Padding Income or Deductions?

Covered CA Subsidies

What happens if you knowingly put down the wrong income information?

Here’s some research below, about what might happen if you use the wrong income to obtain subsidies or special enrollment.

One may correct their MAGI Income Line 37 + by reading the instructions and then logging into their Covered CA Account or appoint us to do it.

We are NOT tax accountants. Please check with your own CPA, Attorney, IRS or tax adviser. Here’s a memo we just got Sept. 2018, prohibiting us from giving ANY tax advice or guidance and suggestions of where you can get guidance. I do NOT want to hear that you are self-employed and can put in ANY number you want. Please ask a professional to help you with the number you want to put in the application, under penalty of perjury….

Resources & Links

- Fraud in Federal & Covered CA Market Places CNBC 9.12.2016 *

- Covered CA Application (see what you are declaring under Oath)

- tax-whistle blower.com *

- Our webpage on Fraud, Waste & Abuse

- agents and brokers who suspect or know a fraudulent application for insurance has been submitted to report the potential fraud to the California Department of Insurance Fraud Division. Read more >>> Wshblaw.com

- Tools to estimate income

Don’t Fake Income

- Some people falsely increase the income they report to the IRS. This scam involves inflating or including income on a tax return that was never earned, either as wages or as self-employment income, usually in order to maximize refundable credits.

- Just like falsely claiming an expense or deduction you did not pay, claiming income you did not earn in order to secure larger refundable credits such as the Earned Income Tax Credit [or Covered CA Subsidies] could have serious repercussions.

- See tax form 8962 subsidy reconciliation – Premium tax credit

- This could result in taxpayers facing a large bill to repay the erroneous refunds, including interest and penalties. In some cases, they may even face criminal prosecution. Taxpayers may encounter unscrupulous return preparers, Covered CA agents, navigators or Covered CA telephone reps who make them aware of this scam.

- Remember: Taxpayers are legally responsible for what’s on their tax return even if it is prepared by someone else. Make sure the preparer you hire is ethical and up to the task. IRS.Gov

Falsely Padding Deductions on Returns

Avoid the temptation of falsely inflating deductions or expenses on their returns to under pay what they owe and possibly receive larger refunds. Falsely claiming deductions, expenses or credits on tax returns is on the “Dirty Dozen” tax scams list. Taxpayers should think twice before overstating deductions such as charitable contributions, padding their claimed business expenses or including credits that they are not entitled to receive – like the Earned Income Tax Credit, Covered CA Subsidies or Child Tax Credit.

The IRS can normally audit returns filed within the last three years. Additional years can be added if substantial errors are identified or fraud is suspected. Significant civil penalties may apply for taxpayers who file incorrect tax returns including:

- 20 percent of the disallowed amount for filing an erroneous claim for a refund or credit.

- $5,000 if the IRS determines a taxpayer has filed a “frivolous tax return.” A frivolous tax return is one that does not include enough information to figure the correct tax or that contains information clearly showing that the tax reported is substantially incorrect.

- In addition to the full amount of tax owed, a taxpayer could be assessed a penalty of 75 percent of the amount owed if the underpayment on the return resulted from tax fraud.

Taxpayers even may be subject to criminal prosecution (brought to trial) for actions such as:

- Tax evasion

- Willful failure to file a return, supply information, or pay any tax due

- Fraud and false statements

- Preparing and filing a fraudulent return, or

- Identity theft.

Criminal prosecution could lead to additional penalties and even prison time. Using tax software is one of the best ways for taxpayers to ensure they file an accurate return and claim only the tax benefits they’re eligible to receive.

IRS Free File is an option for taxpayers to use online software programs to prepare and e-file their tax returns for free.

Community-based volunteers at locations around the country also provide free face-to-face tax assistance to qualifying taxpayers helping make sure they file their taxes correctly, claiming only the credits and deductions for which they’re entitled by law.

Taxpayers should remember that they are legally responsible for what is on their tax return even if it is prepared by someone else, so they should be wise when selecting a tax professional. The IRS offers important tips for choosing a tax preparer at IRS.gov.

More information about IRS audits, the balance due collection process and possible civil and criminal penalties for noncompliance is available at the IRS.gov website.

Sheriff’s deputies charged with perjury after stopping cops for speeding, then citing for only not having proof of Insurance LA Times 12.14.2019 *

Try turning your phone sideways to see the graphs & pdf's?

- Visit our webpage on how to report changes

- Estimate your MAGI Income

Fraud and #false statements

Any Person who…

(1) Declaration under penalties of perjury – Willfully makes and subscribes any return, statement, or other document, which contains or is verified by a written declaration that is made under the penalties of perjury, and which he does not believe to be true and correct as to every material matter; shall be guilty of a felony and, upon conviction thereof;

- Shall be imprisoned not more than 3 years

- Or fined not more than $250,000 for individuals ($500,000 for corporations)

- Or both, together with cost of prosecution Title 26 USC § 7206(1) *

(2) Aid or assistance – Willfully aids or assists in, or procures, counsels, or advises the preparation or presentation under, or in connection with any matter arising under, the Internal Revenue laws, of a return, affidavit, claim, or other document, which is fraudulent or is false as to any material matter, whether or not such falsity or fraud is with the knowledge or consent of the person authorized or required to present such return, affidavit, claim, or document; shall be guilty of a felony and, upon conviction thereof:

- Shall be imprisoned not more than 3 years

- Or fined not more than $250,000 for individuals ($500,000 for corporations)

- Or both, together with cost of prosecution Title 26 USC § 7206(2) *

- IRS Form1040 Instructions

- See below on perjury

- Get Instant Quotes for Health Insurance

Conspiracy to commit offense or to defraud the United States

If two or more persons conspire either to commit any offense against the United States, or to defraud the United States, or any agency thereof in any manner or for any purpose, and one or more of such persons do any act to effect the object of the conspiracy, each:

- Shall be imprisoned not more than 5 years

- Or fined not more than $250,000 for individuals ($500,000 for corporations)

- Or both Title 18 USC § 371 *

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

IRS Volunteer Income Tax #Assistance (VITA ) program offers free tax help

Covered CA prohibits agents giving tax advice

IRS Volunteer Income Tax Assistance (VITA)

The IRS Volunteer Income Tax Assistance (VITA) program offers free tax help & Covered CA Subsidy compliance to individuals who generally make $54,000 or less, persons with disabilities, the elderly and individuals with limited English proficiency who need assistance in preparing their taxes.

The Tax Counseling for the Elderly (TCE) program offers free tax help for all taxpayers, particularly those who are 60 and older. The IRS certified VITA and TCE volunteers are trained to help with many tax questions, including credits such

- Child and Dependent Care Credit. publication 503

- ACA/Obamacare Subsidies

- How to file taxes and get your refund for free

Warning we just got from Covered CA

Per law and regulation, agents cannot initiate conversations regarding whether or not the consumer is a non-tax filer.

Do not provide any tax filing advice under any circumstance or answer any tax filing questions – refer them to the consumer service center at 1-800-300-1506 with the Primary Tax Filer (or their Authorized Representative) on the line. 9.14.2018 Agent Bulletin *

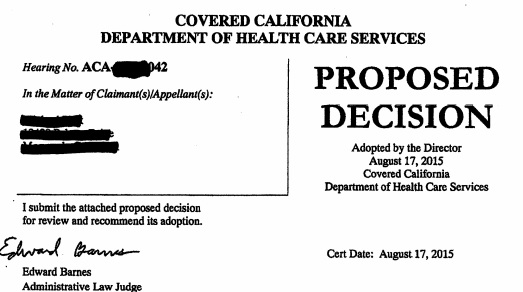

Check out where administrative law judge said he wished he could make Covered CA pay the costs of their bogus advise but didn’t have that authority click to scroll down – view more commentary in our FAQ on Form # 8962 Polk Case.

We are willing though to do research and show you what the law, rule, IRS Publication is. That way IMHO we don’t give advise and aren’t practicing law or accounting.

What happens if you actually call the Covered CA Consumer Center and ask a tax question?

FAQ’s

Covered California Representatives are not permitted to offer tax advice. If an Agent or Consumer have any tax inquires, they are advised to contact their tax professional regarding Federal tax regulations or requirements.

However, the Covered California Website [and ours] has 12 pages of what is MAGI countable income:

And Healthcare.gov – can also be used as a resource for countable income:

You can find examples on the following:

- Question: Is Alimony taxable and considered income?

- Answer: Divorces and separations finalized before January 1, 2019: Include as income. Divorces and separations finalized on or after January 1, 2019: Don’t include as income.

- Question: I have a 25 year old son that lives at home. Should I claim him as a dependent and put him on my Covered California Application?

- Answer: You would need to refer to a tax specialist if you need to claim him as a dependent. Anyone that is claimed as a tax dependent, needs to be listed on the Covered California Application whether they want coverage or not. Email dated Thu 12/30/2021 5:00 PM *

#VITA Volunteers Income Tax Assistance

get your taxes done Free

- Publication 3676 with more details on VITA

- Find a local VITA FREE Provider locator tool

- Turbo Tax -

- See more tax calculation links in the section on IRS Publication 974 Premium Tax Credit

Covered CA Appeals Decision #Polk Case

- Sample Letter for Appeal

- Explanation on Insure Me Kevin . com - Polk Case

- Check out where administrative law judge said he wished he could make Covered CA pay the costs of their bogus advise but didn't have that authority

- Doesn't matter what Covered CA says, it's what the IRS says Form 8962 attaches to Form 1040

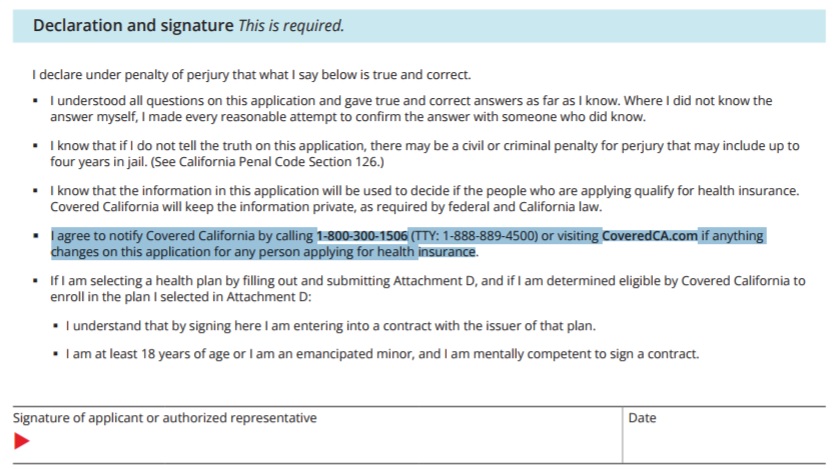

Perjury Declaration - Signature - Agree to notify changes

and that the application is correct in the first place

What is #Perjury?

Perjury is Breaking an oath to tell the truth, the whole truth, and nothing but the truth is perjury. Wikipedia

Telling the truth is good for your health

- Penal Code §118. (a)& 125 provides that:

- a) Every person who, having taken an oath that he or she will testify…before any competent tribunal…willfully and contrary to the oath, states as true any material matter which he or she knows to be false…is guilty of perjury.

- Under California law, falsity element of the crime of perjury requires that a statement be literally false; misleading and nonresponsive testimony that is literally true cannot support a perjury conviction. Chein v. Shumsky,* West’s Ann.Cal.Penal Code § 118 California Criminal Jury Instruction Perjury 2640 * shouselaw.com

- An unqualified statement of that which one does not know to be true is equivalent to a statement of that which one knows to be false.

- In order to lawfully hold a person to answer on the charge of perjury under [California Penal Code] section 118, evidence must exist of a “willful statement, under oath, of any material matter which the witness knows to be false.” Cabe v. Superior Court, (1998) 63 Cal.App.4th 732

- in order for there to be a lawsuit in the first place, somebody involved somewhere along the line is not telling the whole truth. power of attorney.com

- the crime of perjury depends not only upon the clarity of the questioning itself, but also upon the knowledge and reasonable understanding of the testifier as to what is meant by the questioning, we hold that a defendant may be found guilty of perjury if a jury could find beyond a reasonable doubt from the evidence presented that the defendant knew what the question meant and gave knowingly untruthful and materially misleading answers in response. USA v. Dezarn

- Chief Justice Burger emphasized that the perjury statute refers to what the witness “states,” not to what he “implies.” source Bronson v US?

- As the California Supreme Court has stated:

- W]hen ··· a witness’ answers are literally true he may not be faulted for failing to volunteer more explicit information. Although such testimony may cause a misleading impression due to the failure of counsel to ask more specific questions, the witness’ failure to volunteer testimony to avoid the misleading impression does not constitute perjury because the crucial element of falsity is not present in his testimony. Chein v. Shumsky

- a) Every person who, having taken an oath that he or she will testify…before any competent tribunal…willfully and contrary to the oath, states as true any material matter which he or she knows to be false…is guilty of perjury.

Links & Resources

- Crime Victim Restitution Form Interrogatories – CR 200

- The Free Library.com/

- No one should benefit from their own wrong.” Civil Code 3517

- Bronston_v._United_States

- Perjury under Federal Law – Overview

- See above on Fraud & False Statements

Steve Shorr

Website Video #Introduction

- VIDEO What is APTC Advance Premium Tax Credit

- Interactive Tax Assistant (ITA)

- Am I eligible to claim the Premium Tax Credit?

Tax #Estimators

- turbo tax.com - FREE for simple returns

- H & R Block

- E file.com

- Estimate the Subsidy for Health Insurance, benefits, premiums, etc.

- 8962 ONLINE Calculator

- Our webpage on 8962 Premium Tax Credit Reconciliation

- Tax Form Calculator.com

- e tax.com

- Marriage Higher or Lower Taxes?

ACA What You Need To Know #5187 (2020) is the most recent

- VITA - Volunteers to help you

- Publication 17 - Your Federal Income tax

- Health Savings Accounts HSA our webpage

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()