Advance Payments of the Premium Tax Credit APTC

ARPA American Rescue Plan Act

How to get & qualify for Subsidies

Covered California Subsidies, MAGI Income & Tax Credits — Start Here

Covered California subsidies are based on your estimated annual Modified Adjusted Gross Income (MAGI), household size, tax filing status, access to employer coverage, and other eligibility rules. The hard part is that income, Medicare, Medi-Cal, employer coverage, and IRS tax reconciliation can all overlap. This page is designed to help you find the right topic quickly.

Not sure where to start? Pick the situation that sounds most like you:

- I need to know what income counts for Covered California MAGI

- My income, address, household, or coverage situation changed

- I received Form 1095-A or need help with IRS Form 8962

- I am over age 65 and want to know if I can still get tax credits

- My employer or spouse’s employer offers coverage

- I sold a house, stocks, crypto, or had capital gains

- I have rental income or Schedule E income

- I have gambling winnings or losses

- Covered California is asking me for proof of income

- Why is Covered California so confusing?

Most Common Covered California Subsidy Mistakes

Many subsidy problems happen because people estimate income incorrectly, forget to report changes, or do not realize that tax credits are reconciled later on their federal tax return.

- Using take-home pay instead of MAGI. Covered California generally looks at projected annual MAGI, not just what is deposited into your checking account. Read more about MAGI income.

- Forgetting capital gains. A home sale, stock sale, crypto gain, or other taxable gain may affect subsidies. See capital gains and Covered California income.

- Not reporting mid-year changes. Income, household size, address, employer coverage, Medi-Cal eligibility, or Medicare eligibility changes can affect your subsidy. Learn when and how to report a change.

- Ignoring Form 8962. Advance Premium Tax Credits are reconciled when you file your tax return. Learn about IRS Form 8962 and subsidy reconciliation.

- Assuming age 65 automatically ends all subsidies. Medicare eligibility can affect Covered California, but the rules are more complicated if you are not eligible for premium-free Medicare Part A. Read about Covered California tax credits after age 65.

- Misunderstanding employer coverage. Employer coverage, affordability, spouse coverage, and family coverage can affect subsidy eligibility. Review the employer coverage and family glitch rules.

- Forgetting California’s penalty rules. If you go without qualifying coverage, California may impose a state individual mandate penalty. Read about California’s health insurance mandate penalty.

Important: If your income or coverage situation changes, do not wait until tax time to fix it. A subsidy that looks correct today can become a repayment problem later if Covered California has the wrong income or eligibility information.

Report a change |

Form 8962 tax reconciliation |

Proof of income documents

Quick Covered California Subsidy Questions

What determines my subsidy?

Your subsidy is generally based on household size, projected annual MAGI income, age, ZIP code, and the benchmark plan available in your area. Start with the MAGI income page.

What if my income changes during the year?

Report the change as soon as possible so your subsidy can be adjusted. See how to report a change to Covered California.

What if I am self-employed or have business income?

Self-employment income can be more complicated because deductions, Schedule C income, and estimated annual income all matter. Start with the MAGI income page.

What if I sold property or investments?

Capital gains may increase MAGI and affect your subsidy. See capital gains and Covered California income.

What if I got a 1095-A?

You may need IRS Form 8962 to reconcile the tax credits you received. See Covered California, Form 1095-A, and IRS Form 8962.

Why is this so confusing?

Because Covered California connects insurance eligibility, tax law, income estimates, Medi-Cal rules, employer coverage rules, and Medicare rules. For a plain-English explanation, see Why Is Covered California So Confusing?

You do not have to figure this out alone.

Steve Shorr Insurance can help you review your Covered California options, estimate subsidy eligibility, compare plans, and understand how income changes may affect your coverage. There is generally no additional cost to have Steve Shorr Insurance help as your Covered California agent.

Thanks! Just saw your video [above] and your explanation was spot on.

Have a good evening,

J H

Sat 1/3/2026 5:47 PM

See more unsolicited testimonials our webpage

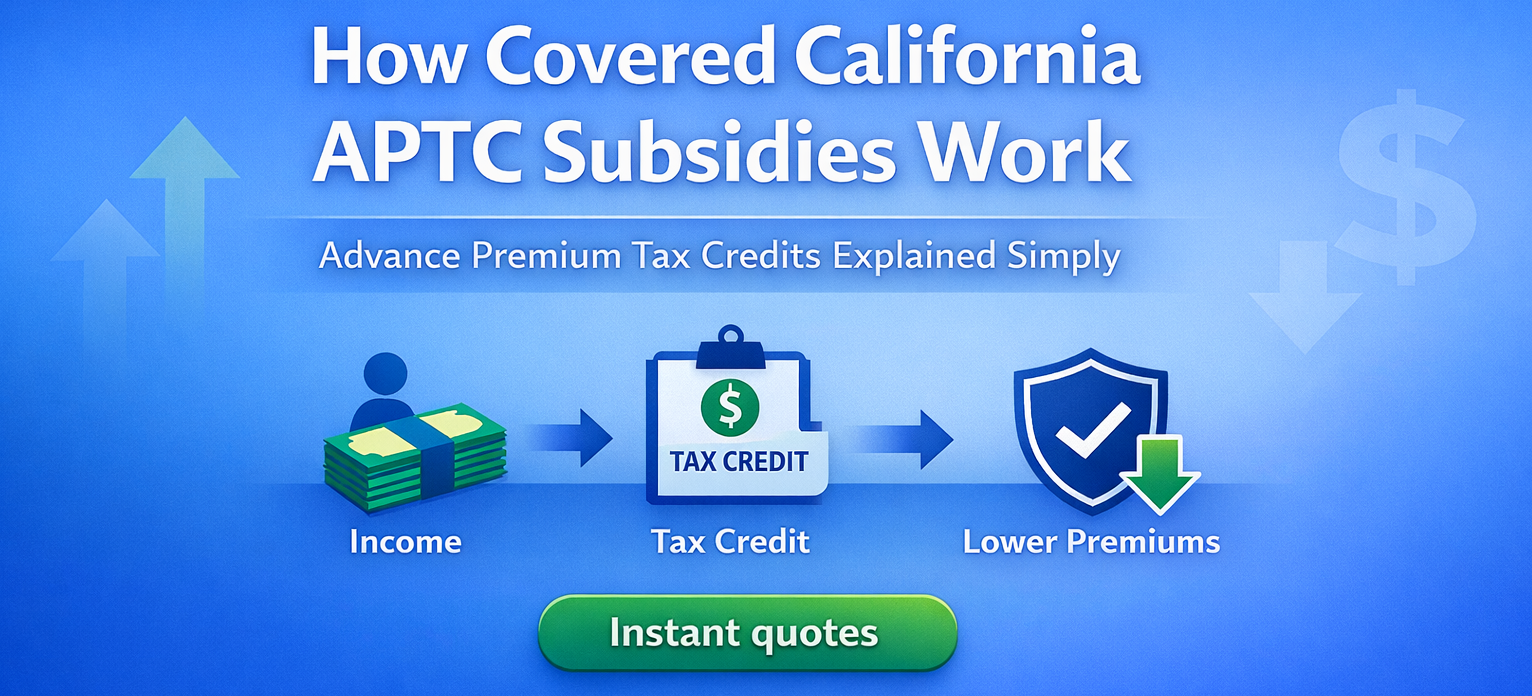

Introduction to Subsidies – Premium Tax Credit

- ACA/Obamacare and tax subsidies APTC are one of the most confusing things you’ll ever come across. The simplest thing to do is just get an Instant quote.

- Enter your projected AGI Adjusted Gross Income, line 11 of your tax return, note that MAGI Modified Adjusted Gross Income has a few other things,

- your date of birth, zip code and

- then we can set a Zoom Meeting to go over all of it.

- 2026 loss of ARPA subsidies???

- Latest Status as of 12/21/2025

- Congress Is Ending the Year Without a Health Care Deal. What Comes Next? Time 12/21/2025

- Basically Time says it won’t pass. Don’t for get though that the original subsidies for those between 138% and 400% of FPL are still there.

- California will continue the enhanced subsidies for those earning up to 150% of FPL… Hey, it’s confusing… see links to get an instant quote. Covered CA.com 10/25/2025

- Agent Briefing * Covered California Rates and Plans for 2026: Consumer Affordability on the Line with Uncertainty Surrounding Federal Premium Tax Credit Extension * coveredca.com/important-changes

- White House circulates a plan to extend Obamacare subsidies as Trump pledges health care fix Pbs.org *

- Anthem Explanation

- How the Change in Enhanced ACA Tax Credits Could Impact You

- Your ACA health insurance premiums for the remainder of 2025 will stay the same.

- Since 2021, enhanced premium tax credits have increased the financial help available to individuals to pay their Affordable Care Act (ACA) health insurance premiums.

- If enhanced premium tax credits are not extended, they will expire on December 31, 2025.

Premium tax credits, also known as subsidies, will still be available in 2026, but the amounts may be lower. This means you could pay more out of pocket for Covered CA coverage - These changes impact those enrolling in or renewing a Covered CA health insurance plan for 2026 coverage.

- Kaiser Foundation calculator till Quotit gets updated

- kff.org/payments–double if-enhanced-premium-tax-credits-expire

- How do you get the premium tax credit?

- Check out our quote engine, to get a preliminary indication of the amount of subsidies you’ll qualify for. There is no extra charge for our services, just appoint us as your broker.

- In a lot of ways subsidies are hocus pocus smoke & mirrors as you have to file Form 8962, Premium Tax Credit, with your tax return at the end of the year. You are also mandated to report changes within 30 days. So, at the end of the year if you make too much $$$ you might have to give it back. If you make less, you get money back on your taxes.

- Failing to file your tax return will prevent you from receiving advance credit payments in future years and can cause MAJOR PROBLEMS and coverage CANCELLATION!

- The premium tax credit is refundable so even if you hardly pay any taxes, you still benefit. The credit is generally paid in advance to a taxpayer’s insurance company to help cover the cost of premiums. IRS Website on “The Basics“

- Covered CA step by step guide to Health Insurance

FAQ’s, Links & Resources

- What can agents or brokers do to help prepare their clients who may be newly eligible for savings (Offers of Employer Coverage) on Covered CA plans?

- FAQ’s on IRS website

- Covered CA Brochure

- Tax Subsidy vs $1 Premium Credit

- What is Covered CA? Insure Me Kevin.com

- Covered CA Technical Broker Bulletins…

- If you qualify for Medicare… no subsidies

- Understanding Reasonable Opportunity Period (ROP) & Auto Discontinuance

- Portal Alert Notices Guide for Certified Enrollers

- Online Application Task Guide

- covered ca.com/documents-to-confirm-eligibility

- Tool Kits

- KFF Foundation FAQ’s

- irs.gov/affordable-care-act-tax-provisions

- VIDEO Introduction to Individual Plans for those coming from Employer Group Plans

- Pros – Cons – Complicated FAQ’s Research on staying with under 65 plan? Covered CA? vs Medicare

- Simple calculator to figure out your subsidy and enroll Online

- insure me kevin.com/did-your-covered-california-subsidy-suddenly-vanish

- insure me kevin.com/your-tax-return-is-not-linked-to-your-covered-california-account

- The Untold Story of the Workers Who Make the Affordable Care Act Work | Opinion

- Renewal Toolkit

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

Subsidy Calculation Rules §1.36 B

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

Health Insurance unfortunately is very complicated

President Trump February 27, 2017

- Thus, if we haven't simplified and explained in PLAIN ENGLISH what you are looking for:

Technical Links for

Premium Tax #Credits §136 B

CFR 136 B 3 – How is Tax Credit #Calculated

- § 1.36B-1 Premium tax credit definitions.

§ 1.36B-2 Eligibility for premium tax credit.

§ 1.36B-3 Computing the premium assistance credit amount.

§ 1.36B-4 Reconciling the premium tax credit with advance credit payments.

§ 1.36B-5 Information reporting by Exchanges.

§ 1.36B-6 Minimum value. - CFR 155.305 HTML Eligibility Standards

- §1.36b-1 Premium tax credit definitions

- law.cornell.edu/uscode 1396a

- Notice 2013-41, whether or when individuals are considered eligible for coverage under certain Medicaid, Medicare, CHIP, TRICARE, student health or

- HR 3590 Section 1001 HR 4872

- Code of Federal Regulations §1.36b-2Eligibility for premium tax credit.

- VIDEO What is APTC Advance Premium Tax Credit

- Interactive Tax Assistant (ITA)

- Am I eligible to claim the Premium Tax Credit?

Tax #Estimators

- turbo tax.com - FREE for simple returns

- H & R Block

- E file.com

- Estimate the Subsidy for Health Insurance, benefits, premiums, etc.

- 8962 ONLINE Calculator

- Our webpage on 8962 Premium Tax Credit Reconciliation

- Tax Form Calculator.com

- e tax.com

- Marriage Higher or Lower Taxes?

ACA What You Need To Know #5187 (2020) is the most recent

- VITA - Volunteers to help you

- Publication 17 - Your Federal Income tax

- Health Savings Accounts HSA our webpage

Sorry, this webpage is just getting too big.

For information on ARPA, Inflation Reduction Act, etc. that lapsed 12/31/2025 and Native Americans visit this page on ARCHIVE.org

Trump Make America Healthy Again

- RFK Jr.’s MAHA Movement Has Picked Up Steam in Statehouses. Here’s What To Expect in 2026 Kff.org January 2026

- The Supreme Court has determined that health insurance plans under the Affordable Care Act (ACA), also known as Obamacare, must continue to fully cover preventative services, including cancer screenings, HIV prevention medication, and mental health counseling, without co-pays or deductibles. Forbes *

- Nearly half of the U.S. population is pre-diabetic or has type-2 diabetes. Every month, diabetes causes 13,000 new amputations, 5,000 new cases of kidney failure and up to 2,000 new cases of blindness in our country. In 1960, approximately 13 percent of American adults were obese. Now, more than 40 percent of Americans are obese, and more than 70 percent are either obese or overweight.

- Even more shockingly, one-quarter of our teenagers today are pre-diabetic or have type-2 diabetes, and obesity is the leading medical reason that 71 percent of young Americans are disqualified from military service. Learn More >>> The Hill 11/2024 * Listing of the 6 Points Beckers Hospital Review 12/2024 *

- Federal Changes Toolkits pdf

- Covered CA Toolkits

- Open Enrollment Tool Kit

- Enrollment Dashboard Guide for Certified Enrollers

- FPL Income Chart

- Strike & Lockout

- QLE Major Life Changes

- SEP FAQ's for brokers Covered CA.com

- Documents to Confirm Eligibility

- Income Section

- social press kit.com/lets-talk-health

- Daily Summary Notices Broker Portal

- Medi Cal to Covered CA

- Forms - Including Paper Application

- 1095 toolkit

- how to generate and print plan summaries

- Service & Operating Hours Covered CA.com

- Social Media Toolkit Covered CA.com

- Daily Summary Emails– Notices

- Information Needed

- Understanding Reasonable Opportunity Period (ROP) & Auto Discontinuance Guide

https://www.npr.org/2026/06/26/nx-s1-5860746/aca-health-insurance-subsidies-rates-premiums

https://hub.quotit.com/blog/aca-client-retention-2026-a-playbook-to-keep-your-book-from-dropping-off