2026 MAGI Medi-Cal Income Limits in California

MAGI Medi-Cal is the income-based form of Medi-Cal used for most California adults under age 65, parents, children and pregnant individuals.

This page explains:

- The 2026 MAGI Medi-Cal income limits.

- How household size and income are counted.

- Why Medi-Cal may review monthly income rather than simply using last year’s tax return.

- What happens when parents qualify for Covered California but their children qualify for Medi-Cal.

- How to apply and report changes.

This page focuses on MAGI income rules. Different rules may apply to people who are age 65 or older, have Medicare, have a disability, need long-term care or qualify through another non-MAGI Medi-Cal program.

Source: California Department of Health Care Services — 2026 Federal Poverty Level amounts

Quick Answer: Who May Qualify for MAGI Medi-Cal?

- Most adults ages 19 through 64: Household MAGI generally must be no more than 138% of the Federal Poverty Level.

- Children: Children may qualify at substantially higher income levels than their parents—generally through 266% of the Federal Poverty Level.

- Pregnant individuals: Different and higher income limits may apply, including full-scope Medi-Cal through 213% of the Federal Poverty Level.

- Income period: Medi-Cal often begins with current monthly income, but other methods may be used when income changes or fluctuates.

- Assets: MAGI Medi-Cal generally does not impose an asset or property limit.

- Enrollment: You may apply for Medi-Cal throughout the year. Medi-Cal does not have the same annual open-enrollment restriction as private individual health insurance.

Important: Income is only one part of eligibility. The county must also review household composition and other eligibility requirements.

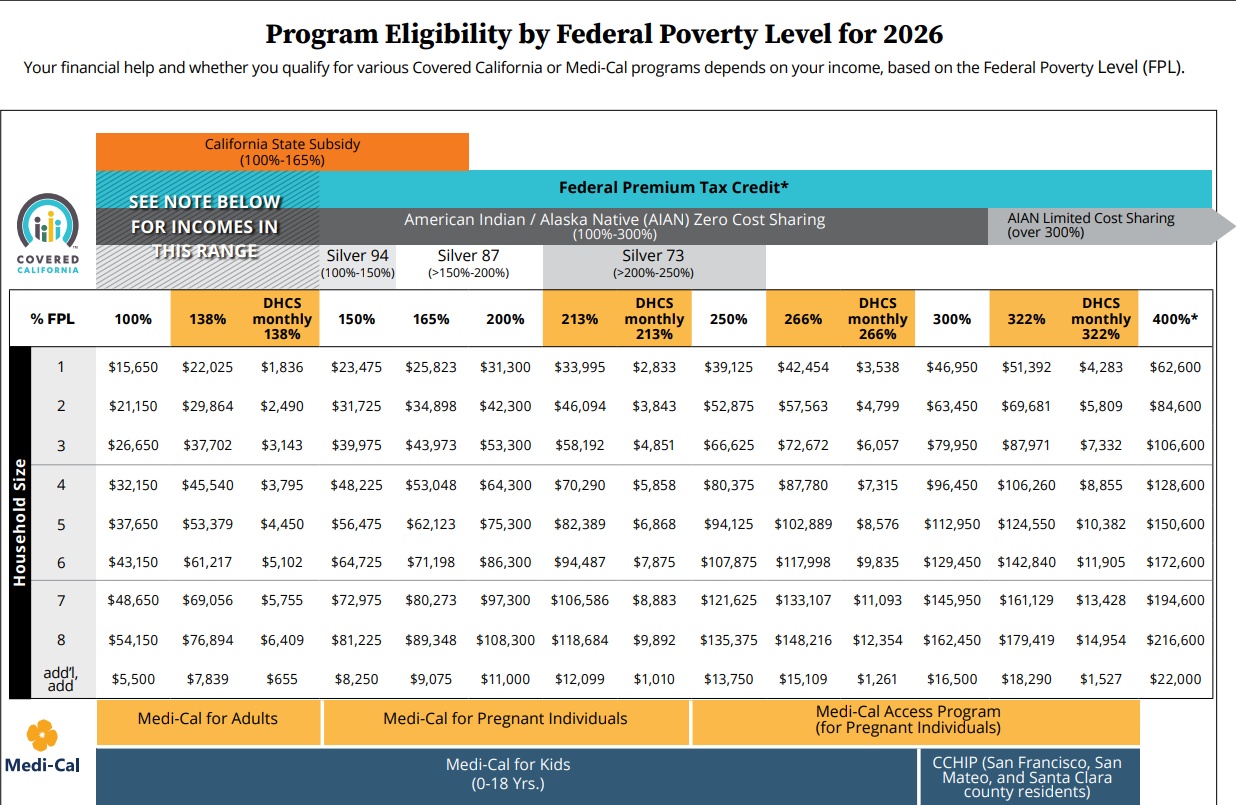

2026 MAGI Medi-Cal Income Limits for Most Adults

The following figures represent 138% of the 2026 Federal Poverty Level, the general MAGI Medi-Cal income limit for most adults ages 19 through 64.

| Household Size | Monthly Limit | Annual Limit |

|---|---|---|

| 1 | $1,836 | $22,025 |

| 2 | $2,490 | $29,864 |

| 3 | $3,143 | $37,702 |

| 4 | $3,795 | $45,540 |

| 5 | $4,450 | $53,379 |

| 6 | $5,102 | $61,217 |

| 7 | $5,755 | $69,056 |

| 8 | $6,409 | $76,894 |

| Each additional person | Add $655 | Add $7,839 |

These figures are guidelines—not a final eligibility determination. Medi-Cal uses countable MAGI rather than take-home pay, and monthly and annual calculations are not always interchangeable.

What Do MAGI and Household Size Mean?

MAGI means Modified Adjusted Gross Income. It is not necessarily the same as your paycheck, take-home pay or total deposits into your bank account.

For health-coverage purposes, MAGI generally begins with the adjusted gross income shown on a federal tax return and adds certain income that may not appear in adjusted gross income, including:

- Tax-exempt interest.

- Nontaxable Social Security benefits.

- Excluded foreign earned income.

Household size is generally based on federal tax-filing relationships—not simply the number of people living at an address.

A household commonly includes:

- The person filing the tax return.

- A spouse when filing jointly.

- People expected to be claimed as tax dependents.

Special household rules apply to some children, married couples, tax dependents and people who do not file a tax return.

- Our Detailed Page on MAGI, Household Size and Countable Income

- Official DHCS MAGI Household-Size Flowchart

- IRS Publication 501 , Dependents, Standard Deduction, and Filing Information

Does Medi-Cal Use Monthly or Annual Income?

Current monthly income is normally the starting point for a MAGI Medi-Cal determination. This generally means income received during the month of:

- An application.

- A reported change in circumstances.

- An annual renewal.

However, income is not always as simple as one paycheck or one calendar month. California also has methods for people whose income is seasonal, irregular, recently changed or reasonably expected to fluctuate.

Depending on the circumstances, the eligibility system may consider:

- Current Monthly Income: Income being received during the current month.

- Reasonably Projected Annual Income: Expected income over a future 12-month period when income is reasonably expected to change.

- State Calendar Annual Income: Income received or expected during the calendar year in certain situations.

A low-income or zero-income month can be important, but it does not automatically guarantee Medi-Cal eligibility. Report both current income and reasonably expected future income accurately so the county can apply the correct method.

Can Parents Have Covered California While Their Children Have Medi-Cal?

Yes. One family may be divided between different health-coverage programs because children can qualify for Medi-Cal at higher household income levels than adults.

A common result is:

- The parents enroll in a Covered California private health plan.

- The parents receive premium assistance based on household income.

- The children enroll in Medi-Cal.

This is sometimes called a mixed-program family. The family can generally submit one application, and the eligibility system evaluates each person separately.

Declining a child’s Medi-Cal does not normally make the child eligible for Covered California financial assistance. A child who qualifies for Medi-Cal may generally be added to a separate private plan only at the full, unsubsidized premium.

Does MAGI Medi-Cal Have an Asset Limit?

MAGI Medi-Cal generally does not have an asset or property limit. Eligibility is primarily determined using household composition and countable MAGI income.

Separate asset rules may apply to certain non-MAGI Medi-Cal programs involving people who:

- Are age 65 or older.

- Have a physical, mental or developmental disability.

- Live in a nursing home or need long-term-care Medi-Cal.

- Do not qualify under the federal tax-based MAGI rules.

Those programs may also use different income deductions, household rules and eligibility limits. Therefore, the 138% MAGI income table on this page should not be used to decide eligibility for every Medi-Cal program.

How to Apply for Medi-Cal or Report a Change

You may apply for Medi-Cal at any time of the year. Applications may be submitted online, through your county or through a health-coverage application that evaluates family members for both Medi-Cal and Covered California.

Ways to apply include:

- BenefitsCal: Apply for and manage Medi-Cal and other California benefits online.

- Your county Medi-Cal office: Apply or obtain assistance by phone, mail or in person.

- Covered California: Useful when one or more family members may need a private Covered California plan while others may qualify for Medi-Cal.

Tell Medi-Cal within 10 days when an important change occurs, including a change in:

- Income or employment.

- Home or mailing address.

- Household size.

- Pregnancy.

- Marriage or separation.

- Tax-filing status or tax dependents.

- Other health coverage.

Official myMedi-Cal Guide

The California Department of Health Care Services publishes myMedi-Cal: How to Get the Health Care You Need.

The guide includes information about:

- How to apply for Medi-Cal.

- MAGI and non-MAGI eligibility.

- Using Medi-Cal benefits.

- Medi-Cal managed-care plans.

- Reporting household changes.

- Annual renewals.

- Appeal and hearing rights.

The guide is available in English, Spanish and numerous additional languages.

Related Medi-Cal and Covered California Information

Use the following pages for more detailed information about your situation:

- Covered California Income, MAGI and Federal Poverty Level Chart

- How to Report Income and Household Changes to Medi-Cal

- Medi-Cal for People Who Are Aged, Blind, Disabled or Have Medicare

- Medi-Cal Share of Cost and Ways to Reduce It

- Complete Medi-Cal Eligibility and Program Information

Need Covered California coverage? We can help California residents compare private individual and family plans and apply for available premium assistance at no additional charge.

Medi-Cal eligibility determinations are made by the county and the California Department of Health Care Services. Steve Shorr Insurance is not a Medi-Cal eligibility office and does not receive compensation for Medi-Cal enrollment.

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

Child & Sibling Pages

- Aged and Disabled Federal Poverty Level Program

- Share of Cost – Eliminate with Dental Insurance Premiums

- SSI – Supplemental Security Benefits – Automatic Medi Cal

- Denti Cal Medi Cal Dental & Vision

- Dual Coverage? Medi Cal?

- MAGI Medi Cal Income Limits

- Medi Cal Report Changes

- Medi Cal Contact Help

- Medi Cal Resources Asset Limits

Program Eligibility by Federal Poverty Level

The chart below compares income guidelines for several Medi-Cal, children’s health and maternity.

Important:

- Not every program shown in the chart uses MAGI income-counting rules.

- Different age, disability, pregnancy, Medicare and household requirements may apply.

- Some non-MAGI programs may also apply asset limits or allow income deductions that are not reflected in a simple FPL chart.

- The chart provides a starting point—not a final eligibility determination.

Official 2026 Sources: