IRA (Individual Retirement Account)

Social Security just isn’t enough!

IRA Introduction

- An IRA individual retirement account allows you to put away money for retirement and the IRS helps you do it by letting you pay less taxes based on the amount that you invest. This is in addition to Social Security and/or your Employer Retirement Plan.

- IRS Publication #590, explains how your allowed you to save for Retirement – Tax Deferred. We generally fund them with Annuities It’s like a bank account, but with an Insurance Company and it can give you a GUARANTEED income for life.

- Mandatory Retirement Option for Employers with 5 or more employees

IRS Contributions – Tax Deductible

- Contributions you make to an IRA may be fully or partially deductible, depending on which type of IRA you have and on your circumstances; and

- Generally, amounts in your IRA (including earnings and gains) aren’t taxed until distributed. In some cases, amounts aren’t taxed at all if distributed according to the rules. IRS.gov Publication 590 *

- Covered CA MAGI Income – Contributions & Retirement Income?

FAQ’s

- Jump to section on:

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

Retirement Calculators – IRS Publications

Will you have #enough for retirement?

Click on image to enlarge

Source = Money.com

Retirement #Calculators

- 360 Degrees of Financial Literacy

- American Institute of Certified Public Accountants - 401(k) plans

- American Institute of Certified Public Accountants - Retirement Planning Basics

- Blueprint Income - Build A Personal Pension Calculator

- Choose-to-Save - Ball Park E$timate

- Financial Calculators: Retirement Savings

- ssa.gov/estimator

- Estimate Your Life Expectancy

- Other Benefit Calculators

- When to Start Receiving Retirement Benefits #10147 SSA.Gov

- Other Things To Consider

- Retirement Toolkit DOL

- my Social Security account

- fairly geeky, there are good spreadsheets at www.analyze now/ but they are not easy

- Forbes 5 calculators

- Smart Asset.com Social Security Calculator

Publication 590 A

#Contributions to IRA's

-

Publication 590 Individual Retirement Arrangements (IRAs)

- Traditional IRAs

- Who Can Open a Traditional IRA?

- When Can a Traditional IRA Be Opened?

- How Can a Traditional IRA Be Opened?

- How Much Can Be Contributed?

- When Can Contributions Be Made?

- How Much Can You Deduct? What if You Inherit an IRA?

- Can You Move Retirement Plan Assets? When Can You Withdraw or Use Assets?

- What Acts Result in Penalties or Additional Taxes?

- What assets can you put into your IRA?

- Roth IRAs

- Publication 590-A HTML

-

and Publication 590-B Distributions from Individual Retirement Arrangements (IRAs)

- Simple IRA for Small Biz # 4334

- Payroll Deduction IRA for Small Biz # 4587

- Payroll Deduction IRAs

- Simple IRA Plan Checklist Publication # 4284

- SEP Retirement Plans for Small Biz # 4333

- SEP Check list # 4258

- Individual Retirement Arrangements (IRAs)

- Roth IRAs 401(k) Plans 403(b) Plans

- SIMPLE IRA Plans (Savings Incentive Match Plans for Employees)

Payroll Deduction & Roth IRA

Payroll Deduction IRA for Small Biz # 4587

A payroll deduction individual retirement account (IRA) is an easy way for businesses to give employees an opportunity to save for retirement. The employer sets up the payroll deduction IRA program with a bank, insurance company, or other financial institution, and then the employees choose whether to participate. Employees decide how much they want deducted from their paychecks and deposited into the IRA. They may also have a choice of investments, depending on the IRA provider.

Many people not covered by an employer retirement plan could save through an IRA, but don’t. A payroll deduction IRA at work can simplify the process and encourage employees to get started.

Under Federal law, See Publication 590 A individuals saving in a traditional IRA may be able to receive some tax advantages on the money they contribute, and the earnings on the contributions are tax-deferred. For individuals saving in a Roth IRA, contributions are after-tax and the earnings are tax-free.

Advantages of a payroll deduction IRA:

- Simple for employees to set up an IRA.

- Employees make all of the contributions. There are no employer contributions.

- Many employees find smaller, regular contributions a more manageable way to save.

- Low administrative costs.

- No filings with the government to establish the program or any annual reports.

- However

- You have to register and tell Cal Savers on their website.

- Payroll deduction IRAs with automatic enrollment are considered a qualified plan Cal Savers *

- However

- No minimum number of employees required.

- Program will not be considered an employer retirement plan subject to Federal reporting and fiduciary responsibility requirements as long as the employer keeps its involvement to a minimum.

- May help attract and retain quality employees.

- Learn more - read Payroll Deduction IRA for Small Biz # 4587

Links & Resources

- Our main webpage on IRA's

- capital group.com/payroll-deduction-IRAs

- Cohesive Insurance Peter Buechler

- Payroll Deduction IRAs for Small Businesses Dol.gov

- SIMPLE IRA Plans for Small Businesses Dol.gov

- Taking the Mystery Out of Retirement Planning DOL.Gov

- Reminders

- Introduction

- Contributions not reported.

- What Is a Roth IRA?

- Get a Retirement Plan Proposal

- Are Distributions Taxable?

Collecting Your Pension – Retirement – IRA

Required Minimum Distributions RMD

Hardships, Early Withdrawals and Loans

- irs.gov/hardships-early-withdrawals-and-loans

- RMD IRS Website

- Schawb.com RMD Calculator

- More resources

- Required Minimum Distributions IRS.gov

- When can a retirement plan distribute benefits? IRS.gov

- Considering a loan from your 401(k) plan? IRS.gov

- Types of Retirement Plan Benefits - lump sums, annuities and spousal rights IRS.gov

- Rollovers to and from other retirement plans IRS.gov

- Retirement Topics - Hardship Distributions IRS.gov

- Retirement Topics - Loans IRS.gov

- Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs)

- Publication 554, Tax Guide for Seniors

Brother – Sister – Sibling Side Pages Subpages

- View our website with your Desktop or Tablet for the most information

Tax Guide for Seniors Publication 554

Business #Retirement Plans # 3998 Rev 11/2023

- What you should know about your retirement plan dol.gov pdf

- Choosing a Retirement Solution for Your Small Business dol.gov

- Taking the Mystery Out of Retirement Planning dol.gov

- Top 10 Ways to Prepare for Retirement dol.gov

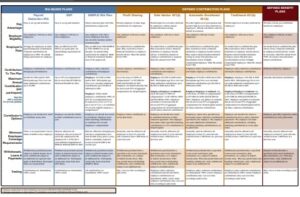

- Side by Side Chart of various retirement plans

- Retirement Plans for Small Biz

- irs.gov/retirement-plans/types-of-retirement-plans

IRS Publication 560- Profit Sharing Plans for Small Biz Publication # 4806 Irs.gov pdf Website DOL.gov

- Profit-Sharing Plans Defined Benefit Plans

- Money Purchase Plans

- Employee Stock Ownership Plans (ESOPs)

- Governmental Plans 457 Plans

- Help with Choosing a Retirement Plan

- What you should know about your Retirement Plan DOL.Gov

401 K Plans for Small Business – IRS # 4222

- Retirement Toolkit dol pdf

- Retirement Plans that don't have tax benefits - you can pick and choose who gets in!

- Lots of Benefits when you participate or set up an employee retirement plan Publication # 4118

- irs.gov/retirement-plans

- saving matters.dol.gov

- dol.gov/choosing-a-plan

- irs.gov/retirement-plans-for-small-entities-and-self-employed

- dol.gov/ask-a-question

- Small Business Retirement Savings Advisor DOL.gov

- QDROs The Division of Retirement Benefits Through Qualified Domestic Relations Orders Dol.gov pdf

- Get a Retirement Plan Proposal

- Department of Labor, Social Security & Medicare – Retirement Toolkit 9 pages

- BROKER ONLY iamsinc.com

- Our Web pages on:

https://www.msn.com/en-us/money/news/what-donald-trump-s-new-retirement-plans-mean-for-millions-of-americans/ar-AA1X2nxt