What about part time & seasonal employees?

- All employees of a participating employer are eligible as long as they are at least age eighteen and have the status of an employee under California law. There are no minimum requirements based on hours worked or tenure with their employer.Employees are eligible to participate in CalSavers from of the first day they are hired. Participating Employers are required to upload them to the portal within 30 days of their hire date Cal Savers FAQ’s

- What’s a Simple Plan an Employer can get, to avoid Cal Savers and have a better and easier to administer program?

- Payroll Deduction IRAs for Small Businesses DOL.Gov

- Forbes.com explanation

- Automatic Enrollment? ez savings 4u.com

- Payroll Deduction IRAs for Small Businesses DOL.Gov

- FAQ’s on Cal Saver Website

- Employer Portal

Resources & Links

- To CalSave or Not to CalSave — That is the Question Cal Broker 3.1.2021

- Cal Savers Mandate – turn problem into opportunity CA Broker 1.2022

- irs.gov/retirement-plan-forms-and-publications

- Pros & Cons of CalSavers Benefits Resources.com 8.2019

- Betterment.com

- shrm.org/calsavers-registration-deadlines-for-california-employers

- 2021 year in review report says the state-run retirement program has a steady 70% participation rate, and 95% of savers opted into an automatic contribution increase. Plan Sponsor.com *

- 2021 Cal Savers Year in Review Report

- Cal Savers vs 401k Betterment.com

- Cal Savers FLYER

- The SECURE Act Setting Every Community Up for Retirement Enhancement Act of 2019 improves access to tax-advantaged retirement accounts, allows people to save more, and encourages employers to provide retirement plans. Betterment.com *

- New Plan Tax Credit FLYER

- Automatic Enrollment – Betterment.com *

- Don’t have a 401(k) through work? Californians have CalSavers and other options LA Times 1.21.2022

Jump to section on

| Payroll Deduction IRA |

Business #Retirement Plans # 3998 Rev 11/2023

- What you should know about your retirement plan dol.gov pdf

- Choosing a Retirement Solution for Your Small Business dol.gov

- Taking the Mystery Out of Retirement Planning dol.gov

- Top 10 Ways to Prepare for Retirement dol.gov

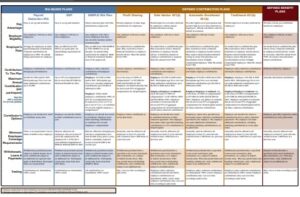

- Side by Side Chart of various retirement plans

- Retirement Plans for Small Biz

- irs.gov/retirement-plans/types-of-retirement-plans

IRS Publication 560- Profit Sharing Plans for Small Biz Publication # 4806 Irs.gov pdf Website DOL.gov

- Profit-Sharing Plans Defined Benefit Plans

- Money Purchase Plans

- Employee Stock Ownership Plans (ESOPs)

- Governmental Plans 457 Plans

- Help with Choosing a Retirement Plan

- What you should know about your Retirement Plan DOL.Gov

401 K Plans for Small Business – IRS # 4222

- Retirement Toolkit dol pdf

- Retirement Plans that don't have tax benefits - you can pick and choose who gets in!

- Lots of Benefits when you participate or set up an employee retirement plan Publication # 4118

- irs.gov/retirement-plans

- saving matters.dol.gov

- dol.gov/choosing-a-plan

- irs.gov/retirement-plans-for-small-entities-and-self-employed

- dol.gov/ask-a-question

- Small Business Retirement Savings Advisor DOL.gov

- QDROs The Division of Retirement Benefits Through Qualified Domestic Relations Orders Dol.gov pdf

- Get a Retirement Plan Proposal

- Department of Labor, Social Security & Medicare – Retirement Toolkit 9 pages

- BROKER ONLY iamsinc.com

- Our Web pages on:

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

IRA Individual Retirement Account

Payroll Deduction IRA for Small Biz # 4587

A payroll deduction individual retirement account (IRA) is an easy way for businesses to give employees an opportunity to save for retirement. The employer sets up the payroll deduction IRA program with a bank, insurance company, or other financial institution, and then the employees choose whether to participate. Employees decide how much they want deducted from their paychecks and deposited into the IRA. They may also have a choice of investments, depending on the IRA provider.

Many people not covered by an employer retirement plan could save through an IRA, but don’t. A payroll deduction IRA at work can simplify the process and encourage employees to get started.

Under Federal law, See Publication 590 A individuals saving in a traditional IRA may be able to receive some tax advantages on the money they contribute, and the earnings on the contributions are tax-deferred. For individuals saving in a Roth IRA, contributions are after-tax and the earnings are tax-free.

Advantages of a payroll deduction IRA:

- Simple for employees to set up an IRA.

- Employees make all of the contributions. There are no employer contributions.

- Many employees find smaller, regular contributions a more manageable way to save.

- Low administrative costs.

- No filings with the government to establish the program or any annual reports.

- However

- You have to register and tell Cal Savers on their website.

- Payroll deduction IRAs with automatic enrollment are considered a qualified plan Cal Savers *

- However

- No minimum number of employees required.

- Program will not be considered an employer retirement plan subject to Federal reporting and fiduciary responsibility requirements as long as the employer keeps its involvement to a minimum.

- May help attract and retain quality employees.

- Learn more - read Payroll Deduction IRA for Small Biz # 4587

Links & Resources

- Our main webpage on IRA's

- capital group.com/payroll-deduction-IRAs

- Cohesive Insurance Peter Buechler

- Payroll Deduction IRAs for Small Businesses Dol.gov

- SIMPLE IRA Plans for Small Businesses Dol.gov

- Taking the Mystery Out of Retirement Planning DOL.Gov

Publication 590 A

#Contributions to IRA's

-

Publication 590 Individual Retirement Arrangements (IRAs)

- Traditional IRAs

- Who Can Open a Traditional IRA?

- When Can a Traditional IRA Be Opened?

- How Can a Traditional IRA Be Opened?

- How Much Can Be Contributed?

- When Can Contributions Be Made?

- How Much Can You Deduct? What if You Inherit an IRA?

- Can You Move Retirement Plan Assets? When Can You Withdraw or Use Assets?

- What Acts Result in Penalties or Additional Taxes?

- What assets can you put into your IRA?

- Roth IRAs

- Publication 590-A HTML

-

and Publication 590-B Distributions from Individual Retirement Arrangements (IRAs)

- Simple IRA for Small Biz # 4334

- Payroll Deduction IRA for Small Biz # 4587

- Payroll Deduction IRAs

- Simple IRA Plan Checklist Publication # 4284

- SEP Retirement Plans for Small Biz # 4333

- SEP Check list # 4258

- Individual Retirement Arrangements (IRAs)

- Roth IRAs 401(k) Plans 403(b) Plans

- SIMPLE IRA Plans (Savings Incentive Match Plans for Employees)

Annuities

-

What Seniors Need to know #about Annuities - HTML CA DOI Pamphlet

- Buyer's Guides NAIC - National Association of Insurance Commissioners

- The NAIC’s Suitability in Annuity Transactions Model Regulation makes sure that consumers receive better information, in plain English, to help them make informed decisions, while preserving access to valuable financial services.

- Are Annuities Taxable? Annuity.org

- Nonqualified vs. Qualified Annuities Annuity.org

- Our webpages on Annuities & Retirement

IRS Types of Retirement Plans

- Individual Retirement Arrangements (IRAs)

- Roth IRAs 401(k) Plans 403(b) Plans

- SIMPLE IRA Plans (Savings Incentive Match Plans for Employees)

- SEP Plans (Simplified Employee Pension)

- SARSEP Plans (Salary Reduction Simplified Employee Pension)

- Payroll Deduction IRAs

- Profit-Sharing Plans Defined Benefit Plans

- Money Purchase Plans

- Employee Stock Ownership Plans (ESOPs)

- Governmental Plans 457 Plans

- 409A Nonqualified Deferred Compensation Plans

- Help with Choosing a Retirement Plan

-

Side by Side Chart of various retirement plans

Steve Shorr

Website Video #Introduction

Bill Summary

The legislation creates a state-run retirement program for workers who don’t have an employer-sponsored plan, many of them working in lower-wage positions. It requires employers to automatically enroll their workers and deduct money from each paycheck, though workers can opt out or set their own savings rate. The account could also be carried from job to job.

The bill would require the opt-out form disseminated by the Employment Development Department to be used to create an option for employees to elect to opt out of the program, as specified. The bill would, commencing 6 months after the program is ready to proceed, require the Employment Development Department to assess a penalty on any eligible employer that fails to make the program available to eligible employees, as specified. The bill also would make a statement of legislative findings. The bill would provide that the state would have no liability for the payment of the benefits under the program, as specified.

The bill, upon sufficient funds being made available through a nonprofit or private entity or federal funding, would require the board to conduct a market analysis to determine whether the necessary conditions for implementation can be met, as specified. The bill would require moneys made available to conduct the market analysis to be deposited in the Secure Choice Retirement Savings Program Fund which would be created in the State Treasury. The bill would provide that the operational provisions of the California Secure Choice Retirement Savings Trust Act shall be operative only if the board determines that, based on the market analysis, the provisions will be self-sustaining, and sufficient funds are made available through a nonprofit or private entity, federal funding, or the annual Budget Act, as specified, to allow the board to implement the program until the trust has sufficient funds to be self-sustaining. The bill would require the board to ensure that an insurance, annuity, or other funding mechanism is in place at all times that protects the value of individuals’ accounts and protects, indemnifies, and holds the state harmless at all times against any and all liability in connection with funding retirement benefits pursuant to these provisions.

The bill would prohibit the board from implementing the program if the IRA arrangements offered fail to qualify for the favorable federal income tax treatment ordinarily accorded to IRAs under the Internal Revenue Code, or if it is determined that the program is an employee benefit plan under the federal Employee Retirement Income Security Act of 1974. Business Insider * Government Code §100,000 * Text of Law

SB 1234, De León. Retirement savings plans. Existing federal law provides for tax-qualified retirement plans and individual retirement accounts or individual retirement annuities by which private citizens may save money for retirement.

This bill would enact the California Secure Choice Retirement Savings Trust Act, which would create the California Secure Choice Retirement Savings Trust to be administered by the California Secure Choice Retirement Savings Investment Board, which would also be established by the bill. The bill would require eligible employers, as defined, to offer a payroll deposit retirement savings arrangement so that eligible employees, as defined, could contribute a portion of their salary or wages to a retirement savings program account in the California Secure Choice Retirement Savings Program, as specified. The bill would require eligible employees to participate in the program, unless the employee opts out of the program, as specified. The bill would specify risk management and investment policies that the board would be subject to regarding administration of the program. The bill would require a specified percentage of the annual salary or wages of an eligible employee participating in the program to be deposited in the California Secure Choice Retirement Savings Trust, which would be segregated into a program fund and an administrative fund, both of which would be continuously appropriated to the board for purposes of the act. The bill would limit expenditures from the administrative fund, as specified. The bill would also authorize the board to establish a Gain and Loss Reserve Account within the program fund.

Learn More==>

San Francisco Chronicle 3.28.2016

Chapter 15 – Calsavers Retirement Savings Board

- § 10000 – Definitions

- § 10001 – Eligible Employers

- § 10002 – Employer Registration

- § 10003 – Participating Employer Duties

- § 10004 – Employee Enrollment

- § 10005 – Default Program Options and Alternative Elections for Contributions, Automatic Escalation, and Investment Options for Participants

- § 10006 – Individual Participation

- § 10007 – Contributions and Distributions

- § 10008 – Enforcement of Employer Compliance

- Note however, that Congress might “attack” this bill.

- Learn More==>

- U.S. Court of Appeals Upholds CalSavers Program JD Supra.com

- LA Times 2.9.2017

- The stage is set for high-stakes court battle by rolling back an Obama-era rule that made it easier legally for states like California to set up 401(k)-type plans for private-sector workers whose jobs don’t offer such benefits

- At issue is a decades-old consumer protection law, the Employee Retirement Income Security Act of 1974 — or ERISA, in industry jargon — that sets minimum standards for private-sector pension plans. Before Obama left office, the Department of Labor wrote regulations to make it easier for local governments and states to establish “auto IRAs” such as Secure Choice without running afoul of the law, waiving some of the requirements deemed too burdensome for small businesses.

- Those Department of Labor rules are what Congress killed this week. US Senate kills ERISA requirements Mercury News 5.3.2017

- K & L Gates 5.17.2017 analysis

- Federal H. R. 2954 To increase retirement savings, simplify and clarify retirement plan rules, and for other purposes.