Evidence of Coverage (EOC):

The Contract That Explains Your Health Insurance

Before reading a hundred laws, start with the document that actually governs your plan.

When people ask me whether a service is covered, how prior approval works, what the copay is, whether they can use a doctor out of network, or what happens when they travel, the answer is usually in the Evidence of Coverage (EOC).

The Evidence of Coverage is the contract between the policyholder and the insurance company or health plan. It explains what is covered, what is excluded, how cost sharing works, and the rules for using the coverage.

A lot of people do not want to read 200 pages, and I understand that. But when you want the real answer about your plan, the EOC is usually where you will find it in plain English.

Why the EOC Matters

You can read summaries, brochures, blog posts, statutes, regulations, and advertisements, but your own EOC tells you how your specific plan works.

The EOC usually explains:

- Covered benefits

- Exclusions and limitations

- Copays, deductibles, and coinsurance

- Prior authorization or referral requirements

- Emergency and urgent care rules

- Out-of-network rules

- Prescription drug coverage

- Appeal and grievance rights

- Definitions that can change how coverage works

You Do Not Have to Read the Whole Policy at Once

Most people are not going to sit down and read an entire policy from beginning to end. The faster way is to use the table of contents, the PDF bookmarks, and the search feature CTRL – F.

Good search words inside the PDF might include:

emergency, prior authorization, out-of-network, travel, durable medical equipment, mental health, prescription drugs, skilled nursing, or rehabilitation.

In many cases, when someone emails me a coverage question, the fastest answer is for me to find the right page in the EOC and send that page back to them.

Start With the Contract Before You Start Arguing About the Law

Sure, there are laws, regulations, bulletins, and court cases that can matter. But in everyday life, the first practical step is usually to check the language in the actual policy.

If the Evidence of Coverage clearly explains the benefit, limitation, exclusion, or process, that will often answer the question much faster than trying to piece it together from multiple outside sources.

That is why so many of the pages on this website ultimately come back to the same point: read your Evidence of Coverage.

Where to Look for Your Evidence of Coverage

Depending on your coverage, your EOC may be found in your member portal, your employer’s benefits materials, your insurance company’s document library, or through member services.

If it’s one of the companies we represent, we can help you. Email us, [email protected].

If you cannot find it, ask for the full Evidence of Coverage, Certificate of Insurance, or plan booklet for your exact plan and year.

It is important to use your own EOC, not just a sample or a general explanation, because benefits and rules can differ from one plan to another.

Related Pages

You may also want to review these related topics:

- Appeals and Grievances

- Independent Medical Review (IMR)

- Medical Necessity

- Prior Approval / Prior Authorization

Need Help Finding or Understanding Your EOC?

If you are in California and cannot find your Evidence of Coverage, or you found it but want help understanding a specific section, email us.

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

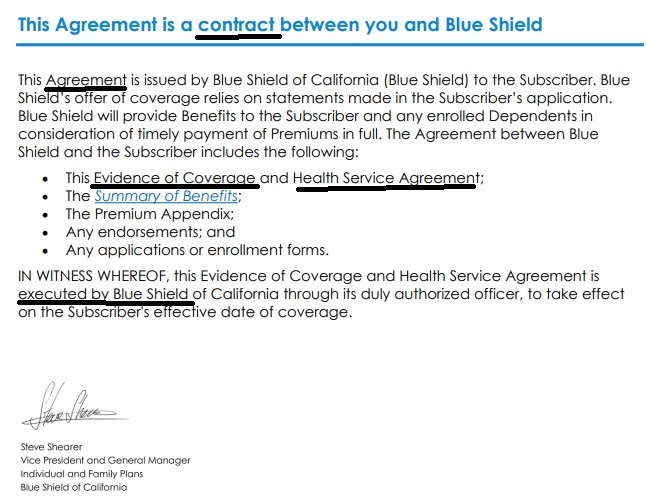

The EOC Evidence of Coverage is the CONTRACT #between you and the Insurance Company

Every policy has a written Evidence of Coverage (EOC). The EOC is your guide to what is covered and what is excluded, how much you will pay depending on the circumstances, what your cost sharing will be, and other information about using your coverage. Keep this document handy for when you have questions about your policy. Insurance.CA.Gov *

Plain English Mandate

AI Summary

- California law requires insurance policies to be written in "plain English" or clear, understandable language, meaning exclusions and conditions must be conspicuous, clear, and understandable to the average person, not hidden in jargon; if ambiguous, they're interpreted for coverage, favoring the insured's reasonable expectations.

- Our webpage on how to read an EOC Evidence of Coverage - Actual Policy

- While laws mandate clarity, courts often find actual policies difficult to read, applying strict rules to insurers who must make terms obvious, or else they're interpreted in favor of coverage. [1, 2, 3, 4, 5, 6]

- Conspicuous, Plain, & Clear: Insurers have the duty to make policy limitations, exclusions, and conditions conspicuous, plain, and clear to the ordinary person.

- Contra Proferentem Rule: If ambiguity remains after applying other rules, ambiguous terms are interpreted strictly against the insurer (the drafter).

- Reasonable Expectations: Courts consider the policyholder's objectively reasonable expectations when interpreting ambiguous terms, often leading to coverage.

- Statutory Mandates: California statutes require clarity, and the California Department of Insurance won't approve policies with unintelligible or misleading language. [1, 2, 3, 5, 6, 7, 8, 9]

- Difficulty in Practice: Despite laws, many policies are still complex, leading to disputes.

- Insurer's Burden: The burden is on the insurer to ensure clarity, especially for exclusions, rather than on the insured to decipher dense text, notes this article on insurance law.

- Judicial Interpretation: Courts actively enforce these principles, protecting policyholders from being misled by hidden or confusing contract language. [1, 2, 3, 4, 5, 6]

Introduction to EOC Evidence of Coverage

So many questions are answered right in the Full Policy the evidence of coverage – EOC, in

- PLAIN English, as mandated by law.

- Along with your duty to read the policy!

Sure beats reading the law and then trying to see for sure if the law applies to you. When you have your actual EOC, a couple of easy ways to find stuff in the policy is the bookmarks, table of contents and the search feature.

The Evidence of Coverage (EOC) is a document that describes in detail the health care benefits covered by the health plan. It provides documentation of what that plan covers and how it works, including how much you pay. The EOC can also refer to a certificate or contract provided to a health plan member that contains information about coverage and other rights. National Disability Rights *

Here’s where to find your EOC Evidence of Coverage for:

- Individual & Family Plans

- Employer Group Plans

- Medi-Cal

- Medicare Advantage Co Ordination Plan –

- Email us if you are in CA and have any questions.

Must #read your policy

A court “must hold the insured bound by clear and conspicuous provisions in the policy even if evidence suggests that the insured did not read or understand them.”

- property casualty 360.com/is-there-a-duty-to-read-insurance-contracts

- IRMI duty to read

- Is there a duty to read? Hastings College of Law

- Fordham Law Review Duty to read a changing concept 1974

- Kenny & Sams Law Firm

(NASE’s prior Carrier, as pointed out by UICI’s to Steve Shorr personally 4/6/2006 letter) This case shows that one must read the ACTUAL policy and can’t rely on Agent’s statements or brochures. There are some exceptions… This doesn’t just apply to NASE, but to ANY Insurance Contract. See attorney Keler.com for more explanation.

Plain Language – Read Policy THREE times

Guide to #Contract Interpretation

#Plain Meaning Rule

How to read a policy

How to read and figure out the law or Insurance Policy Provisions - Evidence of Coverage

- Read the Statute – Policy

- Read the Statute – Policy

- Read the Statute – Policy

- Then when you think you understand it, read it again

-

-

- Then as my cousin reminded me - one needs to check Westlaw, Google or the Talmud to see how the courts have interpreted the law, their might be some jiggery pokery - malarky going on.

- Check your Insurance Company Evidence of Coverage EOC one big advantage of the EOC is that it's in Plain English.

- Scroll down for more...

- Felix Frankfurther – Wikipedia

-

-

- Then when you think you understand it, read it again

- Tools to Read a Statute VIDEO

- Contract Interpretation in California: Plain Meaning, Parol Evidence and Use of the Just Result Principle

- How Will Making English the Official Language of the U.S. Affect Patients with Limited English Proficiency? Commonwealth Fund 12/4/2025

-

More on How to read a contract - Insurance Policy

-

The language of the text of the statute or Evidence of Coverage EOC should serve as the starting point for any inquiry into its meaning. To properly understand and interpret a statute, [first] you must read the text closely, keeping in mind that your initial understanding of the text may not be the only plausible interpretation of the statute or even the correct one, per Justice Felix Frankfurter . Guide to Reading & Interpreting * American Society of Healthcare Risk Management and * Wikipedia.

-

The starting point in statutory construction is the language of the statute - Evidence of Coverage itself. The Supreme Court often recites the “plain meaning rule,” as in, King vs Burwell Subsidies in Health Care.Gov upheld, that, if the language of the statute is clear, there is no need to look outside the statute to its legislative history in order to ascertain the statute’s meaning.

-

Parol Evidence Rule Wikipedia - Contract stands by itself - can't bring up discussions or agreements that were prior to actually signing the written Contract

-

The plain meaning of the contract will be followed where the words used—whether written or oral—have a clear and unambiguous meaning. Words are given their ordinary meaning; technical terms are given their technical meaning; and local, cultural, or Trade Usage of terms are recognized as applicable. The circumstances surrounding the formation of the contract are also admissible to aid in the interpretation. West’s Encyclopedia of American Law,

-

A cardinal rule of construction is that a statute should be read as a

Harmonious Whole,

with its various parts being interpreted within their broader statutory context in a manner that furthers statutory purposes. A provision that may seem ambiguous in isolation is often clarified by the remainder of the statutory scheme — because the same terminology is used elsewhere in a context that makes its meaning clear, or because only one of the permissible meanings produces a substantive effect that is compatible with the rest of the law.”

-

In Edgar v. MITE Corp., 457 U.S. 624 (1982), the Supreme Court ruled: “A state statute is void to the extent that it actually conflicts with a valid Federal statute.” In effect, this means that a State law will be found to violate the supremacy clause when either of the following two conditions (or both) exist:[3]

- Compliance with both the Federal and State laws is impossible, or

- “…state law stands as an obstacle to the accomplishment and execution of the full purposes and objectives of Congress…”

Supreme Court - FINAL Ruling - Plain Meaning - No Jiggery Pokery 47 Pages, view our highlights, annotations & bookmarks

Our webpage on

- jiggery pokery and contract interpretation

- Evidence of Coverage EOC

- Plain Meaning Rule - How to read Policy - Contract

Specimen Individual Policy #EOC with Definitions

Employer Group Sample Policy

It's often so much easier and simpler to just read your Evidence of Coverage EOC-policy, then look all over for the codes, laws, regulations etc! Plus, EOC's are mandated to be written in PLAIN ENGLISH!

- Find your own Individual EOC Evidence of Coverage

- It' important to use YOUR EOC not just stuff in general!

- Obligation to READ your EOC

- Plain Meaning Rule - Plain Writing Act

- Our Webpage on Evidence of Coverage

- OOP Out of Pocket Maximum - Many definitions are explained there.

VIDEO Steve Explains how to read EOC

Jump to section on:

|

Fool & their Folly

|

Plain language makes it easier for the public to read, understand, and use government communications.

- Modern insurance policies, as a result of state statutes, are required to be written in plain language or easy to read language sufficient for anyone with a fourth-grade education can understand. “Sesame Street English.” Merlin Law Group

- The Plain Writing Act of 2010 was signed on October 13, 2010. The law requires that federal agencies use clear government communication that the public can understand and use.

- While the Act does not cover regulations, three separate Executive Orders emphasize the need for plain language: E.O. 12866, E.O. 12988, and E.O. 13563.

- plain language.gov/law/

- Training Videos

- plain language.gov/guidelines/

- California Globe – Plain English

- CA Government Code 11340 – 11342.4

- Contra proferentem is a rule of contract interpretation that states an ambiguous contract term should be construed against the drafter of the contract. The term contra proferentem is derived from a Latin phrase meaning “against the offeror.”Contra proferentem has become increasingly important with the rise of contracts of adhesion. Contracts of adhesion involve pre-written contracts which are offered on a strict take-it or leave-it basis, leaving no opportunity for a party to bargain over specific contractual terms. Because the party does not have an opportunity to negotiate, they may reasonably interpret a term in a different manner than the contract offeror intended. Contra proferentem exists to place the burden of ambiguity on the party most capable of mitigating that ambiguity – the person who wrote it.

-

The doctrine of contra proferentem is also especially important in the field of insurance law due to the generalized nature of many of its terms. For example, it may be unclear if a policy that covers “water damage” will cover damage caused by a rainstorm induced mudslide. The doctrine of contra proferentem encouraged insurance providers to create enumerated lists of events that are excluded under a given policy, ultimately increasing clarity for insurance purchasers. Source Cornell Law *

- Health insurance illiteracy costs employees, study finds Despite spending more than $1 trillion on health insurance each year, many U.S. consumers are making poorly informed decisions – and paying for their lack of understanding.

Steve Shorr

Website Video #Introduction

Jiggery Pokery

King v Burwell – Subsidies Upheld – ScotusCare –

Plain Meaning Rule – Interpretive Jiggery Pokery

Slip Opinion

The

doctrine of privity in contract law

provides that a contract cannot confer rights or impose obligations arising under it on any person or agent except the parties to it.

The premise is that only parties to contracts should be able to sue to enforce their rights or claim damages as such. However, the doctrine has proven problematic due to its implications upon contracts made for the benefit of third parties who are unable to enforce the obligations of the contracting parties. en.wikipedia.org

In tort law, a duty of care is a legal obligation imposed on an individual requiring that they adhere to a standard of reasonable care while performing any acts that could foreseeably harm others. It is the first element that must be established to proceed with an action in negligence. The plaintiff must be able to show a duty of care imposed by law which the defendant has breached. In turn, breaching a duty may subject an individual to liability in tort. The duty of care may be imposed by operation of law between individuals with no current direct relationship (familial or contractual or otherwise), but eventually become related in some manner, as defined by common law (meaning case law). wikipedia.org/

Elements

| the foreseeability of harm to the injured party; |

| the degree of certainty he or she suffered injury; |

| the closeness of the connection between the defendant’s conduct and the injury suffered; |

| the moral blame attached to the defendant’s conduct; |

| the policy of preventing future harm; |

| the extent of the burden to the defendant and the consequences to the community of imposing a duty of care with resulting liability for breach; |

| and the availability, cost, and prevalence of insurance for the risk involved.[6] |

| the social utility of the defendant’s conduct from which the injury arose.[7]wikipedia.org/ |

Health Insurance unfortunately is very complicated

President Trump February 27, 2017

- Thus, if we haven't simplified and explained in PLAIN ENGLISH what you are looking for:

#Insubuy Travel Health Insurance

Instant Quotes, Details and ONLINE Enrollment

Steve talks about International Travel Insurance VIDEO

US State Department - Travel - Insurance

Our webpage on Travel Insurance

Wed, 24 Dec 2008

Steve,

I was looking for some specific Medicare information and found your site on Google.

You have a great site. It is very informative without a lot of meaningless information.

I thought I’d tell you that. I think I am glad you are not in my area. I’d hate to have you as a competitor.

Best regards,

Mark A. Squires.

Principal

Squires. and Associates

Independence MO

Resources & Links

- Wikipedia

- Our webpage on mandated privacy notices – scroll down to section on writing in plain English.

- California Civil Code 1635 et seq – Interpretation of Contracts

- Caminetti_v._United_States

- Thomas v Quintero CASP.net

- Must read policy or you can’t complain it wasn’t what you expected.