Business Retirement Plans for California Employers, Small Business Owners & Self-Employed People

- compare CalSavers vs a private retirement plan,

- SEP IRA plans,

- 401(k) plans,

- SIMPLE IRA choices, profit sharing, rollovers, annuities,

- Social Security and related retirement planning issues.

California employer note: Effective January 1, 2026, California employers with one or more employees generally must provide access to a qualified retirement program or certify a valid exemption with CalSavers. That does not automatically mean CalSavers is the best choice. A private plan may be a better fit when the owner wants larger tax-deductible contributions, employer matching, profit sharing, better employee recruiting, or plan design flexibility. Start with our page on CalSavers Mandate vs Private Pension Plan, then compare the other options below.

Which Retirement Plan Question Are You Trying to Answer?

Do I need to comply with CalSavers?

If your business has California employees and no qualified retirement plan, review our CalSavers employer mandate page. CalSavers can satisfy the mandate, but a private 401(k), SEP, SIMPLE IRA or other qualified plan may provide additional business-owner benefits.

Are you self-employed or a very small employer?

A SEP IRA Plan for self-employed and small business owners is often the simple starting point when the employer wants discretionary, tax-deductible contributions and does not need employee salary deferrals.

Do employees need to save from payroll?

A 401(k) plan or SIMPLE IRA allows employee payroll contributions. A 401(k) can offer more features, higher potential savings and employer design flexibility, while a SIMPLE IRA can be easier to administer for smaller employers.

Leaving a job or closing a plan?

Before cashing out an old plan, review 401(k) Rollover to IRA choices. Rollovers can affect taxes, investment control, creditor protection, future backdoor Roth planning and required minimum distributions.

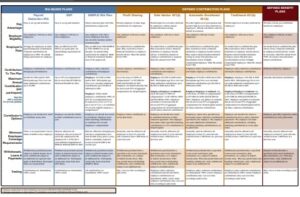

Compare Business Retirement Plan Choices

| Plan or Strategy | Good Fit | Key Planning Point |

|---|---|---|

| CalSavers | California employers that need a basic way to comply when they do not offer their own qualified retirement plan. | CalSavers is a state-facilitated payroll deduction IRA. It has limited employer responsibilities, no employer contributions and no employer fiduciary responsibility, but it is not the same as designing your own employer retirement plan. |

| SEP IRA | Self-employed people, owner-only businesses and small employers that want relatively simple employer contributions. | Employer contributions are generally discretionary. Employee salary deferrals are not allowed in a SEP, so it may not solve every employee-savings or owner-savings goal. |

| SIMPLE IRA | Small employers that want employee salary reduction contributions without the complexity of a traditional 401(k). | Generally easier than a 401(k), but employer contribution rules and lower limits may make it less attractive for high-income owners who want maximum savings. |

| 401(k) / Safe Harbor 401(k) | Employers who want employee deferrals, employer matching, Roth features, owner savings opportunities and recruiting value. | More flexible than CalSavers or a SIMPLE IRA, but requires plan administration, testing or safe-harbor design, investment oversight and employee notices. |

| Profit Sharing | Businesses that want discretionary employer contributions, often combined with a 401(k). | Can be useful when profits vary. Plan design matters, especially when owners and highly compensated employees want meaningful contributions. |

| Defined Benefit / Cash Balance | Established profitable businesses and older owners who may need larger deductible retirement contributions. | Can allow much larger contributions than defined contribution plans, but requires actuarial design, required funding and careful professional administration. |

| 401(k) Rollover to IRA | Employees, owners or retirees leaving a job, retiring, selling a business or terminating a plan. | Compare leaving money in the plan, moving to a new employer plan, rolling to an IRA or using annuities. Do not cash out without understanding taxes and penalties. |

Tax credit planning: Eligible small employers may be able to claim retirement plan startup tax credits, and an additional credit may apply when an eligible auto-enrollment feature is added. Credits and deductions are tax matters, so coordinate with your CPA or tax adviser before choosing the plan design.

401(k) Plans for Small Business

401(k) plans are often the best-known employer retirement plan because employees can contribute from payroll and employers may add matching, profit sharing or safe-harbor contributions. They can be especially useful when owners, highly compensated employees and key employees want more than a basic payroll deduction IRA.

Before selecting a 401(k), ask about plan administration costs, investment lineup, payroll integration, employee notices, Form 5500 reporting, nondiscrimination testing, safe-harbor design, Roth options, loans, hardship withdrawals, vesting and whether a pooled employer plan or multiple employer plan structure is appropriate.

- DOL / IRS: 401(k) Plans for Small Businesses

- IRS: 401(k) and Profit-Sharing Contribution Limits

- IRS / DOL Publication 4674: Automatic Enrollment 401(k) Plans for Small Businesses

Questions to Ask Before Setting Up a Plan

- How many employees do you have in California, and are you currently subject to CalSavers?

- Is the main goal owner tax savings, employee retention, mandate compliance, employee payroll savings or a rollover?

- Do employees need to contribute from payroll, or is the employer contribution enough?

- Do you want employer matching, profit sharing, Roth contributions or loan provisions?

- Do you need a simple low-cost plan, or is professional plan design worth the added administration?

- Who will coordinate payroll, plan administration, investment selection, notices and tax reporting?

Ask Steve About Business Retirement Plan Options

Steve Shorr Insurance can help you compare the insurance and retirement planning pieces, explain the practical differences between CalSavers and private plans, and help you coordinate with plan administrators, payroll providers, CPAs and other professionals. Steve Shorr is not a tax attorney, CPA or plan administrator; this page is for general educational purposes.

Other Retirement Planning Pages

This business retirement page should send readers to the related retirement planning pages as soon as the topic comes up, rather than waiting for a long list at the bottom.

- Benefits of Retirement Planning

- Annuities & MAGI Income Taxation Exemption

- TSA / Teacher Retirement Plans – Tax Sheltered Annuities

- IRA – Individual Retirement Account Tax Deductible & Roth

- Social Security – Retirement Benefits

- Long Term Care Nursing & Home Health Care

- Life Insurance & Estate Planning

- Employer Group Health Insurance

- MAGI – Modified Adjusted Gross Income

Government Resources

- DOL: Choosing a Retirement Plan for Small Business

- IRS: Retirement Plan Resources for Small Employers and Self-Employed

- IRS Publication 560: Retirement Plans for Small Business

- IRS / DOL Publication 3998: Choosing a Retirement Solution for Your Small Business

- IRS / DOL Publication 4222: 401(k) Plans for Small Businesses

- IRS / DOL Publication 4806: Profit Sharing Plans for Small Businesses

- DOL: What You Should Know About Your Retirement Plan

- DOL / Social Security / Medicare: Retirement Toolkit

- DOL: Top 10 Ways to Prepare for Retirement

- IRS: Current Retirement Plan Dollar Limits and Contribution Limits

- IRS: Retirement Plan Startup Costs Tax Credit

- Official CalSavers Website

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

Business #Retirement Plans # 3998 Rev 11/2023

- What you should know about your retirement plan dol.gov pdf

- Choosing a Retirement Solution for Your Small Business dol.gov

- Taking the Mystery Out of Retirement Planning dol.gov

- Top 10 Ways to Prepare for Retirement dol.gov

- Side by Side Chart of various retirement plans

- Retirement Plans for Small Biz

- irs.gov/retirement-plans/types-of-retirement-plans

IRS Publication 560- Profit Sharing Plans for Small Biz Publication # 4806 Irs.gov pdf Website DOL.gov

- Profit-Sharing Plans Defined Benefit Plans

- Money Purchase Plans

- Employee Stock Ownership Plans (ESOPs)

- Governmental Plans 457 Plans

- Help with Choosing a Retirement Plan

- What you should know about your Retirement Plan DOL.Gov

401 K Plans for Small Business – IRS # 4222

- Retirement Toolkit dol pdf

- Retirement Plans that don't have tax benefits - you can pick and choose who gets in!

- Lots of Benefits when you participate or set up an employee retirement plan Publication # 4118

- irs.gov/retirement-plans

- saving matters.dol.gov

- dol.gov/choosing-a-plan

- irs.gov/retirement-plans-for-small-entities-and-self-employed

- dol.gov/ask-a-question

- Small Business Retirement Savings Advisor DOL.gov

- QDROs The Division of Retirement Benefits Through Qualified Domestic Relations Orders Dol.gov pdf

- Get a Retirement Plan Proposal

- Department of Labor, Social Security & Medicare – Retirement Toolkit 9 pages

- BROKER ONLY iamsinc.com

- Our Web pages on:

401 #Kplans

401k plans are the most popular type of retirement plan used today. They can be a powerful tool in promoting financial security in retirement and are a valuable option for businesses considering a retirement plan, providing benefits to employees and their employers.

If you are retiring or laid off… Check with us on the options to Roll Over you current 401K or Pension Plan. Check out our annuities & IRA’s

- IRS Website on Contribution Limits

- Automatic 401k enrollment for small biz publication # 4674

-

401 K Plans for Small Business – IRS.gov # 4222

Steve Shorr

Website Video #Introduction

Links & Resources

- Department of Labor Publication Dol.gov

- Can the Retiree Health Benefits Provided By Your Employer Be Cut? Dol.gov pdf

Administrators