California PPO Plans, Out-of-State Coverage &

International (Blue Card) Provider Access

Many people shopping for California health insurance want to know whether a California provider network will work outside California, while traveling internationally, during temporary travel, while attending college in another state, or after moving permanently. The answer depends on the type of health plan, the insurance company, whether the care is emergency or routine, and the exact wording in the Evidence of Coverage (EOC).

A PPO generally gives more provider flexibility than an HMO or EPO, but that does not automatically mean all routine care outside California will be covered in-network. Many plans provide broader emergency and urgent care protection than they do for scheduled routine non-emergency treatment outside the service area.

Covered California explains the basic differences between HMO, PPO and EPO plan types.

Quick Summary

- Emergency and urgent care are often treated differently from routine non-emergency care.

- Many California individual PPO plans do not work like older broad nationwide PPO plans.

- Employer group PPO plans may have broader national access than individual/family plans.

- International coverage is often limited to emergency or urgent situations.

- Always verify the doctor, hospital, facility, network and benefit level before treatment.

- Always review the Evidence of Coverage.

PPO, HMO and EPO Plan Types

A PPO may allow more provider choice than an HMO or EPO, but the real question is whether the provider is in-network for your exact plan. A doctor may accept one carrier product but not another. Start with the plan’s provider finder, then confirm directly with the carrier and provider.

Blue Shield PPO and BlueCard

BlueCard may help some Blue Shield members access participating providers outside California, but the actual coverage depends on the plan’s benefits, network rules and Evidence of Coverage.

Blue Shield also has information on access to coverage. Before relying on BlueCard, ask whether the service is emergency, urgent, routine, in-network, out-of-network, authorized, or excluded.

Individual PPO vs. Employer Group PPO

A major source of confusion is that employer group health insurance may have different network access than an individual or family PPO plan. Some group PPO plans may offer broader national access, while individual California plans may be more limited for routine out-of-state care.

Do not assume that a PPO through Covered California, a private individual PPO, and a group PPO all work the same way. Check the EOC, provider directory, BlueCard rules and prior authorization requirements.

Traveling, Snowbirds, Students and Moving Out of California

Out-of-state questions often come up for college students, snowbirds, remote workers, temporary travelers, people helping family members in another state, and people who are moving permanently. A temporary trip is different from a permanent move.

If you permanently move out of California, you may need to report a change and review whether you qualify for a Special Enrollment Period.

Emergency, Urgent and Routine Care

Emergency care is not the same as routine care. Emergency services may have special legal protections, including federal surprise billing protections. For more detail, see my page on Emergency Room Coverage.

Routine non-emergency care outside the service area may be more limited. Before scheduling care, confirm whether the provider is in-network, whether prior authorization is required, and whether the plan will apply in-network or out-of-network benefits.

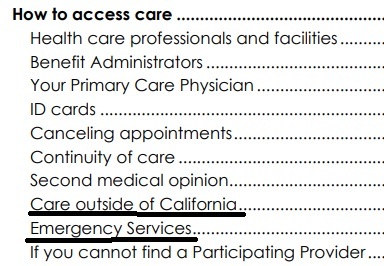

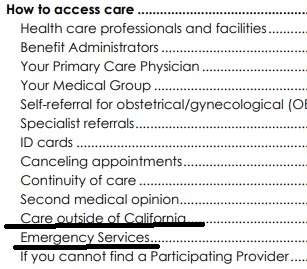

International Coverage

International health coverage is often more limited than people expect. Some plans may cover emergency or urgent care outside the United States, but routine care, claim procedures and reimbursement rules vary by plan. Always check the Evidence of Coverage before international travel.

Before traveling internationally, verify emergency coverage, claim filing rules, reimbursement procedures, travel assistance programs, and whether separate travel medical insurance may be appropriate.

Before You Schedule Treatment Outside California

- Use the plan’s provider finder.

- Confirm directly with the insurance company.

- Confirm directly with the doctor, hospital or facility.

- Ask whether the provider is in-network for your exact plan.

- Ask whether prior authorization is required.

- Write down names, dates, times and reference numbers.

- Review the Evidence of Coverage.

- Ask how negotiated rates and itemized bills may apply.

Related Pages

- Provider Finder Resources

- Evidence of Coverage (EOC)

- Report a Change to Covered California

- Special Enrollment Periods

- Employer Group Health Insurance

- Prior Authorization

- Emergency Room Coverage

- Negotiated Rates & Itemized Bills

- ACA Metal Levels

Need help checking PPO provider access, BlueCard rules, out-of-state coverage or plan documents?

CA Insurance Company Travel Guides

- Kaiser – KP.org Travel Care away from home * 951-268-3900 *

- Provider Finder for all our companies

- Sharp

- sutter health plus.org/care-while-traveling

- Free Quotes, Brochures and complete information on travel coverage and International Medical Plans

- Medicare.Gov/Travel

- $50k Emergency Coverage in Medi Gap aka Supplemental & Medicare Advantage Plans - Check your EOC! See our section on Medicare Below

- California Medi Cal rules on out of area coverage

- Constitutional right to travel from one state to another 14th Amendment

#Insubuy Travel Health Insurance

Instant Quotes, Details and ONLINE Enrollment

Steve talks about International Travel Insurance VIDEO

US State Department - Travel - Insurance

Our webpage on Travel Insurance

Introduction

How does my California Coverage work out of Area?

- What coverage is there under a California issued Health Policy, when you need:

-

- Emergency or Urgent Care

- Out of CA – Not an Emergency or Urgent? Like if you want to seek out specialists at prestigious world famous clinics and hospitals

-

- Find the EOC Evidence of Coverage for YOUR Insurance Company

- Blue Shield PPO Table of Contents

-

- Out of your HMO Service Area?

- Outside of USA?

- Learn more and enroll in International Travel Insurance.

- Medicare outside of USA

- Note – Employer Group Plans appear MUCH more liberal!

-

Definition Urgent Care and #Emergency Services

Emergency Medical Condition

An illness, injury, symptom (including severe pain), or condition severe enough to risk serious danger to your health if you didn’t get medical attention right away. If you didn’t get immediate medical attention you could reasonably expect one of the following:

1) Your health would be put in serious danger; or

2) You would have serious problems with your bodily functions; or

3) You would have serious damage to any part or organ of your body. Health Net Glossary *

Urgent Care

Care for an illness, injury, or condition serious enough that a reasonable person would seek care right away, but not so severe as to require emergency room care.

Prior Authorization – Preauthorization

- A decision by your health insurer or plan that a health care service, treatment plan, prescription drug or durable medical equipment (DME) is medically necessary. EOC * Our Webpage * Sometimes called prior authorization, prior approval or precertification. Your health insurance or plan may require preauthorization for certain services before you receive them, except in an emergency. Preauthorization isn’t a promise your health insurance or plan will cover the cost. Health Net Glossary * Our webpage on Prior Authorization *

Be sure to check the definition in YOUR EOC

Links related to Urgent & Emergency Care Definition

- Urgent Care vs ER

- Emergency Room – Obligation to treat uninsured patients

- Emergency Room – Balance Billing

- Health Net Provider Networks & Search

- Definitions – Glossary

- Providence Health – Difference between ER and Urgent Care

- Viewpoints: Insurance Companies Can Drop Patients Whenever; Choosing Between Doctor Vs. Urgent Care KFF

Specimen Individual Policy #EOC with Definitions

Employer Group Sample Policy

It's often so much easier and simpler to just read your Evidence of Coverage EOC-policy, then look all over for the codes, laws, regulations etc! Plus, EOC's are mandated to be written in PLAIN ENGLISH!

- Find your own Individual EOC Evidence of Coverage

- It' important to use YOUR EOC not just stuff in general!

- Obligation to READ your EOC

- Plain Meaning Rule - Plain Writing Act

- Our Webpage on Evidence of Coverage

- OOP Out of Pocket Maximum - Many definitions are explained there.

VIDEO Steve Explains how to read EOC

Blue Shield INDIVIDUAL Plans

Unauthorized Excerpt of Confidential Agent Guide

Blue Shield BlueCard Program frequently asked questions

Going to Urgent Care vs ER Emergency Room

What if you’re out of the area, out of state?

Visiting an urgent care center can cost up to five times less than a visit to the ER and significantly reduce your wait time. While the average wait at a California ER is 4 hours and 34 minutes, urgent care center wait times are usually under an hour*. That means you can bypass the crowds and take your first step on the road to recovery.

- 49 Ways to stay out of the ER – Emergency Room Kevin MD.com

-

Why CA Insurance Companies limited out of area – CA to urgent and emergency only

Too Many Claims

BlueCard Program for Doctors & Hospitals

& Inter plan Arrangements -

for members traveling out of state & outside of the united states

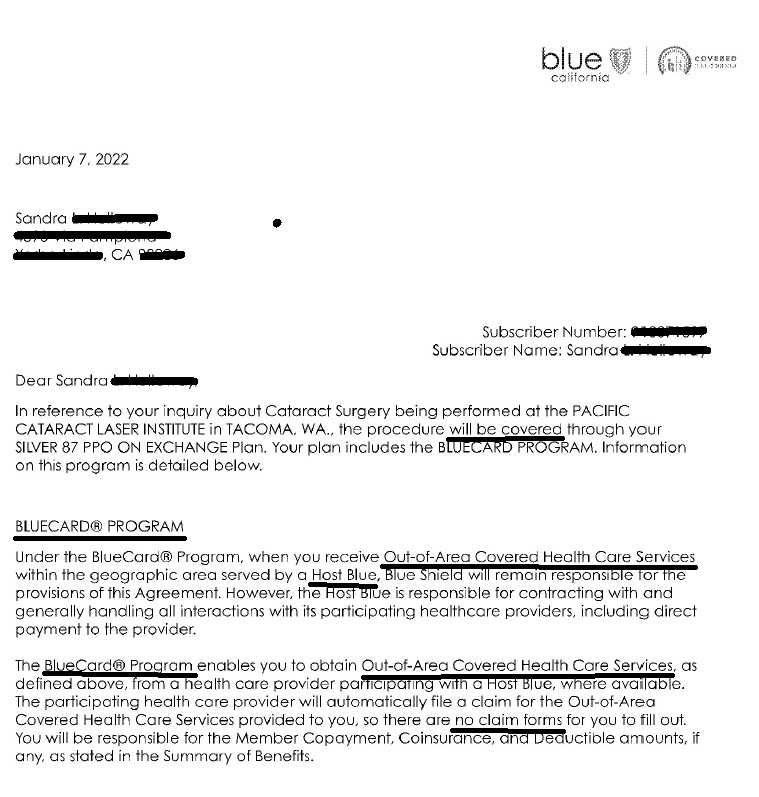

Excerpt from Typical EOC Evidence of Coverage

Out-of-area services

- Blue Shield has a variety of relationships with other Blue Cross and/or Blue Shield licensees. Generally, these relationships are called Inter-Plan Arrangements and they work based on rules and procedures issued by the Blue Cross Blue Shield Association. Whenever you receive health care services outside of California, the claims for those services may be processed through one of these Inter-Plan Arrangements described below.

- When you access health care services outside of the Plan Service Area, you will receive the care from one of two kinds of providers.

- Most providers are participating providers and contract with the local Blue Cross and/or Blue Shield licensee in that other geographic area (Host Blue). S

- home providers are non-participating providers because they do not contract with the Host Blue. Blue Shield’s payment practices in both instances are described below and in the Introduction section of this Agreement.

- This Blue Shield plan provides limited coverage for health care services received outside of the Plan Service Area. Out-of-Area Covered Health Care Services are restricted to

-

- Emergency Services,

- Urgent Services, and

- Out-of-Area Follow-up Care.

- Any other services will not be covered when processed through an Inter-Plan Arrangement unless prior authorized by Blue Shield. Please see the Medical Management Programs section for additional information on prior authorization and the Emergency Benefits section for information on emergency admission notification.

- View YOUR actual EOC - It's YOUR EOC Policy that rules, not what you read on the Internet

-

- Here's the Individual Blue Shield Silver PPO It's a lot of material, so we won't just copy and paste, nor summarize it. It's mandated to be in plain English.

- Please note that Employer Group Plans may have MUCH better coverage than Individual, namely they may cover out of state Non Emergency, Non Urgent. Here's a Blue Cross Group EOC.

-

- Co Pays, Deductibles, OOP In vs Out of Network

- Appoint us as your Covered CA broker, no extra charge

- Get Instant California Health Quotes

- Get a Blue Shield Member Portal

Steve Shorr

Website Video #Introduction

Contact us – Get Quotes

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

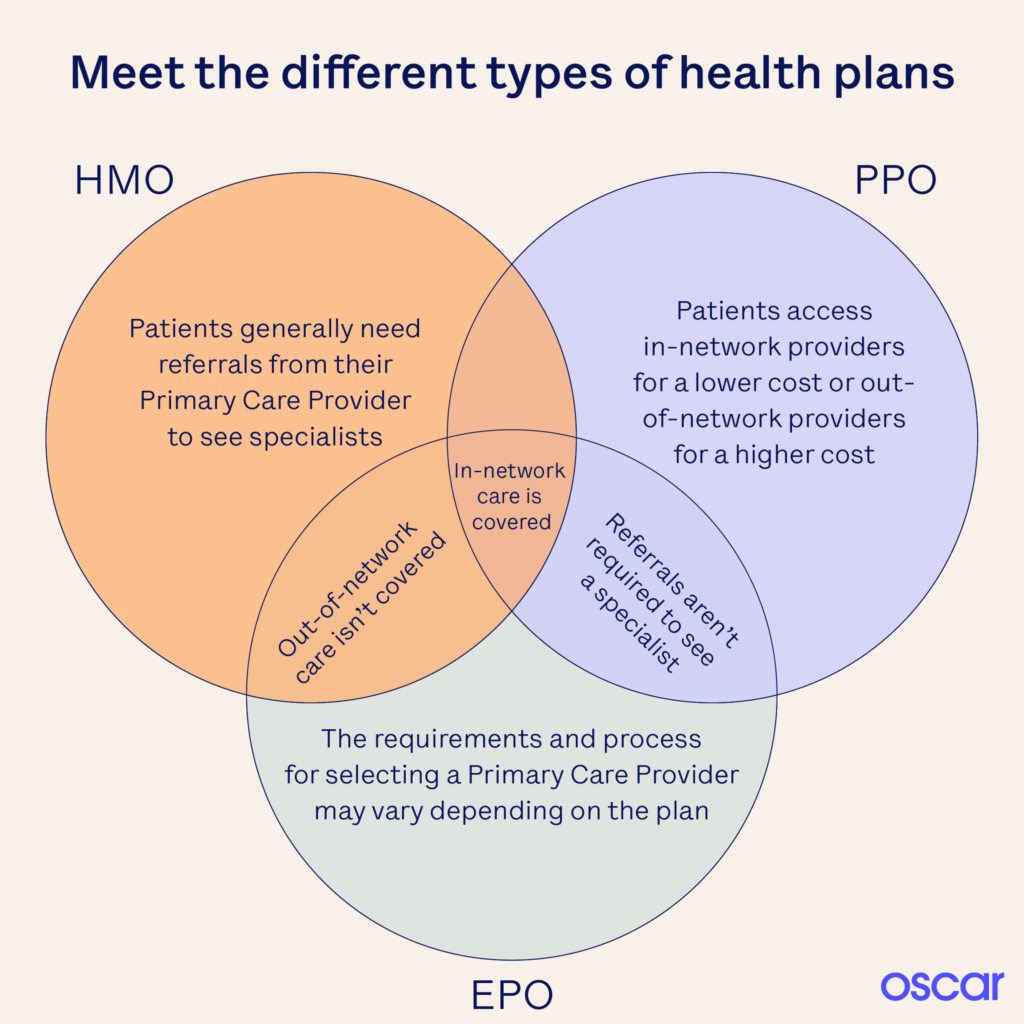

HMO - PPO - EPO

- Learn More - Oscar Explanation

- Provider Finder See also our Site Map for instructions & details on each companies provider finder

- ‘Father Of The HMO’ Dies At 95; Idea Didn’t Turn Out Like He Envisioned KFF

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

#Covered CA Certified Agent

No extra charge for complementary assistance

Related Pages - Travel Insurance

https://www.torrancememorial.org/healthy-living/blog/urgent-care-vs-emergency-department/

https://www.caloes.ca.gov/

https://www.fire.ca.gov/