Advantages of getting an Annuity

Safety of Principal!

Annuity Introduction

Most people have worked hard all their life accumulating their “nest-egg”. They should not put their money in risky investments, especially our senior citizens. Most seniors are more concerned about the “return OF their money than the return ON their money”. Annuities are considered to be safe investments for the following reasons:

- No market risk

- Backed by the financial strength of large life insurance companies who are required to set aside a portion of their assets (reserves) to cover claims.

- They also spread their risk through the industry’s reinsurance network, i.e. several companies share in a particular risk.

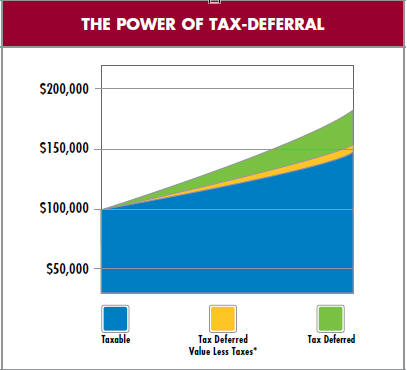

- Tax Deferral – Taxes are paid only when money is received. IRC Section 72 This results in a much faster cash build-up. Your principal grows because you receive:

- 1) interest on the principal;

- 2) interest on the interest;

- 3) interest on the money that normally would have been paid in taxes.

- Competitive Interest Rates – At present, and historically, annuities outperform CD’s and money market accounts.

- Accessibility– One of the biggest concerns, especially with seniors, is “Do I Have Access to My Money, Should I Need It?” There are a number of choices:

- Withdraw interest as needed, monthly, quarterly, etc.

- Exercise free withdrawal privilege

- Total surrender

- Annuitize (choose one of a number of income options)

- Lifetime Income – Annuity Calculator

- Get your annuity from [email protected] just use the tool to get an instant idea of what the market is.

- Lifetime Income – Annuity Calculator

- Avoids Probate – By naming a beneficiary, your annuity account is paid directly to a named individual, making it accessible and eliminating probate costs.

- Interest Rate Guarantees – Almost all annuity contracts have minimum rate guarantees…the rate can never go below a specified amount.

- Current Income Reduction – CD’s, money market accounts, savings accounts, etc. require current taxation of interest earned even if it is not taken. Annuities are taxed only upon receipt of interest.

- Lifetime Income Option – Annuities are the only investment vehicles available that guarantee you cannot outlive your monthly payments

- Retirement Annuities: Know the Pros and Cons Investopedia

- General Information on Annuities Annuity.org

Avoid Risk and invest in a tax deferred annuity!

Your PRINCIPLE & INTEREST is FULLY GUARANTEED at all times!!

You get:

- Triple Compounding

- Tax Savings

- No Fees or Load Charges

- Competitive Interest

- Probate Avoidance

- No Market Risk

- Does not affect taxation of your social security

- Liquidity (Ability to withdraw funds) (Brsan)

- Jump to section on:

Power of Tax Deferral -

from North American Brochure

-

What Seniors Need to know #about Annuities - HTML CA DOI Pamphlet

- Buyer's Guides NAIC - National Association of Insurance Commissioners

- The NAIC’s Suitability in Annuity Transactions Model Regulation makes sure that consumers receive better information, in plain English, to help them make informed decisions, while preserving access to valuable financial services.

- Are Annuities Taxable? Annuity.org

- Nonqualified vs. Qualified Annuities Annuity.org

- Our webpages on Annuities & Retirement

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

IRS Tax Publications

Publication 590 A

#Contributions to IRA's

-

Publication 590 Individual Retirement Arrangements (IRAs)

- Traditional IRAs

- Who Can Open a Traditional IRA?

- When Can a Traditional IRA Be Opened?

- How Can a Traditional IRA Be Opened?

- How Much Can Be Contributed?

- When Can Contributions Be Made?

- How Much Can You Deduct? What if You Inherit an IRA?

- Can You Move Retirement Plan Assets? When Can You Withdraw or Use Assets?

- What Acts Result in Penalties or Additional Taxes?

- What assets can you put into your IRA?

- Roth IRAs

- Publication 590-A HTML

-

and Publication 590-B Distributions from Individual Retirement Arrangements (IRAs)

- Simple IRA for Small Biz # 4334

- Payroll Deduction IRA for Small Biz # 4587

- Payroll Deduction IRAs

- Simple IRA Plan Checklist Publication # 4284

- SEP Retirement Plans for Small Biz # 4333

- SEP Check list # 4258

- Individual Retirement Arrangements (IRAs)

- Roth IRAs 401(k) Plans 403(b) Plans

- SIMPLE IRA Plans (Savings Incentive Match Plans for Employees)

#Pension & Annuity Income

Publication 575 pdf * HTML

- VIDEO Basic taxation of annuities BROKER ONLY

- About 1099-R

- Required Minimum Distributions FAQ's IRS.Gov

- Lifetime Income - Annuity Calculator

- Get your annuity from [email protected] just use the tool to get an instant idea of what the market is.

How much of your #Pensiona & Annuity Income goes on line 4a & 5a of IRS 1040 and

thus counts towards MAGI Income for Covered CA subsidies?

See our new webpage