Find Your Doctor Before You Enroll

One of the most common questions we receive is whether a doctor, hospital, medical group, or specialist participates in a particular health plan. Provider networks can vary significantly between plans, and a lower premium often comes with a more limited network of doctors and hospitals.

Before enrolling, we strongly recommend verifying that your preferred doctors, specialists, hospitals, and medical groups participate in the network you are considering. Provider directories have improved over the years, but inaccuracies still occur.

- Provider Finder – All Companies

- Provider Finder Hub

- Appeals & Grievances

- Continuity of Care Protections

Major Hospitals & Medical Groups

- Cedars-Sinai Insurance Plans Accepted

- Optum / HealthCare Partners Insurance Accepted

- Providence Little Company of Mary Insurance Accepted

- THIPA (Torrance Memorial IPA) Insurance Accepted

- UCLA Health Insurance Accepted

- hoag.org accepted-health-plans

- memorial care.org health-insurance-plans

- Stanford Health Care Accepted Insurance Plans

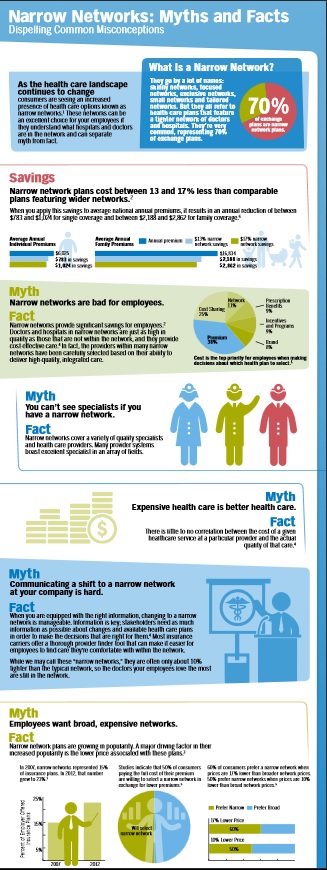

What Is A Narrow Network?

A narrow network is a health plan that contracts with a smaller group of physicians, hospitals, medical groups, and specialists. By concentrating patient volume among fewer providers, insurers are often able to negotiate lower reimbursement rates, helping keep premiums more affordable.

Narrow networks are common in both Covered California and Medicare Advantage plans. A lower premium does not necessarily mean poor quality care, but it may mean fewer provider choices and less flexibility if you wish to continue seeing a specific doctor.

Provider Directories Have Improved – But Problems Still Exist

California has spent years trying to improve provider directory accuracy. Covered California now utilizes the Integrated Healthcare Association’s Symphony provider directory platform to improve the accuracy of physician and facility listings across participating plans.

At the same time, California regulators continue to monitor so-called “ghost networks” where providers appear in directories but may not actually be accepting patients, may have moved locations, retired, or no longer participate in a particular network.

Medicare Advantage plans face similar challenges. CMS has begun integrating provider directory information into Medicare Plan Finder, but consumers should still independently verify provider participation whenever possible. 10 CCR § 2240 et seq.

What If The Directory Says My Doctor Participates?

Always verify network participation directly with the doctor’s office before enrolling.

- Confirm the exact office location.

- Confirm the physician is accepting new patients.

- Confirm the physician participates with your specific plan.

- Confirm the physician participates through the correct medical group or IPA.

- Save screenshots of directory results before enrolling.

Many network discrepancies occur because a physician participates at one office location but not another, or participates through one medical group but not another.

Covered California Mirror Plans

California law generally requires plans sold directly by insurance companies and plans sold through Covered California to mirror one another. This means the provider networks and benefits are generally the same whether purchased directly or through Covered California. The main exception involves certain Silver plan pricing differences related to enhanced subsidies and Silver Loading rules. (SB 639 *

Related Resources

- Hospital & Medical Group Directory

- Continuity of Care

- Doctor Not In Network?

- Appeals & Grievances

- Schedule a Zoom Consultation

Questions? Email [email protected]. Email is usually the fastest and easiest way to reach us.

Narrow Networks - Myths & Facts

Quotit - #Find Provider - ALL Companies

Get Quotes:

How to see MD list when using our quote engine

- Which plan is right for you?

- Covered CA Provider VIDEO - How to use it Steve's video

- Can’t Find A Doctor? Look at Low Star Rated Docs InsureMeKevin.com

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

#MAPD Medicare Advantage

Narrow Networks

Senate bill addresses inaccurate Medicare Advantage directories AMA.org

MAPD customers, are usually restricted to getting care from doctors and organizations included in their plan’s provider network. Most MAPD plans are HMOs, or health maintenance organizations, that have what are called narrow networks – relatively small groups of providers located only in the plan’s home market. PBS *

Health Care Dive.com Narrow Networks can cut costs

One can’t easily or accurately observe plan networks. The surest way to know if a physician is covered by a plan is to scrutinize the contracts between plans and providers. But these are closely held by the organizations, so are unavailable to researchers. Plans do publish provider directories, but there are no validated, comprehensive, historical archives of directories. Those that are available are not uniformly machine readable and are known to contain errors and omissions, such as listing physicians not in networks or failing to list those that are.

“secret shoppers” were able to schedule an appointment with a selected in-network provider in fewer than 30% of cases

on average, Medicare Advantage networks included 46% of all physicians in a county. There is considerable variation by specialty, with psychiatrists being least the likely to be included in plan networks (on average, a plan covered care by 23% of psychiatrists in a county) and ophthalmologists the most likely (59%). 16% of Medicare Advantage plans in 20 counties covered care at less than 30% of hospitals.) As for costs, the October study found that broader-network plans tend to charge higher premiums than narrow-network plans. Jama Network.com *

narrow network plans, insurers that offer these work with a smaller pool of doctors, hospitals, and treatment centers, who agree to a lower price for services with the expectation that they will get greater patient volume.

narrow networks are not strictly defined, the plans often have 25 percent or less of the physicians in the local area participating. The most restrictive plans have less than 10 percent of local doctors signed on.

One in 10 insured Americans say that within the past two years, they have been surprised to find that a doctor, lab, or facility that they thought was in their provider’s network actually wasn’t,

Identifying a plan as a narrow network can be very difficult.

Outdated directories are a problem

Even if you do everything you can to stay in network, sometimes needing out-of-network care is unavoidable, so you’ll want to take a close look at your out-of-network coverage. Some insurers will cover a portion of the cost of seeing a doctor who doesn’t take your insurance.

But an increasing number of plans have no out-of-network coverage at all. Consumer Reports *

KFF.org MAPD Robust Networks???

Urban.org Why MAPD plans have narrow networks

How much gets #paid to an out of network provider?

- How Your In-Network Health Coverage Can Vanish Before You Know It CA Health Line

. - Question? Scripps is no longer taking Medicare Advantage Plans, per their website. If you have a Medicare Advantage Plan MAPD PPO, will the PPO pay, how much and will Scripps take it?

. - Answer – Scripts states they take Medicare A & B on their website. The PPO pays the same benefits as A & B, thus it looks to me like the PPO will pay and Scripps should take it. Call to double check 800-727-4777. I’d email them, but I don’t find an email address. I don’t post or listen to hearsay. If you call, PLEASE get it in writing!

- See our webpage on Medicare Assignment.

- Sample MAPD Advantage EOC Evidence of Coverage.

- Email us about the Broker only explanation from UnitedHealthcare on options.