Can My Business Deduct Health Insurance Premiums?

IRC Section 106 is one of the main tax rules that makes employer health insurance valuable. In plain English, employer-provided accident or health plan coverage is generally not included in the employee’s gross income. 26 U.S. Code §106

For the employer, health insurance premiums may generally be treated as a business expense when the plan is properly set up. For the employee, employer-paid health coverage may be better than an ordinary taxable raise because the coverage is usually excluded from taxable income. Treasury Regulation §1.106-1

The real question is not just “Is health insurance deductible?” The better question is: What type of business do you have, and what is the correct way to set up the coverage?

| Your Situation | Start Here |

| You have employees and want a group health plan | Get instant employer group quotes |

| You are self-employed or file Schedule C | Schedule C health insurance deduction |

| You are a partner in a partnership | Partnership health insurance deduction |

| You own more than 2% of an S corporation | S corporation health insurance deduction |

| You want to pay for employees’ individual health insurance | Can my business pay for individual health insurance? |

Why This Matters for Small Employers

Health insurance can help a small employer recruit and keep good employees. In California, it can also help employees avoid being uninsured and potentially subject to California’s individual mandate penalty. If employees pay part of the premium, a Section 125 Premium Only Plan may allow their share to be paid pre-tax.

Do not simply reimburse employees for individual health insurance without checking the rules. Employer reimbursement of individual coverage can create ACA compliance problems unless it is done through the correct arrangement, such as a compliant HRA, ICHRA, QSEHRA, or taxable compensation approach. IRS HRA / employer payment plan guidance

What Should You Do Next?

The right answer depends on your business structure, number of employees, payroll setup, employee contribution strategy, and whether you are trying to cover owners, employees, spouses, dependents, or individual-market policies.

| Get Employer Group Quotes | Email Steve | Schedule Zoom |

Related Employer Health Insurance Tax Pages

- Schedule C – Self-Employment Income & Health Insurance

- Partnership Health Insurance Deduction

- S Corporation Health Insurance Deduction

- Can My Business Pay for Individual Health Insurance?

- Section 125 Premium Only Plan

- Section 105 HRA, QSEHRA & ICHRA

- Participation & Employer Contribution Requirements

- Who Qualifies as an Employer?

- Resources

Steve Shorr is a California licensed insurance agent, not a CPA, attorney, or tax advisor. This page is for general education. Please review your tax filing position with your CPA or tax professional.

Employer Health Coverage Tax #Deduction IRS Section §106

- Group Health Insurance under IRS Code Section §106 is tax deduction as a business expense for both the employer and is not income to the employee. It’s the biggest break there is in the Tax Code, even more so than Mortgage Interest.

- Providing Health Insurance is a GREAT way for EmployER’s to attract and retain better, stable, dependable workers. It’s also the law for large employers (over 50 lives) to meet the mandate and for the employees in CA to meet the California individual mandate.

- Internal Revenue Code Section §106

-

Except as otherwise provided in this section, gross income of an employee does not include employer-provided coverage under an accident or health plan.

-

- Internal Revenue Code Section §106

- This allows Employers to deduct Group Health Insurance Premiums for their employees including the owners and officers, as long as it’s a qualifying Group Health Insurance plan as a business expense.

- PLUS, Employees do not have to report employer paid premiums or the benefits in their gross income!

- If your employees are contributing to the premiums, their portion can also be tax deductible by using a Section §125 POP (Premium Only Plan) or a cafeteria plan.

- Employees whose employers do not currently provide Affordable Group Coverage, might qualify for Tax Credits Subsidies under ACA/Health Reform/Obamacare Section 45 R our webpage

- If the employees on their own want Medical Coverage – they can get Covered CA with us.

- Writing off medical expenses IRS Publication 502

- Get Employer Health Quotes

- Get Individual & Family Quotes

- LTC Insurance for Owners and Executives Journal of Accountancy.com *

Steve Shorr

Website Video #Introduction

Tax Publications & Guides

#Adjustments to Income - Schedule 1

#Schedule1 1040

- Part I Additional Income

- 2a Alimony received

- 3 Business income or (loss). Attach Schedule C

- Get Health Quote for your business

- 5 Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E

- 7 Unemployment compensation

- 8 Other income:

- a Net operating loss

- b Gambling income

- c Cancellation of debt

- d Foreign earned income exclusion from Form 2555

- e Taxable Health Savings Account distribution

- Part II Adjustments to Income

- 11 Educator expenses

- 13 Health savings account deduction. Attach Form 8889

- 15 Deductible part of self-employment tax. Attach Schedule SE

- Learn more about your Social Security Benefits

- 16 Self-employed SEP, SIMPLE, and qualified plans -

- 17 Self-employed health insurance deduction

- 19a Alimony paid

- 20 IRA Individual Retirement Account deduction

- 21 Student loan interest deduction

- Instant Business Health Insurance Proposals

IRS Publication 502 pdf * html

Medical & Dental #Expenses

-

- Aetna Listing of HSA allowable expense

- Topic no. 502, Medical and dental expenses IRS.Gov

- expenses exceed 7.5% of your adjusted gross income for the year may be deductiblexxx

- Medical Necessity? Our webpage

- The Tax Definition of "Medical Care:" Repository Law.com

- Medical expenses also include amounts paid for qualified long-term care services and limited amounts paid for any qualified long-term care insurance contract.

- Turbo Tax

- Schedule A 1040 Itemized Deductions

Health Coverage #Guide

Art Gallagher

Health Care Reform FAQ's

Understanding Health Reform

***********************************

Compliance #Assistance Guide from DOL.Gov Health Benefits under Federal Law

- Health Care Reform Explained Kaiser Foundation Cartoon VIDEO

- Choosing a Health Plan for Your Small Business VIDEO DOL.gov

- ACA Quick Reference Guide California Small Group Employers Revision 2020 Word & Brown

- kff.org/health-policy-101/

- Health Savings Accounts

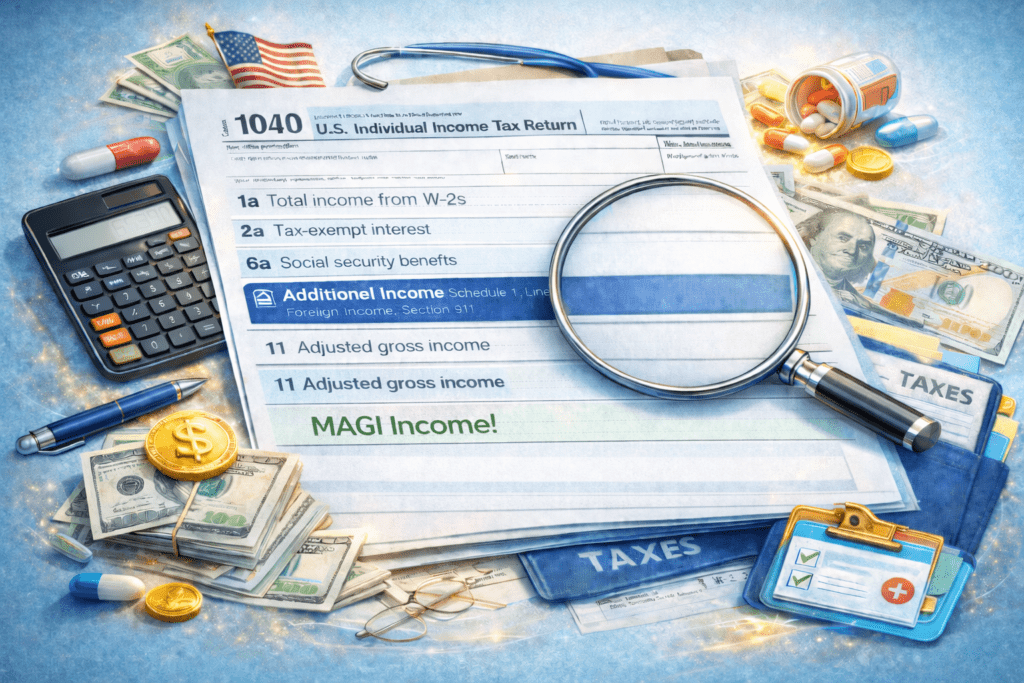

Calculate your Covered CA MAGI Income

take #Line8b 11 IRS 1040 Adjusted Gross income then add line 2a, 6a & 8 (Foreign Income)

Chat GBT isn’t showing the numbers quite right, but you get the idea.

-

-

IMPORTANT!!!

The upcoming year – the future for what you tell Covered CA!

Sure, many people think it’s the past as Covered CA may ask for last years paperwork, but that’s BS! You might have to give back all the subsidies when you file Subsidy Reconciliation form #8962!

- Visit our MAIN webpage on MAGI Income

-

References and Technical Links

- IRS More Info on Health Care Arrangements to not have a group plan but pay for employee individual plans. IRS Notice 2013-54

- IRS Publication — Business Expenses #535

- Tax Guide to Fringe Benefits — Publication 15-B

- Internal Revenue Code Title 26 USC

- ⋄Cornell’s Site ⋄

- GPO’s Site

- ⋄Formilab’s Site

- Rev. Rul. 82-196

- Rev. Rul. 67-360

- IRS Withholding Calculator

- CA Franchise Tax Board

- IRS Publication 502(all Medical Expenses) Insurance Premiums

- irs.gov/1040

- Paying into Social Security # 10022

- IRS 8885 Health Coverage Tax Credit A partner with net earnings from self-employment reported on line 15a of Schedule K–1 (Form 1065).

- IRC Section 162 (l)

A shareholder owning more than 2% of the outstanding stock of an S corporation with wages from the corporation reported on Form W–2. - IRS Publication #535 Business Expenses

- Schedule C Profit or Loss from Business 1040

- Instructions Schedule C

- Learn more — No more salary discrimination §2716,

- Tax Estimators

Can you pay an employee NOT to take the group health plan?

Opt out or waiver payment

- You must do a Full Section 125 Cafeteria Plan

- law.cornell.edu/125

- Our webpage on POP Premium only Section 125 Plans

- Reimbursing individual insurance coverage in the ACA era

-

Prior to the ACA, another popular benefit was simply reimbursing employees for individual insurance coverage that they purchased on their own. In most cases, these types of reimbursements could be made on a non-taxable basis. However, as part of the implementation of the ACA, these types of so called “employer payment plans” became largely prohibited, regardless of whether the reimbursements are taxable or non-taxable.

-

-

For the time being, the only ways for an employer to “pay for” individual insurance coverage obtained by an employee is to establish a “Qualified Small Employer Health Reimbursement Arrangement” (QSEHRA) or provide additional taxable compensation, whether though a simple salary increase or a monthly “bonus” or “stipend.” Regarding the additional compensation approach, the key is that the payment not be a “reimbursement”—i.e., not conditioned on proof that the employee indeed obtained his or her own individual insurance coverage. Rather, the increased compensation (regardless of the form) must be unconditional and taxable. Learn More Just Work.com *

Child & Sibling Pages

- Can My Business Pay For Individual Health Insurance?

- Partnership Health Insurance Deduction

- S Corporation Health Insurance Deduction

- Schedule C – Self-Employment Income – Hobby? Office in home?

- IRC §106 – 162 Health Insurance Deduction for Employers & Employees

- Level Funding

- Section §105 -HRA Health Reimbursement & ICHRA

- Section 125 – POP Plan Employee Contributions are Tax Deductible

Thank you Steve for all the information. I appreciate it.

We will move forward with deducting it [our health premiums] in taxes.

regards,

Maria