Full details and definition of MAGI Income for Covered CA Subsidies

#What Is MAGI for Covered California?

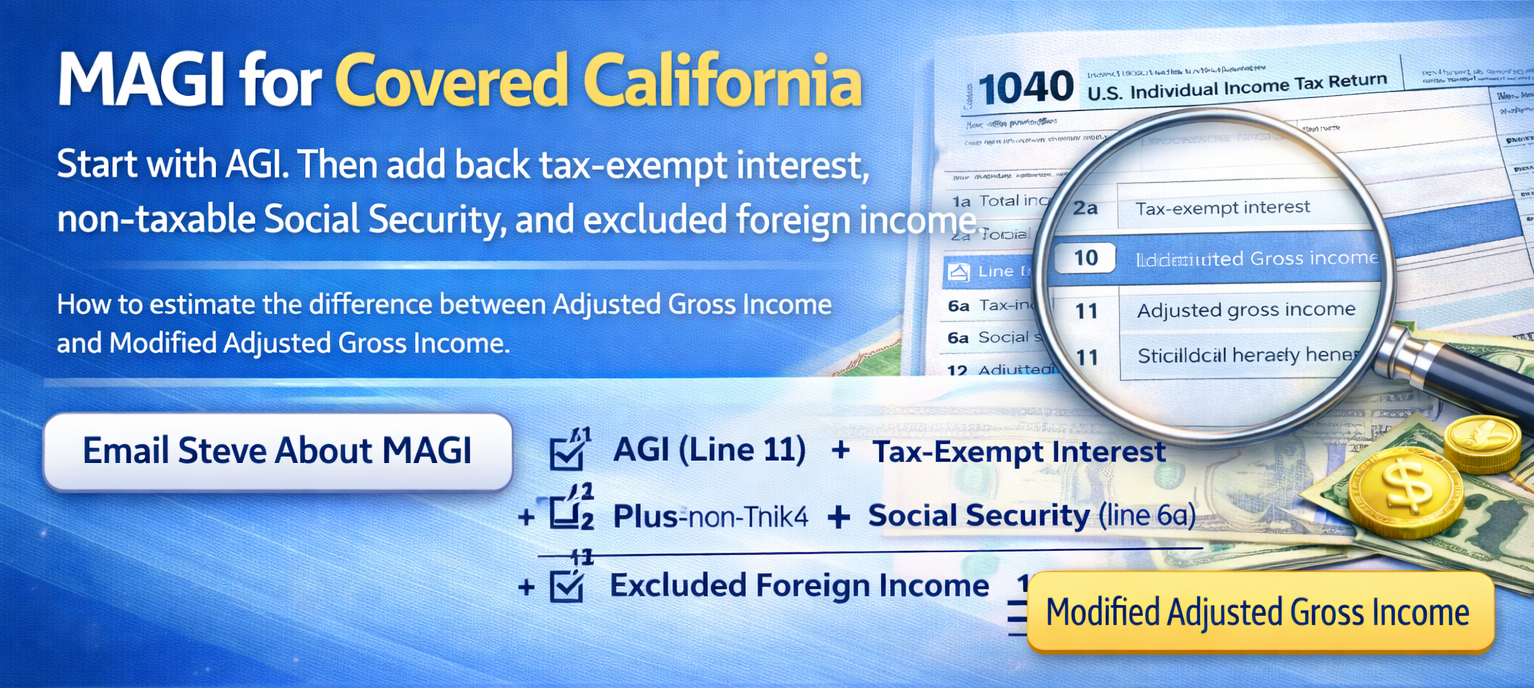

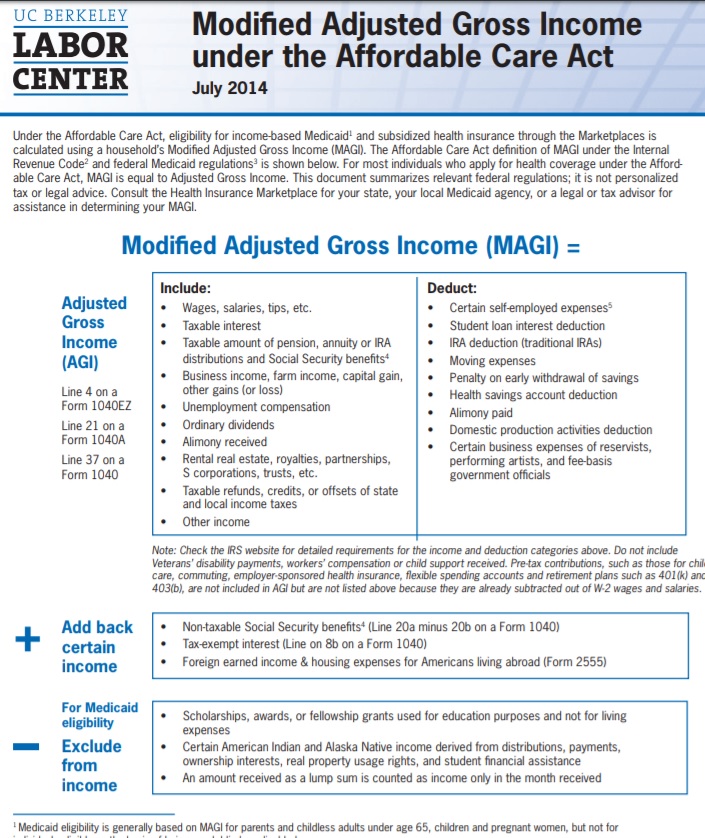

MAGI is usually a little different from Adjusted Gross Income.

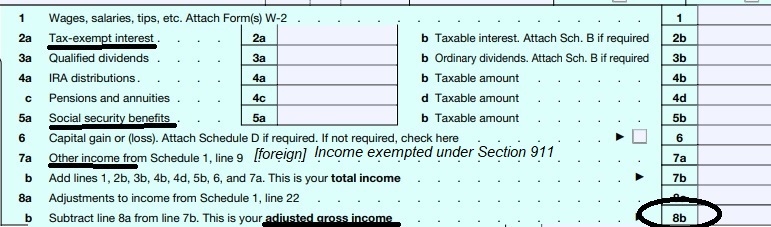

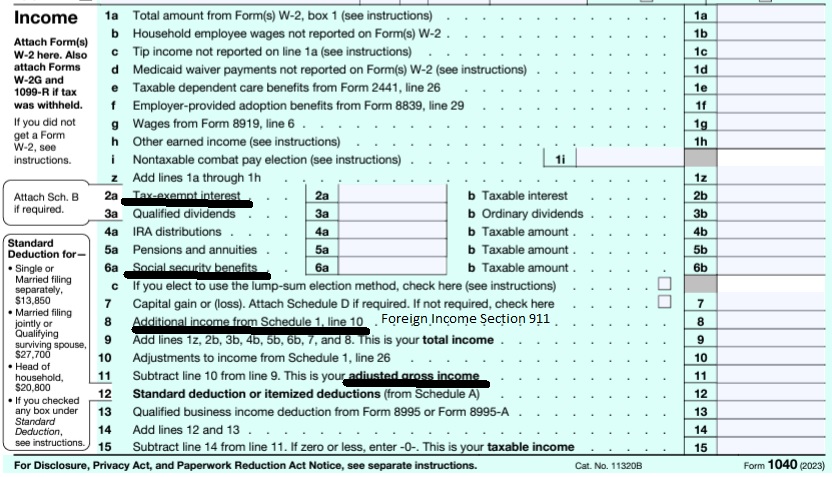

If you are trying to figure out your Covered California income, the place to start is usually your Adjusted Gross Income (AGI) on Form 1040, Line 11.

Then add back, if applicable:

Tax-exempt interest

Non-taxable Social Security benefits

Excluded foreign income

That is generally how you get from AGI to MAGI for Covered California.

For many people, MAGI is the same as AGI or very close to it. But if you have tax-exempt interest, non-taxable Social Security, or excluded foreign income, your MAGI may be higher than your AGI.

Important: Covered California is usually looking at your estimated income for the upcoming coverage year, not just what appears on last year’s tax return.

AGI Income Calculator from Tax Act.com

How Do You Calculate MAGI?

Step 1: Start with Form 1040, Line 11 — your Adjusted Gross Income.

Step 2: Add any tax-exempt interest.

Step 3: Add any non-taxable Social Security benefits.

Step 4: Add any excluded foreign income.

That total is generally your MAGI for Covered California.

Quick MAGI Worksheet

AGI (Form 1040, Line 11) __________

Plus tax-exempt interest __________

Plus non-taxable Social Security __________

Plus excluded foreign income __________

= Estimated MAGI for Covered California __________

What Gets Added Back?

Tax-exempt interest

This is interest that may not be taxable for regular income tax purposes, but may still count for MAGI.

Non-taxable Social Security

If part of your Social Security is not taxable, that non-taxable portion may still get added back for MAGI.

Excluded foreign income

If you excluded foreign earned income from taxable income, it may still count for MAGI.

What Does Not Usually Change the Basic Formula?

Do not double count your wages, self-employment income, or taxable Social Security.

Those items are generally already reflected in your Adjusted Gross Income.

Why Last Year’s Tax Return Is Only a Starting Point

Covered California usually wants your best estimate for the upcoming year.

Last year’s tax return can be a helpful starting point, but if your income is changing, your estimate for the coverage year may be different.

If your income changes during the year, report the change promptly so your subsidy does not end up too high or too low.

[PASTE BUTTON HERE]

Frequently Asked Questions

Is MAGI always different from AGI?

No. For many people, MAGI is the same as AGI or only slightly different.

Where do I start on my tax return?

Start with Form 1040, Line 11, which is your Adjusted Gross Income.

What usually gets added back?

Usually tax-exempt interest, non-taxable Social Security, and excluded foreign income.

Should I use last year’s income or this year’s estimate?

Usually your best estimate for the upcoming coverage year.

What if I am not sure what to include?

That is where I may be able to help.

Need Help Estimating Your MAGI?

If you are not sure what counts and what does not, reach out.

You can email me your basic numbers, or your recent tax return information, and I can help you estimate your Covered California MAGI.

Steve Shorr

Covered California Certified Insurance Agent

Email: [email protected]

[PASTE BUTTON HERE]

This page is for general educational purposes only and is not tax or legal advice. Final eligibility is determined by official program rules and your application.

Scroll down for a comprehensive list and details of all the ins and outs of the definition of MAGI Income

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

More information on MAGI Definition

- 1040 IRS Annual Tax Form

- Schedule 1 Additional Income & Adjustments to Lower your MAGI Income

- IRA Retirement

- Health Savings Account

- Trumps Big Beautiful Bill – may lower line 6 A Social Security Income Learn More >>> Newsweek * PBS *

- Estimate next years MAGI Income?

- Get instant quotes, subsidy calculation and coverages

- NO ASSET TEST for MAGI based subsidies in Covered CA or MAGI Medi Cal Qualification. Steve’s VIDEO

- Nor is there a lien against your estate for Covered CA or MAGI Medi Cal

- Schedule 1 Additional Income & Adjustments to Lower your MAGI Income

-

Modified Adjusted Gross Income (MAGI) (2) … means

adjusted gross income – Line 11 of the 1040 Form * Health Care.Gov * 26 USC §62 *

*Plus +

(i) Amounts excluded from gross income under IRC §911 * Foreign Exempted * IRS Form 2555 * CFR 1.36 B – 1 *

(ii) Tax-exempt interest [IRS Coursework] [Form 8815 * Interest Income * Investing Answers.com] the taxpayer receives or accrues during the taxable year; and

(iii) some Social Security Benefits Western Poverty & Law Explanation of MAGI ♦ (UC Berkely One Page Summary) ♦ CFR 1.36 B 1 * IRS Publication 974 ♦ George Town.edu

Get even more details & definitions of MAGI Income

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

Jump to the section you want:

Try turning your phone sideways to see the graphs & pdf's?

Official Publications on MAGI

UC Berkeley explains MAGI Modified Adjusted Gross Income –

Click on image to enlarge and for a more clear picture

- Western Poverty & Law Explanation of MAGI – IMHO one of the most authoritative publications I’ve ever seen!

- It’s important to read the all material & links as one can’t rely on Covered CA to give you the correct answer.

- How to estimate your MAGI income?

- CHCF 2 page summary on what is MAGI

-

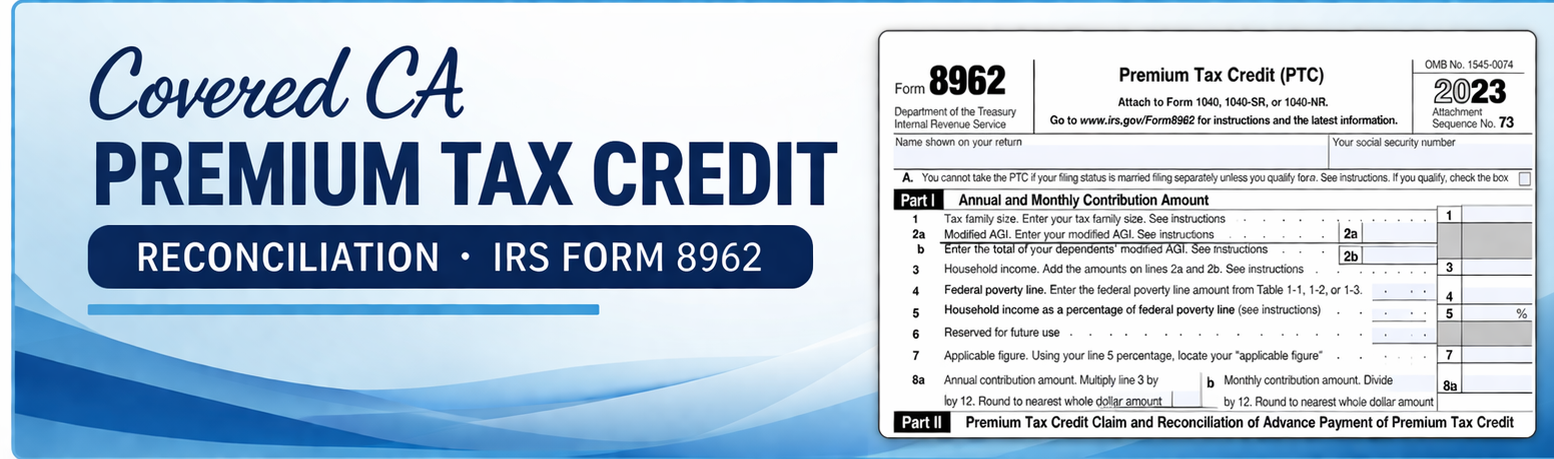

Covered CA Premium Tax Credit Reconciliation IRS Form 8962

|

#Adjustments to Income - Schedule 1

#Schedule1 1040

- Part I Additional Income

- 2a Alimony received

- 3 Business income or (loss). Attach Schedule C

- Get Health Quote for your business

- 5 Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E

- 7 Unemployment compensation

- 8 Other income:

- a Net operating loss

- b Gambling income

- c Cancellation of debt

- d Foreign earned income exclusion from Form 2555

- e Taxable Health Savings Account distribution

- Part II Adjustments to Income

- 11 Educator expenses

- 13 Health savings account deduction. Attach Form 8889

- 15 Deductible part of self-employment tax. Attach Schedule SE

- Learn more about your Social Security Benefits

- 16 Self-employed SEP, SIMPLE, and qualified plans -

- 17 Self-employed health insurance deduction

- 19a Alimony paid

- 20 IRA Individual Retirement Account deduction

- 21 Student loan interest deduction

- Instant Business Health Insurance Proposals

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

Covered CA (& Medi Cal) - Calculate - #Countable Sources of MAGI Income

Short Summary

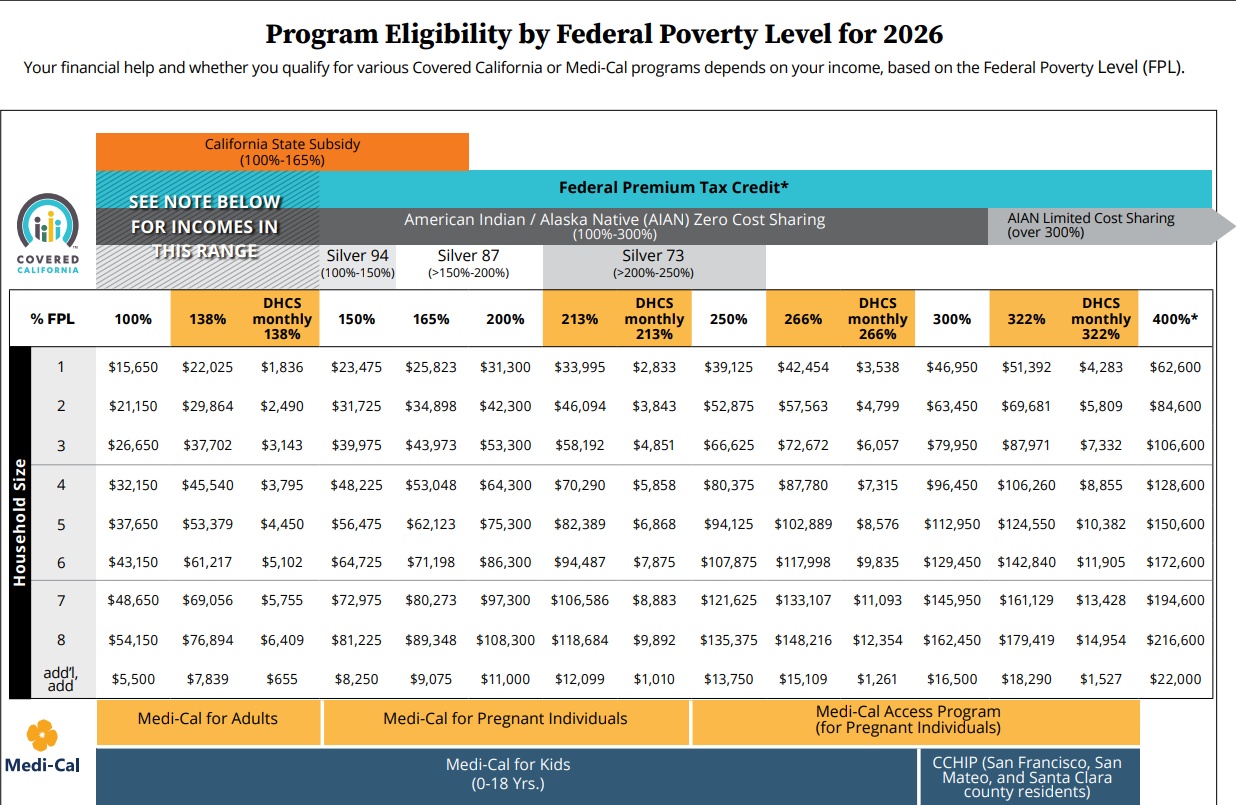

Know your estimated income? See your 2026 plans and subsidy.

Use the income chart as a starting point, then compare the 2026 health plans available in your ZIP code and see an estimate of your Covered California subsidy.

See My 2026 Plans & Estimated Subsidy

No obligation. There is no extra charge for my help when you use me as your Covered California Certified Insurance Agent.

- Source - Covered CA

- When Your Tax Return Income Makes You Medi-Cal Eligible Insure Me Kevin.com

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

Foreign Income

How does #Foreign Income get added back in, for Covered CA?

If you live and work abroad, you may be able to claim the foreign earned income exclusion. If you qualify, you won’t pay tax on up to $100,800 of your wages.

(i) IRC §911 [foreign income] Form 2555

***However, Foreign Income count’s towards Covered CA MAGI income, if you want subsidies! So you have to add back in Line 8 d of Schedule 1 to AGI Adjusted Gross Income to get Modified AGI

Foreign Earned Income IRS Form # 2555

Foreign Earned Income Instructions for # 2555 & Exclusion

- Do you need USA health coverage, as a resident? Get quotes

- Travel Insurance? Get Quotes

- Do you qualify for an exemption?

- For more information – See Tax Guides & Publications

#Insubuy Travel Health Insurance

Instant Quotes, Details and ONLINE Enrollment

Steve talks about International Travel Insurance VIDEO

US State Department - Travel - Insurance

Our webpage on Travel Insurance

Medicare A & B if you don't #live in USA

Publication 11871

Medicare just visiting Out of County Publication # 11037

- medicare.gov/travel-outside-the-u.s.

- Our webpage on Medicare Coverage outside of USA

- FAQ - Buying Medi Gap if you live outside USA

- Get International Travel Quotes & Information

- Medi Gap - Covers up to $50k

- Medicare Advantage may cover unlimited ER and Urgent care - check the details

*********Social Security*****

Payments if you are living outside of USA # 10137

- Learn More

Our Webpages on:

- Visit our webpage on how to report changes

- Estimate your MAGI Income

Schedule D - Capital #Gains

- Visit our main webpage on capital gains

-

IRS Publication 550 investment & interest income & expense

#Interest Income 550

HTML PDF

- You tube VIDEO on Schedule D

- Schedule 1040 D Capital Gains & Losses

- Net Operating Losses Investopedia

- Sales and Disposition of Assets 544

- HTML

- Learn More ⇒IRS Tax Topic 409

- Report most sales and other capital transactions and calculate gain or loss on Form 8949 (PDF), Sales and Other Dispositions of Capital Assets, then summarize capital gains and deductible capital losses on

- Form 1040, Schedule D (PDF), Capital Gains and Losses.

- Publication 505, Tax Withholding and Estimated Tax

- Publication 550, Investment Income and Expenses

- 551 - Basis of Assets

- Publication 544, Sales and Other Dispositions of Assets

- Topics 701 and 703, and Publication 523, Selling Your Home.

- How much does Term Life Insurance to cover any loans and protect your family run?

- A “paper loss” – a drop in an investment’s value below its purchase price – does not qualify for the deduction. The loss must be realized through the capital asset’s sale or exchange.

- Publication 544, Sales and Other Dispositions of Assets (PDF 321K)

- Form 1040, U.S. Individual Income Tax Return (PDF 136K)

- Publication 505, Tax Withholding and Estimated Tax (PDF 367K)

- Publication 550, Investment Income and Expenses (PDF 516K)

- Publication 17, Your Federal Income Tax (PDF 2075K)

- Publication 564, 551 - Mutual Fund Distributions (PDF 178K)

- Publication 547, Casualties, Disasters, and Thefts (PDF 133K)

- Publication 527, Residential Rental Property (Including Rental of Vacation Homes)

- Schedule B (Form 1040), Interest and Ordinary Dividends General Information

- Publication 537 (2024), Installment Sales Sale of a business

- Settlements—Taxability Publication 4345

- irs.gov/tax-implications-of-settlements-and-judgments

- Legal Settlement - Taxable vs. Nontaxable Tax Act.com

- A Primer on the Taxability of Legal Settlement Proceeds nstp.org

Details… of MAGI

#Household.income means Code of FEDERAL Regulations – IRS Income Taxes – 1.36B 1 – (e) …(1) … the sum of—

(i) A taxpayer’s modified adjusted gross income; (Line 37 Line 11 1040) plus

(ii) The aggregate modified adjusted gross income of all other individuals who—

(A) Are included in the taxpayer’s family under paragraph (d) [below] of this section; and

(B) Are required to file a return of tax imposed by section 1 for the taxable year (determined without regard to the exception under section (1)(g)(7) to the requirement to file a return). [26 USC §6012 ♦ IRS tool to see if you must file a return ♦ Medi-Cal Household Size Flow Chart ♦ Blog – Insure Me Kevin.com] DHCS *

(f) Dependent has the same meaning as in section §152. * IRS Interactive Assistant *

(d) … A taxpayer’s family means the individuals for whom a taxpayer properly claims a deduction for a personal exemption under section 151 for the taxable year.

Family size [Medi-Cal Household Size Flow Chart ♦ Blog – Insure Me Kevin.com] means the number of individuals in the family. Family and family size may include individuals who are not subject to or are exempt from the penalty [mandate] under §5000 A (f) (1) for failing to maintain minimum essential coverage. Health Care.gov explanation *

26 USC § 151 – Allowance of deductions for personal exemptions pdf

(a) Allowance of deductions

In the case of an individual, the exemptions provided by this section shall be allowed as deductions in computing taxable income.

To be more clear — (2) Married taxpayers must file joint return. A taxpayer who is married (within the meaning of section 7703) at the close of the taxable year is an applicable taxpayer only if the taxpayer and the taxpayer’s spouse file a joint return for the taxable year. GPO.Gov Final Regulations Page 11 * Turbo Tax Calculator * Tax Policy Center….. Joint or separate? * Estranged Spouse?

Premium Tax Credit Form 8962 & Instructions

Get a Free No Obligation Calculation of your Tax Credit, Premiums and see the benefit brochures.

View other pages & resources in this section…

- Getting MAGI Right – 23 page primer by George Town University on differences that apply to Medicaid (Medi-Cal) and CHIP Children’s Health Insurance Program Insure Kids now CA

- Power Point presentation CMS Income Counting MAGI

- InsureMeKevin.com analysis

- See also this article on Kevin’s site

- If you would like to talk to a professional tax adviser about this try Bruce Bialosky [email protected] 310.273.8250

- Agent Training – MAGI and APTC PowerPoint Presentation

View old HISTORICAL versions of this webpage at archive.org

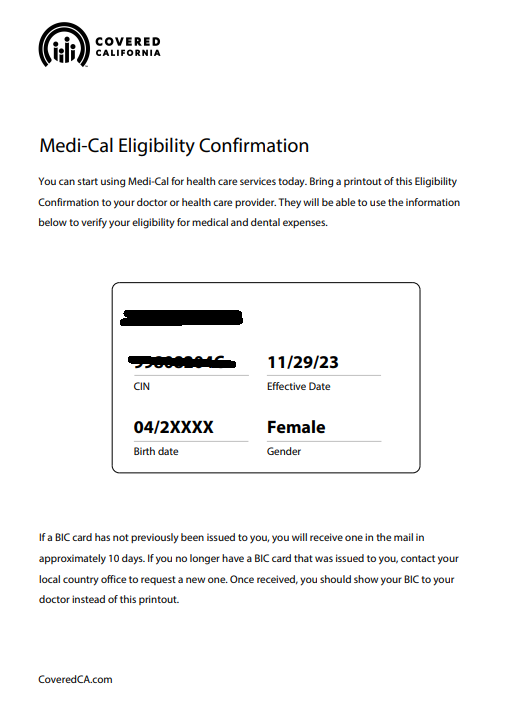

FAQ's #Negative MAGI Income – Qualification for Medi Cal? Subsidies?”

- Question If your MAGI Income is negative, can you still qualify for Covered CA subsidies APTC even if you have some income, before you get to line 11 of your 1040?

. - Answer - NO! See the income chart. Your MAGI Income - AGI needs to be over 138% of FPL Federal Poverty Level

- CFR 1.36 B C how APTC Premium Assistance is calculated

- We also have no idea how long a tax loss will show up on line 11 adjusted gross income line of your 1040? See our webpage on Long Term Capital gains.

- No problem getting health coverage, you just won’t get subsidies. Click here to get quotes and enroll online.

- Sources

- Western Poverty Law and go over them with appropriate counsel.

- How to calculate MAGI Income

- Q & A on Intuit Site

- See IRS publication 536 Net Operating Loss

- Form 8962 Reconcile Premium Tax Credit You must enter your Modified Adjusted Gross Income MAGI

- IRS FAQ - What are the Income Limits

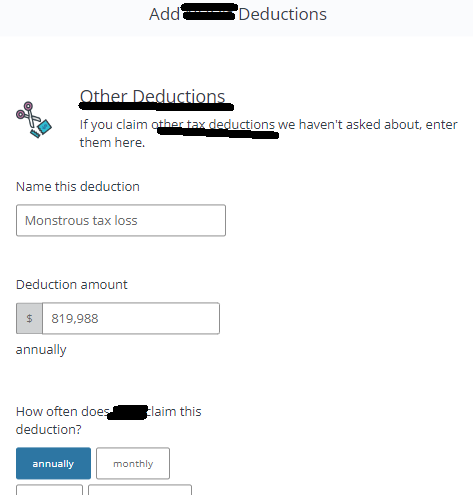

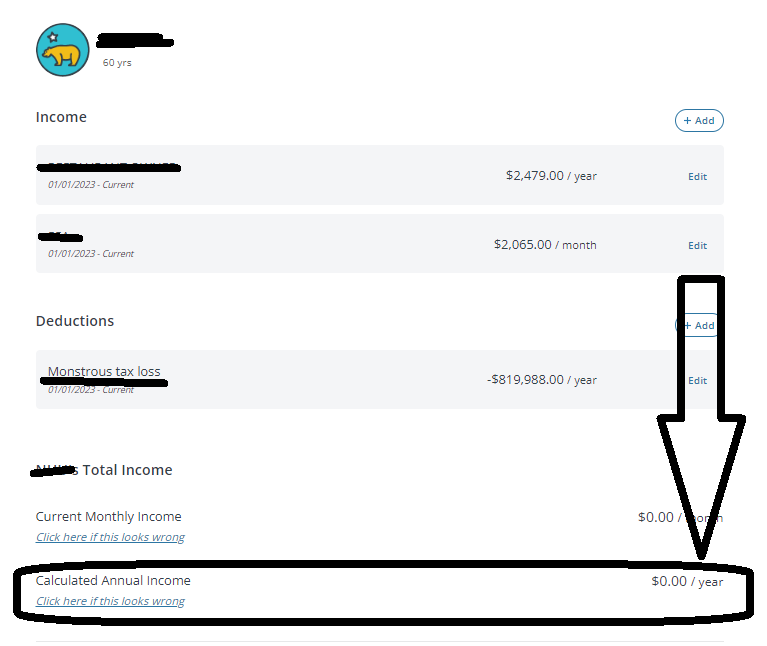

- Covered CA online application asks for Tax Deductions Email dated Wed 11/29/2023 8:54 AM Click on image to enlarge

-

- Question If your carry over net operating loss (from prior years) is allowed to be taken into account, is it part of the Federal Modified Adjusted Gross Income number ) or does California specifically require you to take it out of the equation?

- Answer Please see above on the definition of MAGI Income. I’m not aware of states having any authority over your Federal Tax return.

- Covered CA does not authorize agents to give tax advise. They suggest you get it from Volunteers at VITA.

- Note that the Income Chart says FEDERAL Poverty Level!

-

IRS Publication 536 Net Operating Loss

-

Do you really expect a clerk at Medi Cal to answer this kind of question?

-

We can help you with Covered CA when your income reaches 138% or more of FPL or if you go direct. Get quotes here.

- Answer Please see above on the definition of MAGI Income. I’m not aware of states having any authority over your Federal Tax return.

-

MAGI details from a Higher Up at Medi Cal

- Medi Cal agrees that MAGI can be negative and will educate the Counties...

-

Good morning,

For Modified Adjusted Gross Income (MAGI) Medi-Cal income and deductions policy, DHCS published All County Welfare Director’s Letter (ACWDL 21-04).

Page 2, Section 1 provides guidance on policy for countable income for MAGI program calculation, which is federal taxable income minus any allowable (post-tax) deductions under federal code. Page 3 links to an Income and Deductions chart tool to determine if a post-tax deduction can be used for MAGI-based Medi-Cal and for Covered California eligibility. Please note that the chart and the Covered California website deductions are post-tax deductions, and pre-tax deductions are already included when calculating AGI.

Tax loss is not considered an acceptable post-deduction for MAGI Medi-Cal or Covered California per federal code. The Centers for Medicare and Medicaid Services (CMS) has also published a document detailing MAGI rules with deduction information on page 7.

If the tax loss is considered as more of a capital gains/loss, or other loss such as real estate reported on Schedule E, then this amount should be entered into the system as an income with a negative (for example: -819,988). This will tell the system the income is actually at a loss and will reduce the income.

Thank you, and please let us know if you have any further questions.

Kathryn Floto, MPA | Health Program Specialist II

Medi-Cal Eligibility Division

California Department of Health Care Services

- VIDEO What is APTC Advance Premium Tax Credit

- Interactive Tax Assistant (ITA)

- Am I eligible to claim the Premium Tax Credit?

Tax #Estimators

- turbo tax.com - FREE for simple returns

- H & R Block

- E file.com

- Estimate the Subsidy for Health Insurance, benefits, premiums, etc.

- 8962 ONLINE Calculator

- Our webpage on 8962 Premium Tax Credit Reconciliation

- Tax Form Calculator.com

- e tax.com

- Marriage Higher or Lower Taxes?

ACA What You Need To Know #5187 (2020) is the most recent

- VITA - Volunteers to help you

- Publication 17 - Your Federal Income tax

- Health Savings Accounts HSA our webpage

Child & Sibling Pages

- APTC Advance Premium Tax Credit – Subsidies ARPA

- MAGI Income Chart – Line 11 1040 Covered CA

- Report a Change – How & When – Especially Income Create Account

- Table of Contents -Income, Deductions & Expenses for MAGI no index

- Alimony – From a Divorce Settlement taxable

- Capital Gains, Sale of Home & Dividends

- Clergy – Housing Allowance? Covered CA MAGI Income

- Covered CA MAGI Retirement Income

- Educational Credits – Student Loan Interest

- Gambling Income & Losses – Other Income Line 21

- Medical or any Debt Cancellation Covered CA MAGI Income?

- Social Security Benefits MAGI Covered CA Income Subsidies

- ACA Health Care Reform – Obamacare Introduction

- 10 Essential Mandatory Benefits + CA Benefits

- Metal Levels – Platinum, Gold, Bronze – Silver & Enhanced

- Enhanced Silver 94, 87, 73 Cost-sharing reductions House v Price

- Grand Fathered Plans What does that mean?

- HSA Health Savings Accounts

- OOP -Out of Pocket Maximum – Participating or Not? Deductibles & Co- Pays

- Provider Finder Quotit

- MLR 80% Medical Loss Ratio – Actuarial Value Minimum Payout

- Special & Open Enrollment Periods Covered CA & Direct with Broker

- Trump Great American Health Plan

- Covered California vs Direct Enrollment

- MAGI – Modified Adjusted Gross Income – Line 11

- APTC Advance Premium Tax Credit – Subsidies ARPA

- MAGI Income Chart – Line 11 1040 Covered CA

- Report a Change – How & When – Especially Income Create Account

- Table of Contents -Income, Deductions & Expenses for MAGI no index

- Alimony – From a Divorce Settlement taxable

- Capital Gains, Sale of Home & Dividends

- Clergy – Housing Allowance? Covered CA MAGI Income

- Covered CA MAGI Retirement Income

- Educational Credits – Student Loan Interest

- Gambling Income & Losses – Other Income Line 21

- Medical or any Debt Cancellation Covered CA MAGI Income?

- Social Security Benefits MAGI Covered CA Income Subsidies

- Why is Covered CA so confusing

ftb.ca.gov/net-operating-loss