Over Age 65 and Not Eligible for Free Medicare Part A?

Over age 65 does not automatically disqualify you from Covered California premium assistance. The key issue is whether you are eligible for premium-free Medicare Part A.

If you are not eligible for premium-free Medicare Part A, you may still qualify for Covered California subsidies. If you are eligible for premium-free Medicare Part A, you generally cannot receive Covered California premium tax credits, even if you choose not to enroll. Scroll down for more details and video explanation.

Start here — this determines everything:

- Are you eligible for premium-free Medicare Part A?

- Yes: You generally cannot receive Covered California premium tax credits.

- No: You may still qualify for Covered California subsidies.

- Are you paying for Medicare Part A, do you lack enough work credits, or did you delay enrollment?

- You may still have Covered California options.

If you are not eligible for premium-free Medicare Part A, you may also want to review how income is calculated for subsidies on the

Covered California MAGI income page.

- Federal Rule – Medicare & the Health Insurance Marketplace (Publication 11694)

- Covered California Medicare Fact Sheet

- Compare Plans & Check Subsidy Options

More details and citations below.

Details, Rules, and Official References

Eligibility for Covered California premium assistance after age 65 depends primarily on whether you are eligible for premium-free Medicare Part A. Age alone does not disqualify you from receiving subsidies.

In general, individuals who must pay a premium for Medicare Part A may still qualify for Covered California premium tax credits and cost-sharing reductions, as long as they are not enrolled in Medicare Part A.

However, if you are eligible for premium-free Medicare Part A, federal law treats that as minimum essential coverage, and you typically are not eligible for Covered California subsidies, even if you choose not to enroll.

- A person may qualify for Covered California subsidies if they are over age 65 and not eligible for premium-free Medicare Part A.

- If a person enrolls in Medicare Part A, they generally become ineligible for Covered California premium tax credits.

- Delaying Medicare enrollment may result in late enrollment penalties, depending on the situation.

- Some individuals qualify for Medicare but must pay a premium because of limited work history or other factors.

These rules can become complex depending on income, immigration status, work history, and other coverage options. You can also review how Medi-Cal income limits compare to Covered California, especially if your income is close to the threshold.

Official Sources and References

- Medicare & the Health Insurance Marketplace – Publication 11694

- Covered California Medicare Fact Sheet

- IRS Publication 974 – Premium Tax Credit Rules

- Medi-Cal Program Overview (DHCS)

When to Look Closer at Your Situation

- Paying for Medicare Part A instead of receiving it free

- Not having enough work credits for premium-free Part A

- Delayed Medicare enrollment

- Recently turning age 65 and evaluating options

- Transitioning between Covered California and Medicare

Because small differences in eligibility can significantly affect your options and costs, it is often helpful to review your situation before making a decision.

If you want help reviewing your situation, you can compare plans or email Steve at [email protected].

|

|

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

Introduction

If someone is over 65 and not eligible for no premium Part A Hospital Medicare They can get Covered CA subsidies!!!

|

Video about Covered CA – if no Premium Free Part A – jump to 2:30 |

|

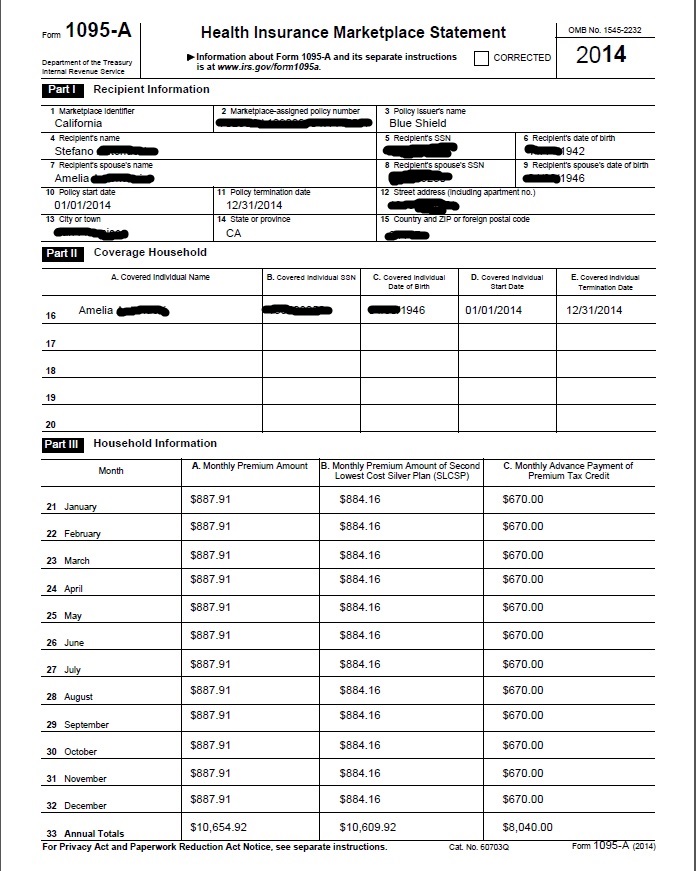

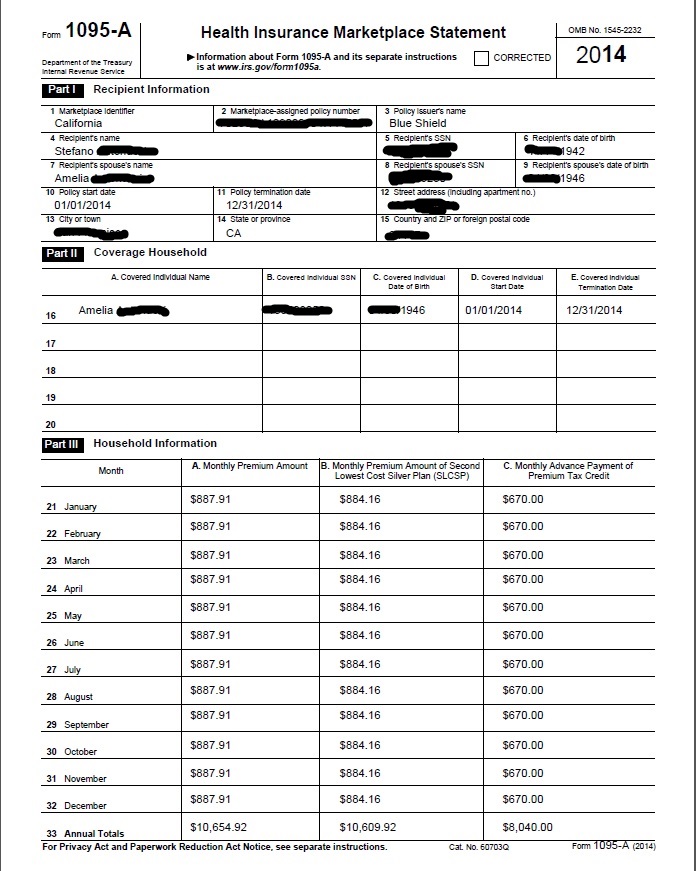

1095 Showing Tax Subsidy

Covered California Subsidies for someone over 65

if ineligible for Free Medicare Part A Hospitalization

Proofs & References

That one can get subsidies even if over 65

- If someone qualifies for Medicare but has to pay a premium for Part A and does not enroll in Medicare Part A, they may be eligible for a Covered California health plan. Depending on a consumer’s income, they may be eligible for premium assistance and cost-sharing subsidies for the Covered California health plan. Covered CA – Medicare Info

- Code of Federal Regulations 1.36B-2 Eligibility for Premium Tax Credit Is not eligible for minimum essential coverage [Can’t get Medicare!]

- 26 USC §36B Refundable Credit for Coverage under a QHP Qualified Health Plan

- Eligibility for Minimum Essential Coverage for Purposes of the Premium Tax Credit Notice 2013-41 Latest Info

- CFR §1.37-1 General rules for the credit for the elderly. * §1.37-2 Credit for individuals age 65 or over.

- FAQ’s Medicare & Covered CA CMS.gov

- IRC §5000 A Minimum Essential Coverage

You cannot buy additional coverage through #Covered California

if you have premium-free Medicare Part A Hospital

Medicare complies with Health Care Reform, so you do NOT need to get a an Individual policy or a subsidized one from Covered CA. It fact, it's illegal for anyone to sell you a policy! Kaiser Health News * Covered CA Medicare Fact Sheet * Medicare.Gov Medicare & Market Place #11694 * CMS.Gov FAQ Medicare & Marketplace * HealthCare.Gov when - how to change from Covered CA to Medicare * Social Security §1882 * Health Care.Gov

NOTE: This information also applies to people younger than 65 whose benefits begin the first month they receive disability benefits because they have Amyotrophic Lateral Sclerosis (ALS), better known as Lou Gehrig’s Disease, and to people younger than 65 who have Medicare because of a disability and are receiving SSDI Social Security Disability Insurance.

There are a lot of ands, if or buts in this complex issue. Please refer to the source material below. There are some exceptions, but they are very complex. Don't even think of getting a 1/2 correct answer over the phone. If you have to pay for Part A Hospital, then are options, like subsided Covered CA Plans. Email us [email protected]

Video about Covered CA – if no Premium Free Part A – jump to 2:30 Medicare & the Marketplace (Covered CA

- Medicare Publication # 11694 Medicare & Covered CA

- Covered CA Medicare Fact Sheet

- Medicare vs Covered CA - Publication 11694Selling Covered CA Plans To Medicare Beneficiaries Will Be Illegal Kff.org

- InsureMeKevin.com

- Publication 02179 How Medicare works with other Insurance Our webpage

(3)(A)

(i) It is unlawful for a person to sell or issue to an individual entitled [no premium] to benefits under part A or enrolled under part B of this title (including an individual electing a Medicare+Choice plan [MAPD] under section 1851)—

(I) a health insurance policy with knowledge that the policy duplicates health benefits to which the individual is otherwise entitled under this title or title XIX,

(II) in the case of an individual not electing a Medicare+Choice plan, [aka MAPD Medicare Advantage] a medicare supplemental policy with knowledge that the individual is entitled to benefits under another medicare supplemental policy or in the case of an individual electing a Medicare+Choice plan, a medicare supplemental policy with knowledge that the policy duplicates health benefits to which the individual is otherwise entitled under the Medicare+Choice plan or under another medicare supplemental policy, or

(III) a health insurance policy (other than a medicare supplemental policy) with knowledge that the policy duplicates health benefits to which the individual is otherwise entitled, other than benefits to which the individual is entitled under a requirement of State or Federal law.

(ii) Whoever violates clause (i) shall be fined under title 18, United States Code, or imprisoned not more than 5 years, or both, and, in addition to or in lieu of such a criminal penalty, is subject to a civil money penalty of not to exceed $25,000 (or $15,000 in the case of a person other than the issuer of the policy) for each such prohibited act. Sec. 1882. [42 U.S.C. 1395ss]

Our webpages that touch on this Issue:

- VIDEO What is APTC Advance Premium Tax Credit

- Interactive Tax Assistant (ITA)

- Am I eligible to claim the Premium Tax Credit?

Tax #Estimators

- turbo tax.com - FREE for simple returns

- H & R Block

- E file.com

- Estimate the Subsidy for Health Insurance, benefits, premiums, etc.

- 8962 ONLINE Calculator

- Our webpage on 8962 Premium Tax Credit Reconciliation

- Tax Form Calculator.com

- e tax.com

- Marriage Higher or Lower Taxes?

ACA What You Need To Know #5187 (2020) is the most recent

- VITA - Volunteers to help you

- Publication 17 - Your Federal Income tax

- Health Savings Accounts HSA our webpage

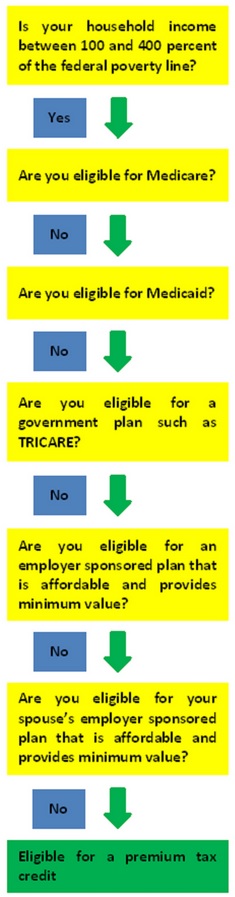

Moulder Law – Subsidy Flow Chart over 65

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()