Covered California Metal Levels – Quick Guide

A simple overview of Bronze, Silver, Gold, and Platinum, plus Enhanced Silver plans for people who qualify.

| Plan | Best For | Primary Care | Deductible | Max Out-of-Pocket |

|---|---|---|---|---|

| Bronze 60 | Lower premium, higher costs when you use care | $60 | $5,800 individual | $9,800 individual |

| Silver 70 | Middle-ground option | $50 | $5,200 individual | $9,800 individual |

| Silver 73 / 87 / 94 | Qualified lower-income households | $15 / $5 | $1,400 / none | $3,350 / $1,400 |

|

||||

| Gold 80 | Regular use of care, labs, prescriptions | $40 | No medical deductible | $9,200 individual |

| Platinum 90 | Highest premium, richest routine benefits | $15 | No medical deductible | $5,000 individual |

General rule: Bronze usually costs less each month but more when you use care. Gold and Platinum usually cost more each month but less when you need treatment. Enhanced Silver can be one of the best values if you qualify.

View the Full Official Covered California 2026 Metal Level Benefits Table

| Get Instant Quotes | Email Steve |

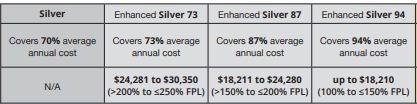

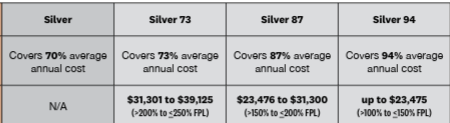

Silver 87, 94 & 73 Enhanced Silver Benefits

Cost-sharing CSR – subsidies

- Cost-sharing – Enhanced Silver subsidies in the Silver 87, 94 & 73 will reduce your out-of-pocket cost, including your

- by lowering co-pays & deductibles vs the Plain Silver 70. See chart below.

- Enhanced Silver – CSR cost-sharing reductions – subsidies are only available if you enroll in a silver-level plan. Once Covered California determines Get instant quotes here! that you are eligible for cost-sharing subsidies, you will be able to enroll in a Silver Plan with CSR, based on your income level. You can’t just say you want to buy Silver 97, it’s based on FPL Federal Poverty Level. Get instant quotes & Poverty Level Calculation here!

- Scroll down for our Metal Level Chart

Resources & Links

- page 174 of Western Poverty Law for explanation of Cost Sharing Reductions

- If you’re a techy here’s the full code on Cost Sharing Reductions

- Right to change plans when your Silver Level changes – significant income change

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

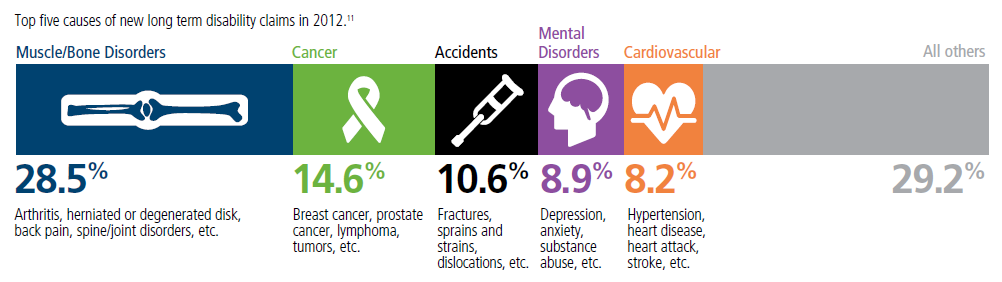

Top 5 - 10 causes of Long Term Disability Claims

Lower back disorders ♦ Depression ♦ Coronary heart disease, arthritis and pulmonary diseases (Met Life) ♦ Disability Can Happen ♦ CDC Statistics

Our webpage on Disability Payments - Insurance

Get Disability Quotes for Parents, Caretakers & Wage Earners

Major Supreme Court #Cases on ACA/Obamacare

- Mandate Penalty UPHELD as a TAX NFIB vs Sebelius

- Our old webpage on Archive.org

- Wikipedia

- Texas vs USA California v Texas Supreme Court rules in favor of Obamacare

- King vs Burwell APTC Subsidies Upheld in Federal Exchange – Covered California

FAQ’s “Enhanced Silver – Cost Sharing Reductions”

- The plan says 87% cost share reduction, does that mean the plan covers 87% of the medical costs?

- 87% is the actuarial value The actuarial value of a health insurance policy is the percentage of the total covered expenses that the plan covers, on average for a typical population. [Age & Zip Code] For example, a plan with a 70% actuarial value means that consumers would on average pay 30% of the cost of health care expenses through features like deductibles and coinsurance. The amount that each enrollee pays will vary substantially by the amount of services they use.

- To find out what the actual expenses are for your plan, click where it says “plan details” and you’ll see the detail on your deductibles, co pays, etc. If you look at the chart on the top of this page, it will show Silver 87 with a $15 office co-pay, $1,400 deductible and the maximum out of pocket of $2,700. Click here for definitions of deductible and OOP Out of Pocket maximum.

- Whenever you have a change, you are required to report it to Covered CA within 30 days.

- Once you have a qualifying event, there is 60 days to change your plan. Covered CA Site…

- negotiated rate. here’s a premium & subsidy calculator.

Child & Sibling Pages

- Enhanced Silver 94, 87, 73 Cost-sharing reductions House v Price

- Grand Fathered Plans What does that mean?

- HSA Health Savings Accounts

- OOP -Out of Pocket Maximum – Participating or Not? Deductibles & Co- Pays

- Provider Finder Quotit