Why Did My Covered CA Premium Go Up?

If your Covered California or individual health insurance premium increased, it does not necessarily mean you did anything wrong, used too many claims, or picked the wrong plan. Premiums can change because of medical costs, prescription drug costs, age, region, plan changes, and subsidy changes.

Quick Answer

Health insurance rates are based on the cost of covering the whole group of people in your area and plan, not just your own claims. In 2026, Covered California announced a weighted average rate increase of 10.3%, and many people also saw higher net premiums because the federal enhanced premium tax credits ended December 31, 2025. Financial help may still be available, but the amount can be different than before.

Covered CA 2026 rates

Federal changes

The Most Common Reasons Premiums Increase

1. Overall rate increases

Each year, insurance companies file rates based on expected medical claims, prescription drug costs, hospital contracts, doctor costs, and administrative expenses. Even if you had no claims, the premium may increase because the total cost of care for the group went up.

2. Your subsidy changed

Your monthly cost depends heavily on your premium tax credit. If your income estimate, household size, tax filing status, or subsidy rules changed, your net premium can go up even when the plan itself did not change very much.

3. Age and rating area

Individual and family health insurance premiums are affected by age, location, household members, and the plan selected. A birthday, a move, or adding/removing a family member can change the premium.

4. Plan design changed

Deductibles, co-pays, drug tiers, provider networks, and out-of-pocket limits can change from year to year. A lower monthly premium is not always the cheapest choice if you use doctors, hospitals, or prescriptions.

5. Prescription drug costs

New specialty drugs, brand-name medications, pharmacy contracts, and drug-tier changes can affect premiums and out-of-pocket costs. Always check your prescriptions before switching plans.

6. Medical Loss Ratio rules

The ACA Medical Loss Ratio rule generally requires health insurers to spend at least 80% or 85% of premium dollars on medical care and quality improvement, or issue rebates if they miss the standard.

CMS MLR rules Our webpage on MLR

Before You Cancel or Switch Plans

Do not judge a plan only by the monthly premium. A cheaper plan may have a smaller network, higher deductible, different drug coverage, or higher out-of-pocket costs when you actually use care.

- Check your subsidy: Is your income estimate current?

- Check your doctors: Are they still in the plan network?

- Check your prescriptions: Are your medications covered, and at what tier?

- Check the deductible and out-of-pocket maximum: Low premium does not always mean low total cost.

- Check Enhanced Silver: If you qualify, Silver 73, 87, or 94 may reduce co-pays, deductibles, and out-of-pocket exposure.

What I Can Help You Review

Compare your renewal notice

I can help compare your current plan against other Covered CA and individual market options.

Review subsidy estimates

Income, household size, and tax filing status can make a big difference in your net premium.

Check doctors and hospitals

Network mistakes can be expensive. Do not switch without checking providers.

Check prescriptions

A plan that looks cheaper can cost more if your medications are not covered well.

Want Help Before You Decide?

Send your renewal notice, current plan name, doctors, prescriptions, and estimated household income. I can help you compare options before you switch, cancel, or miss a deadline.

Questions People Ask

Why did my premium go up if I had no claims?

Individual health insurance is pooled. Your rate is not based only on your own claims. It reflects the expected cost of medical care, prescription drugs, hospitals, doctors, and everyone covered in that rating pool.

Is the insurance company just keeping the increase?

The Medical Loss Ratio rule limits how much premium can go to administration and profit. That does not prevent rates from increasing, but it does mean insurers generally must spend most premium dollars on medical care and quality improvement.

Can California block health insurance rate increases?

California reviews proposed rate increases and can ask questions, require justification, and create public accountability. The Department of Managed Health Care says it does not have authority to approve or deny rate increases, but its review can result in reductions.

DMHC rate review

Should I switch to the cheapest plan?

Not automatically. The cheapest monthly premium may have a narrower network, higher deductible, different drug coverage, or higher costs when you need care. Compare total risk, not just the premium.

What should I send Steve?

Send the renewal notice, current plan name, county/ZIP code, doctors, hospitals, prescriptions, household size, and estimated annual income. Do not send Social Security numbers or private medical records unless specifically needed.

Steve Shorr

Website Video #Introduction

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

How can I explain premium increases?

It’s difficult for me to explain when people facing a premium increase, ask why. For some reason, I feel it’s argumentative. I’ll hear that they aren’t having claims, they watch their health don’t have any pre X, etc.

- The 25% Problem: (We don’t need 25% of the services) Why Health Care Is So Expensive (And What We Can Do About It) CHCF 10/2025

- Co Pays and Deductibles or not??? LA Times 1.8.2025 *

- Breaking down the conditions raising employer health care costs UHC 10/2024

- California Office of Health Care Affordability (OHCA) visit their website *

- Medical inflation vs the rest of the economy Kff.org *

- 2024 Failing US Health System comparing to 10 other countries Commonwealth Fund *

- Shining a Light on Health Insurance Rate Increases CMS.Gov

Thus, I’ve compiled on this just about every resource I could find to help explain why it’s so expensive to go to a doctor, hospital or get a Rx drug. Including a feed from CHCF California Health Care Foundation on the latest health care news and trends

Please note also, that under ACA/Obamacare and even before, Insurance Companies are mandated to spend under Medical Loss Ratio Rules a certain amount 80-85% on health care costs.

- Options to improve affordability in CA Health Market 68 pages June 2019

- President Trump said Insurance was more complicated than anyone knew. He should have asked me or reviewed my website!

- If you have comments or questions, please post those below. You don’t have to put in your name.

Resources & Links

- A $336 Band-Aid for a cut finger? Our healthcare system is nuts Los Angeles Times *

- How Much Does Sex Reassignment Surgery Cost? Cost Helper.com *

- California Health Care Almanac Spending pdf

- Facebook.com Discussion of paying your own bills or not…???

- Survey data shows stress spreading beyond medical bills hcamag.com 1/2026

- In 2026, Affordable Care Act (ACA) premiums increased by more than 20 percent, in large part because insurers believe they are facing increased risk due to the expiration of enhanced premium tax credits and other policies. Read more Commonwealth Fund.org 1/2026

- Health Insurers, Lawmakers Lock Horns Over High Cost Of Medical Care KFF.org 1/2026

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

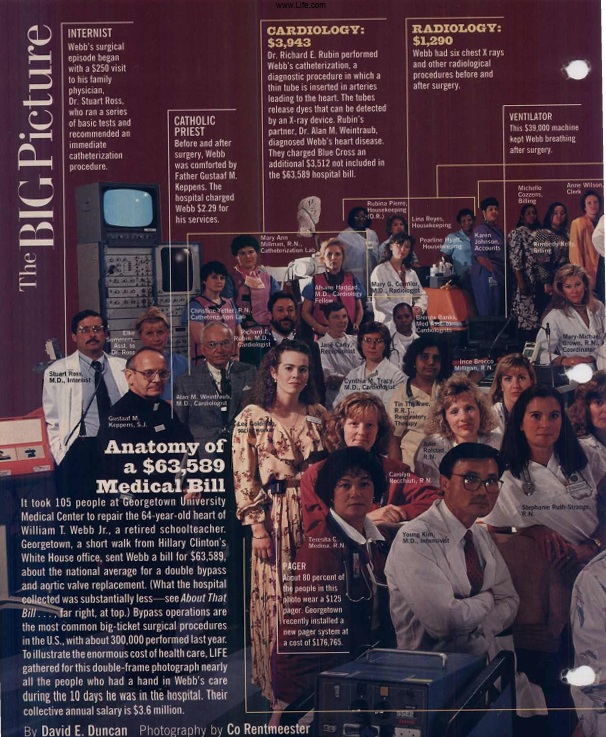

Life Magazine 1993 – Medical Costs have been an issue for a LONG Time

- Here's where the premium for the plan you are NOT using goes. This guy has $4k/month in bills - be thankful it's not you. Los Angeles Times 11.13.2016

- 5 reasons medical costs are rising, according to payers July 2023

- Our webpages on:

HMO Act of 1973

- Cost Control Strategy: The act was designed as a proactive strategy to combat medical inflation by providing a prepaid, cost-effective alternative to traditional insurance.

- Preventative Focus: Supporters aimed to incentivize “health maintenance” rather than just sick care, theoretically providing better, more efficient service.

- Mandated Dual Choice: Section 1310 required employers with 25 or more employees to offer a federally certified HMO option if they already offered traditional health insurance.

- Corporate Expansion: It allowed for-profit entities to run HMOs and offered federal backing for their development. [1, 2, 5, 6, 7]

- The Ehrlichman Tape: A known 1971 conversation between President Nixon and his domestic policy advisor, John Ehrlichman, reveals an understanding that HMO incentives differed from traditional care.

- Incentive Structure: Ehrlichman explicitly told Nixon: “All the incentives are toward less medical care, because the less care they give them, the more money they make”.

- Strategic Choice: While proponents believed in the preventative benefits, the Nixon administration embraced the model specifically to cut costs, acknowledging that the profit-driven structure might result in lower utilization of services. [1, 8, 9, 10, 11]

IRS Form 8889 HSA Health Savings Account #Deduction

Visit our Main Webpage on HSA Health Savings Accounts

https://calmatters.org/health/2026/06/california-health-tax-medi-cal-premiums/