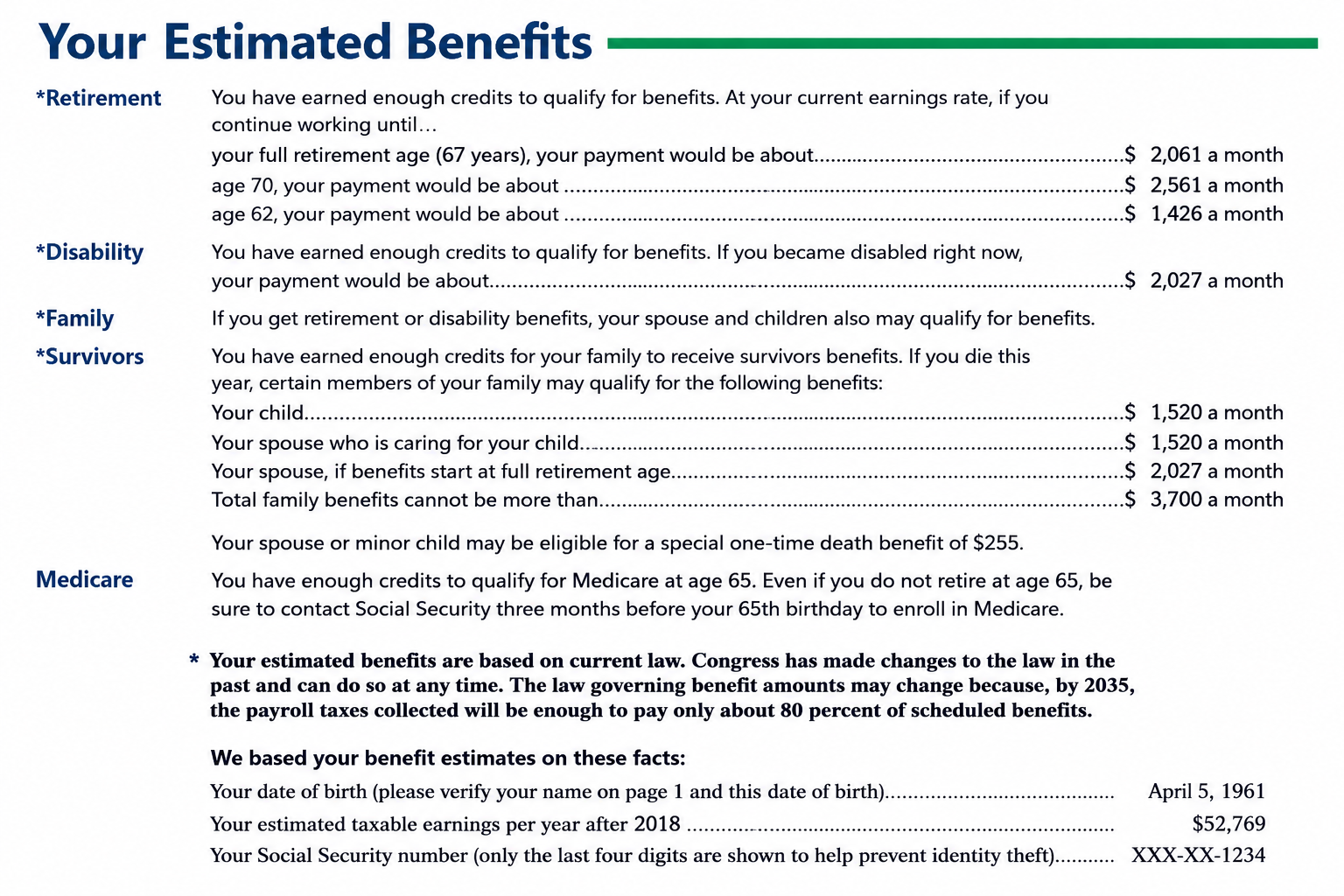

How Much Will Social Security Pay You?

Before deciding whether to start Social Security at age 62, wait until your Full Retirement Age, or delay until age 70, first get your own personalized estimate from Social Security.

Your estimate is based on your actual earnings record. It can show projected benefits at age 62, Full Retirement Age, and age 70.

How to Get Your Estimate

- Create or sign in to your my Social Security account.

- Or use this estimator on Social Security’s Website

- Review your earnings history for mistakes.

- Compare your estimated monthly benefit at age 62, Full Retirement Age, and age 70.

- Use those numbers before making a retirement claiming decision.

Create or Sign In to my Social Security

Why This Matters

Social Security is not one fixed number. Starting early usually means a lower monthly benefit. Waiting may increase the monthly amount. The right choice depends on your health, work plans, spouse, survivor benefit issues, taxes, Medicare timing, and other retirement income.

The first step is simple: know your own numbers before deciding when to file.

Introduction to Social Security Retirement & Family Benefits

along with ways to get even more at retirement

When you take your Social Security benefits, they will be paid out as long as you live including cost of living increases. Social Security & Medicare, with it's preventative benefits provide a base on which to you can build a financially secure retirement. Savings and Employer and Individual Retirement Plans - pensions add on to your Social Security, as Social Security was never meant that it would be enough to enjoy retirement.

Social Security is an “entitlement” program Merriam-Webster *. This means that since you and your employer paid Social Security taxes. You qualify for these benefits based on your work history (or your spouse or parent). The amount you get is based on these earnings. Fact Sheet *

View Social Security #Retirementa Benefits

Publication # 10035

- View Social Security Understanding the Benefits Publication # 10024 25 pages

- Self Employed & Social Security # 10022

- Retirement Check List # 10377

- Top Ten Facts about Social Security Center on Budget & Policy Priorities

- Sample Your Social Security Statement

- Provisions Affecting Cost-of-Living Adjustment SSA.gov

- Money Geek - Introduction

Child & Sibling Pages

- Best age to take Social Security Benefits? 62 or 70?

- How working affects Social Security Benefits

- Survivor Benefits Social Security

- Annuities & MAGI Income Taxation Exemption

- Business – Employer Sponsored Retirement Plans

- IRA – Individual Retirement Account Tax Deductible & Roth

- Social Security – Retirement Benefits

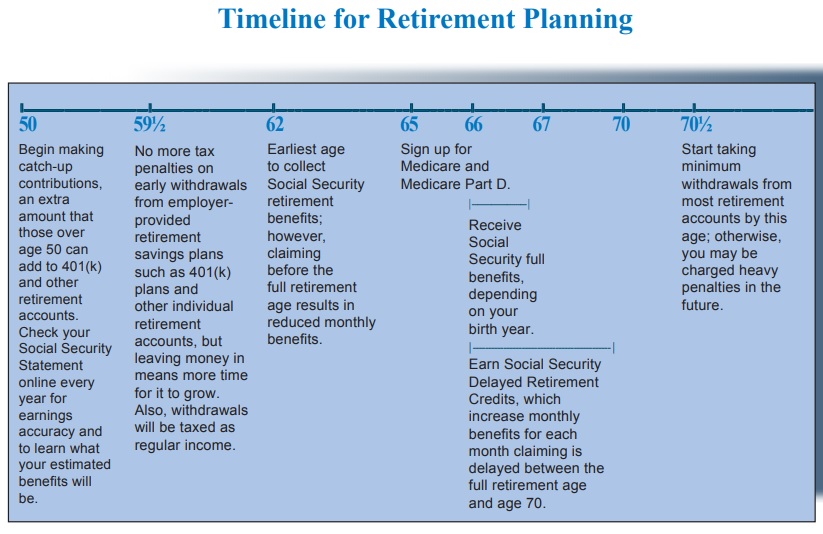

View #Time Line Retirement Planning

Department of Labor, Social Security & Medicare – View Retirement Toolkit 9 pages

Social Security’s Planning Tools

- Retirement Benefits Publication 10035

- Use the benefit calculators to test out different retirement ages or future earnings amounts,

- What happens if you work after you retire?, and

- How do certain types of earnings and pensions can affect your benefits?

Links & Resources

- Social Security’s Benefit Calculators

- Get your Personal Statement, Records and Retirement Estimate ONLINE

- Outline of Questions on Social Security

- Nolo Press Social Security, Medicare & Government Pensions – Get the most out of your retirement and Medical Benefits.

- Cost of Living Increase socialsecurity.gov/

- Spousal Benefits socialsecurity.gov/

- If your self employed – how to pay your premiums – taxes publication # 10022

- Social Security Educator Toolkit

- Department of Labor, Social Security & Medicare – Retirement Toolkit 9 pages

Social Security’s Website

FAQ’s

- Benefit Calculators

- Get your Personal Statement, Records and Retirement Estimate ONLINE

- Social Security also provides a lump-sum death payment of $255. Your spouse and young children can receive benefits equal to a $354,000 life insurance policy.

- Documents needed for retirement

- REQUEST FOR CORRECTION OF EARNINGS RECORD

Official IRS Tax Guides on Benefits

- View How work affects your Social Security Benefits Publication # 10069

- Tax Guide for Seniors # 554

-

Social Security Benefits Taxation #Pub915

-

Each January you will receive a Social Security Benefit Statement 1099 showing the amount of benefits you received in the previous year.

You can use this Benefit Statement when you complete your federal income tax return to find out if your benefits are subject to tax. See publication # 915 for details.

Resources & Links

- 2 page summary that comes with the policy

- Minimum Reserves required by California DOI

- Met Life Annuity Definitions – Glossary

- Annuity.com

- Annuities – CA Dept. of Insurance – What Seniors need to know

- IRS FAQ Required Minimum Distributions

- The wealth advisor.com new-irs-rule-lets-early-retirees-take-more-money-plans

- North American Life

- BROKER ONLY

Visit our webpages Extra ways to Save for Retirement & Medicare

Child & Sibling Pages

- Best age to take Social Security Benefits? 62 or 70?

- How working affects Social Security Benefits

- Survivor Benefits Social Security

- Annuities & MAGI Income Taxation Exemption

- Business – Employer Sponsored Retirement Plans

- IRA – Individual Retirement Account Tax Deductible & Roth

- Social Security – Retirement Benefits

Nolo's Guide to Social Security Disability

We do have a reference copy in our office

My #CPA ’s Newsletter on Retirement

RETIRING?

Not me – regardless of how one defines the word. This is a topic you cannot wait to focus on until you reach a late age. You have to plan for a long time.

There are four major concepts that override the issue of retiring. You may know these to some extent, but it’s important to refocus on these:

- The earlier you start putting away for your retirement and the more you contribute the better. That will give you the best flexibility when you get older.

- Here is something you know – people are living longer and are healthier for longer periods of time. Whatever you think is “sufficient” savings, think more.

- Because people are living longer and healthier lives, they are working longer. When I was young everything focused on the age of 65 when one retires. That is when Medicare and Social Security kicked in. People now think 65 is nothing and many people I know are working way past that age. My favorite writer said he was hanging it up when he was 87 years old. Broke my heart. He still writes a column occasionally. Like him others may be working a little less hard and taking more vacations. But if you can, there is good reason to continue working. As a professional, most of the people I know are more skilled and knowledgeable than they were 10-15 years ago. They are wiser and more experienced. They have irreplaceable skills. Many may want to keep busy and stretch out their retirement savings. Remember what happened to Bear Bryant, the famous Alabama football coach? They finally got him to retire and he was dead six months later. The bottom line is the longer you can postpone tapping your retirement assets, the better.

- Investment advisors focus on creating lots of savings. When thinking of retirement, you must likewise think of outflows. Most people think of not having a house payment as crucial. It may not make sense in some instances to pay off your house when you have a 3.5% loan, but you are earning 6% on your retirement investments. Minimizing other outflows are very important.

Delineating your income can be pretty easy. You have your social security and if you have a spouse theirs also. But then you must net that against what you must pay for your Medicare costs. Your outflows for Medicare B, D and your supplemental can add up and cut into your social security proceeds.

Next, there are the earnings from your pensions. Since most people outside of government are on defined contribution plans (401K, IRA, etc.), you must determine how much you can draw out every year and not run out of money.

That will begin to outline on what you have available for paying for your needs. It is of utmost importance that you analyze what you are going to give up of your current lifestyle and what you want to do when you retire. How often do you hear someone say when they retire they are going to do all that travelling they put off while they were working? Traveling costs lots of money even if you go on the cheap. A suggestion from a very experienced traveler — don’t wait until you retire to travel if that is what you want to do. The sooner you begin traveling the better. You will also learn more about what your reality is for travel during retirement.

Then there are the things you love to do. Baseball, theater, football, Hollywood Bowl concerts, basketball. These things cost a lot and may not fit into your budget if you have no revenue coming in from work. And there are always the big-ticket items such as helping your children or paying for your grandchildren’s private schooling. One person told us when we asked the name of the school his grandchild was attending (and he was funding) – it’s called “Dear Grandparents.”

Here are the major concerns beyond what has already been mentioned above:

- Home expenses – You may have paid off your home loan, but there are still significant outlays. People understand they must pay their home insurance and property taxes. What most people don’t plan for is the constant repairs. It seems like we don’t go a month without having to fix something. That is not considering remodeling or simply updating. Those expenditures can add up and may be out of the question unless you have significant resources set aside.

- Medical expenses – Even if you have all the elements of Medicare coverage including a supplemental plan, you can run into significant out-of-pocket expenses. Then there are dental expenses which can pile up for some people especially as they get older.

- Long-Term Care – The one insurance I tell people they should get is Long-Term Care. Almost everyone will have extensive care expenses near the end of life. We are fortunate to have a plan wherein we made payments for 10 years and are now paid up. Those plans are no longer available. You need to plan for this insurance or you will need to have large sums of money in your retirement plan.

- Loss in Asset Value – Many people experience the anxiety of thinking they are running out of money even if they are not. It is common. I had a client with $15 million in municipal bonds who acted as if she was going to be on the street the next day.

There will always be market fluctuations. It is easier to be patient with a downturn if you are still producing income. When the value of your retirement assets drop 15% because of a normal downturn in the market and you are retired — hysteria may set in.

If you figure you are going to have that happen twice during a retirement period of 20 years and plan for it early on, the anxiety is likely to be less. Most people think their portfolio is going to always be going up and that is not how markets work.

People often do not have a choice about retiring. They may work at a company or firm that has mandatory retirement even though that is less common today. Or there may be a medical condition causing retirement.

My suggestion is that you sit down and make two lists. One of what you believe your inflows are going to be (pensions, social security, rental income, etc.) and your outflows (realistic monthly expenses). Then take those to a professional who can analyze what you have included. The earlier you do this the better. If you are thinking of retiring in two years you may get an eye opening experience and decide to work two additional years. To pay a professional to analyze this instead of flying blind may be a money well spent.

You can then focus on what you are going to do when you are not working. A friend told me he has had friends retiring recently and everyone ninety days in says to him “I don’t know why I retired; I am bored to death.” That is another discussion entirely.

Please contact me Steve [email protected] or Bruce Bialosky with any questions you have about this or other matters.