Full details and definition of MAGI Income for Covered CA Subsidies

What Is MAGI Modified Adjusted Gross Income

for Covered California?

- MAGI is usually a little different from Adjusted Gross Income.

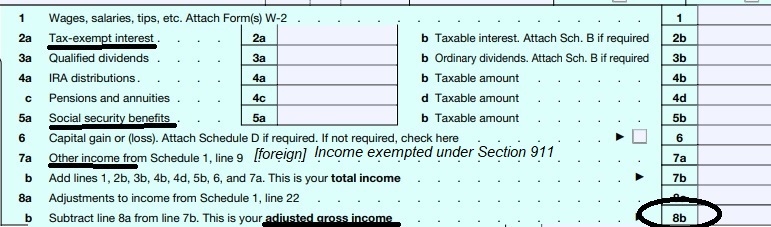

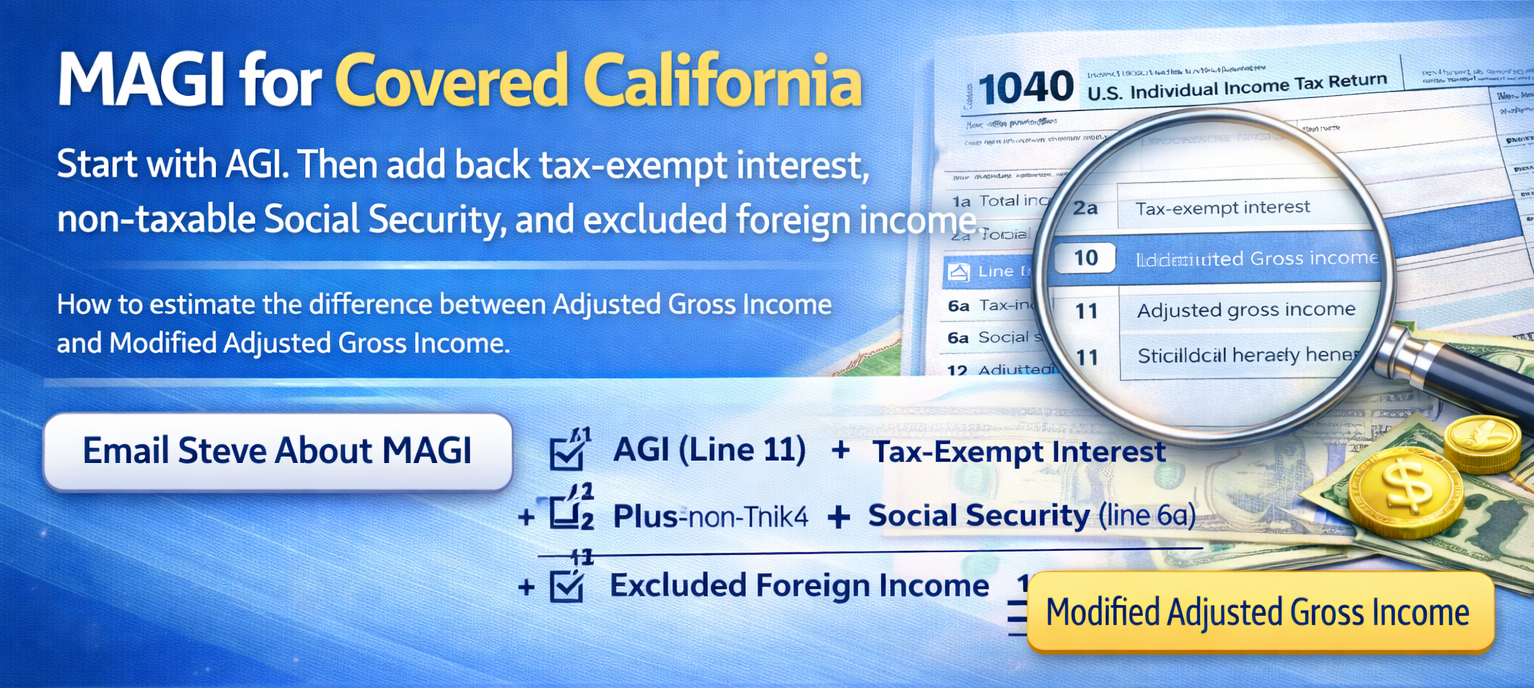

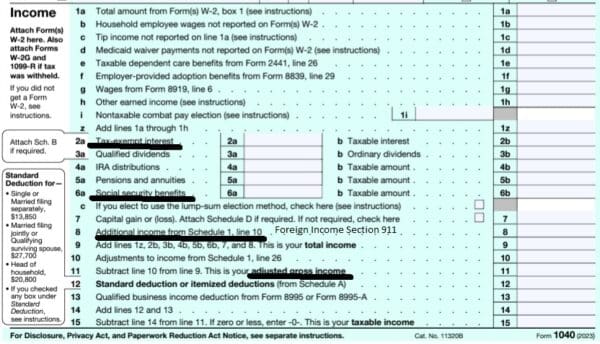

- If you are trying to figure out your Covered California income, the place to start is usually your Adjusted Gross Income (AGI) on Form 1040, Line 11 a

- Then add back, if applicable:

- Tax-exempt Interest Income

- Non-taxable Social Security benefits

- Excluded Foreign Income

- That is generally how you get from AGI to MAGI for Covered California.

- For many people, MAGI is the same as AGI or very close to it. But if you have tax-exempt interest, non-taxable Social Security, or excluded foreign income, your MAGI may be higher than your AGI.

- Important: Covered California is usually looking at your estimated income for the upcoming coverage year, not just what appears on last year’s tax return.

AGI Income Calculator from Tax Act.com

- Why Last Year’s Tax Return Is Only a Starting Point

- Covered California usually wants your best estimate for the upcoming year.

- Last year’s tax return can be a helpful starting point, but if your income is changing, your estimate for the coverage year may be different.

- If your income changes during the year, report the change promptly so your subsidy does not end up too high or too low.

Frequently Asked Questions

- Is MAGI always different from AGI?

- No. For many people, MAGI is the same as AGI line 11a on your 1040 or only slightly different.

- Where do I start on my tax return?

- Start with Form 1040, Line 11a, which is your Adjusted Gross Income.

- What usually gets added back?

- Usually tax-exempt interest,

- non-taxable Social Security, and

- excluded foreign income.

- Should I use last year’s income or this year’s estimate?

- Usually your best estimate for the upcoming coverage year.

- What if I am not sure what to include?

- That is where I may be able to help. Email me [email protected]

- Need Help Estimating Your MAGI?

- If you are not sure what counts and what does not, reach out.

- You can email me your basic numbers, or your recent tax return information, and I can help you estimate your Covered California MAGI.

- Steve Shorr

Covered California Certified Insurance Agent

Email: [email protected]

Links & References

- Covered CA – Countable Sources of Income

- IRS Publication 974 Premium Tax Credit

- Premium Reconciation Form 8962

- Covered CA Income Application Questions

- Household Income

- Mandate to promptly report changes

- Schedule 1 – Lower your income & adjust your income

- IRS Tax Guides Small Biz

- Medicare & Individual IRS Tax Guides

This page is for general educational purposes only and is not tax or legal advice. Final eligibility is determined by official program rules and your application.

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

Know your estimated income? See your 2026 plans and subsidy.

Use the income chart as a starting point, then compare the 2026 health plans available in your ZIP code and see an estimate of your Covered California subsidy.

See My 2026 Plans & Estimated Subsidy

No obligation. There is no extra charge for my help when you use me as your Covered California Certified Insurance Agent.

- Source - Covered CA

- When Your Tax Return Income Makes You Medi-Cal Eligible Insure Me Kevin.com

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

Details… of MAGI

#Household.income means Code of FEDERAL Regulations – IRS Income Taxes – 1.36B 1 – (e) …(1) … the sum of—

(i) A taxpayer’s modified adjusted gross income; (Line 37 Line 11 1040) plus

(ii) The aggregate modified adjusted gross income of all other individuals who—

(A) Are included in the taxpayer’s family under paragraph (d) [below] of this section; and

(B) Are required to file a return of tax imposed by section 1 for the taxable year (determined without regard to the exception under section (1)(g)(7) to the requirement to file a return). [26 USC §6012 ♦ IRS tool to see if you must file a return ♦ Medi-Cal Household Size Flow Chart ♦ Blog – Insure Me Kevin.com] DHCS *

(f) Dependent has the same meaning as in section §152. * IRS Interactive Assistant *

(d) … A taxpayer’s family means the individuals for whom a taxpayer properly claims a deduction for a personal exemption under section 151 for the taxable year.

Family size [Medi-Cal Household Size Flow Chart ♦ Blog – Insure Me Kevin.com] means the number of individuals in the family. Family and family size may include individuals who are not subject to or are exempt from the penalty [mandate] under §5000 A (f) (1) for failing to maintain minimum essential coverage. Health Care.gov explanation *

26 USC § 151 – Allowance of deductions for personal exemptions pdf

(a) Allowance of deductions

In the case of an individual, the exemptions provided by this section shall be allowed as deductions in computing taxable income.

To be more clear — (2) Married taxpayers must file joint return. A taxpayer who is married (within the meaning of section 7703) at the close of the taxable year is an applicable taxpayer only if the taxpayer and the taxpayer’s spouse file a joint return for the taxable year. GPO.Gov Final Regulations Page 11 * Turbo Tax Calculator * Tax Policy Center….. Joint or separate? * Estranged Spouse?

Premium Tax Credit Form 8962 & Instructions

Get a Free No Obligation Calculation of your Tax Credit, Premiums and see the benefit brochures.

View other pages & resources in this section…

- Getting MAGI Right – 23 page primer by George Town University on differences that apply to Medicaid (Medi-Cal) and CHIP Children’s Health Insurance Program Insure Kids now CA

- Power Point presentation CMS Income Counting MAGI

- InsureMeKevin.com analysis

- See also this article on Kevin’s site

View old HISTORICAL versions of this webpage at archive.org

Child & Sibling Pages

{kind=link}

- APTC Advance Premium Tax Credit – Subsidies ARPA

- MAGI Income Chart – Line 11 1040 Covered CA

- Negative MAGI – Medi Cal even if you are rich

- Report a Change – How & When – Especially Income Create Account

- Table of Contents -Income, Deductions & Expenses for MAGI no index

- Alimony – From a Divorce Settlement taxable

- Capital Gains, Sale of Home & Dividends

- Clergy – Housing Allowance? Covered CA MAGI Income

- Covered CA MAGI Retirement Income

- Educational Credits – Student Loan Interest

- Gambling Income & Losses – Other Income Line 21

- Medical or any Debt Cancellation Covered CA MAGI Income?

- Social Security Benefits MAGI Covered CA Income Subsidies

- ACA Health Care Reform – Obamacare Introduction

- 10 Essential Mandatory Benefits + CA Benefits

- Metal Levels – Platinum, Gold, Bronze – Silver & Enhanced

- Enhanced Silver 94, 87, 73 Cost-sharing reductions House v Price

- Grand Fathered Plans What does that mean?

- HSA Health Savings Accounts

- OOP -Out of Pocket Maximum – Participating or Not? Deductibles & Co- Pays

- Provider Finder Quotit

- MLR 80% Medical Loss Ratio – Actuarial Value Minimum Payout

- Special & Open Enrollment Periods Covered CA & Direct with Broker

- Trump Great American Health Plan

- Covered California vs Direct Enrollment

- MAGI – Modified Adjusted Gross Income – Line 11

- APTC Advance Premium Tax Credit – Subsidies ARPA

- MAGI Income Chart – Line 11 1040 Covered CA

- Negative MAGI – Medi Cal even if you are rich

- Report a Change – How & When – Especially Income Create Account

- Table of Contents -Income, Deductions & Expenses for MAGI no index

- Alimony – From a Divorce Settlement taxable

- Capital Gains, Sale of Home & Dividends

- Clergy – Housing Allowance? Covered CA MAGI Income

- Covered CA MAGI Retirement Income

- Educational Credits – Student Loan Interest

- Gambling Income & Losses – Other Income Line 21

- Medical or any Debt Cancellation Covered CA MAGI Income?

- Social Security Benefits MAGI Covered CA Income Subsidies

- Why is Covered CA so confusing