Can You Get a Medigap Plan With No Health Questions?

Guaranteed Issue

California has several situations where you may be able to buy or change a Medicare Supplement / Medigap plan without medical underwriting. The two most common questions I get are: “Can I use the California Birthday Rule?” and “What happens if my Medi-Cal changes?”

Start here — which situation applies to you?

1. I have a birthday coming up.

You may be able to change to another Medigap plan under California’s Birthday Rule.

2. My Medi-Cal changed, ended, or my share of cost changed.

You may have a special Medigap opportunity, depending on your Medicare, Medi-Cal, and current coverage situation.

3. My Medicare Advantage plan ended, changed, or I moved.

You may have a guaranteed-right-to-buy situation, depending on the facts and timing.

4. I’m turning 65 or just enrolled in Medicare Part B.

This is usually the cleanest time to buy a Medigap plan because medical underwriting generally does not apply during your Medigap open enrollment window.

Important: Many Medigap rights are time-sensitive. If your birthday, Medi-Cal notice, Medicare Advantage termination, move, or Part B effective date is involved, do not wait until the deadline is almost over.

What to email me: your date of birth, Medicare Part A and Part B effective dates, current plan name, county, and any notice you received from Medi-Cal, Medicare Advantage, or your insurance company.

- What’s on this (our Medi Gap Guaranteed Acceptance) page?

- You Just turned 65

- MAPD Plan lowers benefits or raised premium

- If you are Under 65

- Birthday Rule

- On year Trial test of MAPD Plan

- Underwriting Holiday rules waived if you want to transfer from one Medi Gap plan to another

- Your Employer Coverage is ending

- Health Questions if you don’t qualify for guaranteed issue

- You have a Change in Medi Cal Benefits

- Official Company Guaranteed Acceptance Guides

Introduction to #MediGap

Publication 02110

- 2025 Official Medicare Guide to choosing a Medi Gap Policy # 02110

- MORE Information and Links

- Matrix - Spreadsheet of what Medicare Pays, Medi Gap pays and what little you pay

#Guaranteed Acceptance Guides Medi Gap

- Blue Shield

- Health Net

- Blue Cross Guaranteed Guide CA Scroll down to page 7 Guaranteed Issue Section of the application

- United Health Care - Email us [email protected]

- Get more detail compare contract explanation at:

- Legislation to make Medi Gap easier to get into, if Medicare Advantage cancels or something >>> Think Advisor *

Introduction

Medi Gap Guaranteed Issue

There are only certain times (Special & Open Enrollment) when you can enroll in a Medi-Gap – Supplemental plans without Medical Health Underwriting questions. These times are called Guaranteed Acceptance – Issue.

Medi Gap is not like Medicare Advantage, where if you enroll when you turn 65 or at AEP Annual Open Enrollment, there are no health questions asked, or ACA under 65 Health Care Reform, where no questions are asked if you enroll at Open Enrollment (Age 65) or a Special Enrollment, See below.

The basic most common time, is when you turn 65.

See below of a summary of the times, then check with us [email protected] or the actual documents we’ve linked to for the exact rules.

- What is a better choice for Me?

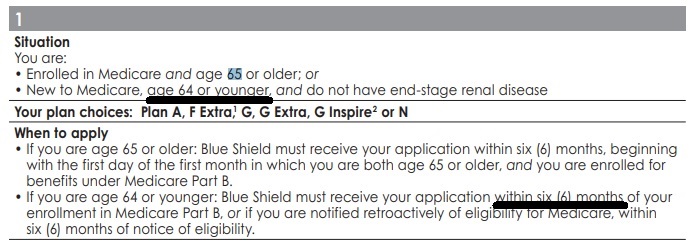

When you turn 65

Medi Gap Guaranteed Issue Rules when you have #turned 65?

Or just enrolled in Part B?

Here’s Blue Shield rule from their Guaranteed Issue Guide:

When’s the best time to buy a Medi Gap policy?

The best time to buy a Medigap policy is during your Medigap Guaranteed Issue Open Enrollment Period. This period lasts for 6 months and begins on the first day of the month in which you’re both 65 or older and enrolled in Medicare Part B. Publication 02110 Page 14 & 45

FAQ’s just turned Age 65 or newly enrolled in Part B”

- Hello – I just signed up for Medicare Part B using the current GEP General Enrollment Period Timetable and Guaranteed Issue Availability Since I relied on Cobra coverage, which isn’t considered Employer Coverage, I will be subject to a penalty Am I entitled to a guaranteed issue Medigap policy, and how soon before July do I have to obtain the policy?

- Yes, under situation # 1 above, you are entitled to guaranteed issue Medi Gap as it says 65 and enrolled in Part B!

- I grant you, I don’t like the wording… but I’ve checked with the carriers and have actually had coverage issued.

- I suggest you enroll, as soon as you get confirmation that Part B has been approved!

- See our Medi Gap Pages for Blue Cross , UHC United Health and Blue Shield,

- There is no extra charge for our expertise. You can enroll online or we can help you in a Zoom meeting.

- 1 Is it true that one has to sign up for a Medigap plan within 6 months of starting Medicare?

2 I will be starting in June, [that’s when I turn 65] so can I wait until November to sign up for a Medi-gap plan ? (to save money?)- 1 Yes, see above for details

2 Yes, if I’m counting on my fingers correctly. Your six months would start in June.- I do not recommend that you wait. If this is your plan, you might be better off finding another agent to help you. Purposely waiting can only lead to a malpractice claim and a major hurt to your pocket book. If one knew when they were going to have a claim or be in an accident, they just wouldn’t leave the house that day.

- Will your next question be, how long can you wait to sign up for Part B?

- 3 months after the month you turn 65. That would save you $134/month.

- If you are on a budget, how about Hi F? You pay the first 2k of bills, not paid by Medicare A or B and you save around $100/month on premium. Get quotes and enroll online.

- 1 Yes, see above for details

#Birthday Rule Medicare Guaranteed Issue rules

to change to plan A, F, G or N.

An individual shall be entitled to an annual open enrollment period lasting 60 days or more, commencing with the individual’s birthday, during which time that person may purchase any Medicare supplement coverage that offers benefits equal to or lesser than those provided by the previous coverage. 1358.11. (h) (1) * SB 407 Effective 7.1.2020?

Blue Cross Innovative F or G or Blue Shield Plan F or G Extra, count the same as F or G and don’t require underwriting. CA Health Care Advocates * What Plans can you get? CA Health Care Advocates *

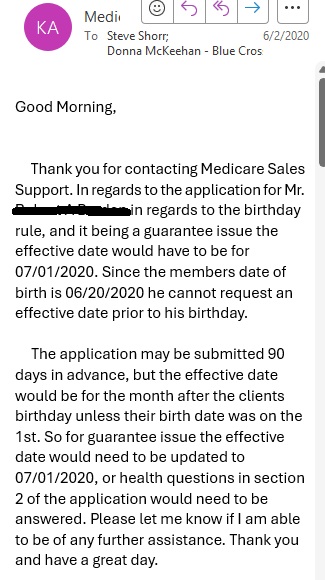

The application may be submitted 90 days in advance, for Blue Cross, but the effective date would be for the month after the clients birthday unless their birth date was on the 1st. CA Health Care Advocates * excerpt of email from BC 6.2.2020 * Ritter Insurance Marketing * CA Insurance Code §10192.11 (h) open enrollment birthday Rule * CA DOI Memo 2/2010 *

- nor discriminate in the pricing of coverage, because of health status,

- claims experience,

- receipt of health care, or

- medical condition of the individual

Blue Shield – Birthday Rule – Chart

Typical Guidelines for all Insurance Companies

Guaranteed Issue Chart – Guide

California Birthday Rule FAQ’s

Don’t wait to wait for your birthday? Try Blue Shields and other companies Underwriting Holiday and/or Just go ahead & Answer Health Questions

Do NOT confuse the birthday rule with Medicare Advantage * AEP Annual Election Period October 15th to December 7th for the next January 1st. They are two totally separate things!!!

FAQ’s on “Birthday Rule”

Effective Date of new policy?

- California’s Medi Gap birthday rule DOES NOT APPLY for Plan C Medicare Advantage

- MAPD Changes can be made only during end-of-year period AEP October 15 through December 7th or a special enrollment MAPD Open & Special Enrollments

- #tobacco usage? It’s guaranteed issue isn’t it?

- CA Insurance Code 10192.11. (h) (1) … annual open enrollment period … During this open enrollment period, no issuer that falls under this provision shall deny or condition the issuance or effectiveness of Medicare supplement coverage, nor discriminate in the pricing of coverage, because of health status, claims experience, receipt of health care, or medical condition of the individual if, at the time of the open enrollment period, the individual is covered under another Medicare supplement policy or contract.

- So, is tobacco usage protected under health status?

- Resource Brokerage.com Central States Indemnity agent underwriting guide – CA requires Tobacco usage question even in Open Enrollment or Guaranteed Issue

- (24)(36) “Health status” means the determination bya carrier ofthe past, present, or expected risk of an individual or the employer due to the health conditions of THE INDIVIDUAL OR the employees of the employer.

(24.5) (37) “Health-status-related factor” means any of the following factors:- (a) Health status;

(b) Medical condition, including both physical and mental illnesses;

(c) Claims experience;

(d) Receipt of health care; Ch. 217 Insurance 913

(e) Medical history;

(f) Genetic information;

(g) Evidence of insurability, including conditions arising out of acts of domestic violence; and

(h) Disability. Colorado.Gov

- (a) Health status;

- One might also check with https://cahealthadvocates.org/ for their research, which isn’t answered on their website

- d. Tobacco Use – If a carrier reflects tobacco usage in the calculation of rates, then it shall do so according to the following requirements:

- Confidential Agent Manual 2017

- Members who have smoked tobacco cigarettes or used any tobacco product at any time within the past 12 months will pay the tobacco rate. Non-tobacco rates apply to all applicants who meet open enrollment or guaranteed issue requirements.

- Obamacare/ACA doesn’t allow health questions, but it does allow tobacco usage to be surcharged 50%. CA though doesn’t allow the surcharge.

- If I sign up for Plan G, Hi-F Medicare Supplement plan now, can I easily switch to a regular Plan F or something higher later?

- The birthday rule above used to only allow you to change from one plan to another of the same or lesser value on your birthday. See the Medi Gap Plans A – N Chart.

- Underwriting Holiday or Freedom to Switch may allow you to do that.

- If you are healthy when you want to make a change, you can do that anytime. Here’s typical underwriting questions.

- What's on this (our Medi Gap Guaranteed Acceptance) page?

- You Just turned 65

- MAPD Plan lowers benefits or raised premium

- If you are Under 65

- Birthday Rule

- On year Trial test of MAPD Plan

- Underwriting Holiday rules waived if you want to transfer from one Medi Gap plan to another

- Your Employer Coverage is ending

- Health Questions if you don't qualify for guaranteed issue

- You have a Change in Medi Cal Benefits

- Official Company Guaranteed Acceptance Guides

Transfer Application

No need to fill out Health Questions

When you fill out the transfer application under the birthday rule, whether ONLINE or Paper, check off the equal or lesser plan that you want.

![]()

Then put down the rule – situation # for the Insurance Company that you are using.

When you get to the Statement of Health, you don’t have to fill out any questions.

While these pictures are from the Blue Shield application, the general principles apply to all Insurance Companies.

Blue Shield of California Authorized Agent - Broker

![]()

Reference Medicare.gov Choosing a Medi Gap policy

- Our webpage on F vs G

- Fact Sheet Medicare Costs

- Fact Sheet Innovative Benefits Hi Cap

When you lose Employer Coverage

When you enroll in Medi Gap beyond age 65 for Part B as you had

Qualifying #Employer Coverage

Termination of Employment or Retirement Plan

You have the right to purchase a Medi-gap policy for 6 months if your, your spouse’s or a family member’s current employment or retirement plan coverage terminates, or you lose your eligibility due to divorce or death of a spouse or family member.

The 6-month period to apply for a Medigap policy starts on the date you receive notice that your health benefits will end. If you do not receive advance notice, the 6-month period starts the date the benefits end or the date of your first denied claim. This protection of California law applies whether your group health benefits were primary or secondary to Medicare.

Our webpage on the pros & cons of Employer Coverage vs Medicare

Loss of COBRA or Cal Cobra

You are also entitled to this protection when you become eligible for COBRA (Our webpage on COBRA) or have used up all your COBRA benefits. It does not apply if you stop paying COBRA premiums before you use all your benefits. COBRA benefits are always secondary to Medicare benefits unless you have ESRD Renal Kidney Failure and are in a 30-month coordination period. For more information on COBRA, see Medicare & Other Health Insurance. CA HealthCare Advocates *

COBRA and Medicare are VERY VERY confusing. Double check with us [email protected] on your specific situation!!!

Situation 4 From Medi Gap Guaranteed Issue Guide

You received notice of termination, or your coverage was terminated from any employer-sponsored health plan, including an employer-sponsored retiree health plan. This includes termination for loss of eligibility due to divorce or death of a spouse.

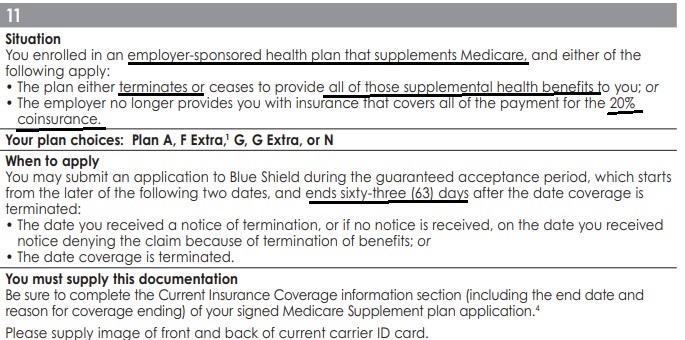

Situation 11 from Medi Gap Guaranteed Issue Guide

- You enrolled in an employer-sponsored health plan that supplements Medicare, §419 (e) Welfare Benefit Plans and either of the following apply:

- The plan either terminates or ceases to provide all of those supplemental health benefits to you; or

- The employer no longer provides you with insurance that covers all of the payment for the 20% coinsurance.

- Why is there Both situation 4 and 11?

- I asked and was told # 11 applies to §419 (e) Welfare Benefit Plans

- Learn More about not enrolling in Part B if you have employer coverage

- See our main page on loss of employer coverage

FAQ Loss of Employer Coverage

FAQ’s

Loss of Employer Coverage

- Where can one find the Official list for Medicare Advantage Plans, being as they differ from Medi Gap Plans?

- Are Medigap policies written during the 8-month Special Enrollment Period issued subject to the same terms as terms, with regard to pre-existing conditions, as those written during the Initial Enrollment Period?

- The waiver of Pre X would be the same. Situation # 4 above says the enrollment period is 6 months. It gets QUITE confusing with different rules for different enrollments… Part B Outpatient, Part D Rx, Medicare Advantage, etc. One has to check each option with a fine tooth comb!

- See links above to enroll online with Blue Cross and Blue Shield, email us for UHC United Health Care

- Here’s our scheduler to set a zoom meeting with screen sharing. set-a-meeting/

- See links above to enroll online with Blue Cross and Blue Shield, email us for UHC United Health Care

- The waiver of Pre X would be the same. Situation # 4 above says the enrollment period is 6 months. It gets QUITE confusing with different rules for different enrollments… Part B Outpatient, Part D Rx, Medicare Advantage, etc. One has to check each option with a fine tooth comb!

- I already have Medicare A and want part B. I am covered by a federal employee health plan (FEHB). Medicare (SSA) says I need to have a form filled out by my company president to verify employment- my W2 and tax form indicating coverage is not enough. Online it says my Medicare part B won’t start until July.

- We will answer that question on our page about if you have employer coverage – do you have to enroll in parts A, B & D?

- If you want more information and details – Please send a copy of your termination notice and if at all possible, all documents from your Employer’s Health Plan. Don’t hold back. We need to see if your under situation 4 or 11.

- Did the employer plan supplement Medicare or not?

- If one gets terminated from their spouses retiree benefits plan when the spouse passes away is there a guaranteed enrollment period into Medi Gap and how does it work?

- Yes. See situation # 4 above.

- If you cancel your Part B, then you to reinstate Part B later will you have guaranteed issue rights for Medi Gap?

- Excerpt from Medicare Medi Gap Guide # 02110 * Medicare.Gov *

- It’s also important to understand that your Medi gap rights may depend on when you choose to enroll in Medicare Part B. If you’re 65 or older, your Medigap Open Enrollment Period begins when you enroll in Part B and it can’t be changed or repeated.In most cases, it makes sense to enroll in Part B and purchase a Medi gap policy when you’re first eligible for Medicare, because you might otherwise have to pay a Part B late enrollment penalty and you might miss your Medi gap Open Enrollment Period. However, there are exceptions if you have employer coverage.

- From prior conversations and emails, you’ve stated that you have an application pending for Part B, but have not been enrolled. I’d check and see if you can get the application cancelled, as if you never asked to be enrolled in Part B.

- Either you or I can write to HICAP – CA Advocates and see what light they can put on the subject.

- This may be a question to learn when you got Part B and if you can get guaranteed issue at a later date…

- Excerpt from Medicare Medi Gap Guide # 02110 * Medicare.Gov *

Employer loss of Coverage Guaranteed Issue

CA Insurance Code §10192.11

(e) (1) An individual enrolled in Medicare Part B is entitled to open enrollment described in this section for six months following:

(A) Receipt of a notice of termination or, if no notice is received, the effective date of termination from any employer-sponsored health plan including an employer-sponsored retiree health plan.

(B) Receipt of a notice of loss of eligibility due to the divorce or death of a spouse or, if no notice is received, the effective date of loss of eligibility due to the divorce or death of a spouse, from any employer-sponsored health plan including an employer-sponsored retiree health plan.

(C) Termination of health care services for a military retiree or the retiree’s Medicare eligible spouse or dependent as a result of a military base closure or loss of access to health care services because the base no longer offers services or because the individual relocates.

(2) For purposes of this subdivision, “employer-sponsored retiree health plan” includes any coverage for medical expenses, including, but not limited to, coverage under the Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA) and the California Continuation Benefits Replacement Act (Cal-COBRA), that is directly or indirectly sponsored or established by an employer for employees or retirees, their spouses, dependents, or other included insureds.

Be careful and double check – COBRA might not get you out of the Part B Late Enrollment Penalty!

- Interaction between COBRA and Medigap Guaranteed Issue Requirements in Situations Involving Termination of Employer Group Coverage

You tried Medicare Advantage, but didn’t like it

Medicare #Trial Period rules & guarantees about if you get a

Medicare Advantage Plan MAPD and

then you would rather switch to Originial Medicare A-Hospital & B- Doctor Visits and a Medi-Gap plan?

There is a Medicare Advantage 12 month trial period (free-look) in which you can get an MAPD and come back to Medi Gap. This trial period can be either when you first turn 65, or you drop a Medi-Gap plan to enroll in a MAPD Plan.

Trial Rights FAQ

FAQ’s

MAPD Trial Period – Come back to Medicare and Medi-Gap”

- Question I enrolled in a Medi-Gap plan, last year when I turned 65. If I enroll in a Medicare Advantage plan, can we go back to our Medi Gap plan anytime or do we have to wait for Open Enrollment, 10.15 to 12.7 annually?

. - Answer If you cancel the MAPD plan within 12 months, you can go back to your Medi Gap plan.

- If you stay in the MAPD plan longer than a year, you would have to meet underwriting – health questions to get a Medi Gap policy. There might be some Insurance Companies more liberal, but the law doesn’t require it.

- Check with us when you’re ready to change. Sometimes there are “limited time” special offers, underwriting holidays – freedom to switch

- The Open Enrollment Period is only for MAPD and Part D Rx guaranteed sign up, switching plans or going back to original medicare, Parts A & B.

- Again, if you are in a MAPD plan longer than a year, it’s not guaranteed issue to get your Medi Gap plan back

- The Trial right is only for the first time you drop Medi Gap to try MAPD

.

- Question If I understand it, this benefit – Right to get a Medi Gap Plan occurs because there is a “trial” period for MA in certain cases. However, those cases don’t seem to include the case in which MA was obtained upon returning from overseas. What am I missing?

.- Answer Federal Guaranteed Rights to get Medi Gap is shown in Publication 02110 above

- You are right, in your case, as you are not currently living in the USA you wouldn’t be joining at age 65, since you are not resident in any MAPD Service area.

- Check the other guaranteed issue rights, like if there is a change in premium or benefits.

- Blue Shield is liberal… Plus CA has or may have more liberal rights for guaranteed issue into Medi Gap Check out situation 14 Check out Situation # 17 if you get another company who changes benefits or premium 15% or more…

- One must read all these rules at least 3 times and then when you think you understand it, read it again. Justice Felix Frankfurter

.

- Question Do I understand correctly that a MAPD plan that was guaranteed issued, as I was living overseas and returned to USA as we discussed in this can be reverted to original Medicare + Medigap also on a guaranteed issue basis after a year?

- Answer Yes. That’s what this whole section is about. See above for details and explanation. If you have further questions, email us

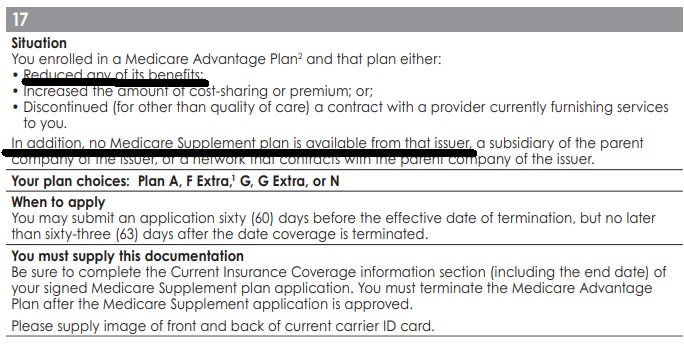

Renewal Medicare Advantage Plan offers #less benefits or raises premium

Excerpt from Blue Shield

Situation # 17

MAPD plan ends – Medi Gap in CA purchasable till May 3rd CA Health Care Advocates.com

CA Insurance Code §10192.12 (D) (i) The Medicare Advantage plan in which the individual is enrolled reduces any of its benefits or increases the amount of cost sharing or premium or discontinues for other than good cause relating to quality of care its relationship or contract under the plan with a provider who is currently furnishing services to the individual.

An individual shall be eligible under this subparagraph for a Medicare supplement policy issued by the same issuer through which the individual was enrolled at the time the reduction, increase, or discontinuance described above occurs or, commencing January 1, 2007, for one issued by a subsidiary of the parent company of that issuer or by a network that contracts with the parent company of that issuer.

If no Medicare supplement policy is available to the individual from the same issuer, a subsidiary of the parent company of the issuer, or a network that contracts with the parent company of the issuer, the individual shall be eligible for a Medicare supplement policy pursuant to paragraph (1) of subdivision (e) issued by any issuer, if the Medicare Advantage plan in which the individual is enrolled does any of the following:

(I) Increases the premium by 15 percent or more.

(II) Increases physician, hospital, or drug copayments by 15 percent or more.

(III) Reduces any benefits under the plan.

(IV) Discontinues, for other than good cause relating to quality of care, its relationship or contract under the plan with a provider who is currently furnishing services to the individual.

(ii) Enrollment in a Medicare supplement policy from an issuer unaffiliated with the issuer of the Medicare Advantage plan in which the individual is enrolled shall be permitted only during the annual election period for a Medicare Advantage plan, except where the Medicare Advantage plan has discontinued its relationship with a provider currently furnishing services to the individual. Nothing in this section shall be construed to authorize an individual to enroll in a group Medicare supplement policy if the individual does not meet the eligibility requirements for the group.

- I don’t see that the Federal Law per the Medi Gap Guide has this rule.

- – Have us or your agent review bullet points 7 & 8 in confidential agent manual.

- When a Medicare Advantage Plan Does Not Renew Its Contract * California Health Care Advocates * Medicare Advocacy.org

Under 65 – Medi Cal Changes

I have Medicare and I’m #under 65,

What Medi Gap or Medicare Advantage Plans can I get?

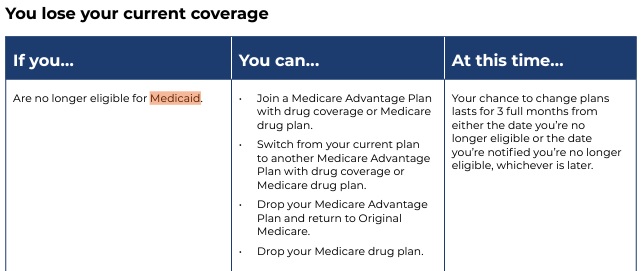

If you are under 65 and have Medicare due to a disability, SSDI, SSI? you can get Part D Rx, Medicare Advantage and Medi Gap plans, guaranteed issue, no medical questions asked, in California by enrolling when you are first eligible or in the case of Part D & Medicare Advantage, at Open Enrollment 10.15 to 12.7 each year. Other states may differ, learn more CA Healthline 1.4.2016.

When you turn 65, that gives you an additional time to enroll in a Medicare Supplement plan at LOWER rates.

See Medicare and You # 10050 and each Insurance Companies Web Page (see menu above) for details, brochures, enrollment forms and rates.

Please email us, [email protected] if you want more personalized attention.

FAQ’s, Resources & Links

Special Enrollment times for Medicare Advantage

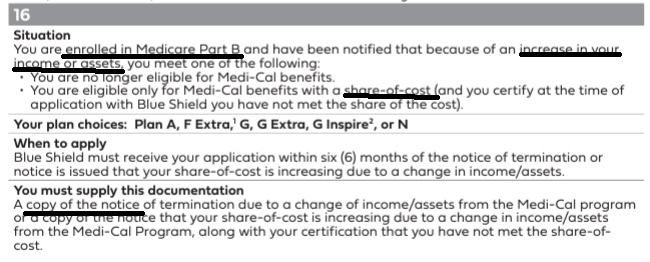

Guaranteed Right to get Medi Gap if your #Medi-Cal benefits change...

- You can deduct the cost of that policy or product and that may help them get under the strict income limit in the Aged & Disabled Federal Poverty Level FPL and Blind FPL programs. See above, you must have original Medicare, A & B not Medicare Advantage. Learn More Medicare.gov

- You may be able to drop Medicare Advantage - but that is up to YOU! We are not telling you to do it!

- If your purchase private health insurance with coverage that duplicates Medi-Cal coverage, the private health coverage would be billed first and then Medi–Cal would pay for the services it covers after the private health carrier pays or denies a claim. Our webpage on Dual Coverage * Western Center Law & Poverty Guide for Low Income Americans * CA Code of Regulations 22 § 50555.2 * Health Care Rights.org *

Guaranteed Issue Rules to Get Medi Gap

- Here’s a video explanation of our research on how one might get Medi Gap even if they are not healthy. If you have a Medicare Advantage plan, see also Situation # 17

- Visit our Medi Gap Guaranteed Issue Page

- Problems getting Medi Gap if you have full benefits Medi Cal?

Right to Opt out of Medicare Advantage

FAQ under 65

FAQ’s “Under 65 disabled & Medicare Qualified”

- I have been trying to get a Medicare supplement for two years. NO one will give me one. I get denied for anything, for an H. Pylori infection. Every company I apply with denies me. I was born in 1957 and have Medicare but no company will give me a supplement. They all want to give me prescription drug plan while denying the medical plan. I live in California.

- How about Medicare Advantage at the next Open Enrollment? Medicare Advantage is guaranteed issue, while Medicare Supplements where you can go to any doctor or hospital that accepts Medicare is not. Check out our page on when Supplements are guaranteed issue. See also the subpage where if you take a Medicare Advantage Plan and don’t like it, you can then get a supplement. Let’s talk privately about some companies that have an unofficial practice of being more liberal…

- Please note that Medicare Supplements are not like Obama Care, there is no right to guaranteed issue, any time. Even Obama Care has certain open enrollment periods. See our page on Medical Loss Ratio, the Insurance Companies take in a small premium…from lots of people, but have to be able to pay all claims from all policy holders. See also the new page – under construction we are building on Donald Care. It appears that many of our leaders don’t understand medical underwriting and the law of large numbers.

- Hi. I’m looking for the best price on a Pre-65 Plan N supplement. We have Anthem at $249/month. My wife is on Social Security Disability. Birthdate: 10/25/1954. The price for Anthem started at $174 and after six months they raised it to $249. Any possibilities we should look into?

- I’ve responded to you privately. Use the menu above to check out other companies for Medi-Gap… but there may be a problem with Guaranteed Issue. In October there is Medicare Advantage.

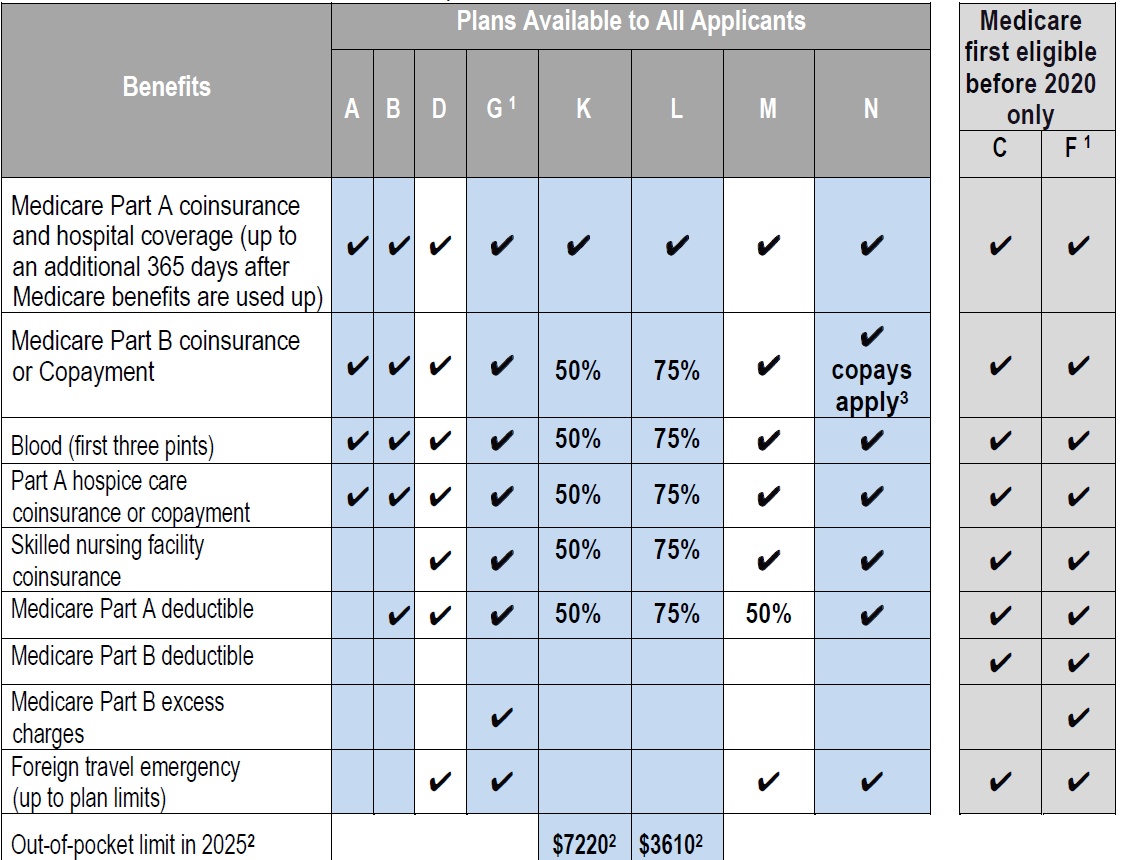

Steve talks about Plan G & Extra - Innovative VIDEO

What Plan G pays in addition to Medicare Parts A & B

- Check our Carrier Pages for the latest Info

- Anthem Blue Cross

- Blue Shield – Medi-Gap

- Email us [email protected] for UHC United Health Care information

- Plan G vs Plan F much better pricing our webpage

- Medicare Advantage and Part D Rx enrollment periods - THEY ARE NOT THE SAME AS Medi GAP! our webpage

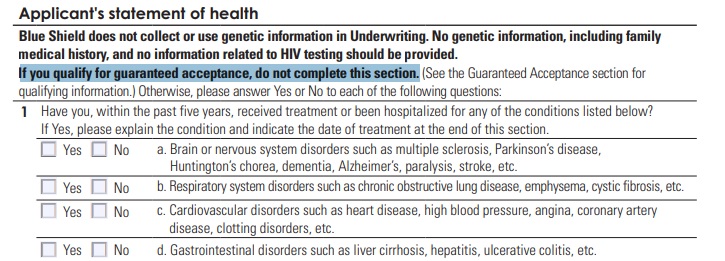

Underwriting – Health Questions

What are the Medical #Underwriting Questions for a Medi-Gap policy

if I’m not in a guaranteed issue period, like just turning 65?

Check the paper applications below and review the questions:

- Blue Cross Application – Section 2A

- Blue Shield Application Page 121 of Enrollment Kit – Page 6 Application

- We have other companies that don’t allow agents to post information…. email us [email protected]

- Possible Pre X period if you don’t have prior creditable coverage

- Email us to discuss [email protected]

“Medical Questions – Underwriting – If not in Guaranteed Issue Period?”

- CANCER

- Question I have Plan F Medi Gap and applied for Plan G to save premium. So what if the Part B Deductible is higher. It wasn’t my birthday. What RIGHT does the Insurance Company have to deny the transfer because I had an alleged pre-existing condition a nothing squamous cell skin cancer. It’s hard to find someone who has not had a skin cancer.

- Answer 1st off, when I ask my higher ups at any of the Medi Gap Insurance Carriers about health underwriting, I get a blank stare, as most everyone gets a Medi Gap policy or change at a Guaranteed Issue date – period.

- Thus, I can’t get underwriting guidelines from anyone. Here’s an excerpt from a well known carrier, prior to ACA/Obamacare when asking health questions and pre X clauses where outlawed for under 65. Conversely, there is a mandate and only certain times one can enroll.

- There are exclusions for tons of stuff. Insurance Companies need to collect $1 to pay claims of 80 cents. It’s called MRL Medical Loss Ratio and is written into ACA/Obamcare. It was pretty much the way it was before.

- Insurance underwriters evaluate the risk and exposures of potential clients. They decide how much coverage the client should receive, how much they should pay for it, or whether even to accept the risk and insure them. Underwriting involves measuring risk exposure and determining the premium that needs to be charged to insure that risk. The function of the underwriter is to protect the company’s book of business from risks that they feel will make a loss and issue insurance policies at a premium that is commensurate with the exposure presented by a risk.

- Each insurance company has its own set of underwriting guidelines to help the underwriter determine whether or not the company should accept the risk. The information used to evaluate the risk of an applicant for insurance will depend on the type of coverage involved. For example, in underwriting automobile coverage, an individual’s driving record is critical. However, the type of automobile is actually far more critical. As part of the underwriting process for life or health insurance, medical underwriting may be used to examine the applicant’s health status (other factors may be considered as well, such as age & occupation). The factors that insurers use to classify risks are generally objective, clearly related to the likely cost of providing coverage, practical to administer, consistent with applicable law, and designed to protect the long-term viability of the insurance program.[3]

- The underwriters may decline the risk or may provide a quotation in which the premiums have been loaded (including the amount needed to generate a profit, in addition to covering expenses[4]) or in which various exclusions have been stipulated, which restrict the circumstances under which a claim would be paid. Depending on the type of insurance product (line of business), insurance companies use automated underwriting systems to encode these rules, and reduce the amount of manual work in processing quotations and policy issuance. This is especially the case for certain simpler life or personal lines (auto, homeowners) insurance. Some insurance companies, however, rely on agents to underwrite for them. This arrangement allows an insurer to operate in a market closer to its clients without having to establish a physical presence.

- Two major categories of exclusion in insurance underwriting are moral hazard and correlated losses.[5] With a moral hazard, the consequences of the customer’s actions are insured, making the customer more likely to take costly actions. For example, bedbugs are typically excluded from homeowners’ insurance to avoid paying for the consequence of recklessly bringing in a used mattress.[5] Insured events are generally those outside the control of the customer, for example (typical in life insurance) death by automobile accident, contrasted with death by suicide. Correlated losses are those that can affect a large number of customers at the same time, thus potentially bankrupting the insurance company. This is why typical homeowner’s policies cover damage from fire or falling trees (usually affecting an individual house), but not floods or earthquakes (which affect many houses at the same time).[5]wikipedia.orgInsurance_underwriting

- Here’s our webpage on the rate review process. That is, the CA Department of Insurance reviews the rates and underwriting guidelines to make sure they are actuarially sound.

- COST OF TREATMENT FOR SQUAMOUS CELL CARCINOMA OF THE HEAD AND NECK IN THE UNITED STATES

- Average per patient cost of care for SCCHN in the US was estimated to be $20,876.

- Higher costs resulted for patients that present with advanced cancers.

- The estimated cost of treating a patient with Stage IV lip SCC ($19,274) was four times that of Stage 0 lip SCC ($5,062).

- The site with the lowest cost of treatment was lip ($7,261) while the highest cost was associated with hypopharyngeal SCC ($28,584).

- The cost per patient for palliative care ranged from $2,052 for lip SCC (28% of total cost of care) to $7,172 for sinonasal SCC (30% of total cost of care).

- The lifetime cost of managing annual incident SCCHN cases was estimated to approximate $976 million.

- CONCLUSION: This study found that tumor stage and location are useful predictors of increased treatment costs. The results suggest that prevention and early detection are critical in reducing the treatment costs of SCCHN. wiley.com/

.

- CONCLUSION: This study found that tumor stage and location are useful predictors of increased treatment costs. The results suggest that prevention and early detection are critical in reducing the treatment costs of SCCHN. wiley.com/

- Question I’m living outside the USA, if I apply for a Medigap plan and am subject to underwriting, how much extra would coverage cost and what are the underwriting requirements?

- The requirements or at least the questions are in the respective insurance company applications.

- The price – premium is the same for those who enroll during a SEP or Guaranteed Enrollment Period. You can get those rates on our webpages for each company by using the site map, menu above or the link above to Blue Cross and Blue Shield affiliate sites.

- I find it very odd that there are some situations where you can be offered an underwriting-free MediGap choice upon return to the US.

- Is this only if you have or once had a policy?

- What if the provider cancels the policy when you are out of state/country (as it can do)?

- Those situations are limited to getting a Medicare Advantage Plan and then using the Trial Period to get a Medi-Gap plan or did I forget an SEP into Medi Gap?

- MAPD enrollment when returning to USA doesn’t matter on if you had a MAPD or Medi Gap policy before.

- I’m not aware that a Medi Gap carrier can cancel coverage when you move out of state or country. Residency is only required when you purchase coverage..

- Answer I don’t ever want to deal with underwriting because even though I’m a healthy person, the insurance companies may look at the info in the MIB and think I am not. So it sounds like I should get a regular Plan F at the get go when starting Medicare in June. Is that what you would recommend?

- How healthy are you, related to the questions on the applications above?

- Have your reviewed your MIB Medical Information Bureau File? mib.com/request_your_record

- MIB shouldn’t have anything that isn’t being asked in the applications. There’s a law somewhere that says Insurance Companies cannot deny you based only on the MIB file. They can only use it to indicate things that need to be investigated further.

- If you want the Medi Gap plan with the highest benefits Plan F and don’t want to worry about underwriting, yes. Note Plan F is no longer available if you turned 65 after January 1st 2020.

- Get Instant Medi Gap Quotes

Underwriting Holiday

“Underwriting #Holiday”

Freedom to Switch

Blue Shield is offering a Underwriting Holiday offer beginning on June 1 through December 31, 2023. Email 8.31.2022 & 9.27.2022

This offer allows you to enroll in ANY* available Blue Shield of California Medicare Supplement plan without answering any health questions or obtaining underwriting approval. You can enroll in ANY* available Blue Shield of California Medicare Supplement Plan without answering any health questions or obtaining underwriting approval.

email us [email protected] for more details

Sometimes, The Insurance Companies might have a “Underwriting Holiday” or Freedom to Switch where you can change to the Insurance Company celebrating the Holiday with NO health questions, as long as you currenlty have a Medi Gap Plan and sometimes a Medicare Advantage Plan.

We don’t have a crystal ball and the Companies don’t seem to allow us to post information about the holidays. So, email us [email protected] and we can let you know the current offerings.

Be sure to do this early in AEP so that there isn’t any lapse in getting Part D Rx… See our webpage on Part D enrollment periods.

*Plan F is limited to those who became Medicare eligible before 1.1.2020, learn more MACRA

InsuBuy International Medical Coverage –

Instant Quotes & Enrollment

Coverage for Travel - $50k Emergency under Medicare Medi Gap or MAPD Advantage may not be enough!

California Law

CA Insurance Code §10192.11 (h) open enrollment birthday Rule

ARTICLE 6. Medicare Supplement Policies [10192.1 – 10192.24]

CA Health Advocates Guaranteed Issue More

#Medicare10050 and You 2025

Spanish

Everything you want to know

- Steve's Video Seminar Introduction to Medicare & You

- Clear View to Medicare Patient Advocate.org - 36 pages

- Get Ready for Medicare * Spanish

***********

- Your Medicare #Benefits # 10116

- Inpatient ONLY - How Medicare Pays for your Surgery Part A vs Part B Very Well Health.com

- 2026 Updates CMS.gov

- Enroll in Blue Cross

- Use our scheduler to Set a phone, Skype or Face to Face meeting

- #Intake Form - We can better prepare for the meeting (National Contracting Center)

- Get more information and FAQ's

- #Intake Form - We can better prepare for the meeting (National Contracting Center)

https://cahealthadvocates.org/birthday-rule-is-not-to-blame-for-rising-medigap-premiums/

Medi Gap Birthday Rule 60 days

https://share.google/aimode/rFCv6r2tIBVWjTQpl

https://cahealthadvocates.org/understanding-californias-unique-medigap-rules-extra-consumer-rights/

https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?lawCode=INS§ionNum=10192.12

https://share.google/aimode/deYza9IpYshloUnya

https://share.google/aimode/deYza9IpYshloUnya

https://cahealthadvocates.org/medigap/guaranteed-issue/

https://cahealthadvocates.org/wp-content/uploads/2026/05/NAIC-SITF-Meidgap-BirthdayRule-05.18.26.pdf

Steve the statute applies to MA plans that reduce any benefits or increases costs. So yes a GI right applies if benefits are cut or costs go up

Bonnie Burns, Consultant

Training, Policy, Technical Assistance

California Health Advocates

21 Locke Way

Scotts Valley, CA 95066

831-438-6677 (office phone)

[email protected]

http://www.cahealthadvocates.org

“Of the moment,be. In the moment,live. The art of remaining in the present,learn. Neither the past nor the future exists.” Yoda.

On 2/21/2026 10:28 AM, Steve Shorr wrote:

Does this rule also count if MAPD lowered benefits?

https://cahealthadvocates.org/medicare-advantage-plan-ended-you-have-a-guaranteed-right-to-medigap/