Section 125 Premium Only Plan (POP)

Pre-tax premium savings for employees. Payroll tax savings for employers.

Already have a plan? I can review whether it is set up correctly and whether you are actually capturing the available tax savings.

Email Steve for Section 125 Help

“Serving CA employers since 1981″

Before You Set This Up, Read This

A Section 125 Premium Only Plan can be simple, but only if it is set up correctly. Common problems include missing documents, payroll deductions not handled as true pre-tax deductions, and employers not understanding the compliance rules.

- No written plan document

- Payroll not truly set up pre-tax

- Employee elections not documented

- Compliance misunderstandings

Quick Compliance Checklist

Use this quick checklist to make sure your plan is not missing a step that could reduce the tax savings or create a compliance problem.

- Written POP plan document is in place

- Employee elections are documented and stored

- Payroll deductions are truly pre-tax

- Employer payroll tax savings are being applied

- The plan is reviewed annually

- Non-discrimination rules are satisfied

Start Here

I Want to Learn More

Learn how a Section 125 POP plan works, what documents are needed, and where the tax savings come from.

How a Section 125 POP Plan Can Help

- Employees may pay eligible health insurance premiums with pre-tax dollars

- Employers may reduce certain payroll taxes on those pre-tax amounts

- Employees may see more take-home pay

- The plan can be simple, but it still needs proper documentation and administration

A POP plan can be attractive to small employers because it is often simpler than more complicated cafeteria plan arrangements. But simple does not mean automatic. The paperwork and payroll setup still need to be done correctly.

Already Have a Plan? Here Is What to Check

- Do you have a current written plan document?

- Are employee elections documented?

- Are payroll deductions set up as pre-tax?

- Are employer payroll tax savings actually being captured?

- Has the setup been reviewed recently?

Need Help With a Section 125 POP Plan?

Whether you are starting from scratch or reviewing an existing setup, I can help you understand the moving parts and spot issues before they become expensive mistakes.

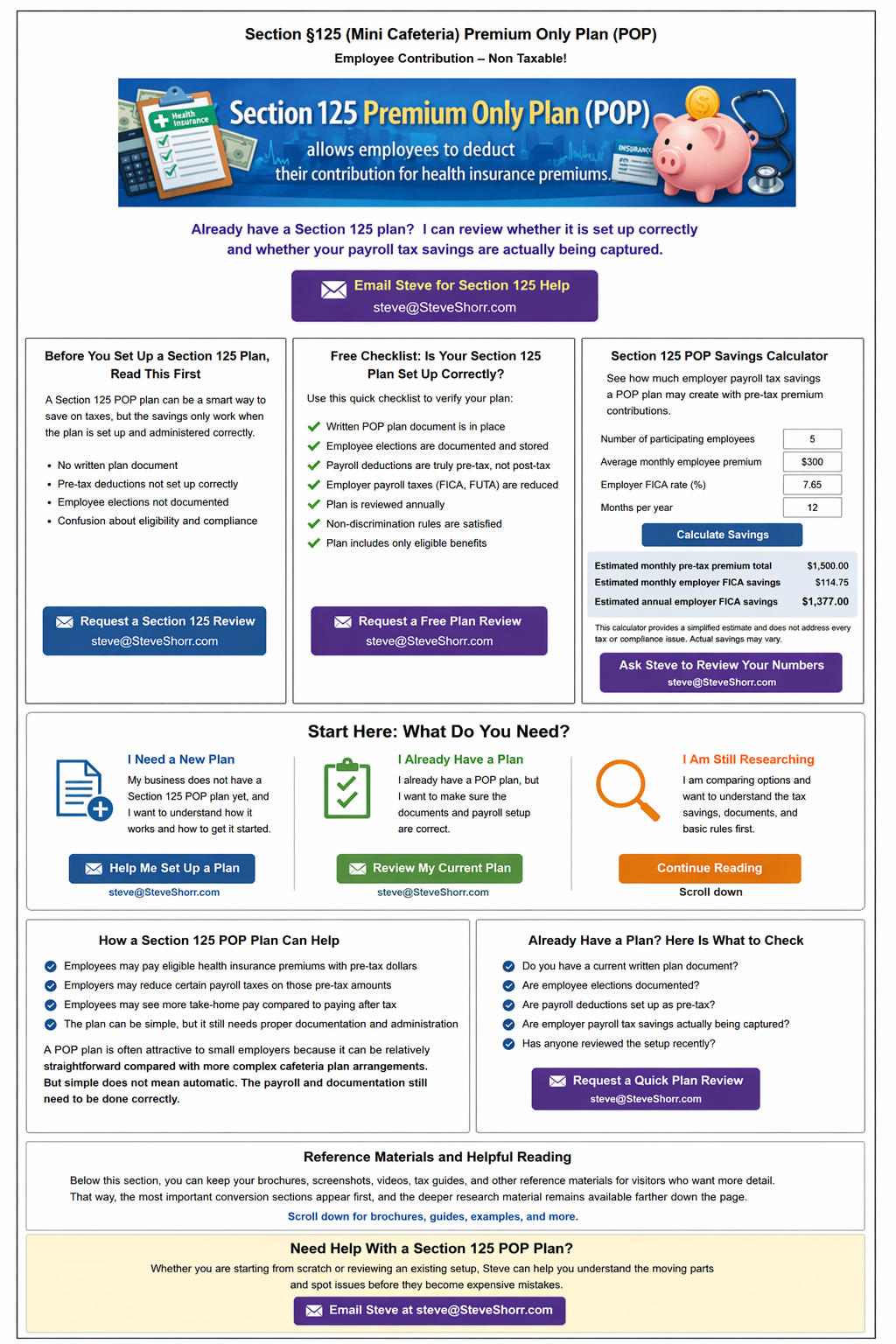

POP Savings Calculator

Estimate employer payroll tax savings from employee pre-tax premium contributions.

Estimated Savings

This simple estimate focuses on employer FICA savings and does not include possible employee income tax savings or other payroll-related effects.

More Detail & Brochures

POP Premium Only Cafeteria Plan

Introduction

Internal Revenue Code (IRC) Section §125

If your employee’s (and dependent’s) are contributing to your group health plan, their contribution-deduction from their paycheck, for your companies group medical premiums can be tax deductible with a Premium Only Plan – (POP 125) Mini Cafeteria Plan. Internal Revenue Code (IRC) §125 * html .

- Lower taxable AGI – Adjusted Gross Income on the employee’s Tax Return #1040

- PLUS, the POP will lower the employER’s payroll taxes such as

-

-

- FICA *

- FUTA, *

- Medicare Tax, *

- Income Tax Withholding US Code 26 C 21, Publication 535Publication 15-A * 26 U.S. Code § 125 – Cafeteria plans *

- State Disability Insurance (SDI) and

- possibly Worker’s Comp. About.com

-

The way it works, is that your company signs up for a POP plan, with an authorized administrator – vendor, see the links below and on the sides, it’s often the same Insurance Company that your medical coverage is through, but it doesn’t have to be. The cost of the 125 plan is in the neighborhood of $135/year. The administrator-vendor sends you a kit and you distribute the forms and have each employee enroll. The forms do not have to be filed with the government or even the administrator. You just keep them on file in your company records.

The premiums you as the employer is paying for Medical Coverage are already tax deductible for your company is not reportable as income to the employees under Internal Revenue Code §106. The POP plan, allows the portion of the premium that the employee is paying to also be tax deductible, above the line as it lowers Adjusted Gross Income.

See below and the brochures in the margins for more information. Email us for any questions. Send us or enter your census for Group Health Insurance Quotes

To start your companies POP Plan,

Just review the brochures, below, complete the application and return to us, [email protected] . The administrative process and fees (around $150/year) are nominal. It’s a WIN/WIN for both employER, employee and the dependents.

ACA/Obamacare HCR (Health Care Reform) IRC §125 (f) (3) narrows the definition of qualified benefit to exclude Individual Coverage offered through – Covered CA. Notice 2013-54 cuts off employer reimbursement outside of exchange too. Check with us, there might be updates on this.

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

- Paycheck Manager Calculators – Video Instructions @ 2.16 minutes

- irs.gov Withholding-Calculator (Annual Maintenance?)

- paycheckcity.com/calculator/salary

Just Enter your census or securely send us an excel spreadsheet or a list of employees and get instant proposals

for all these companies that we are Authorized Agents for in California

CORE HSA Health Savings Plan + Section §125 POP Cafeteria Plan

Plan Document Package

- Section 125 POP PDF Document by CoreDocuments.com VIDEO

- What is Section 125?

- Do I need a Section 125 Plan Document for my business?

- How well do free ‘fill-in’ plan document templates work?

- How much do employees save?

- Does a plan bring the employer any tax breaks?

- Who can participate?

- What is a “cafeteria plan”?

- Can I add a health FSA, dependent care FSA, or Health Savings Account?

- Do I have to start a Section 125 plan on January 1?

- What comes with a comprehensive plan document package?

- How do I set up a new Section 125 plan?

- When does a plan document need to be updated?

- How do I order a Core 125 Plan Document package customized for my benefit plan?

- Is there a video on Section 125 plans?

- Where can I find additional resources?

FAQ

- Question Is there any kind of non-discrimination testing in a POP ONLY plan?

. - Answer There are three different non-discrimination tests that must be passed relating to

- 1) eligibility,

- 2) actual contributions and benefits, and

- 3) key employee concentration.

- Employers will get an automatic pass of the three non-discrimination tests if they can satisfy one simple requirement.

- AKA Safe Harbor Rule

- If the ratio of non-highly compensated employees participating in the POP plan compared to the ratio of highly compensated participating in the POP plan is 50% or greater, the employer will be treated as passing all of the non-discrimination tests.

- AKA Safe Harbor Rule

- A key employee is generally an employee who is:

- An officer whose annual pay exceeds $170,000 ($165,000 for 2013); or

- An employee who is either of the following:

- o A 5 percent (or greater) owner of the business; or

- o A 1 percent (or greater) owner whose annual pay is greater than $150,000.

- We imagine testing to non be relevant, considering Insurance Company participation rules at generally 75%

- .

- Question Is this an above or below the line deduction? For Employees ? Employer?

. - Answer Above the line deductions are also known as “adjustments to income” Schedule 1 and are shown above line 11 Adjusted Gross Income of Form 1040.

- In the United States tax law, an above-the-line deduction is a deduction that the Internal Revenue Service allows a taxpayer to subtract from his or her gross income in arriving at “adjusted gross income” for the taxable year. These deductions are set forth in Internal Revenue Code Section 62. A taxpayer’s gross income minus his or her above-the-line deductions is equal to the adjusted gross income. Because these deductions are taken before adjusted gross income is calculated, they are designated “above-the-line.” Thus, those deductions allowed in computing “taxable income” under section 63 of the IRC are “below the line deductions” (thus, adjusted gross income represents “the line”). Above-the-line deductions may be more valuable to high income taxpayers than below-the-line deductions. wikipedia.org

- Income allotted to cafeteria plans is taken directly from an employee’s paycheck before taxes are taken out. These pre-tax contributions can save the employee hundreds—possibly even thousands—of dollars in income taxes and Social Security and Medicare taxes over the course of a year. Turbo Tax * PayCheck *

- A cafeteria plan, including an FSA and POP provides participants an opportunity to receive qualified benefits on a pre-tax basis. It is a written plan that allows your employees to choose between receiving cash or taxable benefits, instead of certain qualified benefits like health insurance for which the law provides an exclusion from wages.

- How to set up your POP Plan in Quickbooks Intuit.com

Tax Guides for Employers

EDD California 2025 Employers Guide #DE44

- Forms & Publications EDD

- FORMS REQUIRED TO GIVE NEW EMPLOYEES

- More workplace protections in 2022 New laws will shield employee health, safety and wages, but some ‘job killer’ bills were axed Los Angeles Times

- Social Security Forms

Brother – Sister – Sibling Side Pages Subpages

View our website with your Desktop or Tablet for the most information

Links & Reference Material

- ACA Requirement to report value of Health Coverage on W 2

- EDD Taxability of Employee Benefits DE 231 EB

- Our webpage on Management Carve Outs

Broker ONLY

Testimonials

Mr. Shorr,

I’m doing research on using 125 plans for employees who purchase individual insurance, and found your website very helpful, so I thought I would share the following legal analysis of mine, which might be helpful to others:

Mark A. Hall, J.D.

Professor of Law and Public Health

Wake Forest University faculty/profile