Retirement Income and Covered California MAGI

Social Security, IRA withdrawals, pensions, annuities, investments and other retirement income can affect your Covered California tax credits.

Quick answer: Covered California financial help is based on your expected household income for the coverage year. Retirement income may count toward MAGI if it is taxable or otherwise included under the Marketplace income rules. Covered California lists Social Security, retirement or pension income, investment income, rental income, capital gains and other income categories as countable income for financial help purposes. Covered California: What Counts as Income

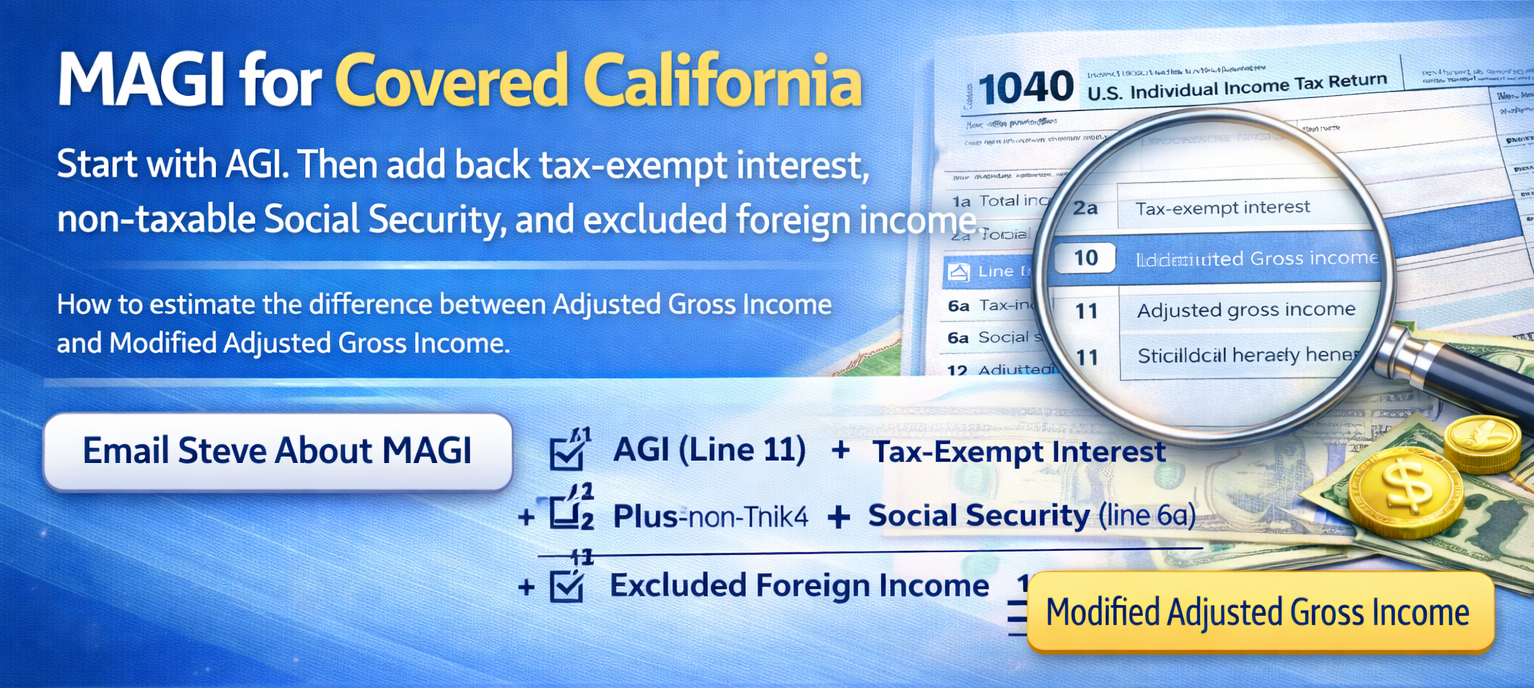

The Basic Rule: MAGI Starts With Your Tax Return

For Affordable Care Act premium tax credits, income is generally based on Modified Adjusted Gross Income, often called MAGI. HealthCare.gov explains that Marketplace MAGI generally starts with Adjusted Gross Income from IRS Form 1040, then adds certain items such as non-taxable Social Security benefits, tax-exempt interest and excluded foreign income. HealthCare.gov: What’s Included as Income

This means that the question is usually not simply, “Is this retirement money?” The better question is:

“Does this retirement money show up in MAGI for Covered California?”

Retirement Income That May Affect Covered California MAGI

Traditional IRA, 401(k), 403(b), SEP, SIMPLE and pension withdrawals: Taxable retirement distributions generally increase Adjusted Gross Income, which usually means they can increase MAGI for Covered California.

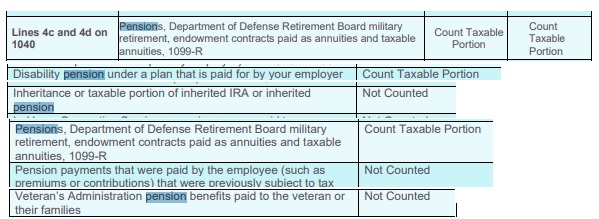

Company pensions and annuities: Pension and annuity income may count if taxable. IRS Publication 575 explains the federal tax treatment of pension and annuity income. IRS Publication 575: Pension and Annuity Income

Social Security retirement benefits: Covered California lists Social Security as income, and Marketplace MAGI also adds back non-taxable Social Security benefits. Because Social Security has its own rules, see my separate Social Security MAGI page rather than relying only on this general retirement-income page.

Investment income: Interest, dividends and capital gains may affect MAGI. Covered California lists investment income and capital gains among income categories used for financial help. Covered California: What Counts as Income

Rental income: Net rental income may affect MAGI, but rental income has its own deductions and tax treatment. See the separate rental income page in this MAGI category section.

Required Minimum Distributions: Required Minimum Distributions from traditional retirement accounts can increase taxable income and may reduce Covered California tax credits. This is especially important for people near an income threshold.

Retirement Money That May Not Count the Same Way

Roth IRA withdrawals: Qualified Roth IRA withdrawals may be non-taxable and may not increase AGI the way traditional IRA withdrawals do. However, the tax facts matter, so confirm with a qualified tax professional before making coverage decisions.

Return of basis: Some annuity, pension or investment payments may include a return of after-tax money. The taxable portion may be treated differently from the non-taxable portion.

Savings account withdrawals: Taking money out of a bank account is not usually income by itself. However, the interest earned on the account may be income.

Plain English example:

If you withdraw $10,000 from a regular savings account, that is usually just using your own money. If you withdraw $10,000 from a traditional IRA, that may be taxable income and may affect Covered California tax credits.

Common Planning Traps for Retirees Under 65

Trap #1: Taking extra IRA money without checking subsidies. A larger IRA withdrawal may help pay bills, but it can also increase MAGI and reduce Covered California premium tax credits.

Trap #2: Selling investments late in the year. Capital gains can increase MAGI. This can matter if the gain is large or if the household is already near an important income level.

Trap #3: Confusing Medicare and Covered California. Once a person is eligible for premium-free Medicare Part A, Covered California tax credit eligibility may change. This page is mainly for people using Covered California before Medicare or for households where one person is still on Covered California.

Trap #4: Looking only at monthly income. Covered California generally looks at expected annual household income for the coverage year, not just what came in this month. Covered California says financial help is based on what you expect your household income will be for the coverage year. Covered California: How to Estimate Your Income

Simple Retirement MAGI Checklist

- Social Security: Check the Social Security MAGI rules.

- Traditional IRA / 401(k) withdrawals: Usually review as taxable income.

- Pension or annuity: Determine the taxable portion.

- Roth withdrawals: Confirm whether the withdrawal is qualified and non-taxable.

- Capital gains: Watch for one-time sales that increase annual income.

- Rental income: Review net taxable rental income, not just gross rent.

- Interest and dividends: Include investment income where required.

- Household members: Include the income of household members who are part of the tax household when required.

Real-World Examples

Example 1: Early retiree before Medicare.

A 62-year-old retires and uses Covered California until Medicare starts. Social Security, IRA withdrawals, pension income and investment income may all affect the amount of tax credit available.

Example 2: Married couple, one on Medicare and one on Covered California.

One spouse may be on Medicare while the younger spouse still needs Covered California. Household income can still matter for the younger spouse’s tax credit.

Example 3: Extra IRA withdrawal for home repairs.

A one-time IRA withdrawal may solve a cash problem but also raise annual MAGI. That may reduce tax credits or create a repayment issue at tax time.

Example 4: Selling stock to create retirement cash.

Capital gains may increase MAGI. A retiree using Covered California should consider the health-insurance impact before selling investments with large gains.

Related MAGI Income Pages

Because retirement income can come from many sources, this page is only the general overview. Use the more specific MAGI pages below for the detailed treatment of each income type.

Capital Gains & Dividends

Rental Income

Gambling Income

Debt Cancellation

All MAGI Categories

Before You Change Retirement Withdrawals

If you are using Covered California, it may be smart to estimate the health-insurance effect before making a major retirement-income decision. A withdrawal, pension election, Roth conversion, investment sale or rental-income change may affect your annual MAGI.

Planning reminder: The best question is not just “How much money do I need?” It is also “How will this income affect my Covered California tax credits?”

Ask Steve

Steve Shorr is a California health insurance agent. He does not provide tax, legal or investment advice. But he can help you look at how health insurance choices, Covered California subsidies, Medicare timing and income estimates may fit together.

Disclaimer: This page is general educational information only. It is not tax, legal, financial-planning, investment or Medi-Cal eligibility advice. MAGI rules depend on tax law, household size, filing status, income sources and Covered California eligibility rules. Check with a qualified tax professional for tax advice.

#Pension & Annuity Income

Publication 575 pdf * HTML

- VIDEO Basic taxation of annuities BROKER ONLY

- About 1099-R

- Required Minimum Distributions FAQ's IRS.Gov

- Lifetime Income - Annuity Calculator

- Get your annuity from [email protected] just use the tool to get an instant idea of what the market is.

Child & Sibling Pages

- Alimony – From a Divorce Settlement taxable

- Capital Gains, Sale of Home & Dividends

- Clergy – Housing Allowance? Covered CA MAGI Income

- Covered CA MAGI Retirement Income

- Educational Credits – Student Loan Interest

- Gambling Income & Losses – Other Income Line 21

- Medical or any Debt Cancellation Covered CA MAGI Income?

- Social Security Benefits MAGI Covered CA Income Subsidies