Schedule C Income and Covered California Subsidies

If you are self-employed, the net profit or loss reported on your IRS Schedule C can affect whether you qualify for Covered California financial assistance and how much help you receive.

Covered California explains that self-employed applicants should estimate their income and expenses for the year they will be covered. The calculation generally begins with your expected business NET income after ordinary business expenses—not simply the total amount customers pay you.

Quick Answer

- Gross business receipts are the amounts your business receives.

- Business expenses reduce your gross receipts when they are properly deductible.

- The result is your Schedule C net profit or loss, line 31.

- Your Schedule C result flows into your federal tax return and becomes part of your household income calculation.

- Covered California uses your estimated household Modified Adjusted Gross Income, or MAGI, to determine financial assistance.

- Your Schedule C income is important, but it may not be your household’s only income.

- Wages,

- retirement distributions,

- investment income,

- Capital Gains

- Social Security benefits and

- income received by other members of your tax household may also affect your MAGI.

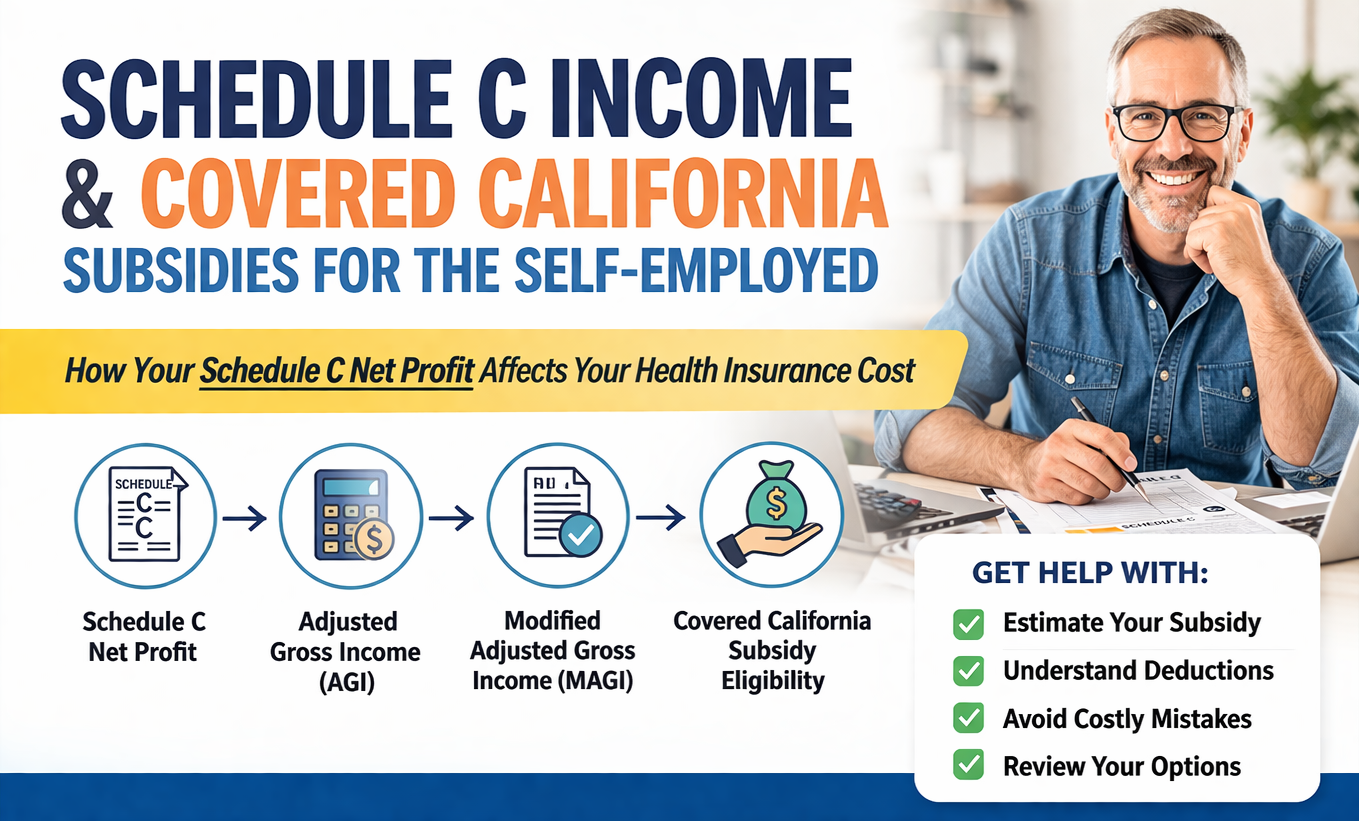

How Schedule C Income Flows to Covered California MAGI Income

For a sole proprietor, the basic flow generally looks like this:

- Gross business receipts

- Minus allowable business expenses

- Equals Schedule C net profit or loss

- Schedule C line 31 flows to Schedule 1, line 3

- Schedule 1 flows into your Form 1040

- Your tax-return income and applicable adjustments help determine Adjusted Gross Income

- Applicable MAGI rules are then used to determine eligibility for Covered California financial assistance

The amount on Schedule C is therefore an important starting point, but it is not automatically the final income figure entered in a Covered California application.

See our explanation of how to estimate MAGI income for Covered California.

Schedule C Income Example

Assume a self-employed person expects the following results for the coverage year:

- Gross business income: $72,000

- Allowable business expenses: $24,000

- Estimated Schedule C net profit: $48,000

The estimated $48,000 net profit becomes part of that person’s household income calculation. Other income and allowable adjustments may increase or decrease the final MAGI amount used to determine Covered California financial assistance.

This is why entering $72,000 of gross receipts instead of $48,000 of estimated net business income could produce a very different result. It is also why a business owner should not invent or exaggerate expenses merely to qualify for additional financial assistance.

The objective is a reasonable, good-faith projection based on the information available when you apply.

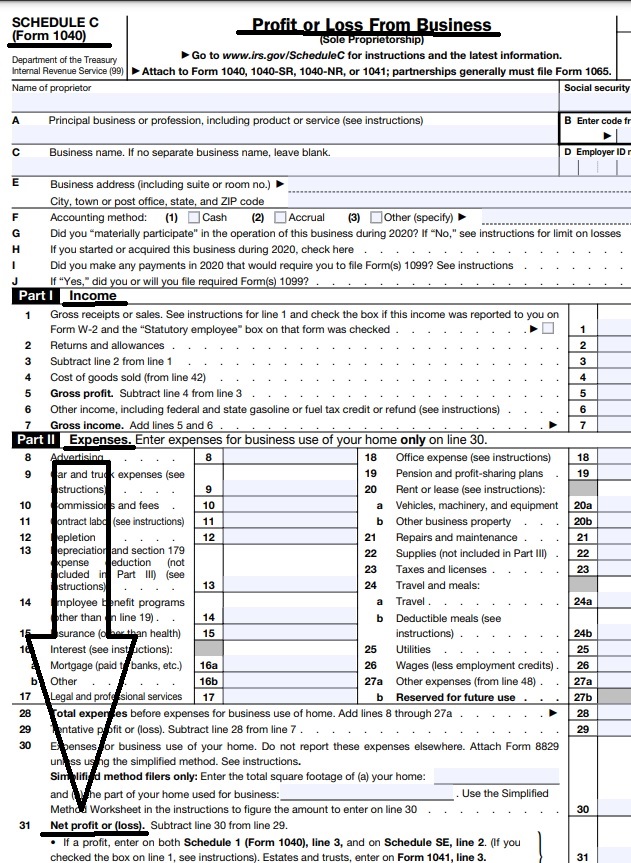

Schedule C 1040 Profit or Loss from Business

Income from your business get’s reported for Covered CA MAGI Income subsidies basically by what you put on your Schedule C, line 31 Schedule 1 and 1040 Form .

VIDEO Explanation Part 1 ** Part 2

Line 31 Net Profit or Loss from Schedule C goes on line 3 Schedule 1 of your 1040.

Use the Income You Reasonably Expect This Year

Covered California financial assistance is generally based on the income you expect during the year you will have coverage—not automatically the income shown on last year’s tax return.

Your prior tax return can be a useful starting point, but you should consider known or reasonably expected changes, including:

- New or lost customers.

- Changes in your rates or the number of hours you work.

- Seasonal increases or decreases in business.

- New business expenses or the end of prior expenses.

- A new W-2 job or the loss of employment.

- Retirement, Social Security or investment income.

- Income expected by a spouse or another member of your tax household.

When your circumstances materially change during the year, review our instructions for reporting an income or household change to Covered California.

Get Help Estimating Your Income and Comparing Plans

If you are self-employed and unsure what income figure to enter, I can help you review the health-insurance side of the calculation and compare the plans available in your California ZIP code.

I can help you:

- Review the income amount you are considering reporting to Covered California.

- Estimate available Covered California financial assistance.

- Compare premiums, provider networks, deductibles and benefits.

- Review Covered California plans and plans purchased directly from an insurance company.

- Update your Covered California account when your income or household information changes.

- Serve as your authorized Covered California insurance agent at no additional charge.

Compare Individual Health Plans and Subsidies

Independent California insurance agent. No obligation and no additional broker fee.

What Kind of Health Insurance Help Do You Need?

- Schedule C income can affect health insurance differently depending on whether you are

- buying coverage for yourself,

- group plans require a non-spousal w-2 employee,

- offering benefits to employees, or

- reviewing the tax treatment of health insurance premiums Section IRC 106

- Section 106 and Schedule C Guidance: You want to understand how health insurance premiums, business deductions and Covered California subsidies may work together.

Individual and Covered California Coverage

This choice may be appropriate when you are self-employed and buying health insurance for yourself or your family.

- Compare individual health plans available in your California ZIP code.

- Estimate Covered California premium assistance.

- Compare premiums, deductibles, benefits and provider networks.

- Review Covered California and direct-from-carrier options.

- Appoint Steve Shorr as your Covered California agent at no additional charge.

Compare Individual Plans and Subsidies

Independent California insurance agent. No obligation.

California Small-Group Health Coverage

This choice may be appropriate when your business has eligible W-2 employees and you are considering an employer-sponsored health plan.

- Compare California small-group health insurance carriers.

- Review employer contribution and employee participation requirements.

- Compare plan choices for owners, employees and eligible dependents.

- Review whether the business may qualify as a small employer group.

- Compare small-group coverage with individual Covered California options.

- You want the business to contribute toward employee health coverage and get the Section 106 deduction.

- You want employees to select from multiple available plans.

- You are comparing an employer group plan with individual Covered California coverage.

- You need help determining whether the business meets carrier participation and contribution requirements.

A business owner and spouse by themselves usually will not satisfy any carrier’s group-eligibility rules. Eligibility depends on the business structure, employees and applicable carrier requirements.

|

|

Schedule C Help by Topic

Schedule C connects to several other parts of the federal tax return. Select the subject that best matches your question:

- Schedule 1: Additional Income and Adjustments to Income — See how Schedule C income, the self-employed health insurance deduction and other adjustments flow through the tax return.

- Home Office Deduction — Review the general requirements and the simplified and regular methods for claiming business use of a home.

- Hobby or Business? — Learn why an activity must be examined carefully before income and expenses are reported as a business on Schedule C.

- 1099 Independent Contractor or W-2 Employee? — Receiving a Form 1099 does not necessarily settle whether a worker was properly classified.

- Estimate Covered California MAGI Income — Review household income, adjustments and other amounts that may affect eligibility.

- IRA and Retirement Contributions — Learn how qualifying retirement contributions may affect adjusted gross income.

Section 106 and Schedule C Guidance

This choice is for business owners who want to understand how health insurance premiums may fit into their business and Covered California income calculations.

- Review how Schedule C net profit flows into household income.

- Understand the difference between a Schedule C business expense and the self-employed health insurance deduction.

- Review how Covered California subsidies may interact with the self-employed health insurance deduction.

- Learn when Form 7206, Schedule 1 and Form 8962 may be involved.

- Review Section 106 information for businesses paying employee health insurance premiums.

- Find official IRS forms, publications and instructions.

Steve can explain the health insurance and enrollment side of these rules. Final tax deductions, tax-return preparation and individual tax advice should be reviewed with qualified tax software or a tax professional.

Covered California Subsidies and the Self-Employed Health Insurance Deduction

A person with net self-employment income may be eligible for the self-employed health insurance deduction calculated on IRS Form 7206. The allowable deduction is generally reported on Schedule 1, line 17, rather than as an ordinary insurance expense on Schedule C.

The calculation can become more complicated when the same taxpayer also qualifies for a Premium Tax Credit through Covered California:

- The self-employed health insurance deduction may reduce adjusted gross income.

- A change in adjusted gross income may change the Premium Tax Credit.

- The Premium Tax Credit affects the portion of the insurance premium paid by the taxpayer.

- The taxpayer-paid portion can affect the allowable self-employed health insurance deduction.

Because the two calculations can affect each other, IRS Publication 974 provides both an iterative calculation method and a simplified calculation method.

Most consumers will not calculate this repeatedly by hand. Tax-preparation software or a qualified tax professional will normally perform the calculation using information from Form 1095-A, Form 8962, Form 7206 and the taxpayer’s return.

See our page about Form 8962 and Premium Tax Credit reconciliation.

Steve Shorr Insurance provides health insurance information and enrollment assistance, but does not prepare tax returns or provide individual tax advice.

Common Schedule C and Covered California Mistakes

- Reporting gross receipts as net income. Business receipts and Schedule C net profit are not necessarily the same amount.

- Automatically copying last year’s income. Covered California requires an estimate for the current coverage year.

- Forgetting other household income. Schedule C income is only one part of the household MAGI calculation.

- Leaving income unchanged after the business improves. Underestimating income may result in having to repay some or all excess advance Premium Tax Credit when the tax return is filed.

- Failing to report a substantial business upturn or downturn. A lower reasonable income projection may increase financial assistance or affect Medi-Cal eligibility.

- Claiming personal expenses as business deductions. Only qualifying business expenses should reduce Schedule C income.

- Entering health insurance in the wrong place. The self-employed health insurance deduction is generally handled separately from ordinary Schedule C expenses. IRS Form 7206

- Assuming that receiving a Form 1099 proves independent-contractor status. The actual working relationship may still indicate that the person should have been treated as an employee.

Keep records supporting the amounts used in your estimate, and update Covered California when your income or household circumstances materially change.

1099 Contractor or Schedule C Business Owner?

These are related questions, but they are not the same question.

- The 1099 independent contractor versus employee page asks whether a person was properly classified as an independent contractor rather than a W-2 employee.

- This Schedule C page explains how someone who is legitimately self-employed reports business income and how that income may affect Covered California financial assistance.

A business cannot necessarily turn an employee into an independent contractor merely by issuing a Form 1099. Worker classification depends on the actual facts and applicable federal and California rules.

On the other hand, a person who truly operates an independent business will generally report business receipts and allowable expenses through Schedule C and may also owe self-employment tax.

Start with worker classification when that issue is uncertain. Start with Schedule C when you already know that you are properly self-employed.

Frequently Asked Questions

- Does Schedule C income count for Covered California?

- Yes. For many self-employed applicants, Schedule C net profit or loss is an important part of the household-income calculation. Other household income and applicable MAGI adjustments must also be considered.

- Does Covered California use gross business revenue?

- Self-employed income is generally considered after allowable business expenses. Gross receipts alone do not necessarily represent the amount used in the household-income calculation.

- Does Covered California use last year’s tax return?

- A prior tax return may be used as a starting point, but financial assistance is generally based on the income you reasonably expect during the coverage year.

- What happens if my business income changes?

- You should review the change and update Covered California when appropriate. Waiting until tax-filing time can result in receiving too much or too little advance financial assistance.

- Can business deductions increase my subsidy?

- Legitimate business deductions may reduce Schedule C net profit and therefore may affect household MAGI. Expenses should be claimed because they are allowable business expenses—not created merely to obtain additional health insurance assistance.

- Are health insurance premiums deducted on Schedule C?

- The self-employed health insurance deduction is generally calculated separately and reported as an adjustment to income on Schedule 1. Special coordination rules apply when the taxpayer also claims a Premium Tax Credit.

- Can Steve prepare my tax calculation?

- Steve can help explain how the income estimate affects Covered California plans and financial assistance. Tax-return preparation, the final deduction and Form 8962 reconciliation should be handled by the taxpayer, tax software or a qualified tax professional.

Official Forms and Helpful Resources

- IRS Schedule C — Profit or Loss From Business

- IRS Instructions for Schedule C

- IRS Schedule 1 — Additional Income and Adjustments to Income

- IRS Form 7206 — Self-Employed Health Insurance Deduction

- IRS Publication 974 — Premium Tax Credit

- Covered California Information for Self-Employed People

- Covered California Proof-of-Income Requirements

Our Related Pages

- Estimate Covered California MAGI Income

- Report an Income or Household Change

- Form 8962 Premium Tax Credit Reconciliation

- 1099 Independent Contractor Versus W-2 Employee

- Health Insurance Tax Deductions for Employers and Business Owners

- IRA Individual Retirement Accounts

- IRS Tax Guides for Small Business

Calculate your AGI & MAGI for Covered CA

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

How does retirement income – pension, IRA distributions count for MAGI Income and subsidy qualification?

Check our webpage on retirement distributions