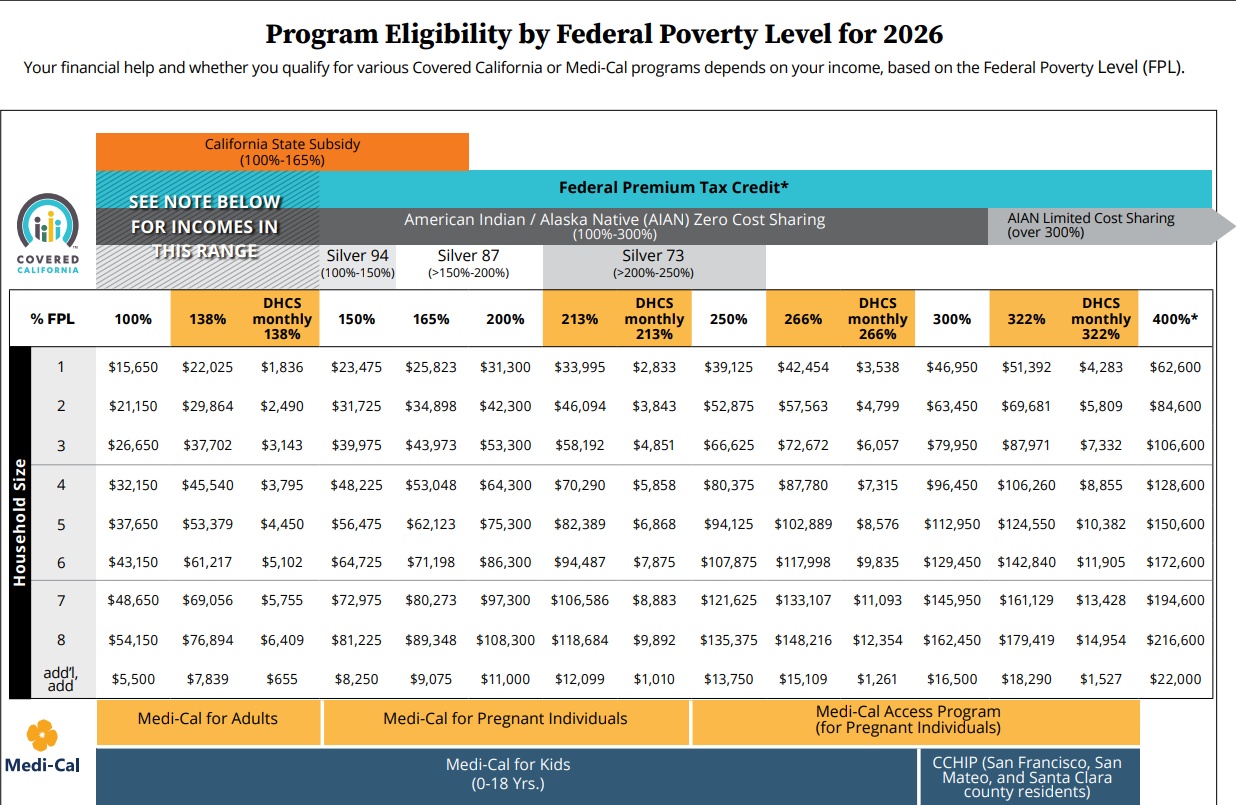

Does Social Security Count as Income for Covered California?

Yes. Covered California counts Social Security benefits in MAGI income.

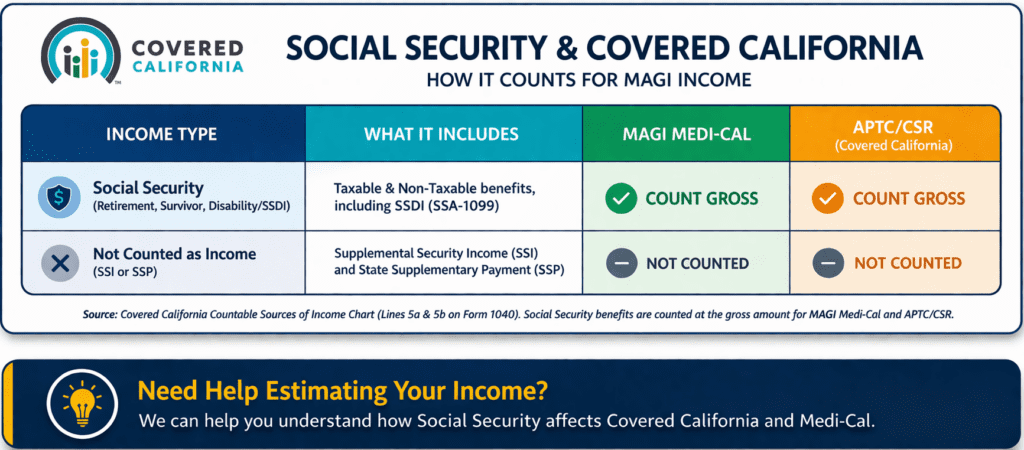

Social Security DOES count as income for Covered California and MAGI Medi-Cal.

Covered California’s official what counts as income chart shows Social Security benefits (taxable and non-taxable), including SSDI, are counted at the gross amount.

View Covered California What counts as Income Chart (official proof)

Important

Do not confuse Social Security with SSI (Supplemental Security Income).

SSI is not counted on the Covered California countable income chart and is not taxable.

Federal Taxes

Federal tax rules are different. Only part of Social Security may be taxable depending on total income.

Bottom Line

Do not assume tax rules = health coverage rules.

Covered California and Medi-Cal count Social Security income even when it is not taxed by California.

Need help estimating your income?

Use our AGI Calculator and then do the Add Ins

Covered CA (& Medi Cal) - Calculate - #Countable Sources of MAGI Income

Short Summary

Count Gross Social Security Income

Here’s where Covered CA asks about Social Security Income

See our FAQ’s about figuring out MAGI Income on your own and just entering the final number, rather then get caught in the quagmire of answering all the Covered CA questions where they try to help you, but I see too many people get sucked into the quick sand.

Insure Me Kevin.com – how to enter retirement income, so you don’t wind up on Medi Cal…

Calculate your Covered CA MAGI Income

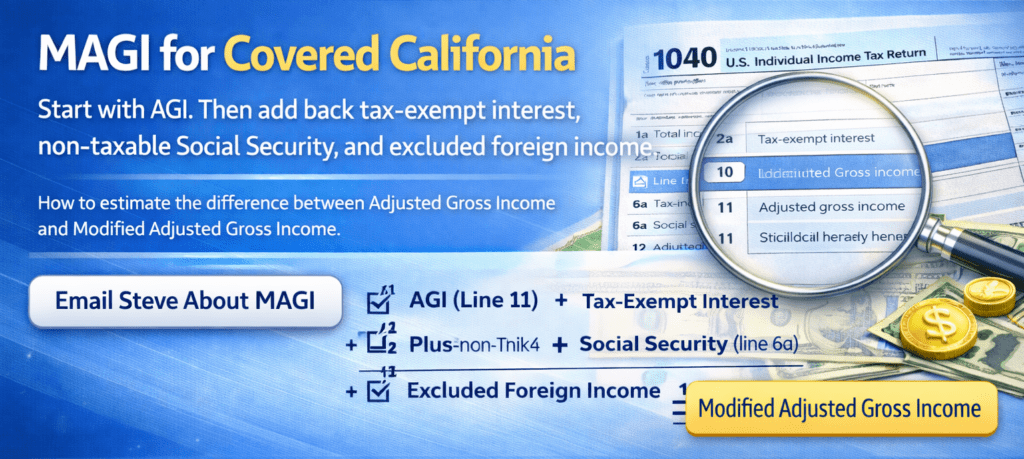

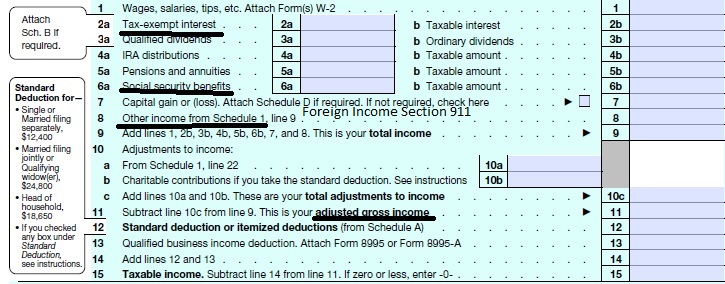

- Take #Line8b 11 or your projected IRS 1040 Adjusted Gross income for the upcoming year then add

- line 2a tax exempt interest

- 6a Social Security &

- 8 (Foreign Income)

-

-

-

IMPORTANT!!!

The upcoming year – the future for what you tell Covered CA!

Sure, many people think it’s the past as Covered CA may ask for last years paperwork, but that’s BS! You might have to give back all the subsidies when you file Subsidy Reconciliation form #8962!

- Visit our MAIN webpage on MAGI Income

-

-

Social security benefits taxation for MAGI Covered California or Medi-Cal?

How to #Estimate MAGI Income for Covered CA?

- From the AGI above, Line 11 Add back in any

- foreign income,

- Social Security benefits and

- interest that are tax-exempt.

- View our main webpage on estimating income

-

- Covered CA Job Aid Countable Sources of Income

- At the end of the year when you file taxes 1040 - you also file Premium Tax Credit Form 8962 to reconcile your estimate with the actual and either get money back or pay more.

- Report changes to income and household status within 30 days, to avoid surprises.

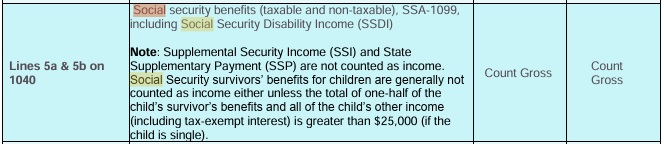

- In general, all your Social Security counts when calculating MAGI-Modified Adjusted Gross Income (AGI), that is the bottom line number on line 8b on your 1040 tax return then add back in the difference between line 5a & 5b of your 1040.

- Please note that neither I nor Covered CA give tax advice. Here’s where Covered CA’s advise caused someone to pay back $13k in subsidies.

- cnbc.com younger-retirees-tax

Summary of what is taxable MAGI (SSA.Gov)

Some people have to pay federal income taxes on their Social Security benefits. This usually happens only if you have other substantial income (such as wages, self-employment, interest, dividends and other taxable income that must be reported on your tax return) in addition to your benefits.

No one pays federal income tax on more than 85 percent of his or her Social Security benefits based on Internal Revenue Service (IRS) rules. If you:

- file a federal tax return as an “individual” and your combined income* is

- between $25,000 and $34,000, you may have to pay income tax on up to 50 percent of your benefits.

- more than $34,000, up to 85 percent of your benefits may be taxable.

- file a joint return, and you and your spouse have a combined income* that is

- between $32,000 and $44,000, you may have to pay income tax on up to 50 percent of your benefits

- more than $44,000, up to 85 percent of your benefits may be taxable.

- are married and file a separate tax return, you probably will pay taxes on your benefits.

*Note:

+ Nontaxable interest

+ ½ of your Social Security benefits

= Your “combined income“

Each January you will receive a Social Security Benefit Statement (Form SSA-1099) showing the amount of benefits you received in the previous year. You can use this Benefit Statement when you complete your federal income tax return to find out if your benefits are subject to tax.

- Request an SSA 1099 ♦

- SSA.Gov ♦

- Page 14 Retirement Guide Pub. 10035 ♦

- 26 US Code §86 Taxable Income Social Security

- Publication 915 Social Security and Equivalent Railroad Retirement Benefits

Your Social Security Benefits May be Taxable

If you receive Social Security benefits, you may have to pay federal income tax on part of your benefits. These IRS tips will help you determine if you need to pay taxes on your benefits.

- Form SSA-1099. If you received Social Security benefits in 2015, you should receive a Form SSA-1099, Social Security Benefit Statement, showing the amount of your benefits.

- Only Social Security. If Social Security was your only income in 2015, your benefits may not be taxable. You also may not need to file a federal income tax return. If you get income from other sources you may have to pay taxes on some of your benefits.

- Free File. Use IRS Free File to prepare and e-file your tax return for free. If you earned $62,000 or less, you can use brand-name software. The software does the math for you and helps avoid mistakes. If you earned more, you can use Free File Fillable Forms. This option uses electronic versions of IRS paper forms. It’s best for people who are used to doing their own taxes. Free File is available only by going to IRS.gov/freefile.

- Interactive Tax Assistant. You can get answers to your tax questions with this helpful tool and see if any of your benefits are taxable. Visit IRS.gov and use the Interactive Tax Assistant tool.

- Tax Formula. Here’s a quick way to find out if you must pay taxes on your Social Security benefits: Add one-half of your Social Security to all your other income, including tax-exempt interest. Then compare the total to the base amount for your filing status. If your total is more than the base amount, some of your benefits may be taxable.

- Base Amounts. The three base amounts are:

- $25,000 – if you are single, head of household, qualifying widow or widower with a dependent child or married filing separately and lived apart from your spouse for all of 2015

- $32,000 – if you are married filing jointly

- $0 – if you are married filing separately and lived with your spouse at any time during the year

Each and every taxpayer has a set of fundamental rights they should be aware of when dealing with the IRS. These are your Taxpayer Bill of Rights. Explore your rights and our obligations to protect them on IRS.gov.

See also publication 915 Social Security Benefits

Covered CA Subsidies – MAGI Income – Social Security?

Social Security Benefits

Taxation #Pub915

- Social Security & Covered CA MAGI Income

- How work affects your Social Security Benefits Publication # 10069

- Tax Guide for Seniors # 554

How & if Social Security Benefits are Taxed?

Annual Benefit Statements

Each January you will receive a Social Security Benefit Statement 1099 showing the amount of benefits you received in the previous year.

You can use this Benefit Statement when you complete your federal income tax return to find out if your benefits are subject to tax. See publication # 915 for details. It's on your right or if on smartphone, scroll down.

- VIDEO What is APTC Advance Premium Tax Credit

- Interactive Tax Assistant (ITA)

- Am I eligible to claim the Premium Tax Credit?

Tax #Estimators

- turbo tax.com - FREE for simple returns

- H & R Block

- E file.com

- Estimate the Subsidy for Health Insurance, benefits, premiums, etc.

- 8962 ONLINE Calculator

- Our webpage on 8962 Premium Tax Credit Reconciliation

- Tax Form Calculator.com

- e tax.com

- Marriage Higher or Lower Taxes?

ACA What You Need To Know #5187 (2020) is the most recent

- VITA - Volunteers to help you

- Publication 17 - Your Federal Income tax

- Health Savings Accounts HSA our webpage

Covered CA

Retirement Income MAGI Calculation

How much of your #Pensiona & Annuity Income goes on line 4a & 5a of IRS 1040 and

thus counts towards MAGI Income for Covered CA subsidies?

Covered CA (& Medi Cal) - Calculate - #Countable Sources of MAGI Income

Short Summary

Just the Count Taxable Portion of your Pension

Covered CA Cheat Sheet pdf

- Where does your retirement check go on your tax return?

- IRS Instructions Form # 1040

- IRS Publication #575 Pension & Annuity Income

![]()

![]()

![]()

![]()

![]()

- Reported on

#VITA Volunteers Income Tax Assistance

get your taxes done Free

- Publication 3676 with more details on VITA

- Our Webpage on VITA & Covered CA prohibition to give tax advice

- Find a local VITA FREE Provider locator tool

- Turbo Tax -

- See more tax calculation links in the section on IRS Publication 974 Premium Tax Credit

**********************************

Do Social Security #Survivor Benefits count for MAGI?

YES. See Covered CA countable income above.

Is child survivors benefits counted as income even if son is not listed as dependent?

Is your child a member of the household? Check out this Flow Chart

Why isn’t the child on the tax return?

Is your child eligible to be listed as a dependent under IRS Section 152?

Are Social Security survivor benefits for children considered taxable income?

Yes, under certain circumstances, although a child generally will not receive enough additional income to make the child’s Social Security benefits taxable.

- The taxability of benefits must be determined using the income of the person entitled to receive the benefits.

- If you and your child both receive benefits, you should calculate the taxability of your benefits separately from the taxability of your child’s benefits.

- The amount of income tax that your child must pay on that part of the benefits that belongs to your child depends on the child’s total amount of income and benefits for the taxable year.

To find our whether any of the child’s benefits may be taxable, compare the base amount for the child’s filing status with the total of:

- One-half of the child’s benefits.

- All the child’s other income, including tax-exempt interest.

If the child is single, the base amount for the child’s filing status is $25,000. If the child is married, see Publication 915, Social Security and Equivalent Railroad Retirement Benefits, for the applicable base amount and the other rules that apply to married individuals receiving Social Security benefits.

If the total of (1) one half of the child’s Social Security benefits and (2) all the child’s other income is greater than the base amount that applies to the child’s filing status, part of the child’s Social Security benefits may be taxable. You can figure the taxable amount of the benefits on a worksheet in the Instructions for Form 1040, Instructions for Form 1040A, or in Publication 915.

Additional Information:

- Tax Topic 423 – Social Security and Equivalent Railroad Retirement Benefits

- 42 CFR 435.603 for Medicaid – ….determining ongoing eligibility for beneficiaries determined eligible for Medicaid – Medi-Cal coverage … financial methodologies set forth in this section ….renewal of eligibility for such individual under § 435.916 of this part, whichever is later.

-

(2) Income of children and tax dependents.(i) The MAGI-based income of an individual who is included in the household of his or her natural, adopted or step parent and is not expected to be required to file a tax return under section 6012(a)(1) of the Code for the taxable year in which eligibility for Medicaid is being determined, is not included in household income whether or not the individual files a tax return.(ii) The MAGI-based income of a tax dependent described in paragraph (f)(2)(i) of this section who is not expected to be required to file a tax return under section 6012(a)(1) of the Code for the taxable year in which eligibility for Medicaid is being determined is not included in the household income of the taxpayer whether or not such tax dependent files a tax return.

-

- The Kinship Guardianship Assistance Payment Program pdf

Copied from IRS.gov

See our FAQ’s below