High Deductible Plan G vs Regular Plan G

High Deductible Plan G can be a good option for people who want the freedom of Original Medicare and a Medigap plan, but want a lower monthly premium. Medicare still pays first. You pay Medicare-covered deductibles, copayments, and coinsurance until the High Deductible Plan G deductible is met. For 2026, that deductible is $2,950.

Why Health Net Matters on This Page

At this time, Health Net is the company I represent that offers High Deductible Plan G. I also represent other companies that offer regular Plan G. That is why the quote engine is helpful: you can compare regular Plan G options and then look specifically at Health Net if you are considering High Deductible Plan G.

Who Should Consider High Deductible Plan G?

It may be a good fit if:

- You want lower monthly Medigap premiums.

- You can afford a larger medical bill if you have claims.

- You want to keep Original Medicare provider freedom.

- You rarely use doctors or specialists.

- You prefer saving premium dollars instead of paying more every month for regular Plan G.

It may not be the best fit if:

- A $2,950 deductible would create financial stress.

- You have frequent outpatient treatment.

- You prefer predictable monthly costs.

- You would rather pay a higher premium for regular Plan G and have less claim uncertainty.

Simple Break-Even Example

| Regular Plan G | High Deductible Plan G |

|---|---|

| Higher monthly premium | Lower monthly premium |

| Lower claim exposure after Medicare pays | You pay Medicare-approved cost-sharing until the deductible is met |

| Better for people who want predictable costs | Better for people who can handle risk and want premium savings |

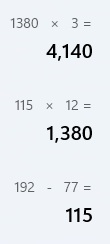

Example: if High Deductible Plan G saves you $120 per month compared with regular Plan G, that is $1,440 per year in premium savings. The question is whether the premium savings are worth taking on the possible deductible exposure.

Important: Medicare Still Pays First

High Deductible Plan G does not mean you pay the entire medical bill yourself. Medicare pays first. The deductible applies to Medicare-covered deductibles, copayments, and coinsurance that the Medigap policy would otherwise pay.

Frequently Asked Questions

Does High Deductible Plan G have a doctor network?

No. With Original Medicare and Medigap, you can generally use any doctor or hospital that accepts Medicare.

Is High Deductible Plan G the same as regular Plan G after the deductible?

Yes. After the high deductible is met, High Deductible Plan G works like regular Plan G for covered Medicare cost-sharing.

Can I compare regular Plan G and High Deductible Plan G?

Yes. Use the quote engine to compare regular Plan G options. For High Deductible Plan G, review the Health Net option.

Can I switch later?

Possibly, but you may need health underwriting unless you qualify for a guaranteed issue right, such as California’s Birthday Rule.

Is this better than Medicare Advantage?

It depends. Medicare Advantage may have lower or zero premiums, but usually has networks and copays. Medigap usually costs more in premium but gives more provider freedom with Original Medicare.

What To Send Me

If you are not sure whether regular Plan G or High Deductible Plan G makes more sense, email your ZIP code, date of birth, Medicare start date, and any current Medigap or Medicare Advantage plan. I can help you compare the premium savings against the deductible risk.

Official References

Explanation of the High Deductible $2,950

- View Official Health Net Brochure Medi Gap Outline of Coverage Page 45

- Our Health Net Medi Gap High G Webpage

- View Coverage Chart for Standard Plan G no extra deductible

- What's on this (our Medi Gap Guaranteed Acceptance) page?

- You Just turned 65

- MAPD Plan lowers benefits or raised premium

- If you are Under 65

- Birthday Rule

- On year Trial test of MAPD Plan

- Underwriting Holiday rules waived if you want to transfer from one Medi Gap plan to another

- Your Employer Coverage is ending

- Health Questions if you don't qualify for guaranteed issue

- You have a Change in Medi Cal Benefits

- Official Company Guaranteed Acceptance Guides

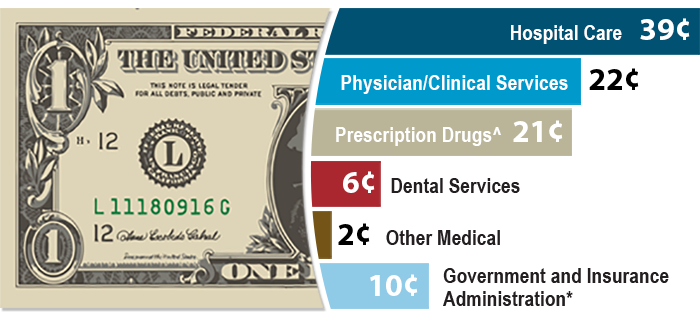

Medical Loss Ratio 80% Claims - 20% Operating Costs & Profit

So, why trade $$$ back and forth if you can afford not to?

Image from BCBS.com

Steve's Explanation of MLR Medical Loss Ratio

More Video's

- Kaiser Health News - Medical Loss Ratio video

- White House – YouTube Channel on Health Care Reform

- Tom Petersen Insurance 101 History of Lloyds to present EXCELLENT!!!

- Our Webpage on MLR & Actuarial Value

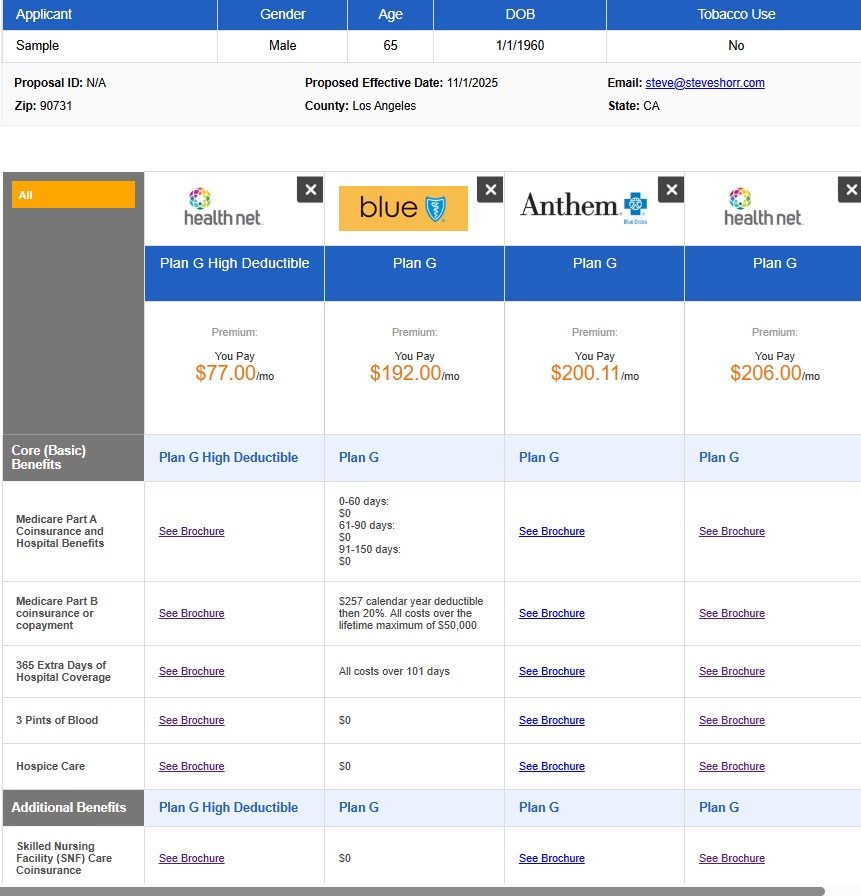

Get instant comparisons for Medi Gap Supplement Plans

Plan G vs Plan G High Deductible

Sample premium comparison

Get more information & Details

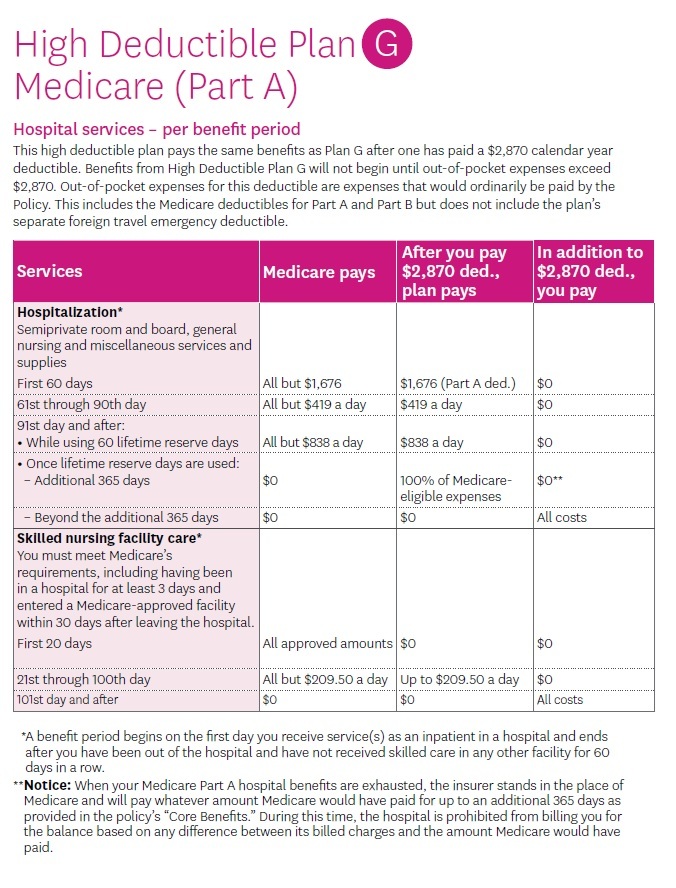

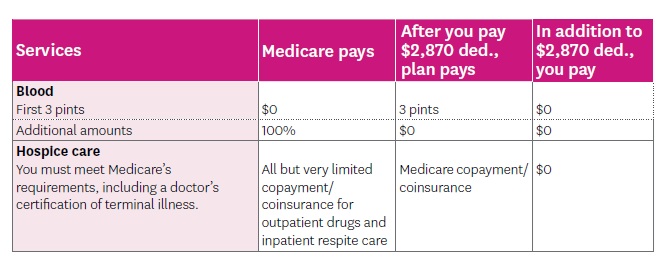

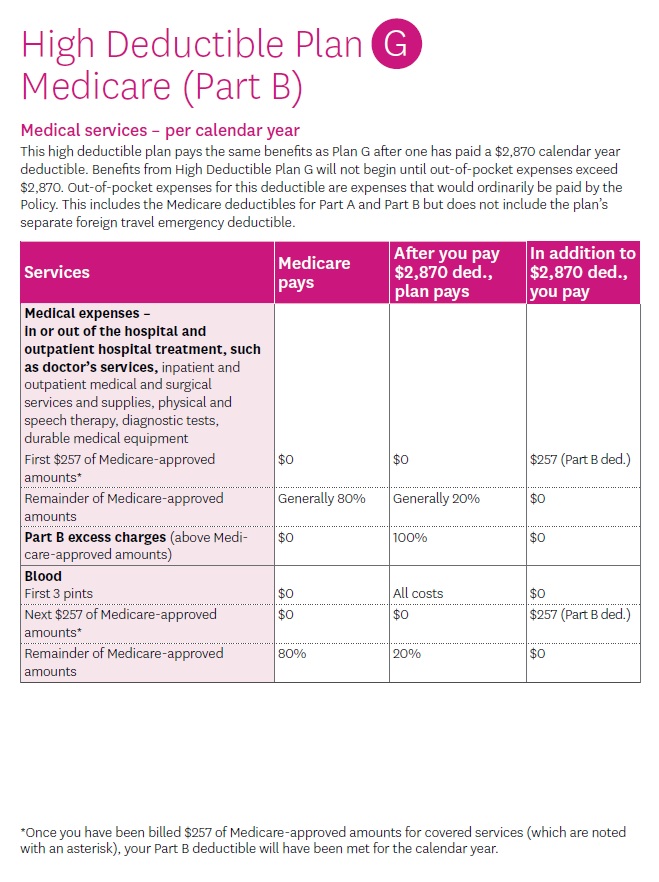

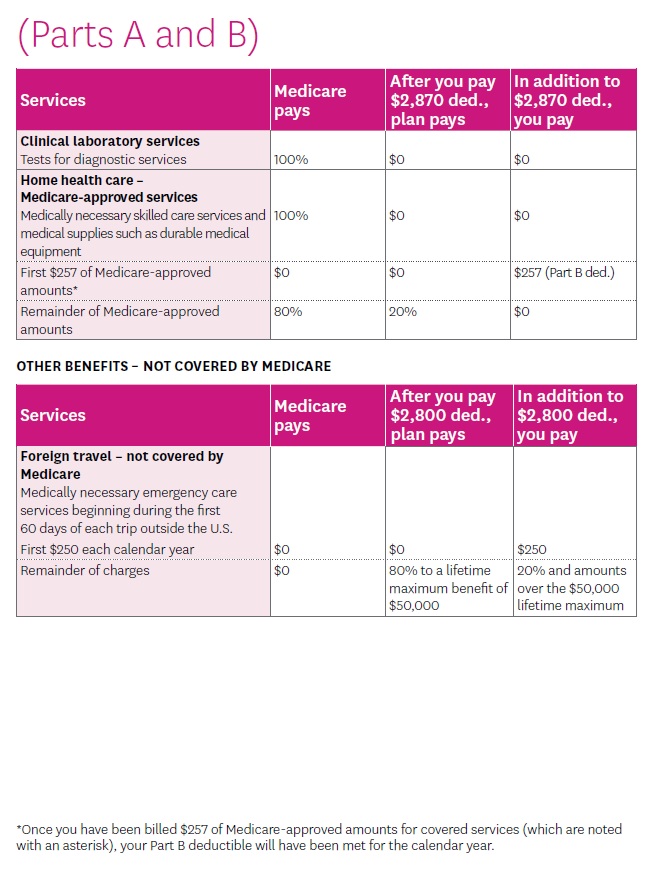

After Medicare pays – you pay $2,870 – then plan pays…

|

|

|

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

Introduction to #MediGap

Publication 02110

- 2025 Official Medicare Guide to choosing a Medi Gap Policy # 02110

- MORE Information and Links

- Matrix - Spreadsheet of what Medicare Pays, Medi Gap pays and what little you pay