Health Net 8 Questions

To see if your plan is Grandfathered

Enlarge or view pdf for a sharper image

- UnitedHealthcare Video on Grandfathering

- Decision Flow Chart Do I keep the Grandfathered Plan or get a new ACA Plan? Health Net 2014 *

What are Grandfathered PLans?

Grandfathering Exemption?

Grandfathering Introduction

Grandfathering means that if your coverage was in place on 9.23.2010, when the Affordable Care Act was enacted, President Obama promised that you could keep it, see also USA Today as long as there were no “major” changes to your coverage.

However, UNCovered CA, did NOT honor that! Covered CA forced insurers to cancel policies!

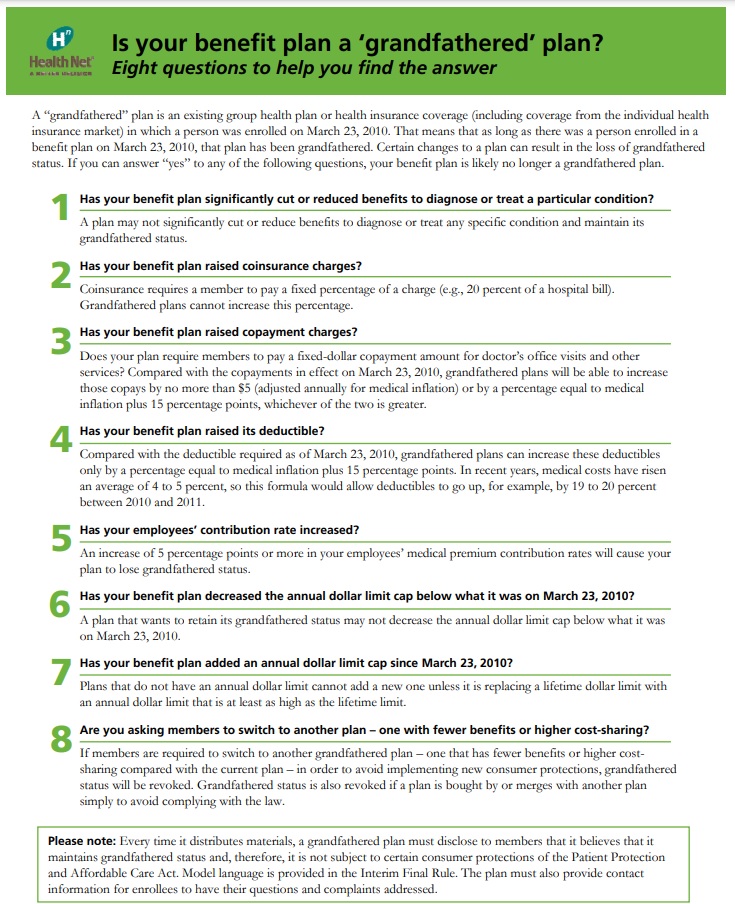

8 questions to determine Grandfathered status

Check out the Health Net Flyer below, where it explains that if health plans significantly raise co-payments or deductibles, or if they significantly reduce benefits – for example, if they stop covering treatment for a disease like HIV/AIDS or cystic fibrosis – they’ll lose their grandfathered status and their customers will get the same full set of consumer protections as new plans. (healthreform.gov)

Steve Shorr

Website Video #Introduction

Change Plans

Advantage of a Grandfathered Plan

The primary one is that in 2014 the rating for the non grandfathered plans (ACA Obamacare) will be subject to additional taxes and fees. These could total upwards of 50% higher than a comparable grandfathered plans. Since the rates will be so much higher than the grandfathered plans we feel it would be a good idea to keep those plans until at least we see how the rates look like in 2014.Excerpt of Email Rec’d 1.25.2013 from a Major Insurance Company

However, the

Government says NO

in Q & A on their website at healthreform.gov

-

Individual Grandfathered plans are “closed” plans, no longer sold to new applicants. It is possible that premiums or costs may increase because new, healthy applicants are no longer being added to the closed “pool” of members. Premium changes for all plans, whether “closed” or open to new sales, are driven by several factors. These include increased consumer demand for services, rising prescription drug costs, advances in medical technology, and benefits and/or taxes required by state and federal legislation. Blue Cross Flyer

- make some changes to the benefits their plans offer,

- raise premiums or change employee cost-sharing to keep pace with health costs within some limits, and

- continue to enroll new employees and their families.

The bottom line is that under the Affordable Care Act, if you like your doctor and plan, you can keep them, subject to “Narrow Lists.” But if you aren’t satisfied with your insurance options today, the Affordable Care Act provides for better, more affordable health care choices through new consumer protections. (healthreform.gov)

Wikipedia on Health Reform & Grandfathering

No more RAF – Rating Adjustment Factor §10753.14 in Employer Group Plans

Insurance Companies NOT offering Plans?

Thus the End of Grand Fathering?

- Blue Cross is dropping 79 plans.

- California Health Line 10.3.2014 reports Blue Cross, Kaiser and various other insurers are not renewing pre ACA plans, that don’t have the 10 essential benefits and other provisions of ACA.

- Reasoning – Washington Post?

FAQ’s

- Which will be less expensive Grandfathered or Not?

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

General Client Resources & Links

Research & Technical Links

- Fact Sheet on Regulation

- Health Care Reform Provisions Summary Chart

- Model Notice for Grand Fathered Plans

- Group Health Plans CAN change Insurer’s without affecting Grand Father Status. (HHS.gov Amendment)

- SB 1446 Grandmothering for Group Plans

- Whatever happened to grandfathered #rates & premiums our our policy. Seems that every time the policy renews it’s a lesser coverage?

- Grandfathered plans has nothing to do with stopping rate increases or changes in benefits at policy renewal. Grandfathering means that the plan can stay basically the same as it was, if you had the plan before February 2010 when the ACA was passed.

- pp-aca-obamacare-introduction/

- Insurance rates, premiums, benefits, deductibles are basically a function of the Medical Loss Ratio medical-loss-ratio-mrl/

- Which means that the Insurance Companies are mandated to pay out 80 cents in claims on every dollar they take in, in premium. So, the more they pay in claims, the more they have to charge in premiums.

- Surcharges? When an Insurance Company goes bankrupt

- The surcharge is for Grandfather plans only and will be a reoccurring charge until recovery of the 2017 Penn Treaty is completed.The 2017 Penn Treaty Class B Assessment levied by California Life & Health Insurance Guarantee Association, also known as The Guarantee Association.

Per our IFP renewal information, the surcharge is to not exceed more than 0.02 per dollar of premium. The surcharge is a result of Penn Treaty Network American Insurance Company and their long term care insurance companies that went insolvent back on March 1, 2017. The Guarantee Association imposed an assessment on all other California licensed life & health insurance companies for the funds necessary to provide protection, with Blue Shield of California being one of the companies. The Guarantee Association has allowed the assessed companies to charge members the surcharge to recoup the Penn Treaty assessment.

If more information is needed about the assessment, Penn Treaty and the Guarantee Association, please go to califega.org or call (916) 631-1581, or lastly, the California Department of Insurance, Consumer Communications Bureau at (800) 927-4357.

Reference number: 203150011167

khn.org/whack-insurers-policyholders

- The surcharge is for Grandfather plans only and will be a reoccurring charge until recovery of the 2017 Penn Treaty is completed.The 2017 Penn Treaty Class B Assessment levied by California Life & Health Insurance Guarantee Association, also known as The Guarantee Association.

Anthem Blue Cross Grandfathered PLans being #discontinued!

- grandfathered clients enrolled on the Basic 2500 contract codes R418 & R419 that their plan was discontinued as of 6/1/24 and that they needed to choose an ACA medical plan.

- Anthem Blue Cross will be discontinuing the grandfathered plans below, the rest of their plans are good. The last day of coverage for these plans is December 31, 2022.

- Contract Code Plan description

- 1518 Basic 1000

- 7900 Basic 1000

PE25 Basic 1000

PE26 Basic 1000

- 7900 Basic 1000

- Z165 SmartSense 2500 Full RX

- Z166 SmartSense 2500 Full RX email dated 6.23.2022 *

- Anthem Blue Cross will let you know your options sample letter for selecting a new plan during

- 1518 Basic 1000

Blue Cross doesn't have any downgrade options - that is, the ability to just select a different grandfathered plan. You'll have to

Affected members will still receive rate action notifications through the end of the year.

- Old Brochures

- Our main webpage for Blue Cross Individual