Can Business Owners and Employees Have Different Health Plans?

California small group employers can often offer more than one health plan — but the employer contribution, eligibility rules, and waiting periods must be handled carefully.

- California small employers may offer more than one health plan. However, all eligible employees within the same bona fide employment class should receive a consistent offer of coverage and a consistently applied employer-contribution formula. Different treatment based solely on ownership, executive status or compensation may raise carrier, tax and nondiscrimination concerns and should be reviewed before enrollment.

- Can employees choose different health plans?

- Yes, many California small group arrangements allow an employer to offer more than one plan option. For example, the business might offer a lower-cost HMO, a richer PPO, or several metal-level choices. The key is that the offer should be structured fairly and consistently for eligible employees. Start by comparing available plans on the California small group instant quote page.

- Can the owner pick a better plan?

- The owner may be able to enroll in a richer plan if that plan is part of the employer’s available plan choices. But that is different from quietly giving the owner a special contribution or special eligibility rule. If the employer contributes more for one person or class, review the rules on management carve-outs and ACA §2716 nondiscrimination issues.

- Employer contribution: same rule for similarly situated people

- The employer usually needs a consistent contribution formula for employees who are similarly situated. That might be a percentage of premium, a fixed dollar contribution, or another carrier-approved method. The point is not that everyone must enroll in the same plan. The point is that the contribution method should not unfairly favor owners, officers, or highly compensated employees unless the arrangement has been reviewed properly.

- Related pages:

- Employee payroll deductions and Section 125

- If employees pay part of their premium through payroll deduction, the employer should usually have a Section 125 Premium Only Plan. Section 125 is the cafeteria-plan rule that allows employees to choose between taxable cash compensation and certain nontaxable benefits. You can also read the IRS explanation of cafeteria plans.

- Employer-paid premiums and Section 106

- Employer contributions for accident or health coverage are generally addressed under IRC §106. The IRS explains that employer-provided accident and health benefits can generally be excluded from an employee’s wages. See the IRS Publication 15-B Employer’s Tax Guide to Fringe Benefits.

- Waiting periods should be consistent

- Waiting periods should be handled consistently for eligible employees. Federal ACA rules generally prohibit waiting periods longer than 90 days. See our page on California small group waiting periods and the Department of Labor’s page on the 90-day waiting period limitation.

- What if the owner wants individual coverage instead?

- If the owner or employees want individual health insurance instead of group coverage, be careful. Employers generally should not casually reimburse individual health insurance premiums without using a compliant arrangement. See our pages on Section 105 reimbursement plans, ICHRA, QSEHRA, and reimbursing individual health insurance.

- An ICHRA can sometimes allow different treatment by permitted employee classes, such as full-time, part-time, seasonal, or geographic classes. HealthCare.gov explains that ICHRA classes may be based on job-based criteria, including full-time, part-time, or seasonal status. See the official HealthCare.gov ICHRA explanation.

- Practical examples

- Example 1: The employer offers both an HMO and PPO. The owner chooses the PPO, and some employees choose the HMO. This may be fine if both plans are genuinely available according to the carrier’s rules and the employer contribution formula is consistent.

- Example 2: The owner receives 100% employer-paid PPO coverage, while rank-and-file employees receive only a small contribution toward an HMO. That may create nondiscrimination or carve-out concerns. Review management carve-out rules before doing this.

- Example 3: The employer wants to reimburse only the owner’s individual policy. That is not a simple payroll shortcut. Review reimbursing individual health insurance, ICHRA, and QSEHRA.

- How to pick multiple plans

- You can compare California small group options on our small group instant proposal page. You may also review carrier-specific rules through our California small group carrier pages.

Choose the plans you want to offer from the quote engine and carrier materials.

Contribution method matters.

Waiting periods should be selected carefully.

Frequently asked questions

- Can a business owner have a better health plan than employees?

- Sometimes, yes, if the better plan is part of the employer’s available plan choices and the contribution rules are applied properly. But giving the owner a special contribution or special eligibility rule can create problems.

- Can employees choose between HMO and PPO plans?

- Often yes. Many employers offer more than one plan so employees can choose between lower premium, narrower network options and higher premium, broader network options.

- Can executives receive a larger employer contribution?

- That may raise management carve-out and nondiscrimination questions. Review management carve-outs before setting up special executive-only benefits.

- Do all employees need the same waiting period?

- The safest approach is to use a consistent waiting period for eligible employees. Also remember the federal 90-day maximum waiting-period rule.

- Can the employer reimburse individual health insurance instead?

- Where should I start?

- Start with the California small group quote engine.

- Then set a Zoom meeting if you want help comparing plans, contribution strategies, and carrier rules.

- Compare Small Group Plans

- Set a Zoom Meeting

- Participation & Contribution Rules

.

.

Child & Sibling Pages

- Annual Open Enrollment – SEP no Participation Requirements

- EmployER Definition – Small Group Health Insurance

- Employer Group Association Plans California

- How to offer different Plans to owners employees

- Management Carve Outs – §2716 – Similarly Situated

- Proof in business document required

- Proof of Ownership for Small Business

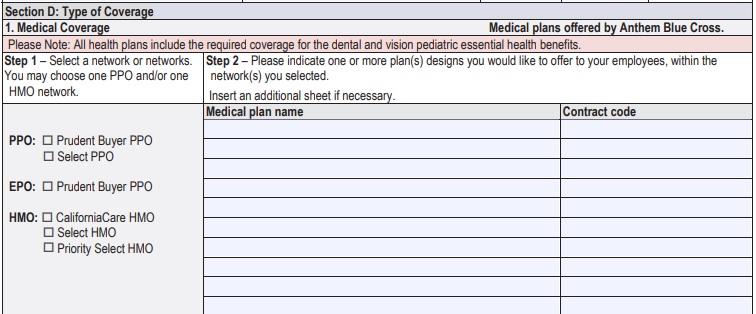

How does it work if you want to #offer more than ONE Health plan?

Let's take a look at the Employer Application

|

Choose what plans you want to offer from our Quote Engine and/or the Anthem/Blue Cross Guides

|

|

Contribution must be the same for all similarly situated Employee's and Owners

|

|

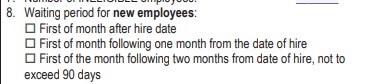

Waiting periods to enroll must be the same for everyone.

Our webpage on waiting periods |

We can also double check links to other pages on our website, cited below, Blue Cross Administrator Manual and their underwriting rules