Capital Gains Can Affect Covered California Subsidies

Selling stock, cryptocurrency, mutual funds, a rental property, or even a home can affect your Covered California MAGI income and premium subsidy eligibility. The important issue is not simply whether you received money, but how much of the gain becomes taxable income for the year.

Covered California subsidies are based on your projected annual Modified Adjusted Gross Income (MAGI). A large capital gain may temporarily increase your income enough to reduce or eliminate subsidy eligibility for that year.

If your income estimate is too low, you may receive excess Advance Premium Tax Credit and later reconcile it on IRS Form 8962. If your estimate is too high, you may miss out on subsidy assistance you could otherwise receive.

Common Situations Where Capital Gains Matter

You sold investments. Stock, mutual fund, ETF, and cryptocurrency gains may increase your taxable income and therefore your Covered California MAGI income.

You sold a rental property. Rental property sales may involve depreciation recapture, basis calculations, and taxable gains that can affect subsidy eligibility.

You sold your home. Some home-sale gains may qualify for exclusions, but taxable portions can still affect MAGI income calculations for Covered California.

You had a one-time income spike. A temporary gain during one tax year does not necessarily mean you will permanently lose subsidy eligibility in future years.

Do Not Guess Your Income Estimate

Many Covered California subsidy problems happen because income was estimated incorrectly. If you know about a major sale, gain, or taxable event, it is usually better to review your estimate before tax time.

Your tax preparer should determine the taxable amount, but once you understand the estimated income impact, I can help you compare health plans, estimate subsidy effects, and review Covered California reporting requirements.

Questions This Page Helps Answer

Click the links or just scroll down

Related MAGI and Subsidy Pages

Capital gains questions are often connected to other Covered California income and subsidy topics.

Already Have Covered California?

You can appoint Steve Shorr as your Covered California agent at no additional cost. Many people already have a Covered California account but still want help understanding:

- Capital gains and MAGI income

- Subsidy eligibility changes

- Form 8962 reconciliation

- Reporting income updates

- Medi-Cal vs Covered California

- Health plan comparisons

The easiest method is usually the secure Covered California text-message verification process. Covered California sends a temporary secret code to your phone, and once verified, Steve can assist with your account.

Covered CA MAGI Income – Capital Gains, etc.

![]()

Long Term Capital Gains & Modified AGI – Adjusted Gross Income

Covered California

Try turning your phone sideways to see the graphs & pdf's?

Calculate your Covered CA MAGI Income

Take #Line8b 11 or your projected IRS 1040 Adjusted Gross income for the upcoming year then

add line 2a, 6a & 8 (Foreign Income)

Chat GBT isn’t showing the numbers quite right, but you get the idea.

-

-

IMPORTANT!!!

The upcoming year – the future for what you tell Covered CA!

Sure, many people think it’s the past as Covered CA may ask for last years paperwork, but that’s BS! You might have to give back all the subsidies when you file Subsidy Reconciliation form #8962!

- Visit our MAIN webpage on MAGI Income

-

Almost everything you own and use for personal or investment purposes is a capital asset.

Examples include a

- home,

- personal-use items like household furnishings, and

- stocks or bonds held as investments.

When you sell a capital asset, the difference between the basis in the asset and the amount you sell it for is a capital gain or a capital loss.

Jump to section on:

- MAGI Countable Income

- §1031 Like Kind Exchange

VIDEO Introduction to this webpage

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

More Explanation & Schedule D

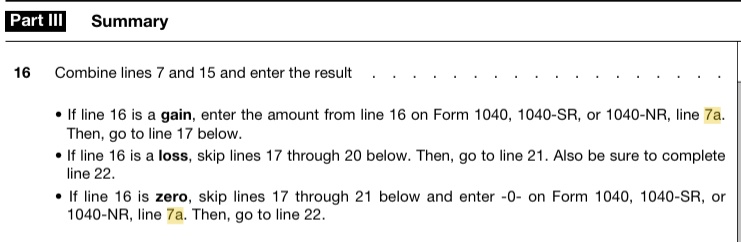

Capital Gains Summary

Capital gains and losses are classified as long-term or short-term, depending on how long you hold the property before you sell it. If you hold it more than one year, your capital gain or loss is long-term. If you hold it one year or less, your capital gain or loss is short-term. Learn More — IRS Publication 544, Sales and Other Dispositions of Assets.

If your capital losses exceed your capital gains, the excess is subtracted from other income on your tax return, up to an annual limit of $3,000 ($1,500 if you are married filing separately).

Capital gains and losses are reported on Schedule D, Capital Gains and Losses, and then transferred to line 13 of Form 1040. This year, the capital loss carryover worksheet has been removed from the Instructions for Schedule D to simplify tax preparation. However, there will be a worksheet in the 2004 Instructions to Schedule D to figure a capital loss carryover to 2004. See FAQ on Covered CA MAGI Income & Carry Over

If you have a taxable capital gain, you may be required to make estimated tax payments. See Publication 505, Tax Withholding and Estimated Tax, for information on estimated tax.

The top tax rate on net capital gain (i.e., net long-term capital gain reduced by any net short-term capital loss) has been reduced from 20% to 15% (and from 10% to 5% for gains that would otherwise be taxed at a regular rate of 10% or 15%) for property sold or otherwise disposed of after May 5, 2003 (and installment sale payments received after that date). The reduced rate applies for both the regular tax and the alternative minimum tax. The higher rates that apply to unrecaptured section 1250 gain, collectibles gain, and section 1202 gain have not changed.

Dividends paid by most domestic and foreign corporations after December 31, 2002, are eligible for the new maximum capital gains tax rate of 15% (5% in some cases). Qualified dividends are reported on line 9b of Forms 1040 or 1040A.

Additional information on capital gains and losses is available in Publications 550, Investment Income and Expenses, and 17, Your Federal Income Tax. You may download the publications from this Web site or order your free copies by calling 1-800-TAX-FORM (1-800-829-3676).

If you have investment or other types of financial losses Source IRS Tax Tip 2004-34, Feb. 19, 2004 should also check out these other IRS publications:

How much does Term Life Insurance cost to cover any loans and protect your family run?

Capital Gains and Losses

When you sell a capital asset, the sale normally results in a capital gain or loss. A capital asset includes most property you own for personal use or own as an investment.

Capital Assets.

Capital assets include property such as your home or car, as well as investment property, such as stocks and bonds.

Gains and Losses.

A capital gain or loss is the difference between your basis and the amount you get when you sell an asset. Your basis is usually what you paid for the asset.

Net Investment Income Tax.

You must include all capital gains in your income and you may be subject to the Net Investment Income Tax if your income is above certain amounts. The rate of this tax is 3.8 percent. For details, visit IRS.gov.

Deductible Losses.

You can deduct capital losses on the sale of investment property. You cannot deduct losses on the sale of property that you hold for personal use.

Limit on Losses.

If your capital losses are more than your capital gains, you can deduct the difference as a loss on your tax return. This loss is limited to $3,000 per year, or $1,500 if you are married and file a separate return.

Carryover Losses.

If your total net capital loss is more than the limit you can deduct, you can carry it over to next year’s tax return. See FAQ

Long and Short Term.

Capital gains and losses are treated as either long-term or short-term, depending on how long you held the property. If you held it for one year or less, the gain or loss is short-term.

Net Capital Gain.

If your long-term gains are more than your long-term losses, the difference between the two is a net long-term capital gain. If your net long-term capital gain is more than your net short-term capital loss, you have a net capital gain.

Tax Rate.

The tax rate on a net capital gain usually depends on your income. The maximum tax rate on a net capital gain is 20 percent. However, for most taxpayers a zero or 15 percent rate will apply. A 25 or 28 percent tax rate can also apply to certain types of net capital gain.

Forms to File.

- You often will need to file Form 8949, Sales and Other Dispositions of Capital Assets, with your federal tax return to report your gains and losses.

- Schedule D, Capital Gains and Losses

FAQ

Sale of Stock

- Question If I sell off some stock and realize about $15,000 in gain from it, and I am in the 0% long term capital gains bracket because of my total income and family size, do I still count this $15,000 toward my MAGI for Covered CA even though I will not be taxed on this by the IRS?

.- Answer I think the bottom line is, what # will you be putting on line 6 of your tax return? Note also that Form 8962 Premium Tax Credit Reconciliation asks for AGI Adjusted Gross Income and doesn’t say anything about line 6 capital gains not counting if you have low income. If your income is lower than $39,375 (or $78,750 for married couples), you’ll pay zero in capital gains taxes. If your income is between $39,376 to $434,550, you’ll pay 15 percent in capital gains taxes. And if your income is $434,551 or more, your capital gains tax rate is 20 percent. acorns.com/how-are-stocks-taxed/

- Be sure to check for updates for the current year.

- While Covered CA’s list of countable income above says to only count taxable portion I’m not sure if that includes what you are talking about as your saying your income is low enough to pay zero in taxes.

- Taxable Capital Gains probably means, after you subtract your costs – basis.

- MAGI income is line 8b – Adjusted Gross Income + other things, see above. It says nothing about an exclusion for taxable gains if you have low income. Will the capital gain take your income above the zero amount?

- 42 CFR 435.603(e) calculates income as defined by 26 U.S.C. § 36B. Any taxable capital gain on the sale of a home is included in AGI and must be entered on IRS Form 1040, line 13, capital gains (IRS Form 8949 and schedule D).

- I checked with my own CPA and he didn’t know the answer, but he did point out that just because income is not subject to tax, doesn’t mean it’s not MAGI Income for APTC subsidies.

- Covered CA nor their agents are allowed to give tax advice. See VITA for free advice

- What my CPA said 5 years ago about the calculation and reporting for subsidies.

- The cost of preparing the paperwork to get them properly qualified to receive the benefit would exceed anything I could reasonably charge them. The instructor, a fine fellow from Iowa, stated he unfortunately had to agree with me. So now tax preparers will have to decide whether to accept clients based on our health care system — just like doctors. Town Hall

- My CPA said that he could give an answer, if he put your numbers though the tax preparation process. That you should ask your own tax preparer. My CPA would need your tax return.

- Has anyone else worked with you to find an answer?

- How about appointing us as your broker Covered CA agent, no extra charge so that we can get paid for helping you.

- Long-term capital gains tax rates https://www.bankrate.com/investing/long-term-capital-gains-tax/

- Here’s the reply I got from Covered CA

- Household will need to speak to a tax professional to confirm what will be their taxable portion. Once they confirm the amount then that is what would need to be reported. If they have no taxable portion then they do not need to report any capital gains.

- A little more clarification from Covered CA

- The Covered CA application needs to match the tax filling information. Member will need to speak to a tax professional to confirm what income he will be reporting and that is the income that would go on the application.

- Let’s Try theIRS Interactive Tool for determining if your eligible for taking the premium tax credit.

- Answer I think the bottom line is, what # will you be putting on line 6 of your tax return? Note also that Form 8962 Premium Tax Credit Reconciliation asks for AGI Adjusted Gross Income and doesn’t say anything about line 6 capital gains not counting if you have low income. If your income is lower than $39,375 (or $78,750 for married couples), you’ll pay zero in capital gains taxes. If your income is between $39,376 to $434,550, you’ll pay 15 percent in capital gains taxes. And if your income is $434,551 or more, your capital gains tax rate is 20 percent. acorns.com/how-are-stocks-taxed/

Schedule D - Capital #Gains

- Visit our main webpage on capital gains

-

IRS Publication 550 investment & interest income & expense

#Interest Income 550

HTML PDF

- You tube VIDEO on Schedule D

- Schedule 1040 D Capital Gains & Losses

- Net Operating Losses Investopedia

- Sales and Disposition of Assets 544

- HTML

- Learn More ⇒IRS Tax Topic 409

- Report most sales and other capital transactions and calculate gain or loss on Form 8949 (PDF), Sales and Other Dispositions of Capital Assets, then summarize capital gains and deductible capital losses on

- Form 1040, Schedule D (PDF), Capital Gains and Losses.

- Publication 505, Tax Withholding and Estimated Tax

- Publication 550, Investment Income and Expenses

- 551 - Basis of Assets

- Publication 544, Sales and Other Dispositions of Assets

- Topics 701 and 703, and Publication 523, Selling Your Home.

- How much does Term Life Insurance to cover any loans and protect your family run?

- A “paper loss” – a drop in an investment’s value below its purchase price – does not qualify for the deduction. The loss must be realized through the capital asset’s sale or exchange.

- Publication 544, Sales and Other Dispositions of Assets (PDF 321K)

- Form 1040, U.S. Individual Income Tax Return (PDF 136K)

- Publication 505, Tax Withholding and Estimated Tax (PDF 367K)

- Publication 550, Investment Income and Expenses (PDF 516K)

- Publication 17, Your Federal Income Tax (PDF 2075K)

- Publication 564, 551 - Mutual Fund Distributions (PDF 178K)

- Publication 547, Casualties, Disasters, and Thefts (PDF 133K)

- Publication 527, Residential Rental Property (Including Rental of Vacation Homes)

- Schedule B (Form 1040), Interest and Ordinary Dividends General Information

- Publication 537 (2024), Installment Sales Sale of a business

- Settlements—Taxability Publication 4345

- irs.gov/tax-implications-of-settlements-and-judgments

- Legal Settlement - Taxable vs. Nontaxable Tax Act.com

- A Primer on the Taxability of Legal Settlement Proceeds nstp.org

#Covered CA Certified Agent

No extra charge for complementary assistance

Sale of Home

Capitol Gains on the sale of your #home

1st please be sure to read the information above on capital gains, so we don’t have to repeat the same information.

How Selling Your Home Can Impact Your Taxes

Usually, profits you earn are taxable. However, if you sell your home, you may not have to pay taxes on the money you gain. Here are ten tips to keep in mind if you sell your home this year.

- Exclusion of Gain. You may be able to exclude part or all of the gain from the sale of your home. This rule may apply if you meet the eligibility test. (Page 3 of Publication 523) Parts of the test involve your ownership and use of the home. You must have owned and used it as your main home for at least two out of the five years before the date of sale.

- Exceptions May Apply. There are exceptions to the ownership, use and other rules. One exception applies to persons with a disability. Another applies to certain members of the military. That rule includes certain government and Peace Corps workers. For more on this topic, see Publication 523, Selling Your Home.

- Exclusion Limit. The most gain you can exclude from tax is $250,000. This limit is $500,000 for joint returns. The Net Investment Income Tax will not apply to the excluded gain.

- May Not Need to Report Sale. If the gain is not taxable, you may not need to report the sale to the IRS on your tax return.

- When You Must Report the Sale. You must report the sale on your tax return if you can’t exclude all or part of the gain. You must report the sale if you choose not to claim the exclusion. That’s also true if you get Form 1099-S, Proceeds From Real Estate Transactions. If you report the sale, you should review the Questions and Answers on the Net Investment Income Tax on IRS.gov.

- Exclusion Frequency Limit. Generally, you may exclude the gain from the sale of your main home only once every two years. Some exceptions may apply to this rule.

- Only a Main Home Qualifies. If you own more than one home, you may only exclude the gain on the sale of your main home. Your main home usually is the home that you live in most of the time.

- First-time Homebuyer Credit. If you claimed the first-time homebuyer credit when you bought the home, special rules apply to the sale. For more on those rules, see Publication 523.

- Home Sold at a Loss. If you sell your main home at a loss, you can’t deduct the loss on your tax return.

- Report Your Address Change. After you sell your home and move, update your address with the IRS. using Form 8822, Change of Address and your friendly Insurance Agent (s).

- irs.gov/irs-tax-tips

Tips to Keep in Mind on Income Taxes and Selling a Home

Homeowners may qualify to exclude from their income all or part of any gain from the sale of their main home.

Below are tips to keep in mind when selling a home:

Ownership and Use. To claim the exclusion, the homeowner must meet the ownership and use tests. This means that during the five-year period ending on the date of the sale, the homeowner must have:

- Owned the home for at least two years

- Lived in the home as their main home for at least two years Gain. If there is a gain from the sale of their main home, the homeowner may be able to exclude up to $250,000 of the gain from income or $500,000 on a joint return in most cases. Homeowners who can exclude all of the gain do not need to report the sale on their tax return

Loss. A main home that sells for lower than purchased is not deductible.

Reporting a Sale. Reporting the sale of a home on a tax return is required if all or part of the gain is not excludable. A sale must also be reported on a tax return if the taxpayer chooses not to claim the exclusion or receives a Form 1099-S, Proceeds from Real Estate Transactions.

Possible Exceptions. There are exceptions to the rules above for persons with a disability, certain members of the military, intelligence community and Peace Corps workers, among others. More information is available in Publication 523, Selling Your Home.

Worksheets. Worksheets are included in Publication 523, Selling Your Home, to help you figure the:

- Adjusted basis of the home sold

- Gain (or loss) on the sale

- Gain that can be excluded

Items to Keep In Mind:

- Taxpayers who own more than one home can only exclude the gain on the sale of their main home. Taxes must paid on the gain from selling any other home.

- Taxpayers who used the first-time homebuyer credit to purchase their home have special rules that apply to the sale. For more on those rules, see Publication 523. Use the First Time Homebuyer Credit Account Look-up to get account information such as the total amount of your credit or your repayment amount.

- Work-related moving expenses might be deductible, see Publication 521, Moving Expenses.

- Taxpayers moving after the sale of their home should update their address with the IRS and the U.S. Postal Service by filing Form 8822, Change of Address.

- Taxpayers who purchased health coverage through the Health Insurance Marketplace should notify the Marketplace when moving out of the area covered by the current Marketplace plan.

Avoid scams. The IRS does not initiate contact using social media or text message. The first contact normally comes in the mail. Those wondering if they owe money to the IRS can view their tax account information on IRS.gov to find out.

Additional Resources:

- Tax Topic 701, Sale of Your Home

- Tax Topic 703, Basis of Assets

- Tax Topic 611, Repayment of the First-Time Homebuyer Credit

- IRS Tax Map, Selling Your Home

Home Energy Tax Credits Save You Money at Tax Time

Certain energy-efficient home improvements can cut your energy bills and save you money at tax time. Here are some key facts that you should know about home energy tax credits:

Non-Business Energy Property Credit

- Part of this credit is worth 10 percent of the cost of certain qualified energy-saving items you added to your main home last year. This may include items such as insulation, windows, doors and roofs.

- The other part of the credit is not a percentage of the cost. This part of the credit is for the actual cost of certain property. This may include items such as water heaters and heating and air conditioning systems. The credit amount for each type of property has a different dollar limit.

- This credit has a maximum lifetime limit of $500. You may only use $200 of this limit for windows.

- Your main home must be located in the U.S. to qualify for the credit.

- Be sure you have the written certification from the manufacturer that their product qualifies for this tax credit. They usually post it on their website or include it with the product’s packaging. You can rely on it to claim the credit, but do not attach it to your return. Keep it with your tax records.

- You must place qualifying improvements in service in your principal residence by Dec. 31, 2016.

Residential Energy Efficient Property Credit

- This tax credit is 30 percent of the cost of alternative energy equipment installed on or in your home.

- Qualified equipment includes solar hot water heaters, solar electric equipment, wind turbines and fuel cell property.

- Qualified wind turbine and fuel cell property must be placed into service by Dec. 31, 2016. Hot water heaters and solar electric equipment must be placed in to service by Dec. 31, 2021.

- The tax credit for qualified fuel cell property is limited to $500 for each one-half kilowatt of capacity. The amount for other qualified expenditures does not have a limit. If your credit is more than the tax you owe, you can carry forward the unused portion of this credit to next year’s tax return. • The home must be in the U.S. It does not have to be your main home, unless the alternative energy equipment is qualified fuel cell property.

Use Form 5695, Residential Energy Credits, to claim these credits. For more on this topic refer to the form’s instructions. You can get IRS forms on IRS.gov/forms anytime.

IRS Tax Tips provide valuable information throughout the year. IRS.gov offers tax help and info on various topics including common tax scams, taxpayer rights and more.

Moving Expenses Can Be Deductible

Did you move due to a change in your job or business location? If so, you may be able to deduct your moving expenses, except for meals. Here are the top tax tips for moving expenses.

In order to deduct moving expenses, your move must meet three requirements:

- The move must closely relate to the start of work. Generally, you can consider moving expenses within one year of the date you start work at a new job location. Additional rules apply to this requirement.

- Your move must meet the distance test. Your new main job location must be at least 50 miles farther from your old home than your previous job location. For example, if your old job was three miles from your old home, your new job must be at least 53 miles from your old home.

- You must meet the time test. After the move, you must work full-time at your new job for at least 39 weeks in the first year. If you’re self-employed, you must meet this test and work full-time for a total of at least 78 weeks during the first two years at your new job site. If your income tax return is due before you’ve met this test, you can still deduct moving expenses if you expect to meet it.

See Publication 521, Moving Expenses, for more information about these rules. It’s available on IRS.gov/forms anytime.

If you can claim this deduction, here are a few more tips from the IRS:

- Travel. You can deduct transportation and lodging expenses for yourself and household members while moving from your old home to your new home. You cannot deduct your travel meal costs.

- Household goods and utilities. You can deduct the cost of packing, crating and shipping your things. You may be able to include the cost of storing and insuring these items while in transit. You can deduct the cost of connecting or disconnecting utilities.

- Nondeductible expenses. You cannot deduct as moving expenses any part of the purchase price of your new home, the cost of selling a home or the cost of entering into or breaking a lease. See Publication 521 for a complete list.

- Reimbursed expenses. If your employer later pays you for the cost of a move that you deducted on your tax return, you may need to include the payment as income. You report any taxable amount on your tax return in the year you get the payment.

- Address Change. When you move, be sure to update your address with the IRS and the U.S. Post Office. To notify the IRS file Form 8822, Change of Address.

Premium Tax Credit – Changes in Circumstances.

If you or anyone in your family purchased health coverage through the Marketplace and had advance payments of the premium tax credit paid in advance to your insurance company to lower your monthly premiums, it is important to report life changes to the Marketplace when they happen. Moving to a new address is one change you should report. Other things to report include changes in your income, employment, family size, and gaining or losing eligibility for other coverage. Reporting life changes as they happen allows the Marketplace to adjust your advance credit payments. This will help you avoid a smaller refund or unexpectedly owing taxes when you file your tax return.

Additional IRS Resources:

- Can I Deduct My Moving Expenses? – Interactive Tax Assistant tool

- Tax Topic 455 – Moving Expenses

- Form 3903, Moving Expenses

Moving Expenses

Publication 521

IRS Publication 936

Home Mortgage Interest Deduction

Our webpage on Rental Property

#Selling your home – publication # 523

Publication 544 Sale & Disposition of Assets –

#Like Kind Exchanges 1031 Exchange are discussed starting on Page 11

All About 1031 Tax Deferred Exchanges – Real Estate Investment Tips VIDEO

- Visit our webpage on how to report changes

- Estimate your MAGI Income

FAQ’s

Capital Gains – #Sale of Home

- If the sale of a personal home (only one owned and for 10 years) generates a capital gain but the amount is under 250,000. (for a single person) which fills all requirements for the allowable exclusion … then even though that sale showed a profit, it would NOT be in included in income figures for MAGI …. correct? I’m selling a primary residence with a capital gain of approx $50,000.

********************Does that count as income for ACA tax credits?I will not owe federal tax on the gain.

I currently receive a tax credit [APTC Subsidy] and do not want to have to pay this back due to selling my primary residence.

*************************If I sell my home and have a capital gain (even after the Sec 121 exclusion), will that gain affect my Modified AGI? Will that gain count toward the income which could push my income high enough to require me to pay back my State Exchange subsidy?

- 1st off, how about appointing us as your broker so that we can get compensated for helping you? No extra charge.

- So, 2nd, let’s check the definition of MAGI.

- Line 11 Adjusted Gross Income, which would include Line 7 Capital Gains Schedule D

- So, if you are correct in that you meet all the requirements for the allowable exclusion, then the capital gain wouldn’t show in line 11 of your 1040 and wouldn’t be part of MAGI.

- IRS publication 523 on selling your home

- Do you meet the eligibility test on page 3 of IRS publication # 523?

- Review of the Eligibility Test. Generally, your home sale qualifies for the maximum exclusion, if all of the following conditions are true.

- You didn’t acquire the property through a like-kind exchange in the past 5 years.

- You aren’t subject to the expatriate tax.

- You owned the home for 2 of the last 5 years and lived in the home for 2 (1 if you become disabled) of the last 5 years leading up to the date of the sale.*

- For the 2 years before the date of the current sale, you didn’t sell another home on which you claimed the exclusion.

- The sale doesn’t involve the transfer of vacant land or a remainder interest.** IRS 523

- Reporting Gain or Loss on Your Home Sale

- Determine whether you need to report the gain from your home. You need to report the gain if ANY of the following is true.

- You have taxable gain on your home sale (or on the residential portion of your property if you made separate calculations for home and business) and don’t qualify to exclude all of the gain.

- You received a Form 1099-S. If so, you must report the sale on Form 8949 even if you have no taxable gain to report. See Instructions for Form 8949 and Instructions for Schedule D for more details.

- You wish to report your gain as a taxable gain even though some or all of it is eligible for exclusion. You may wish to do this if, for example, you plan to sell another main home within the next 2 years and are likely to receive a larger gain from the sale of that property. If you choose to report, rather than exclude, your taxable gain, you can undo that choice by filing an amended return within 3 years of the due date of your return for the year of the sale, excluding extensions.

- If NONE of the three bullets above is true, you don’t need to report your home sale on your tax return. IRS 523

- Form 8949 Sales & Dispositions of Capital Assets

- Gross income shall not include gain from the sale or exchange of property if, during the 5-year period ending on the date of the sale or exchange, such property has been owned and used by the taxpayer as the taxpayer’s principal residence for periods aggregating 2 years or more. 26 U.S. Code § 121

-

Covered CA doesn’t give tax advice nor allow agents to. Here’s what Covered CA suggests, unpaid volunteers VITA.

- Determine whether you need to report the gain from your home. You need to report the gain if ANY of the following is true.

- IRS publication 523 on selling your home

Income from a lawsuit

- Question: I’ve won a lawsuit and will soon receive a large award of money damages. Do I have to pay taxes on this money?

- Answer: The glow of victory may begin to dim after you get your attorney’s bill. As if that disappointment isn’t enough, we have more sobering news — the IRS may try to claim its share of the total. So postpone that trip to Cabo, and read on.

- According to the tax code, the only damages you can enjoy tax-free are those that compensate you for physical injury or physical sickness. (26 U.S.C. § 104(a).) So if this describes your case, you will probably keep the cash safely away from the grip of the IRS. Nolo.com

- References

Negative MAGI Income

FAQ's #Negative MAGI Income – Qualification for Medi Cal? Subsidies?”

- Question If your MAGI Income is negative, can you still qualify for Covered CA subsidies APTC even if you have some income, before you get to line 11 of your 1040?

. - Answer - NO! See the income chart. Your MAGI Income - AGI needs to be over 138% of FPL Federal Poverty Level

- CFR 1.36 B C how APTC Premium Assistance is calculated

- We also have no idea how long a tax loss will show up on line 11 adjusted gross income line of your 1040? See our webpage on Long Term Capital gains.

- No problem getting health coverage, you just won’t get subsidies. Click here to get quotes and enroll online.

- Sources

- Western Poverty Law and go over them with appropriate counsel.

- How to calculate MAGI Income

- Q & A on Intuit Site

- See IRS publication 536 Net Operating Loss

- Form 8962 Reconcile Premium Tax Credit You must enter your Modified Adjusted Gross Income MAGI

- IRS FAQ - What are the Income Limits

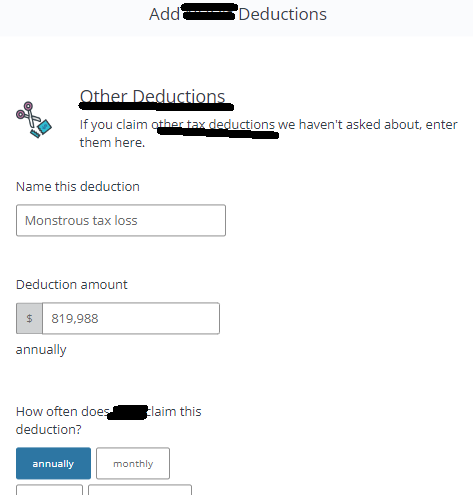

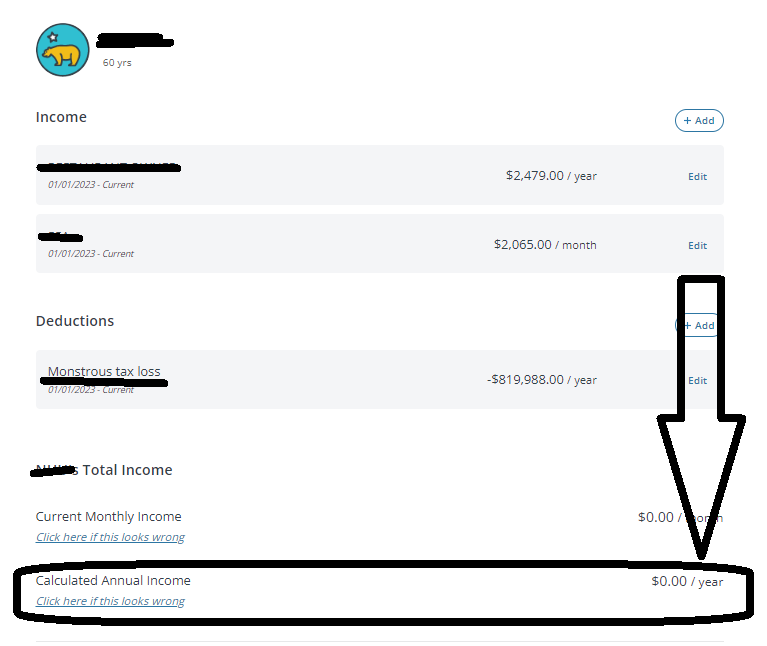

- Covered CA online application asks for Tax Deductions Email dated Wed 11/29/2023 8:54 AM Click on image to enlarge

-

- Question If your carry over net operating loss (from prior years) is allowed to be taken into account, is it part of the Federal Modified Adjusted Gross Income number ) or does California specifically require you to take it out of the equation?

- Answer Please see above on the definition of MAGI Income. I’m not aware of states having any authority over your Federal Tax return.

- Covered CA does not authorize agents to give tax advise. They suggest you get it from Volunteers at VITA.

- Note that the Income Chart says FEDERAL Poverty Level!

-

IRS Publication 536 Net Operating Loss

-

Do you really expect a clerk at Medi Cal to answer this kind of question?

-

We can help you with Covered CA when your income reaches 138% or more of FPL or if you go direct. Get quotes here.

- Answer Please see above on the definition of MAGI Income. I’m not aware of states having any authority over your Federal Tax return.

-

MAGI details from a Higher Up at Medi Cal

- Medi Cal agrees that MAGI can be negative and will educate the Counties...

-

Good morning,

For Modified Adjusted Gross Income (MAGI) Medi-Cal income and deductions policy, DHCS published All County Welfare Director’s Letter (ACWDL 21-04).

Page 2, Section 1 provides guidance on policy for countable income for MAGI program calculation, which is federal taxable income minus any allowable (post-tax) deductions under federal code. Page 3 links to an Income and Deductions chart tool to determine if a post-tax deduction can be used for MAGI-based Medi-Cal and for Covered California eligibility. Please note that the chart and the Covered California website deductions are post-tax deductions, and pre-tax deductions are already included when calculating AGI.

Tax loss is not considered an acceptable post-deduction for MAGI Medi-Cal or Covered California per federal code. The Centers for Medicare and Medicaid Services (CMS) has also published a document detailing MAGI rules with deduction information on page 7.

If the tax loss is considered as more of a capital gains/loss, or other loss such as real estate reported on Schedule E, then this amount should be entered into the system as an income with a negative (for example: -819,988). This will tell the system the income is actually at a loss and will reduce the income.

Thank you, and please let us know if you have any further questions.

Kathryn Floto, MPA | Health Program Specialist II

Medi-Cal Eligibility Division

California Department of Health Care Services

#VITA Volunteers Income Tax Assistance

get your taxes done Free

- Publication 3676 with more details on VITA

- Find a local VITA FREE Provider locator tool

- Turbo Tax -

- See more tax calculation links in the section on IRS Publication 974 Premium Tax Credit

Child & Sibling Pages

- Alimony – From a Divorce Settlement taxable

- Capital Gains, Sale of Home & Dividends

- Clergy – Housing Allowance? Covered CA MAGI Income

- Covered CA MAGI Retirement Income

- Educational Credits – Student Loan Interest

- Gambling Income & Losses – Other Income Line 21

- Medical or any Debt Cancellation Covered CA MAGI Income?

- Social Security Benefits MAGI Covered CA Income Subsidies

https://www.irs.gov/taxtopics/tc409