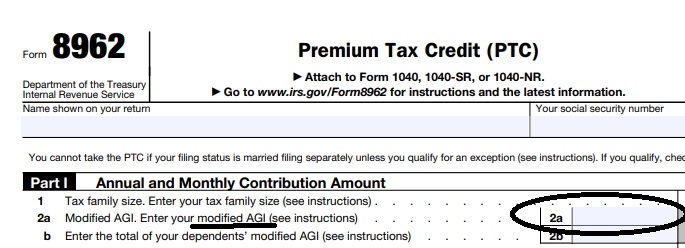

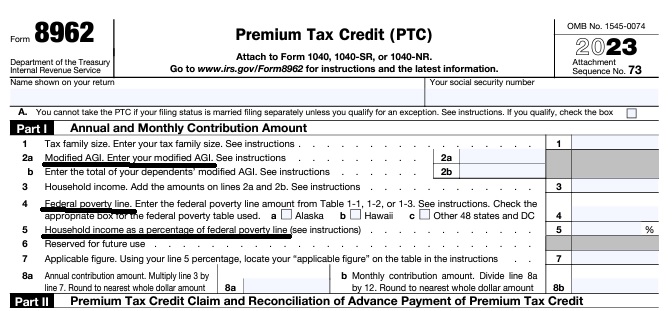

IRS Premium Tax Credit Form #8962 & FTB 3849

is used to reconcile the APTC Advance Premium Tax Credit

subsidy with your IRS # 1040.

Federal IRS #Form8962 Instructions Premium Tax Credit

Reconciliation Form for Covered CA Subsidies attaches to 1040

Subsidy is IMHO hocus pocus - smoke & mirrors

it all comes out when you file taxes!

-

Introduction

-

If you got too high a subsidy or too low, it gets reconciled at tax time on form 8962. If your subsidies were too high you may have to pay the excess back and maybe penalties, if too low, you can get a tax refund or lower the amount you have to pay. In a lot of ways, IMHO subsidies are hocus pocus, jiggery pokery - smoke and mirrors as it's all guesswork and promises. Be sure to report income and household changes within 30 days.

- Instructions for IRS Form #8962 Subsidy Reconcilation

- Tracking Your Covered California Subsidy on your 1040 Federal Tax Return Insure Me Kevin.com

- ARPA & Inflation Reduction Act of 2022

- Instead of increasing taxpayer audits, policymakers should simplify taxes across the board. That way, it would be easier for everyone to pay the correct amount to the government. heritage.org/who-those-87000-new-irs-agents-would-audit

- That 87,000 new tax agents estimate represents everything from IT techs to customer service people who answer the phone and help you file your return. Second, it includes attrition. So, the actual enforcement personnel is 5,000 LA Times * Mother Jones

- IRS backlog hits nearly 24 million returns, further imperiling the 2022 tax filing season

- ARPA Stimulus - you don't have to pay back 2020 overage on subsidies IRS.Gov *

- InsureMeKevin.com on subsidies & pay backs... 1.25.2022 update ARPA and 600% CA

- 1040 Instructions

- Overview FTB site

- How to Reconcile Subsidies FTB

- Calculate Pay Back

- Assistance Repaying California Subsidies

- covered ca.com/the most you might have to pay back

- 2022 Insure Me Kevin.com

- Our webpage on Form 8962 - Premium Tax Credit Subsidy Reconciliation

- VIDEO What is APTC Advance Premium Tax Credit

- Health Net VIDEO How to get subsidies – pay less for coverage

- Interactive Tax Assistant (ITA)

- Am I eligible to claim the Premium Tax Credit?

- IRS FAQ on Premium Tax Credit

Tax #Estimators

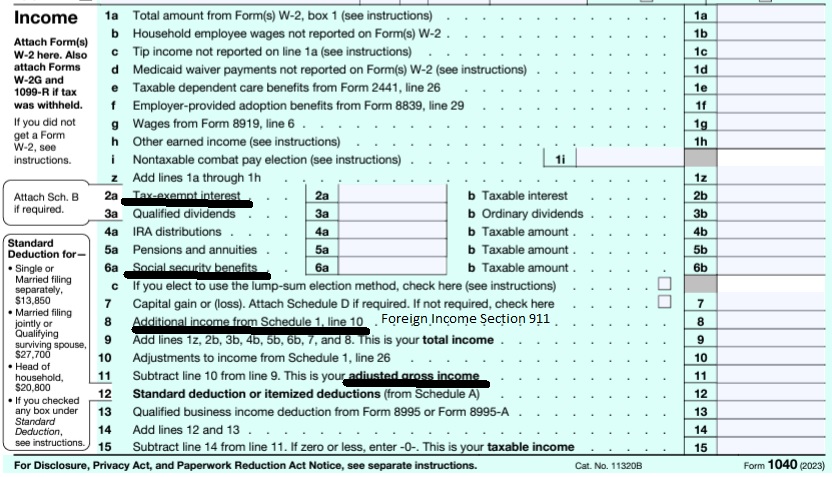

What was last years MAGI Income?

Estimate for the upcoming year.

Calculate your Covered CA MAGI Income

take #Line8b 11 Adjusted Gross income then add line 2a, 6a & 8 (Foreign Income)

- 1040 IRS Annual Tax Form

- Schedule 1 Additional Income & Adjustments to Lower your MAGI Income

- Estimate next years MAGI Income?

- Get instant quotes, subsidy calculation and coverages

- NO ASSET TEST for MAGI based subsidies in Covered CA or MAGI Medi Cal Qualification. Steve's VIDEO

- Nor is there a lien against your estate for Covered CA or MAGI Medi Cal

Schedule 2 1040 Additional Taxes

- Part I Tax

- Part II Other Taxes

- 4 Self-employment tax. Attach Schedule SE

- 5 Social security and Medicare tax on unreported tip income. Attach Form 4137

- 17 Other additional taxes:

More Instructions

- Covered CA Video on tax forms

- See form 2210 Underpayment of tax and the instructions for more details.

- Form # 8962 Instructions HTML * pdf *

- but first you need the Proof of Coverage Form 1095 A from Covered CA

- and B if applicable – like if you had Covered CA part of the year and other coverage the rest of the year, from an Insurance Company, Government – Like Medicare or Medi-Cal or your Employer.

- When you are done completing # 8962, enter the calculation on line 46 and/or 69 of 1040 form.

- Schedule 1 Additional Income & Adjustments to Income

- Do you think this process is complicated?

- See what my CPA thinks.

- Colleagues explanation of how to reconcile

- I got a new job.. why aren’t I getting subsides anymore?

How to report changes

12c Letter

What to Do if You Get a 12c #Letter about the Premium Tax Credit

or your missing form 8962?

If you get a IRS Letter 12C about the Covered CA premium tax credit, read further, here’s what it’s all about.

Why am I getting this letter?

The IRS sent you this letter because Covered CA notified them that they made advance payments of the premium tax credit – subsidy on your behalf to your or your family’s insurance company last year.

- You also received this letter because – when you filed your individual tax return – you didn’t reconcile the advance payments of the premium tax credit, using form Form 8962,

- VIDEO on Missing IRS 12 C or 8962

What do I need to do now?

More detail

- You must respond to the letter, even if you disagree with the information in it. If you disagree, send the IRS a letter explaining what you think is in error.

- If you received this letter, but didn’t enroll in health insurance through Covered CA, where you can have a broker at no additional charge, you must let the IRS know.

- The letter outlines the information you should provide in your response, which includes:

-

- A copy of the Form 1095-A, where Covered CA shows the subsidies you got for the year.

- A completed Form 8962

- The second page of your tax return, which includes the “Tax and Credits” and “Payments” sections, showing the necessary corrections and your signature. You must complete either the line for “excess advance premium tax credit repayment” or the line for “net premium tax credit.”

- If you originally filed a Form 1040EZ tax return, you must transfer the information from your Form 1040EZ to a Form 1040A and include it with your response to the 12C letter.

Is there anything else I need to know?

- If it’s Covered CA we can do that for you, when you appoint us as your agent – here’s instructions.

- If you need your Form 1095-A, you should contact Covered CA or you can have a broker at no additional charge directly.

- The IRS does not issue and cannot provide that information to you.

- Do not file a Form 1040X, Amended U.S. Individual Income Tax Return. Once you respond to the letter, the IRS uses the information you provide to process your tax return.

- You can mail or fax your response. Be sure to include a copy of the letter with your response. Use the mailing address and fax number in the letter to respond.

- For more information about the health care law and the premium tax credit, visit IRS.gov/aca for more information. Tax Tip 2016-43

Understanding Your Letter 12C

Even More detail

Requesting information to reconcile Advance Payments of the Premium Tax Credit

We are sending you this letter because:

- Covered CA notified the IRS that they made advance payments of the premium tax credit to your or your family’s health insurance company to reduce your premium costs and

- you didn’t include the Form 8962, Premium Tax Credit, to reconcile the advance payments that were paid on your behalf when you filed your individual 2015 tax return.

When the Health Insurance Marketplace pays advance payments of the premium tax credit on your behalf, you must file Form 8962 to reconcile the advance payments to the actual amount of the Premium Tax Credit that you are eligible for based on your actual household income and family size. You must use the Form 1095-A, Health Insurance Marketplace Statement, sent to you from your Health Insurance Marketplace to complete Form 8962.

If you don’t reconcile:

If you don’t reconcile, you won’t be eligible for advance payments of the premium tax credit or cost-sharing reductions Enhanced Silver to help pay for your Covered CA health insurance coverage for the following calendar year.

What you need to do

- Read your letter carefully and respond timely.

- You must respond to the letter, even if you disagree with the information in the letter. If you disagree, send us a letter explaining what information you think is in error. If you didn’t purchase a health insurance policy from the Marketplace, you must let us know.

- Provide the information requested in the letter. This includes:

- a copy of your Form 1095A provided by your Marketplace,

- a completed Form 8962

- a copy of the corrected second page from your original return that shows the “Tax and Credits” and “Payments” sections. You must complete either the line for “excess advance premium tax credit repayment” (line 46, Form 1040, or line 29, Form 1040A) or the line for “net premium tax credit” (line 69, Form 1040, or line 45, Form 1040A).NOTE: If you originally filed a Form 1040EZ tax return, you must transfer the information from your Form 1040EZ to a Form 1040A and include it with your response. Form 1040EZ does not have the designated lines needed to carryforward amounts from a Form 8962.

- You should have received a Form 1095-A from your Marketplace. If you didn’t receive your Form 1095-A, log in to your HealthCare.gov or state Marketplace account or contact your agent or Covered CA directly. The IRS cannot answer questions about the information on your Form 1095-A, reissue missing/lost forms, or issue a corrected form.

- Do not file a Form 1040X, Amended U.S. Individual Income Tax Return. After we receive the requested information, we’ll use it to process your original tax return.

- If you’re entitled to a refund after reconciling your advance payments, we’ll send your refund about 6-8 weeks after we receive all of the necessary information.

How to respond

Your Letter 0012C provides a fax number, if you want to send the information by fax. If you prefer to mail your response, send the information to the address listed at the beginning of the letter. Also, include a copy of the letter with your response.

You may want to

- Visit www.irs.gov/aca for more information about filing a tax return with form 8962

- Call us at 1-866-682-7451, extension 568, if you have additional questions.

- irs.gov/understanding-your-letter-12c

- Fax # for responses Follow this link to taxact.com

#Report changes as they happen - within 30 days! 10 CCR California Code of Regulations § 6496

10 days for Medi Cal 22 CCR § 50185

Our webpage on ARPA & Unemployment Benefits - Silver 94

IRS Form 5152 - Report Changes

- Our VIDEO on how to report changes to Covered CA

- Lost your job? How to keep your Health Insurance. Shelter at Home VIDEO

- References & Links

- Here's instructions, job aid, reporting change in income

- Our webpage on the exact definition of MAGI Income

- If you've appointed us - instructions - as your broker, no extra charge, we can do it for you.

- Voter Registration

- Denial of benefits and possible criminal charges if you don't report changes in income!

- When Increasing Your Covered California Income Estimate Creates an Ethical Dilemma Insure Me Kevin.com

- Fudging Income?

- Western Poverty Law on reporting changes

- How to cancel coverage.

- agents and brokers who suspect or know a fraudulent application for insurance has been submitted to report the potential fraud to the California Department of Insurance Fraud Division. Read more >>> Wshblaw.com

- Visit our webpage on how to report changes

Tax Return Deadline

H & R Block advises to file a return and reconcile your credit by April 18, or request an extension so you have more time to file your taxes. An extension will give you until October 17 to file your return and reconcile any credit you received through Covered CA

Will I have to file a federal income tax return to get the premium tax credit?

Yes. For any tax year, if you have APTC in any amount or you do not have APTC but you plan to claim the premium tax credit, you must file a Form 8962, and attach it to your federal income tax return for that year. If you have any APTC, you will use Form 8962 to reconcile the difference between the APTC made on your behalf and the actual amount of the credit that you may claim on your return. This filing requirement applies whether or not you would otherwise be required to file a return.

If APTC is made on behalf of you or an individual in your family, and you do not file a tax return, you will not be eligible for APTC or cost-sharing reductions to help pay for your Marketplace health insurance coverage in future years. This means that you will be responsible for the full cost of your monthly premiums. IRS.gov

CFR 155.305 (f) (4)

Eligibility Standards

Compliance with filing requirement.

(i) Covered CA may not determine a tax filer eligible for advance payments of the premium tax credit if HHS notifies the Exchange as part of the process described in § 155.320(c)(3) that advance payments of the premium tax credit were made on behalf of the tax filer or either spouse if the tax filer is a married couple for a year for which tax data would be utilized for verification of household income and family size in accordance with § 155.320(c)(1)(i), and the tax filer or his or her spouse did not comply with the requirement to file an income tax return for that year as required by 26 U.S.C. 6011, 6012, and implementing regulations and reconcile the advance payments of the premium tax credit for that period.

(ii) Notwithstanding the requirement in paragraph (f)(4)(i) of this section, the Exchange may not deny eligibility for advance payments of the premium tax credit under paragraph (f)(4)(i) of this section unless direct notification is first sent to the tax filer, consistent with thestandards set forth in § 155.230, that his or her eligibility will be discontinued as a result of the tax filer‘s failure to comply with the requirement specified under paragraph (f)(4)(i) of this section.

FAQ’s

Eligibility for other health coverage MEC Minimum Essential Coverage, makes you #ineligible for subsidies

FAQ’s

- I have coverage with “Medi Cal?” as I’m taking care of my Mom under In Home Supportive Services IHSS. Can I keep my Covered CA subsidies APTC?

- It’s my understanding [I’m not a CPA or Attorney] that if one has coverage or is eligible for coverage with MEC Minimum Essential Coverage, then they wouldn’t qualify for subsidies. You are mandated to report MEC to Covered CA.

- Here’s a VIDEO to explain all the reasoning.

- It’s a stretch, maybe you could argue that LA Care is NOT MEC, based on the huge fine they just got! See LA Times article.

- It’s my understanding [I’m not a CPA or Attorney] that if one has coverage or is eligible for coverage with MEC Minimum Essential Coverage, then they wouldn’t qualify for subsidies. You are mandated to report MEC to Covered CA.

- What is Minimum Essential Coverage (MEC)?

- MEC includes the following.

- • Individual market coverage (including qualified health plans).

• Most coverage through government-sponsored programs (including Medicaid [Medi Cal] coverage, Medicare Part A or C, the Children’s Health Insurance Program (CHIP), certain benefits for veterans and their families, TRICARE, and health coverage for Peace Corps volunteers).

• Most types of employer-sponsored coverage.

• Grandfathered health plans.

• Other health coverage designated by the Department of Health and Human Services (HHS) as MEC. - MEC does not include coverage consisting solely of excepted benefits. Excepted benefits include vision and dental coverage not part of a comprehensive health insurance plan, workers’ compensation coverage, and coverage limited to a specified disease or

illness. - For more information on what is MEC, see our webpage or irs.gov/Individual-Shared-Responsibility-Provision

- Your MEC may be reported to you on Form 1095-A, Form 1095-B, or Form 1095-C.

- • Individual market coverage (including qualified health plans).

- MEC includes the following.

- MEC eligibility when you have Covered CA does not automatically discontinue APTC.

- If an individual in your tax family is enrolled in a qualified health plan for which APTC was made and the individual is or will soon become eligible for other MEC, you must report – notify the Marketplace – Covered CA about the other MEC and that the APTC for the individual’s coverage should be discontinued. If the Marketplace does not discontinue APTC for the first calendar month beginning after the month you notify the Marketplace, the individual is treated as eligible for the other MEC no earlier than the first day of the second calendar month beginning after the first month the individual may enroll in the other MEC.

- A different rule applies to Medicaid and CHIP eligibility, discussed later under Government-Sponsored Programs Publication 974 Page 9

- You could waive your coverage with PASC-SEIU Homecare Workers Health Care Plan, but that won’t help, the key word is eligibility.

- Our webpage on Minimum Essential Coverage

- For purposes of the PTC, a qualified health plan is a health insurance plan or policy purchased through a Marketplace [Covered CA] at the bronze, silver, gold, or platinum level. Throughout this publication 974, a qualified health plan is also referred to as a “policy.” Catastrophic health plans and stand-alone dental plans purchased through the Marketplace, and all plans purchased through the Small Business Health Options Program (SHOP), are not qualified health plans for purposes of the PTC. Therefore, they do not qualify a taxpayer to take the PTC Publication 974 Page 7

FAQ’s

How to Get an #exemption for Illness?

Here’s ways and reasons you might get penalties waived

- Fear of IRS. Taxpayer who had been laid off was overwhelmed by Schedule C instructions. As a result he just shut down and stopped filing for several years as the fear and anxiety mounted. He hired a CPA (Weston) to get his books in order. Once all returns were filed and taxes assessed, the IRS abated all penalties, because they agreed that the taxpayer had no malicious intent.

- Health issues. Prolonged illness made it difficult to concentrate, and short-term memory suffered.

- Mourning. Grief due to death of a close family member.

- Burglary. House was robbed and family computer with all records was stolen

- ONE FREE PASS: But before taxpayers go groveling with excuses, they have another, guilt-free option: the first-time penalty abatement waiver. Apparently the IRS has a warm and fuzzy side, because it believes that everyone is entitled to one mistake. So if you’ve got a clean record — you’ve filed (or filed a valid extension for) all required returns and are all paid up — you can qualify for the FTA waiver. Read more USA Today

- Reasonable Cause The key word here is “reasonable,” and it doesn’t include, “I forgot.” If you ask for a waiver for reasonable cause, you need to establish the facts for the issue you are having that keeps you from taking care of your taxes, and you need to produce documentation to back it up.

- Fire, natural disaster, casualty, or other serious disturbances count as reasonable cause. Plenty of people in the U.S. have been hit with extreme weather, devastating forest fires, and other issues over the past year or so. If your home or business is in a riot zone, you may receive a waiver since having your structure blocked off by police tape is probably considered a pretty serious disturbance. If you are unable to obtain your records, the IRS may grant a waiver.

- Death, serious illness, incapacitation, or unavoidable absence of you, the taxpayer, or a member of your immediate family is considered reasonable cause. It’s pretty cool of the government to acknowledge that dead people would have a tough time taking care of their taxes.

- Other reasons establishing you used all “ordinary business care and prudence” to meet your Federal tax obligations but just couldn’t do it. “I forgot” does not, unfortunately, count as reasonable care and prudence. Neither does lack of funds unless the reason for the lack meets reasonable cause criteria. Read more

- More specific information – citation for Covered CA?

- See the rules above on duty to Report Changes within 30 days

- If your MAGI is below 400% of the federal poverty level, there is a cap on the amount you must pay back, even if you received more in assistance than the amount of the cap. However, at higher income levels you’ll have to pay back the entire amount you received, which could be a lot. 8962 Instructions – Payback limitations

- you have until the due date of your return (April 15 plus extensions) to make a traditional IRA contribution and deduct the amount from your taxes. Likewise for contributions to a 401(k), SEP-IRA, SIMPLE Plan, or other tax qualified retirement plan for the self-employed. You also have until the due date of your return to make a contribution to a health savings account. Moreover, you have until the due date of your return to establish a traditional IRA or SEP-IRA account if you don’t already have it. Read more IRS Publication 590A * Nolo – what to do if you owe subsidy repayments?

-

CA Couple must pay back $13k in Advance Subsidies

- They said in their U.S. Tax Court filing that they had been told by Covered California marketplace representatives that they qualified for subsidy assisted insurance coverage.

- If they had known that was not the case, the Walkers said they would not have purchased insurance they did.

- The Tax Court took that into account, noting in the decision:

- “We note that it appears that Covered California may have incorrectly informed petitioners that they were eligible for the APTC for 2014. We are not unsympathetic to petitioners’ plight; however, we are bound by the statute as written and the accompanying regulations when consistent therewith. … The simple facts are that petitioners’ MAGI exceeded eligible levels and that they must repay the APTC payments made on their behalf.” Don’t mess with taxes.com

- Our child has moved out and is now doing his own taxes, but we got subsidies based on him being a dependent. How do we fix that?

- Check this out Quicken – Intuit.

https://hbex.coveredca.com/toolkit/downloads/Failure_to_Reconcile_Quick_Guide.pdf

Can we fax forms #1095 & #8962

if we didn’t get the letter

Fax the forms to where?

What letter?

You can get free tax advice here.

I meant,I already filed. They said a 12c was sent out, but I’m no longer at address, so I didn’t get it. ive already printed out 1095 and downloaded an 8962 form ,can I fax it without the irs letter

Tax Tip 2106-3 states that you need to send the letter. Since you don’t have it, sure try sending without the letter.

I was suffering from a Severe illness

What is the criteria to get an exemption from tax penalties and fix the issues now?

We will try and answer that question in our webpage above

Does Veteran’s Administration va disability get added in to AGI?

The IRS Website on VA Disability Benefits states that benefits do not count as income.

The definition of MAGI Income for Subsidies of taking line 37 of your 1040 and adding back in, Foreign Income and Tax Exempt Interest doesn’t mention VA benefits, so the answer would be no.