“How Much Will You Actually Pay with Health Insurance?”

“Deductibles, coinsurance, and out-of-pocket costs explained simply”

“Most people misunderstand this — See below for a plain English explanation with charts and video’s

#OOPChart

- Graph Source Health Net Glossary Page 6

-

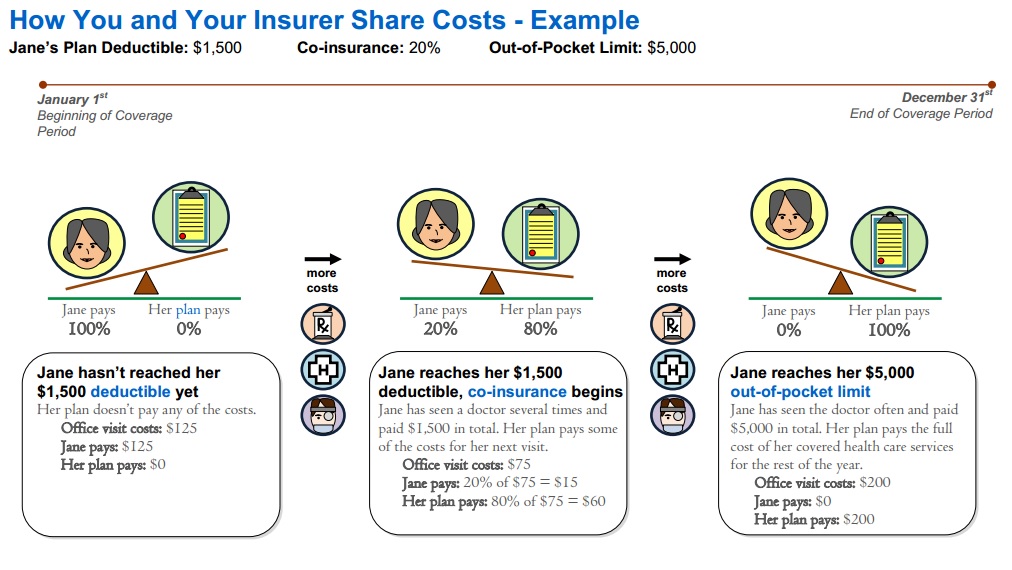

- Let’s say you have a $5,000 out-of-pocket max.If you have a major surgery costing $100,000:

👉 You only pay $5,000 not $20,000

👉 Insurance pays the rest That’s the purpose of the out-of-pocket maximum. - 1. You pay 100% until you hit your deductible

2. Then you share costs (coinsurance)

3. When you hit your out-of-pocket max → insurance pays 100% -

#Calendar Year Deductible

- amount you must pay for specific Covered Services before the plan pays for Covered Services pursuant to this [policy] Agreement. Learn more Deductible & Co Pay

- Copayment The specific dollar amount that a Member is required to pay for Covered Services after meeting any applicable Deductible.

- Learn more Co Pays

- Coinsurance The percentage amount that a Member is required to pay for Covered Services after meeting any applicable Deductible.

- Out-of-Pocket Maximum OOP The highest Deductible, Copayment, and Coinsurance amount an individual or Family is required to pay for designated Covered Services each year as indicated in the Summary of Benefits section.

- Charges for services that are not covered, charges in excess of the Allowable Amount or contracted rate do not accrue to the Calendar Year Out-of-Pocket Maximum. Sample EOC Page 107

- See video’s below for more explanation

-

“Why this matters when choosing a plan”

- Lower premium plans = higher risk if you get sick

- Higher premium plans = more predictable costs

- Out-of-pocket max = your financial safety net

- “If this still feels confusing, I help people walk through this every day — no cost to you.” Email us [email protected]

Our quote engines allows you to compare Bronze, Silver, Platinum and Gold Plans Side by side!

- Let’s say you have a $5,000 out-of-pocket max.If you have a major surgery costing $100,000:

-

How Premiums and Deductibles Work

VIDEO

Deductible & Co Pays

#Deductible s Calendar Year & Co Pays

Deductible – The Calendar Year amount you must pay for specific Covered Services before the plan pays for Covered Services pursuant to this [policy] Agreement. Sample EOC Page 107

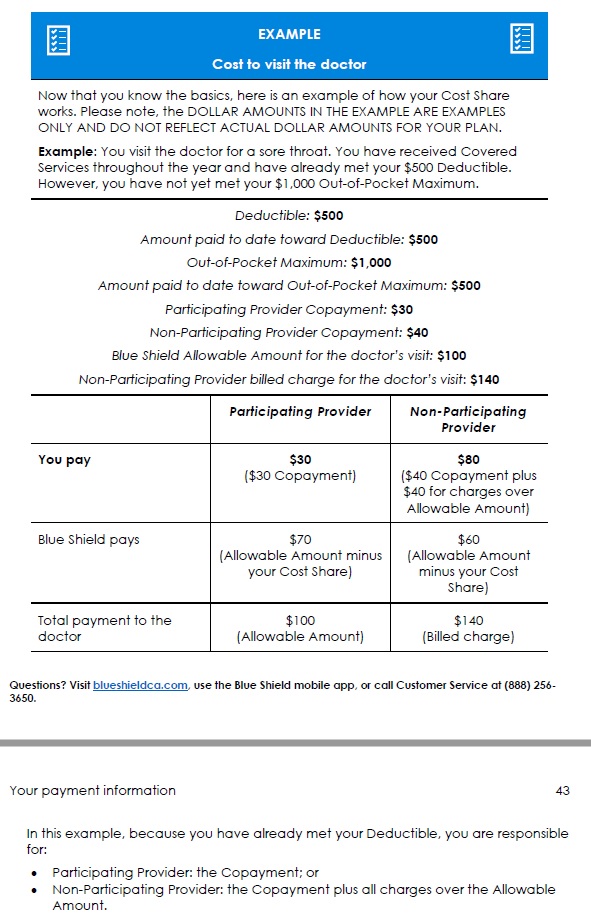

Example from 2022 Silver 70 PPO

See evidence of coverage – Cost concepts in action 2024 Page 42

- Deductibles in ACA Marketplace Plans, 2014-2024

- Metal Level Chart – Scroll to the bottom

- FAQs / Ask Us a Question

- Get Instant Quotes

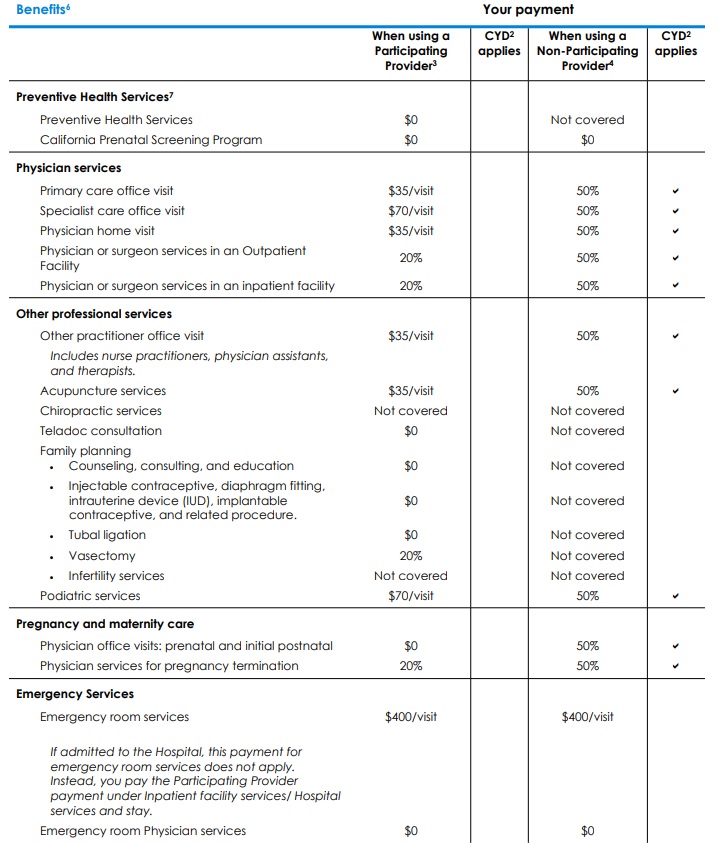

#Co-Payments – Specific Covered Services

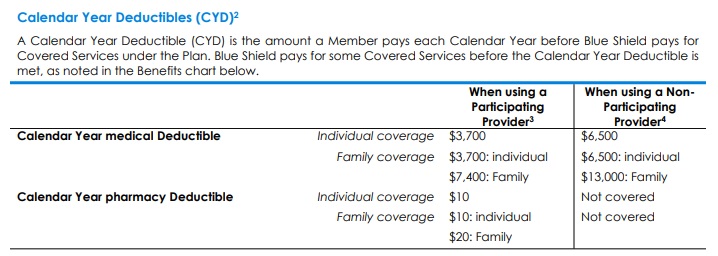

Footnote #2 Calendar Year Deductible (CYD):

- Calendar Year Deductible explained. A Calendar Year Deductible is the amount you pay each Calendar Year before Blue Shield pays for Covered Services under the Plan.

- If this Plan has any Calendar Year Deductible(s), Covered Services subject to that Deductible are identified with a check mark () in the Benefits chart above.

- Covered Services not subject to the Calendar Year medical Deductible. Some Covered Services received from Participating Providers are paid by Blue Shield before you meet any Calendar Year medical Deductible. These Covered Services do not have a check mark () next to them in the “CYD applies” column in the Benefits chart above.

- This Plan has a separate medical Deductible and pharmacy Deductible.

- This Plan has a separate Participating Provider Deductible and Non-Participating Provider Deductible.

- Family coverage has an individual Deductible within the Family Deductible. This means that the Deductible will be met for an individual with Family coverage who meets the individual Deductible prior to the Family meeting the Family Deductible within a Calendar Year. Any amount you have paid toward the individual Deductible will be applied to both the individual Deductible and the Family Deductible. Once the individual Deductible or Family Deductible is reached, cost sharing applies until the Out-of-Pocket Maximum is reached.

- The PAF Co-Pay Relief Program, one of the self-contained divisions of PAF, provides direct financial assistance to insured patients who meet certain qualifications to help them pay for the prescriptions and/or treatments they need. This assistance helps patients afford the out-of-pocket costs for these items that their insurance companies require. Patient Advocate Foundation *

Notification of OOP Out of Pocket Maximum

Explanation of Benefits

- SB 368, requires most state-regulated private-sector health plans to send enrollees updates, an EOB Explanation of Benefits for every month in which they received care, showing how much they have paid toward their annual deductible — the amount a person must shell out before insurance begins to cover most of their care — and how close they are to reaching out-of-pocket limits, the amount after which the insurer pays for 100% of care. CA Health Line.org *

Our Webpage on

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

Comments FAQ’s

Ask Us a Question

News reports about how high deductibles leave people effectively without medical care as people are living on the edge – paycheck to paycheck.

- Los Angeles Times May 2, 2019 * May 2 3 Kids $15k Medical Debt *

- NPR May 3, 2019

- New York Magazine.com 5.3.2019

- North County Public Radio 5.3.2019

- How to figure out the Family Deductible & OOP? Insure Me Kevin.com

- Soaring insurance deductibles and high drug prices hit sick Americans with a ‘double whammy’ LA Times

- Learn about Embedded vs aggregate deductible

- How might an HSA Health Savings Account help you save up to pay the deductible?

- FAQs / Ask Us a Question

- Get quotes, subsidies, net premium, deductibles, co-pays, OOP Out of Pocket maximum from all Individual companies * Employer Group

- Provider Finder See also our Site Map for instructions & details on each companies provider finder

- Glossaries – Dictionaries

- ACA’s Maximum Out-of-Pocket Limit Is Growing Faster Than Wages KFf

- Video On Maximum Out of Pocket

- Patients often can’t afford to pay off what their insurance leaves behind

- Breaking Down Covered California Health Plans By Coverage Sections Insure Me Kevin . com

- Oscar’s Explanation of OOP

Steve Shorr

Website Video #Introduction

-

Brother – Sister – Sibling Side Pages Subpages

- Enhanced Silver 94, 87, 73 Cost-sharing reductions House v Price

- Grand Fathered Plans What does that mean?

- HSA Health Savings Accounts

- OOP -Out of Pocket Maximum – Participating or Not? Deductibles & Co- Pays

- Provider Finder Quotit

- Email us [email protected]

https://www.torrancememorial.org/healthy-living/blog/urgent-care-vs-emergency-department/

https://insuremekevin.com/california-deductibles-and-coinsurance-explained/#gsc.tab=0