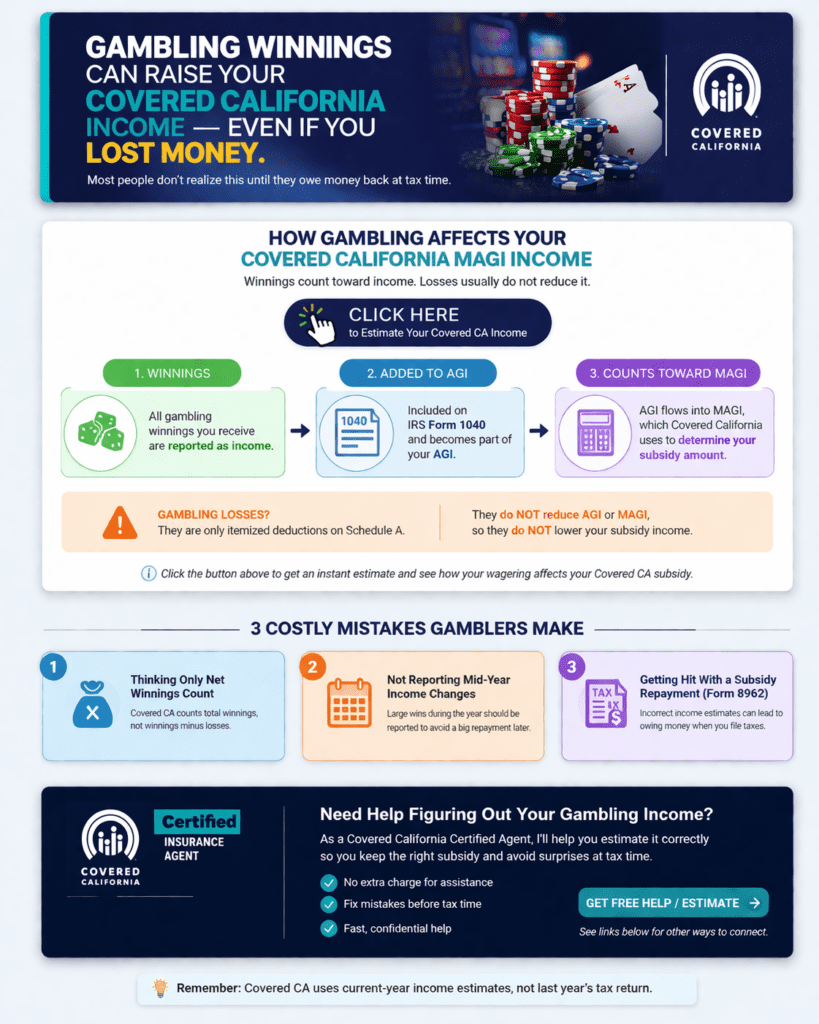

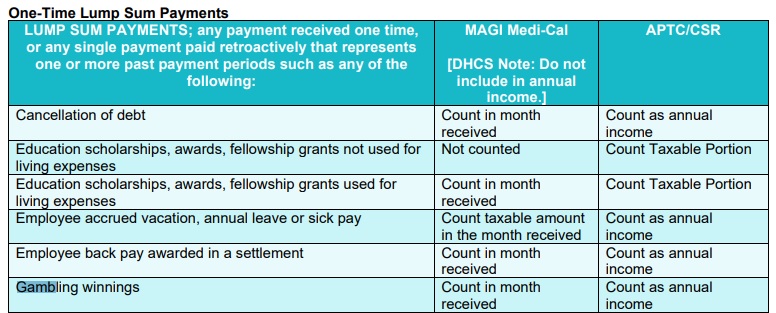

Gambling Winnings Can Raise Your Covered California MAGI Income

Most people do not realize this until their subsidy changes or they owe money back at tax time.

Gambling losses may help on Schedule A itemized deductions, but they usually do not reduce your

Modified Adjusted Gross Income (MAGI) for Covered California subsidy purposes.

How Gambling Affects Your Covered California MAGI Income

Example: You can lose money gambling and still raise your MAGI income

But Covered California may still look at the $15,000 of winnings when determining income for subsidy purposes.

3 Costly Mistakes People Make

For Covered California, the issue is usually whether the winnings increase MAGI. Losses do not usually undo that for MAGI.

A big win during the year can affect subsidy eligibility. Waiting too long can lead to a surprise reconciliation – repayment.

Sometimes a quick review can help you estimate income more accurately and avoid subsidy problems later. See our webpage on reporting changes

Short answer

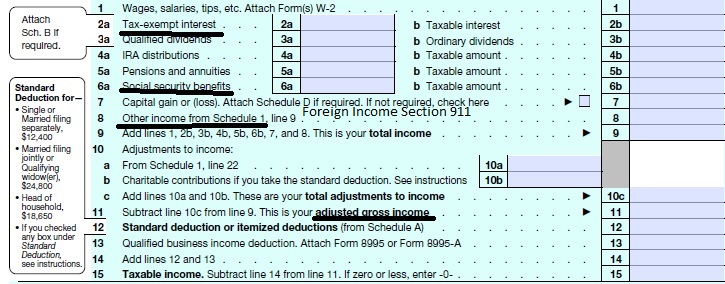

Yes, gambling winnings can count toward income for Covered California because they may increase the AGI income line 11 a shown on your federal tax return 1040.

No, gambling losses usually do not lower Covered California MAGI the same way, because those losses are generally handled as itemized deductions rather than a direct reduction of AGI.

That is why this category causes confusion and why it can help to review the numbers before enrollment or tax filing.

Need help figuring out your Covered California income?

We help people estimate income for Covered California, review subsidy issues, and get quotes at no extra charge for assistance.

✔ No extra charge for complimentary assistance

✔ Phone, Zoom, and email help available

Helpful links

|

Winnings not losses – Professional Gamblers

Unfortunately, for Covered CA subsidies, only #winnings count, NOT losses!!!

- Becky IRS VIDEO

- Tax Topic 419, Gambling Income and Expenses

- gamblers anonymous.org

Report any gambling winnings as income on your tax return. Be sure you itemize to deduct gambling losses up to the amount of your winnings.

The following rules apply to casual gamblers who aren’t in the trade or business of gambling. Gambling winnings are fully taxable and you must report the income on your tax return. Gambling income includes but isn’t limited to winnings from lotteries, raffles, horse races, and casinos. It includes cash winnings and the fair market value of prizes, such as cars and trips.

If you are a casual gambler, (professional – scroll down) these tax tips can help:

Gambling income.

Income from gambling includes winnings from the lottery, horse racing and casinos. It also includes cash and non-cash prizes. You must report the fair market value of non-cash prizes like cars and trips.

A payer is required to issue you a

Form W-2G, Certain Gambling Winnings (PDF), if you receive certain gambling winnings or have any gambling winnings subject to federal income tax withholding.

You must report all gambling winnings as “Other Income” on Form 1040, Schedule 1 (PDF) and attach this to Form 1040 (PDF), including winnings that aren’t reported on a Form W-2G (PDF).

When you have gambling winnings, you may be required to pay an estimated tax on that additional income. For information on withholding on gambling winnings, refer to Publication 505, Tax Withholding and Estimated Tax.

How to report winnings.

You normally report your winnings for the year on your tax return as “Other Income” Line 21. You must report all your gambling winnings as income.

***Thus, a problem for Covered CA subsidies!

This is true even if you don’t get a Form W-2G.

How to deduct losses.

You can deduct your gambling losses on Schedule A, Itemized Deductions.

***Thus, this doesn’t show on line 7 of the 1040 for the MAGI calculation for Covered CA Subsidies!

The total you can deduct, however, is limited to the amount of the gambling income you report on your return.

You may deduct gambling losses only if you itemize your deductions on Form 1040, Schedule A ) and kept a record of your winnings and losses. The amount of losses you deduct can’t be more than the amount of gambling income you reported on your return. Claim your gambling losses up to the amount of winnings, as “Other Itemized Deductions.”

IRS – Interactive Tax Assistant

How Do I Claim My Gambling Winnings and/or Losses?

See Publication 525, Taxable and Nontaxable Income for rules on this topic.

Refer to Publication 529, Miscellaneous Deductions for more on losses. It also lists some of the types of records you should keep.

You can’t reduce your gambling winnings by your gambling losses and report the difference.

You must report the full amount of your winnings as income and claim your losses (up to the amount of winnings) as an itemized deduction. Therefore, your records should show your winnings separately from your losses.

You must keep an accurate diary or similar record of your losses and winnings.

Your diary should contain at least the following information.

- The date and type of your specific wager or wagering activity.

- The name and address or location of the gambling establishment.

- The names of other persons present with you at the gambling establishment.

- The amount(s) you won or lost.

Keep records of your wins and losses. This means keeping items such as a gambling log or diary, receipts, statements or tickets.

Gambling Losses Up to the Amount of Gambling Winnings

- Proof of winnings and losses.

- Keno.

- Slot machines.

- Table games (twenty-one (blackjack), craps, poker, baccarat, roulette, wheel of fortune, etc.).

- Bingo.

- Racing (horse, harness, dog, etc.).

- Lotteries.

- VITA Volunteer Income Tax Assistance.

- Head of addiction medicine society warns of treatment cuts and rising threat of gambling Stat News.com 10/2025

Nonresident Aliens

- If you’re a nonresident alien of the United States for income tax purposes and you have to file a tax return for U.S. source gambling winnings, you must use Form 1040NR, U.S. Nonresident Alien Income Tax Return (PDF).

- Refer to Publication 519, U.S. Tax Guide for Aliens and Publication 901, U.S. Tax Treaties for more information. Generally, nonresident aliens of the United States who aren’t residents of Canada can’t deduct gambling losses.

- IRS.gov/forms

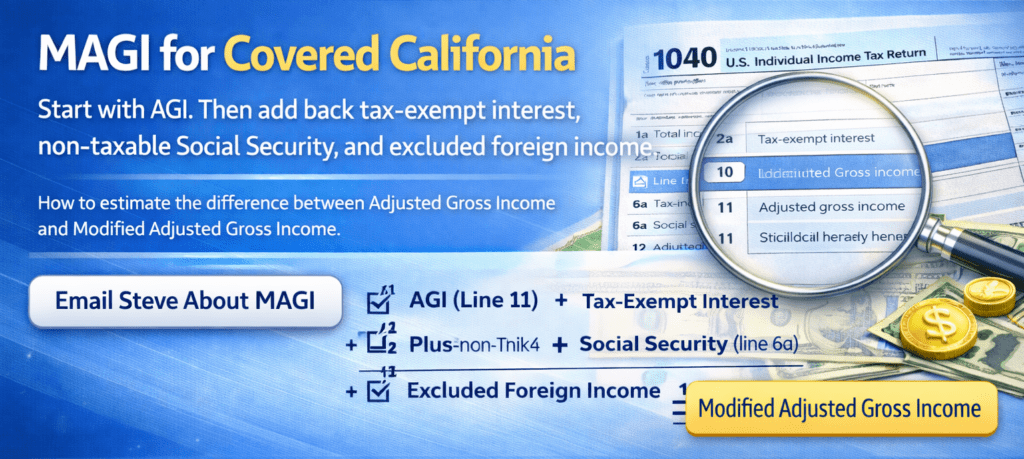

How to #Estimate MAGI Income for Covered CA?

- From the AGI above, Add back in any

- foreign income,

- Social Security benefits and

- interest that are tax-exempt.

- View our main webpage on estimating income

Professional gamblers’ decade long streak of being able to deduct a net loss from gambling as a trade or business was ended this year by P.L. 115-97, known as the Tax Cuts and Jobs Act of 2017 (TCJA)

a gambler engaged in the trade or business of gambling (“professional gambler”) can net gambling winnings against losses and business expenses on Schedule C, Profit or Loss From Business.

This article from the Journal of Tax Accountancy.com is a little too complex for me to summarize, especially since Covered CA prohibits agents giving tax advice. Pleases click the preceding link and read it yourself.

Do you have Professional Gambler Status?

How does one make certain that he or she would be considered a professional gambler in the eyes of the IRS? You can’t be absolutely sure, but if you gamble regularly, frequently, with continuity and with the intent of earning and with the intent of earning your living from the winnings, then you are off to a good start.

As a professional gambler, you can deduct your expenses such as traveling, tokes to dealers, etc. You’re actually allowed to deduct these even if the income received and reported is from an illegal gambling operation (but you may not deduct illegal payments you made for gambling expenses). You can also deduct the amount of your losses, but the losses can’t exceed the net of your gross winnings minus expenses. (Note that it is arguable that the losses can’t exceed your gross winnings without regard to your expenses)

IRS Tax Court Summary Opinion January 4, 2005:

This case upholds the accepted rules for professional gambler status as laid out by the US Supreme Court in Commissioner v Groetzinger, supra at 33 – that if a taxpayer “devotes his full-time activity to gambling, and it is his intended livelihood source, it would seem that basic concepts of fairness * * * demand that his activity be regarded as a trade or business.”

This ruling is the same ruling that allows daytraders to deduct their expenses “above the line” rather than as an itemized deduction.

summary of major similarities and differences:

- security traders, filing with trader status, deduct expenses on Schedule C.

- gamblers, filing with professional gambler status, deduct expenses on Schedule C, consequently, a professional gambler does not have to itemize deductions to deduct gaming expenses.

- security traders without trader status (i.e. investor status) deduct expenses on Schedule A subject to a reduction of 2% of Adjusted Gross Income (AGI).

- gamblers without professional gambler status (a/k/a non-professional gamblers or casual gamblers) deduct expenses on Schedule A, subject to a reduction of 2% of Adjusted Gross Income (AGI).

- security traders, filing with trader status, deduct trading losses either on Schedule D, limited to offsetting capital gains plus an additional $3,000 or on form 4797 where there are no limitations as to the amount deducted.

- gamblers, filing with professional gambler status, deduct gaming losses on Schedule C, limited to reported winnings, net of expenses. i.e. the bottom line may not go below zero. Consequently, a professional gambler does not have to itemize deductions to deduct gaming losses.

(Note #1 that using Schedule C is not necessarily written in stone. There is some discussion and flexibility as to exactly where to deduct gaming losses on the individual income tax return)

(Note #2 that It is arguable that the losses can’t exceed your gross winnings without regard to your expenses via a literal reading of IRS Code §165(d) and IRS Regulation §1.165-10 )

(Note #3 some tax advisors 1.proclaim that losses in excess of winnings are deductible against other non-gambling income. The Courts have consistently knocked this theory down, assessing negligence penalties against those who attempt to get away with it. http://www.ustaxcourt.gov/) - security traders without trader status (i.e. investor status) deduct trading losses on Schedule D, limited to offsetting capital gains plus an additional $3,000.

- gamblers without professional gambler status (a/k/a non-professional gamblers or casual gamblers) deduct gaming losses on Schedule A, limited to reported gaming winnings but these are not subject to a reduction of 2% of Adjusted Gross Income (AGI) as are operating expenses.

- security traders with or without trader status, generally are not subject to self-employment taxes on their trading gains.

- gamblers without professional gambler status are not subject to self-employment taxes on their gaming winnings.

- gamblers with professional gambler status are subject to self-employment taxes on their net gaming winnings.professional gambler status.com

- gamblers anonymous.org

#Covered CA Certified Agent

No extra charge for complementary assistance

Covered CA (& Medi Cal) - Calculate - #Countable Sources of MAGI Income

Short Summary

![]()

Claiming Gambling Income and Losses

Covered California MAGI Income Tax Return

Calculate your Covered CA MAGI Income

- Take #Line8b 11 or your projected IRS 1040 Adjusted Gross income for the upcoming year then add

- line 2a tax exempt interest

- 6a Social Security &

- 8 (Foreign Income)

-

-

-

IMPORTANT!!!

The upcoming year – the future for what you tell Covered CA!

Sure, many people think it’s the past as Covered CA may ask for last years paperwork, but that’s BS! You might have to give back all the subsidies when you file Subsidy Reconciliation form #8962!

- Visit our MAIN webpage on MAGI Income

-

-

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

The total gambling winnings are included in your adjusted gross income (AGI) for the year, and your losses are taken as an itemized deduction and limited to an amount not exceeding your reported winnings.

So, whether or not you itemize your deductions and deduct your gambling losses, the full amount of the gambling winnings is included in your AGI, and your [M] AGI is included in your household income, which is used to determine the amount of premium tax credit (PTC) to which you are entitled. IRS.Gov Topic 419

Gambling Deduction Videos