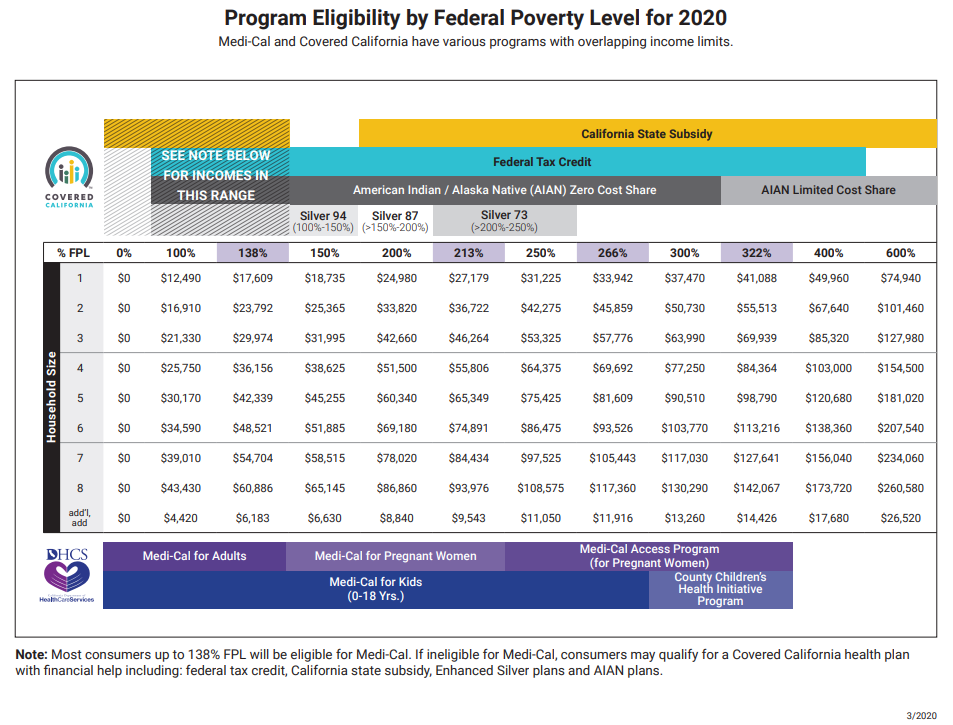

Covered CA & Medi Cal MAGI Income Chart

FPL Federal #PovertyLevel – Program, Eligibility & Subsidy Chart

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

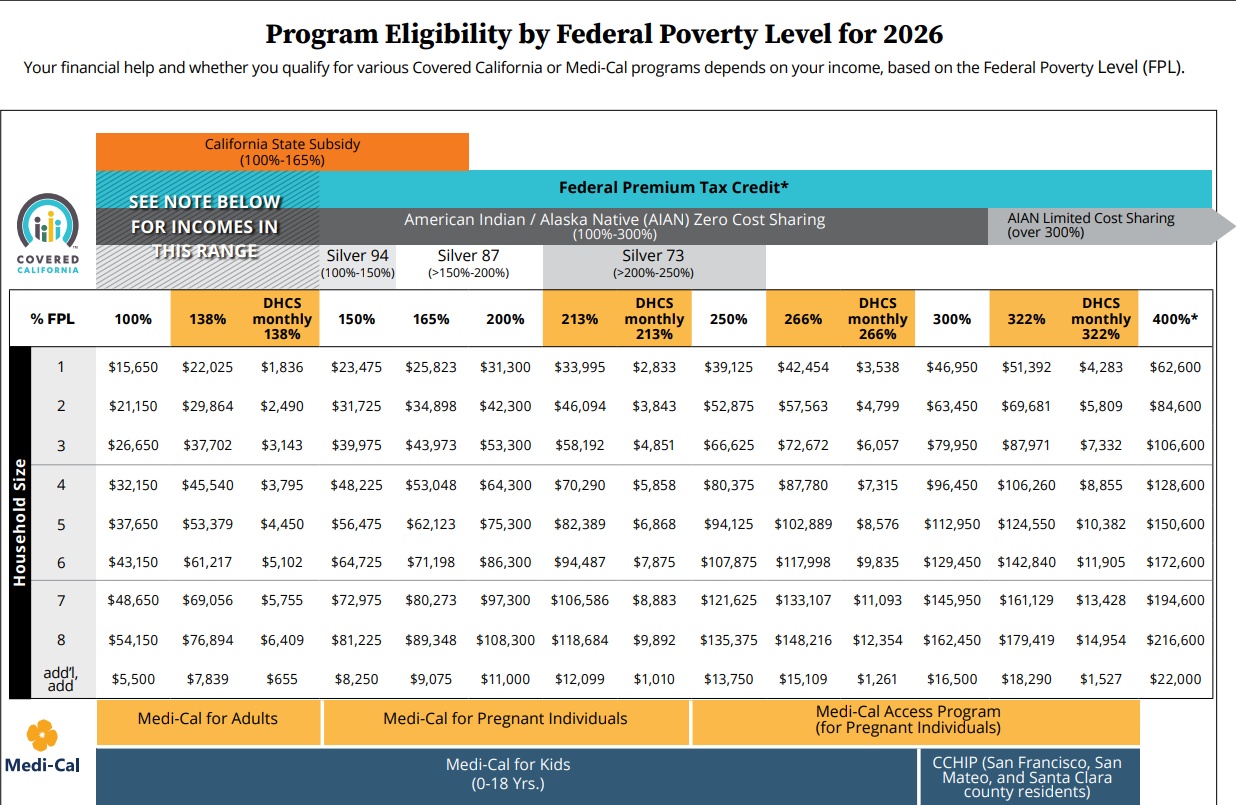

Covered California Income Chart 2026

Do you qualify for Medi-Cal, Covered California subsidies, or an Enhanced Silver plan?

- If you are trying to figure out whether your income is too low, too high, or just right for Covered California… this page will give you a quick starting point.

- The key: your eligibility is usually based on your projected yearly MAGI income and your household size.

- And you do not have to figure this out alone.

- I am a Covered California Certified Insurance Agent, and there is no extra charge for my help when you use me as your agent.

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

Quick Answer

- Here is the short version:

- Up to about 138% FPL → Medi-Cal

- 100% to 400% FPL → Covered California subsidies

- Up to 250% FPL → Enhanced Silver (lower deductibles and copays)

- 100% to 165% FPL → Extra California subsidy (2026)

- Important: These are general guidelines. Final eligibility depends on your full application, ZIP code, ages, and whether you qualify for Medi-Cal.

Before You Use the Chart

- Most people make one of two mistakes.

- Mistake #1: Using the wrong household size

- Mistake #2: Using last year’s income instead of this year’s estimate

- Covered California usually uses your projected yearly MAGI.

- If your estimate is off, your subsidy may be adjusted later when you file your taxes. IRS Form 8962

How to Use This Page

- Step 1: Determine your household size

- Step 2: Estimate your next years MAGI income

- Step 3: Compare your income to the chart

- Step 4: Identify whether you may fall into Medi-Cal, subsidy, or Enhanced Silver range

- Step 5: Confirm it with a real comparison, subsidy quote

Having Trouble Reading the Chart?

You are not alone.

If the chart looks small, blurry, or confusing on your phone, try clicking here for a cleaner pdf, skip the guesswork.

Just email me:

- Your ZIP code

- Your household size

- Your date of births

- Your estimated yearly MAGI income

Email: [email protected]

I will help you figure out your next step.

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

What Counts as Income (MAGI)?

MAGI usually starts with your Adjusted Gross Income.

Then, depending on your situation, you may add:

- Non-taxable Social Security

- Tax-exempt interest

- Foreign income

The important part: Covered California usually looks at your best estimate for the upcoming year, not just last year.

Frequently Asked Questions

- Is Covered California based on monthly or yearly income?

- Usually yearly projected income. Medi-Cal can work differently.

- What if my income is too low?

- You may qualify for Medi-Cal.

- What if my income is too high?

- You can still buy coverage, but without subsidies. If you want Silver, it may be less if we go direct and not through Covered CA

- What if my income changes?

- You should report it. Otherwise your subsidy may be too high or too low at tax time.

- Do I have to figure this out myself?

- No. I can help at no additional cost.

Need Help?

If you want help figuring out your eligibility, just reach out.

Steve Shorr

Covered California Certified Insurance Agent

Email: [email protected]

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

This is general information only and not tax or legal advice. Final eligibility is determined by official program rules and your application.

- Links & Resources

- Medi Cal Policy Changes in California: Who, What, When, and Why? Disability Rights 10/2025

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

Know your estimated income? See your 2026 plans and subsidy.

Use the income chart as a starting point, then compare the 2026 health plans available in your ZIP code and see an estimate of your Covered California subsidy.

See My 2026 Plans & Estimated Subsidy

No obligation. There is no extra charge for my help when you use me as your Covered California Certified Insurance Agent.

- Source - Covered CA

- When Your Tax Return Income Makes You Medi-Cal Eligible Insure Me Kevin.com

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

![]()

Covered CA Certified Insurance Agent

Get Covered CA quotes and Direct Quotes too

Review of the MAGI Medi-Cal income limits for adults and children for 2026. The higher income limits will be updated in the Covered California income table in February.

Child & Sibling Pages

- APTC Advance Premium Tax Credit – Subsidies ARPA

- MAGI Income Chart – Line 11 1040 Covered CA

- Negative MAGI – Medi Cal even if you are rich

- Report a Change – How & When – Especially Income Create Account

- Table of Contents -Income, Deductions & Expenses for MAGI no index

- Alimony – From a Divorce Settlement taxable

- Capital Gains, Sale of Home & Dividends

- Clergy – Housing Allowance? Covered CA MAGI Income

- Covered CA MAGI Retirement Income

- Educational Credits – Student Loan Interest

- Gambling Income & Losses – Other Income Line 21

- Medical or any Debt Cancellation Covered CA MAGI Income?

- Social Security Benefits MAGI Covered CA Income Subsidies