Fraud, Waste & Abuse in Medicare, ObamaCare and Medi-Cal

Fraud, Waste & Abuse in Medicare and Medi-Cal

This page is for general education about healthcare fraud, waste, and abuse. It is intended as a public-service resource, not a political statement or an accusation against any person or organization.

Important: We are not investigators and do not determine whether any specific person, provider, facility, or organization has committed fraud. If you believe wrongdoing may have occurred, use the official reporting channels listed below.

Not every concern is fraud. Some complaints turn out to be misunderstandings, billing mistakes, poor communication, or administrative errors. The safest approach is to gather facts and report concerns through the proper agencies.

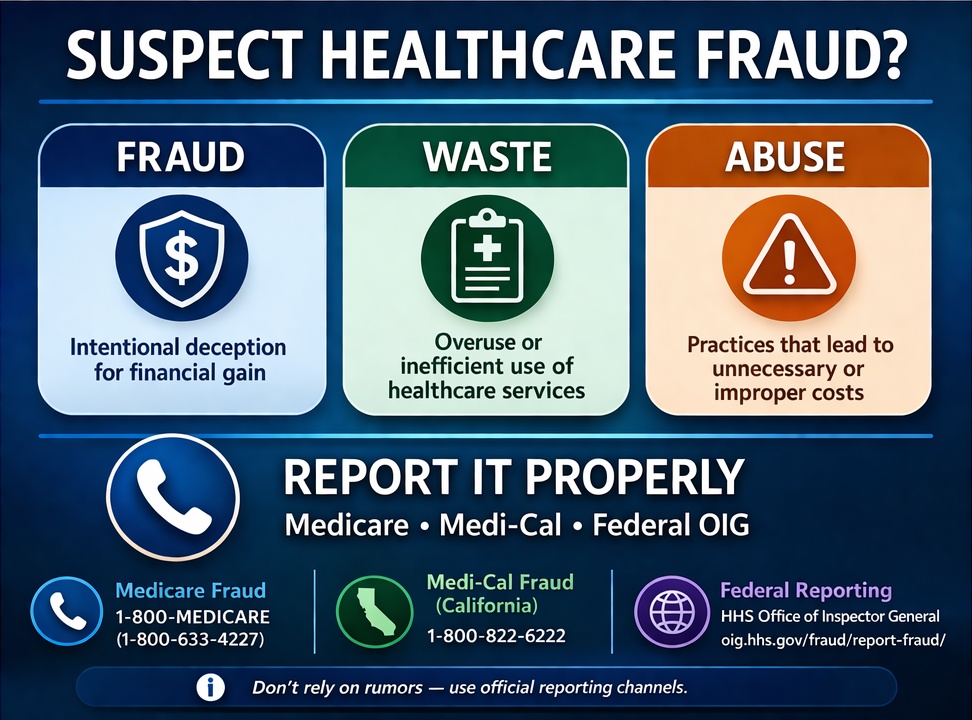

What counts as fraud?

- Billing for services or items that were never provided

- Using false information to obtain payment or benefits

- Kickbacks or illegal referrals tied to federal healthcare business

- Using another person’s Medicare or Medi-Cal identification information

Fraud vs. waste vs. abuse

- Fraud: intentional deception or misrepresentation

- Waste: overuse or inefficient use of services or resources

- Abuse: practices that may create unnecessary costs or improper payments

Before you assume fraud

Healthcare billing and insurance rules are complicated. A concern may involve a real problem, but that does not automatically mean someone committed fraud.

If you have concerns, avoid posting accusations as fact on social media. Make notes about what happened, save documents if you have them, and report the matter through the official channels below.

Where to report suspected fraud

Medicare

For Medicare fraud and abuse reporting information, call 1-800-MEDICARE (1-800-633-4227) or use Medicare’s reporting resources online.

Medi-Cal (California)

The California Department of Health Care Services asks people to report suspected Medi-Cal fraud, waste, or abuse to the DHCS hotline at (800) 822-6222.

Tip: If you are not sure whether something is fraud, you can still submit a report. The agencies decide whether the facts support an investigation.

Examples of concerns worth reporting

- A provider bills for care you never received

- Someone asks to use your Medicare or Medi-Cal number improperly

- You see obvious false statements used to get benefits or payment

- You are pressured into unnecessary services or products tied to billing

- Types of Fraud on this page

Need help understanding your coverage?

If you have questions about Medicare, Covered California, or Medi-Cal eligibility and plan options, we can help explain the rules and point you in the right direction.

Health Care Fraud is #defined as

“knowingly and willfully executing, or attempting to execute, a scheme or artifice

- to defraud any health care benefit program; or

- to obtain, by means of false or fraudulent pretenses, representations, or promises, any of the money or property owned by, or under the custody or control of, any health benefit program.”

Healthcare fraud can result in civil and criminal penalties that include fines, monetary damages, and even imprisonment. Additionally, there is a penalty of up to 20 years in prison or life in prison if the violation resulted in a person’s death. 18 U.S.C. §1347

Fraud occurs when

someone knowingly lies to obtain some benefit or advantage to which they are not otherwise entitled or someone knowingly denies some benefit that is due and to which someone is entitled.

Waste

Waste includes overusing services, or other practices that, directly or indirectly, result in unnecessary costs to the Medicare Program. Waste is generally not considered to be caused by criminally negligent actions but rather by the misuse of resources.

Abuse

Abuse includes actions that may, directly or indirectly, result in unnecessary costs to the Medicare Program. Abuse involves payment for items or services when there is not legal entitlement to that payment and the provider has not knowingly and/or intentionally misrepresented facts to obtain payment. The Medicare Learning Network®

Pamphlets, Brochures & Websites to help prevent Fraud

- Protect yourself from Medicare Fraud Publication # 10111

- Prevent Fraud Publication # 11491

- Medicare Learning Network Prevent, Detect & Report Fraud & Abuse

- California Department of Insurance on Fraud

-

New MD’s – how to avoid Medicare & Medicaid – Medi Cal Fraud and Abuse

- Medicare Fraud & Abuse-12-17-15 Hi Cap CA Health Care Advocates

- Doctor who performed unneeded procedures guilty in $12-million Medicare fraud scheme Los Angeles Times

- CMS will be able to revoke healthcare providers or suppliers’ Medicare enrollment if they are affiliated with targeted “bad actors,” a final rule issued Wednesday established.

- As part of the CMS’ “Program Integrity Enhancements to the Provider Enrollment Process” going into effect Nov. 4, its new “affiliations” provision allows authorities to bar individuals and organizations that “pose an undue risk of fraud, waste or abuse based on their relationships with other sanctioned entities.” Modern Health Care *

- Medicare and Medicaid fraudsters continue to steal taxpayer money

- The rising tide of insurance fraud: an estimated $308B problem

YouTube VIDEO's

Important: This page is for general education about healthcare fraud, waste, and abuse.

We are not investigators and do not determine whether any specific person or organization has committed fraud. If you believe fraud has occurred, please use the official reporting resources below.

This information is provided as a public service to help consumers understand how the system works and where to report concerns.

- How to Report Fraud at ReportFraud.ftc.gov VIDEO

- Here’s where to Report Social Security Fraud, Scams, Waste & Abuse Office of the Inspector General

- 1.800.Medicare

- Blue Shield Fraud Hotline [email protected] (800) 221-2367

- Blue Cross

- Health Net

- Social Security Fraud

- CMS complaint form.

- report fraud.ftc.gov

- irs.gov/report-phishing

- usa.gov/stop-scams-frauds

- fbi.gov/scams-and-safety/on-the-internet

- justice.gov/report-fraud

- support.apple.com Recognize and avoid phishing messages, phony support calls, and other scams

- amazon.com/report something suspicious

- microsoft.com/protect-yourself-from-phishing

- support.google.com Avoid and report phishing emails

- Preventing Real Estate Fraud Publication # 17

- nicb.org/National Insurance Crime Bureau /report-fraud

- HHS.Gov Office of Inspector General

Steve Shorr

Website Video #Introduction

Breaking News

#Latest Busts

- Feds announce massive investigation of $2.75B in health care fraud

- Medicare Fraud Prevention Week 2024

- CMS urged to crack down on health insurance ‘twisting’ Insurance News Net 5/29/2024 *

- Biden Administration Blocks Two Private Sector Enrollment Sites From ACA Marketplace Kff 8/22/2024

- CMS cracks down on ACA brokers to prevent plan switching Health Care Drive 7/22/2024 *

- Unauthorized ACA plan switches drive call for action against rogue agents NPR

- 2 brothers plead guilty to roles in $67M Medicare fraud scheme

- Feds: Fake death certificates part of macabre $26M insurance fraud scam

- Feds charge 4 people in a multimillion-dollar Amtrak health insurance scam

- Seven Californians among people charged in $150-million COVID aid fraud scheme LA Times 4.20.2022

- HHS proposes crackdown on fraudulent ACA signups by brokers Benefits Pro 1.2022

- Mahyar David Yadidi – a San Pedro, California, chiropractor – to prison and ordered him to make restitution for defrauding the International Longshore and Warehouse Union-Pacific Maritime Association (ILWU-PMA) Welfare Plan. The court’s action follows an investigation by the U.S. Department of Labor’s Employee Benefits Security Administration (EBSA) and Office of Inspector General (OIG).

- HHS to look at MA risk adjustment as upcoding in spotlight

- The Cash Monster Was Insatiable’: How Insurers Exploited Medicare for Billions . Most large insurers in the program have been accused in court of fraud.

- 91 Charged in Federal Health Care Fraud Sting Kaiser News

- The court sentenced Mahyar David Yadidi – owner of Philips San Pedro Chiropractic – to 46 months in prison and ordered to make $1,976,832 in restitution for defrauding the maritime union welfare plan. DOL.gov *

- It’s alleged Adam Hocking created fictitious insurance policies and documents for clients, and accepted payments for the same, when no such policies existed. These actions resulted in Iowa consumers being left uninsured when they attempted to file a claim as a result of a loss. Insurance Journal * Charging Complaint on BrokerPurdue Pharma to plead guilty

- OxyContin maker’s admission won’t end liability for executives or the Sackler family.

- New Medicare Rule Aims to Take Back $4.7 Billion From Insurers

The government plans to aggressively audit Medicare Advantage plans for overbilling but may face lawsuits. - CA Health Line 7.19.2017 Fraud & Billing mistakes in Medicare Advantage plans ran $16B in 2016, if you include standard Medicare $60B.

- Orange County Register: Brea Man Gets Decade In Prison In $2.9 Million Dollar Medicare Fraud A Brea man who used his rehabilitation clinics to submit millions of dollars in false Medicare claims was sentenced this week to more than a decade in federal prison, even as he awaits sentencing in a second health care fraud case. U.S. District Judge David O. Carter, during a hearing at the federal courthouse in Santa Ana, ordered Simon Hong on Monday to spend 121 months behind bars and to pay nearly $3 million in restitution, according to the U.S. Department of Justice. (Emery, 1/10)

- Aetna wins $37.4 M civil judgement for fraudulent bills from Bay Area Surgical Management Learn More===> Mercury News 4.21.2016

- Indictments – a doctor at the clinic documented evaluations that never happened, while staff falsified records to justify surgeries, some of which were unnecessary. Further, the indictment said some surgeries were performed by a physician’s assistant who had not attended medical school and was not overseen by a surgeon during the procedures. Although the patient victims sustained physical harm, we who pay higher premiums for health care suffer economic harm when scams are allowed to continue unchecked” (Winton/Hamilton, “L.A. Now,” Los Angeles Times, 9/15). CA Healthline 9.16.2015

- Durable Medical Equipment Fraud – LA Times 9.4.2015

- Nearly 250 people, including 46 providers, were charged with falsely billing Medicare a total of nearly $712 million – Medicare Fraud Strike Force, which has charged more than 2,300 people accused of falsely billing Medicare more than $7 billion since it was established in 2007 —

- federal officials charged:

- Three owners of a hospice service in Detroit who allegedly paid kickbacks for referrals from two physicians who wrote medically unnecessary prescriptions;

- Two home health care companies in New Orleans that allegedly billed Medicare $38 million for glucose monitors they sent to patients regardless of medical need; and

- Administrators of a mental health center in Miami that allegedly paid kickbacks to owners of assisted living facilities and patient recruiters (Department of Justice release, 6/18). CA Health Line 6.19.2015

- Fraud investigations – 3.3B recovered in 2014 Learn More ⇒ CA Healthline 3.19.2015

- CA Healthline 12.5.2014 – New rule to allow Medicare to deny payments to providers with a history of abuse

IRS Urges Public to Stay Alert for #Scam Phone Calls

The IRS continues to warn consumers to guard against scam phone calls from thieves intent on stealing their money or their identity. Criminals pose as the IRS to trick victims out of their money or personal information. Here are several tips to help you avoid being a victim of these scams:

- Scammers make unsolicited calls. Thieves call taxpayers claiming to be IRS officials. They demand that the victim pay a bogus tax bill. They con the victim into sending cash, usually through a prepaid debit card or wire transfer. They may also leave “urgent” callback requests through phone “robo-calls,” or via phishing email.

- Callers try to scare their victims. Many phone scams use threats to intimidate and bully a victim into paying. They may even threaten to arrest, deport or revoke the license of their victim if they don’t get the money.

- Scams use caller ID spoofing. Scammers often alter caller ID to make it look like the IRS or another agency is calling. The callers use IRS titles and fake badge numbers to appear legitimate. They may use the victim’s name, address and other personal information to make the call sound official.

- Cons try new tricks all the time. Some schemes provide an actual IRS address where they tell the victim to mail a receipt for the payment they make. Others use emails that contain a fake IRS document with a phone number or an email address for a reply. These scams often use official IRS letterhead in emails or regular mail that they send to their victims. They try these ploys to make the ruse look official.

- Scams cost victims over $23 million. The Treasury Inspector General for Tax Administration, or TIGTA, has received reports of about 736,000 scam contacts since October 2013. Nearly 4,550 victims have collectively paid over $23 million as a result of the scam.

The IRS will not:

- Call you to demand immediate payment. The IRS will not call you if you owe taxes without first sending you a bill in the mail.

- Demand that you pay taxes and not allow you to question or appeal the amount you owe.

- Require that you pay your taxes a certain way. For instance, require that you pay with a prepaid debit card.

- Ask for your credit or debit card numbers over the phone.

- Threaten to bring in police or other agencies to arrest you for not paying.

If you don’t owe taxes, or have no reason to think that you do:

- Do not give out any information. Hang up immediately.

- Contact TIGTA to report the call. Use their “IRS Impersonation Scam Reporting” web page. You can also call 800-366-4484.

- Report it to the Federal Trade Commission. Use the “FTC Complaint Assistant” on FTC.gov. Please add “IRS Telephone Scam” in the notes.

If you know you owe, or think you may owe tax:

- Call the IRS at 800-829-1040. IRS workers can help you.

Phone scams first tried to sting older people, new immigrants to the U.S. and those who speak English as a second language. Now the crooks try to swindle just about anyone. And they’ve ripped-off people in every state in the nation.

Stay alert to scams that use the IRS as a lure. Tax scams can happen any time of year, not just at tax time. For more, visit “Tax Scams and Consumer Alerts” on IRS.gov.

Each and every taxpayer has a set of fundamental rights they should be aware of when dealing with the IRS. These are your Taxpayer Bill of Rights. Explore your rights and our obligations to protect them on IRS.gov.

Scammers also know that whenever there’s a change or even discussion about possible changes in government programs or policy, the time is ripe to capitalize on consumers’ uncertainty by trying to get them to reveal personal information.

- Government agencies already have your personal information on file. Unless you initiate contact, you will never be asked to provide or verify that data.

- Don’t be fooled if your Caller ID screen indicates that a call is from an agency you recognize. Scammers have technology that lets them display any number or organization name on your screen.

- Government agencies do not send unsolicited emails. Official correspondence is typically delivered by U.S. mail. If you get such a letter, you can authenticate it by looking up the agency’s phone number yourself in a directory and calling the agency.

- Don’t expect government employees to make unannounced door-to-door visits about new or revised programs. You’ll typically receive advance notification of any official knock on your door, and your personal information will already be known to legitimate federal employees.

Fraud Statutes

Fraud #Statutes – Laws

- Civil False Claims Act 31 United States Code (U.S.C.) Sections 3729-3733

- Health Care Fraud Statute 18 U.S.C. Section 1346

- Criminal Fraud 18 U.S.C. Section 1347

- Anti-Kickback Statute; 42 U.S.C. Section 1320a-7b(b)

- Stark Statute (Physician Self-Referral Law); 42 U.S.C. Section 1395nn

- Health Insurance Portability and Accountability Act (HIPAA). Our HIPAA webpage

- Office of Inspector General – Compliance Resource Center

- PART 422 – MEDICARE ADVANTAGE PROGRAM

- PART 423 – VOLUNTARY MEDICARE PRESCRIPTION DRUG BENEFIT

- Prescription Drug Benefit Manual Chapter 9 – Compliance Program Guidelines and Medicare Managed Care Manual Chapter 21 – Compliance Program Guidelines

- CRIMINAL PENALTIES FOR ACTS INVOLVING FEDERAL HEALTH CARE PROGRAMS

Sec. 1128B. [42 U.S.C. 1320a–7b] - CIVIL MONETARY PENALTIES Sec. 1128A. [42 U.S.C. 1320a–7a]

THE INSURANCE FRAUDS PREVENTION ACT

- False and Fraudulent Claims 1871-1871.8

- Bureau of Fraudulent Claims 1872-1872.96

- Insurance Fraud Reporting 1873-1873.4

- Motor Vehicle Theft and Motor Vehicle Insurance

- Fraud Reporting 1874-1874.81

- Insurer Inspections 1874.85-1874.87

- Auto Insurance Fraud Crisis Areas 1874.90-1874.91

- Arson Investigations .1875-1875.8

- Insurance Claims Analysis Bureaus 1875.10-1875.18

- Insurer Fraud Investigation 1875.20-1875.23

- Deposit of Automobile Insurance Claims Information .1876-1876.5

- Workers’ Compensation Insurance Fraud Reporting 1877-1877.5

- Insurance Fraud Prevention §1879-1879.8

- USC 1347 Federal Law on Health Care Fraud

- Medicare – Part D Fraud – Final Rules – Federal Register

Web visitor Q & A

What year are you working through these Death Plans [Medicare Advantage]? I have been fighting with xyz (which is a misnomer because is has no advantage ) since 2018 and and up to Level 4 with appeals and Maximus.

There is no control over Managed Health Plans.

There are no consequences for Managed Health Plans abusing seniors taking money from Medicare and tell bold face lies to cover their tracks.

We need a class action case but who will we take on? All Managed Health Plans do these things to some extent. Things will only get worse.

Managed Health Plans have tons of control.

- I fear selling them! I’m not even allowed to discuss them with you, unless you sign a permission slip first!

- Marketing Rules – Best Plan – SOC Scope of Appointment

- Medicare & You – Publication #10050 – See Fraud Section

- Help Prevent Fraud # 11491 double check your claims

- Stop Medicare Fraud Website

- Publication #10111 – Protecting Yourself and Medicare from Fraud

- Fraud, Waste & Abuse Compliance Training CA Health Advocates.org:

Consumer Resources

- Learn More ⇒

- Individual Plans – Health Care Reform – Abuse of Special Enrollment Period – Blog Insure Me Kevin.com

- File a complaint CA Dept of Insurance Enforcement Branch Overview

- Insurance Journal Fraud Search

- Blue Shield – Fraud Unit(800) 221-2367

- Report Fraud Waste or Abuse to Blue Cross

- www.nicb.org/ National Insurance Crime Bureau

- How to Avoid Becoming a Victim of Insurance Fraud

An illustrated brochure describing the warning signs of insurance fraud and some concrete steps you can take to avoid becoming a victim. This brochure contains information helpful to all consumers. It details several types of insurance fraud, such as fake policies, premium fraud, unlicensed agents, unnecessary services, and insurance scams. It also describes how to get your money back and where to complain about insurance fraud. - National Health Care Anti-Fraud Association is the leading national organization focused exclusively on the fight against health care fraud. We are a private-public partnership — our members comprise more than 100 private health insurers and those public-sector law enforcement and regulatory agencies having jurisdiction over health care fraud committed against both private payers and public programs. Established in 2000,

- The NHCAA Institute for Health Care Fraud Prevention is a separately incorporated, tax-exempt educational foundation that provides education and training to private- and public-sector health care anti-fraud personnel.

- Preventing Credit Card Fraud: Learn How to Protect Yourself

A brochure, available in English and Spanish that describes how crooks steal and use credit cards and card numbers and explains how to protect your credit card and what to do if your card has been stolen.

By Consumer Action. - California Court Website on Fraud & Cyber Crime

- Report Worker’s Compensation Fraud

- cms.gov physician-self-referral

- The Victims of Corporate Fraud Compensation Fund (VCFCF) provides limited restitution to victims of corporate fraud who have otherwise been unable to collect on their judgment. SOS.CA.Gov

#Money Laundering

- Patriot Act

- Placement is the initial stage in which money from criminal activities is placed in financial institutions.

- One of the most common methods of placement is structuring—breaking up currency transactions into portions that fall below the reporting threshold for the specific purpose of avoiding reporting or recordkeeping requirements. Because most carriers do not accept cash payments, insurance producers should be on the lookout for cash equivalents. Gene’s opening of multiple accounts and making payments with bank checks of less than $10,000 are examples of placement and structuring.

- Layering is the process of conducting a complex series of financial transactions, with the purpose of hiding the origin of money from criminal activity and hindering any attempt to trace the funds. In this scenario, Gene’s movement of money between accounts and his exercise of the 10-day free-look provision are examples of layering.

- Integration is the final stage in which an apparently legitimate transaction is used to return the now-laundered funds back to the criminal. Gene’s request to take redemptions from his mutual funds is considered integration as he now has checks from financial institutions. knowledge.limra.com

Insurance Agent – Broker Duty to #Report1 Fraud

- Agents and brokers will be required to report fraud (See links below) to the California Department of Insurance (CDI).

- More specifically, SB 1242 amends the California Insurance Code to require producers who suspect or know a fraudulent application or claim for insurance is being made to submit to the DOI Fraud Division via the electronic Consumer Fraud Reporting Portal (see below) information regarding the factual circumstances of a dubious application and the alleged misrepresentations it contains.

- This must be done within 60 days after the producer determines fraud has or may have occurred. Of note, the mandated notification cannot be made anonymously.

- Where suspected or known fraud is discovered after an application has been placed with a carrier, the agent or brokers will be obligated from January 1 onward to report it to the impacted insurer (specifically, their special investigation unit), along with all documents and evidence that the unit may later request.

- These reporting obligations are entirely new. Only carriers were previously burdened with fraud reporting requirements.

- Consequently, agents and brokers should not turn a blind eye to obvious fraudulent conduct by any insurance applicant. Doing so could come with risk. SB 1242 creates regulatory exposure for failing to comply with the law.

- The good news is that agents and brokers who fulfill their duties by reporting fraud or assisting with related investigations are insulated from civil liability, assuming they have acted in good faith. Insurance Journal *

Related Web Pages

- Medical Necessity rules & definition

- Medicare Learning Network, Fraud, Waste & Abuse 16 pages

- The OIG’s List of Excluded Individuals and Entities (LEIE) The General Services Administration (GSA) database

- Department of Health and Human Services Office of Inspector General

- CMS compliance guidance for MA and Part D plans

- Combating Fraud to keep rates low InsureMeKevin.com

Medi Cal & ACA Obamacare Fraud

- Medi Cal Fraud Website DHCS.CA.Gov

- 1-800-822-6222

- [email protected]

- Medi Cal Internal Memo 1.25.2019 on reporting Fraud and Overpayments

- All About Medicaid Fraud Defense, from Our National Healthcare Criminal Lawyers Chapman Law Group

- Mandate to report changes in income or assets promptly

- Video Medi Cal Fraud – who can be charged? Shouse Law

FAQ’s

Medicare Advantage – Risk Adjustment Fraud

#Risk Adjustment Fraud?

“making patients look sicker than they are,”

False COVID Statistics?

With COVID going on, so many on Facebook are saying the COVID numbers are inflated so that hospitals & insurance companies can get more $$$. Based on the rules of Risk Adjustment Fraud, I don’t think so. Here’s the CDC rules for reporting deaths due to COVID. See also the video at right or scroll down.

xyz and Anthem Blue Cross (and another article) were once accused of “gaming” the Medicare Advantage payment system by

“making patients look sicker than they are,” Risk Adjustment Fraud?

Damages are speculated to top $1 billion.

Medicare Advantage is a popular alternative to traditional Medicare. The privately run health plans have enrolled more than 18 million elderly and people with disabilities — about a third of those eligible for Medicare — at a cost to taxpayers of more than $150 billion a year.

“This is not one company engaged in episodic bad behavior, but a lucrative business plan that appears to be national in scope,”

When Congress created the current Medicare Advantage program in 2003, it expected to pay higher rates for sicker patients than for people in good health using a formula called a risk score.

Resources, Links & Bibliography

- Our webpage ACA/Obamacare on Risk Adjustment and other transfer of costs/risks

- The Centers for Medicare & Medicaid Services (CMS) risk-adjusts payments by using beneficiaries’ diagnoses to pay higher capitated payments to MA companies for beneficiaries expected to have higher-than average medical costs. This may create financial incentives for MA companies to make beneficiaries appear as sick as possible. hhs.gov *

- kff health news.org/insurers-bilked-50b-from-medicare-for-dubious-diagnoses-review-finds/

- An appellate court Friday ruled against xyz insurers, overturning a lower court decision they claimed resulted in underpayment of Medicare Advantage insurers. Modern Health Care *

- Court Rules in favor of xyz

- CA Health Line 5.17.2017 79 page lawsuit filed

- Medicare Part C Fraud: What is it and How to Stop It

- Insurance industry still victimized by growing number of scammers

- Study finds insurance fraud costs at a record $308.6 billion annually

- Medicare phone scam targeting seniors on the rise

- Ex-NBA player pleads guilty in health insurance fraud case

- MedPAC is recommending a new method to make Medicare Advantage risk adjustment more accurate. Here's how

- AHA presses for False Claims Act probes to target payers over Medicare Advantage denials

- Feds brokered record $5B in healthcare fraud cases last year

- Miami doctor sentenced in $38 million health care fraud scheme

- Ramesh “Sunny” Balwani was convicted on 12 charges. Meanwhile, in California a whistleblower physician was reinstated at a Los Angeles Veterans Affairs hospital; the surgeon general addressed health worker burnout; concerns raised over digital mental health companies; and more.

- Justice Department charges 36 in $1.2 billion healthcare fraud schemes

- CA Health Line 3.28.2017

- public integrity.org/medicare-advantage-money-grab

- Medicare Managed Care Manual Chapter 7 – Risk Adjustment

- npr.org/audits-of-some-medicare-advantage-plans-reveal-pervasive-overcharging

- sheppard health law.com/doj/xyz-group/

- CMS identified violations and sent a notice on 11.22.2016 of Part D formulary and benefit administration requirements that resulted in xyz ’s enrollees experiencing inappropriate denials of and/or delayed access to Part D prescription drugs at the point of sale. The fine is $2.5M.

- Freedom Health & Optimum Health Care settle for a $32m fine CA Healthline 5.30.2017

- Our webpage on Risk Adjustment Fraud & Improperly Denying Service

- CMS on Risk Adjustment

- Explaining Health Care Reform: Risk Adjustment, Reinsurance, and Risk Corridors KFF

- Overview of Risk Adjustment and Outcome Measures for Home Health Agency OBQI Reports: Highlights of Current Approaches and Outline of Planned Enhancements CMS

- Why risk adjustment is a crucial component of individual market reform Brookings

- Some Medicare Advantage Companies Leveraged Chart Reviews and Health Risk Assessments To Disproportionately Drive Payments Office of Inspector General

Wrongfully denying claims that should have been covered under Medicare

- Medicare Advantage Denying Care and Overcharging - allegations - Kaiser Health News June 29, 2022

- Medicare for All???

- 13% of Medicare Advantage enrollees had a claim or pre-authorization request denied

- ny times.com deny care medicare-advantage-plans-report

- Audits — Hidden Until Now — Reveal Millions in Medicare Advantage Overcharges

- xyz Doctors Got Diagnoses Checklists To Boost Medicare Payouts

- industry drive to tamp down critics — and retain billions of dollars in overcharges.

What is Risk Adjustment in Medicare Advantage?

**********

Sample Health #Risk Assessment Questionnaire

Health Promotions and Disease Prevention

Breaking News

https://thehill.com/policy/healthcare/5966489-hhs-oig-crackdown-fraud/

https://www.healthcaredive.com/news/hhs-watchdog-focused-fraud-medicaid-medicare-advantage-enforcement-oig/825034/

https://www.coveredca.com/consumer-protection/

https://hbex.coveredca.com/toolkit/downloads/IFM_Fraud_Referral_Guide.pdf

https://hbex.coveredca.com/toolkit/downloads/Privacy_and_Information_Security_Guide.pdf

https://apps.docusign.com/webforms/us/bec9ad6630cdf7767617e27a39279e8f?r=1

https://youtu.be/HrTarwxXo7U?si=2_veQ6VJFGrSYD3i

https://paragoninstitute.org/private-health/the-persistent-obamacare-enrollment-fraud/

https://share.google/aimode/WyK7yatcYcV1hyoHU

Body Brokering still going on

https://www.youtube.com/watch?v=nJgO4Tuc0rQ

https://enewspaper.dailybreeze.com/html5/reader/production/default.aspx?pubname=&edid=099d55a7-a5cb-45f3-8bfd-7db85edf744d&pnum=1&utm_email=B5035514749565C6A445E4F04E&utm_source=listrak&utm_medium=email&utm_term=https%3a%2f%2fedition.pagesuite.com%2flaunch.aspx%3feid%3d099d55a7-a5cb-45f3-8bfd-7db85edf744d%26pnum%3d1&utm_campaign=scng-torrance_daily_breeze-eNotify-nl&utm_content=eNotify

https://youtu.be/SdOG4RsMaCM?si=SDwcgC2EdTr1DWJY

https://www.healthaffairs.org/content/forefront/unfounded-fraud-allegations-threaten-vital-medicaid-home-and-community-based-services

https://cahealthadvocates.org/hicap/

https://youtu.be/Co5kGZMnKYo?si=2b9UaLRbpDy81Uds

https://cahealthadvocates.org/watch-out-for-free-genetic-test-scams/

https://cahealthadvocates.org/senior-medicare-patrol-home/

https://apnews.com/article/dr-oz-cms-fraud-trump-medicaid-health-20e1315861bf715bf5f9d977fd99e9f0

https://www.shouselaw.com/ca/defense/fraud/medi-cal-fraud/

https://www.facebook.com/reel/970584748798467/?mibextid=CDWPTG

https://youtu.be/-3qzF3hXR3Q?si=zq9uG2EEUanwwszu

https://youtu.be/NYAL2a7ytek?si=fNZ1zGIi6OHmfgNw

https://www.cms.gov/files/document/overviewfwaprovidersbooklet072616pdf

https://kffhealthnews.org/morning-breakout/unitedhealths-extreme-tactics-upped-medicare-payouts-senate-inquiry-finds/