Group & Individual Insurance Premiums – ACA Rating Areas Factors AB 1083

Premium Rating Criteria under ACA/ObamaCare

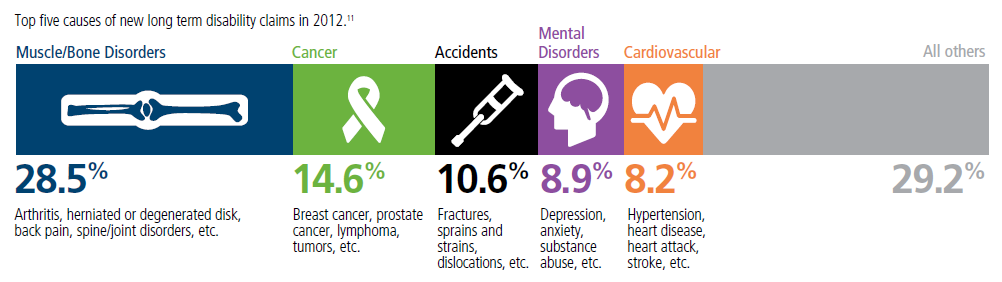

Top 5 - 10 causes of Long Term Disability Claims

Lower back disorders ♦ Depression ♦ Coronary heart disease, arthritis and pulmonary diseases (Met Life) ♦ Disability Can Happen ♦ CDC Statistics

Click here to visit our website on

Health Care Reform has

very few legal Rating – Premium Factors

Under Health Care Reform in California you can only be charged a different premium for the following factors:

- Age

- shall not vary by more than three to one premium difference for adults.

- 19 Zip Code (Geographic Regions) View Chart and if your coverage is for

- Individual or family CMS.gov * Commonwealth Fund * 42 U.S. Code § 300gg – Fair health insurance premiums * Insurance Code §10753.14.

New Advantages

- (a)No more charge for claims experience – §10753.16. RAF Factors

- nor medical questions asked – No Pre X Clause

- CFR §146.121 Prohibiting discrimination against participants and beneficiaries based on a health factor.

- Nor genetics §146.122 Additional requirements prohibiting discrimination based on genetic information.

- Contrast this with “Wellness” Discounts of 30% and 50% to stop smoking.

- No extra charge for using an Agent or Broker

- 12 additional reasons to get your coverage thru Steve Shorr Insurance

- There was no extra charge for our services prior to ACA/Obamacare either.

- More on Rate Regulation & Filings with CA Dept. of Insurance

19 Geographic Regions

Rating Zip Codes, Counties – #Geographic Region

Graphic Map of NEW Rating Regions

10753.14 (2) (A) Geographic region. [Zip Code]

The geographic regions for purposes of rating shall be the following:

(xv) Region 15 shall consist of the ZIP Codes in Los Angeles County starting with 906 to 912, inclusive, 915, 917, 918, and 935.

(xvi) Region 16 shall consist of the ZIP Codes in Los Angeles County other than those identified in clause (xv).

(xvii) Region 17 shall consist of the Counties of San Bernardino and Riverside.

(xviii) Region 18 shall consist of the County of Orange.

(xix) Region 19 shall consist of the County of San Diego.

(i) Region 1 shall consist of the Counties of Alpine, Del Norte, Siskiyou, Modoc, Lassen, Shasta, Trinity, Humboldt, Tehama, Plumas, Nevada, Sierra, Mendocino, Lake, Butte, Glenn, Sutter, Yuba, Colusa, Amador, Calaveras, and Tuolumne.

(ii) Region 2 shall consist of the Counties of Napa, Sonoma, Solano, and Marin.

(iii) Region 3 shall consist of the Counties of Sacramento, Placer, El Dorado, and Yolo.

(iv) Region 4 shall consist of the County of San Francisco.

(v) Region 5 shall consist of the County of Contra Costa.

(vi) Region 6 shall consist of the County of Alameda.

(vii) Region 7 shall consist of the County of Santa Clara.

(viii) Region 8 shall consist of the County of San Mateo.

(ix) Region 9 shall consist of the Counties of Santa Cruz, Monterey, and San Benito.

(x) Region 10 shall consist of the Counties of San Joaquin, Stanislaus, Merced, Mariposa, and Tulare.

(xi) Region 11 shall consist of the Counties of Madera, Fresno, and Kings.

(xii) Region 12 shall consist of the Counties of San Luis Obispo, Santa Barbara, and Ventura.

(xiii) Region 13 shall consist of the Counties of Mono, Inyo, and Imperial.

(xiv) Region 14 shall consist of the County of Kern.

[Calif. Insurance Commissioner 2.20.2013 Proposal to divide into 18 Regions Los Angeles Times]

[Employer zip code, determines rates, however, residential zip by each employee is still needed on census to establish network availability, per Heide S email dated 9.9.2015]

(B) No later than June 1, 2017, the department, in collaboration with the Exchange and the Department of Managed Health Care, shall review the geographic rating regions specified in this paragraph and the impacts of those regions on the health care coverage market in California, and make a report to the appropriate policy committees of the Legislature.

- Service of Process physical address is legally required:

- limited liability company (LLC) or a corporation, or as a limited partnership or a limited liability partnership, you will need to have a registered agent address in the state in which you’ve registered to do business. A registered agent is simply someone that your business has designated to receive important papers related to the business, such as government documents and notices related to lawsuits (also known as “service of process”).

- the address of your registered agent, you will need to appoint a third party to serve as your registered agent. The third party can be an individual, such as an attorney, or it can be a company whose business offers registered agent services. legal zoom

- Prohibition on using post office box.

- It is current procurement and financial assistance practice to not allow post office boxes, other commercial mailbox providers, or short term (less than one year lease) virtual office locations to be recognized as an entity’s physical address.

- Entities without a long-term physical address (mostly sole proprietors) are required to identify the location their business documents (including tax documents) are held as their physical address. federal spending

- Medicare Fee Schedule Geographic Area https://www.law.cornell.edu/uscode/text/42/1395w-4

-

- geographical region – demarcated area of the Earth vocabulary.com

- merriam-webster.com/dictionary/region

What justification is there for Insurance Companies to charge different rates in different Counties or to even have 19 different rating area’s in CA?

The ACA Health Reform allows insurers to use geographic rating factors to adjust premiums to reflect variations in medical costs across rating areas attributable to such factors as differences in labor and other operating costs, the relative strength of their network/provider agreements in a given area, and/or cost shifts associated with high Medicare or Medicaid enrollment and lower payments from these sources. The benefit of geographic rating is that it provides insurers with marketing flexibility and can help ensure that insurance purchasers in low cost areas benefit from the efficiencies of their local health care system. It may also encourage more insurers to offer plans in high cost areas that they would otherwise avoid if these costs could only be recouped across their entire coverage area. On the other hand, geographic rating may also undermine the incentives for health plans to encourage efficiency among health care providers in high-cost areas.

The cost of delivering care varies dramatically from one area to another, and insurers often vary their rates by county or by ZIP code using the employer’s business address in the small group market, or the applicant’s home address in the individual market. Safe harbors for geography have been set for each state, depending on the variation in medical costs within the state, and range from no variation in the District of Columbia to 1.9:1 in Florida

Insurers must submit data that demonstrates a correlation between case characteristics (e.g., geographic area) and

increased medical claims costs

NIH.gov * NAIC.org *

risk screening – insurers could avoid entering counties that have a higher share of unhealthy consumers.

market segmentation – segment a market and avoid competition

entry cost hypothesis – meeting network adequacy standards and establishing a competitive network could be significant for insurers. This will be especially true if an insurer does not have legacy provider networks.

risk selection wpmucdn.com *

Geographic rating areas are units made up of metropolitan statistical areas (MSAs), counties or three-digit zip codes, which are used by insurance carriers to price premiums. An MSA is a geographical region with a relatively high population center and close economic ties throughout the area.

“Variations in health insurance premiums across regions arise due to variations in the cost of health care across regions,” said Insurance Commissioner Marguerite Salazar in a news release. “These variations are not new, but the transparency brought by the Affordable Care Act is new.” CMS.org *

Bibliography, Links & Resources

CA Residency Guidelines #FTB1031 2023

- See our webpage on lawful presence & public charge

- A California resident is one who is in California for other than a temporary or transitory purpose; or Domiciled in California, but outside California for a temporary or transitory purpose. (ftb.ca.gov).

- Amount of time you spend in California versus amount of time you spend outside California;

- Location of your spouse and children;

- Location of your principal residence;

- Where your driver's license was issued;

- Where your vehicles are registered;

- Where you maintain your professional licenses;

- Where you are registered to vote;

- Location of the banks where you maintain accounts;

- Location of your doctors, dentists, accountants, and attorneys;

- Location of the church, temple or mosque, professional associations, or social and country clubs of which you are a member;

- Location of your real property and investments;

- Permanence of your work assignments in California; and

- Location of your social ties.

-

In using these factors, it is the strength of your ties and closest connections not just the number of ties, that determines your residency (ftb.ca.gov/)

- Sanjiv Gupta CPA reviews rules related to residency in California

Dependent Children

ACA Rate Rule for Dependent Children

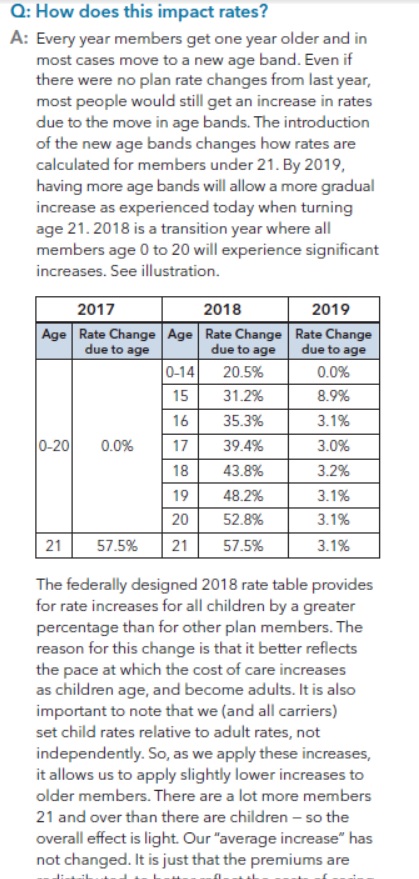

The Final Rule directs all health plan issuers of non-grandfathered small group and individual plan coverage (on and off the Exchanges) to revise the member level rating age bands used for individuals 0-20 years of age from using one age band to now create 7 age bands.

The first age band cover ages 0-14, then single year age bands cover 15, 16, 17, 18, 19 and 20.

This change will align with utilization of services while smoothing rate increases over time. Kaiser

FAQ’s Child Age Rating Band Changes

- frequently asked questions (PDF).

- Guidance 12.16.2016

- More on Small Group Rating Factors

- Blue Cross – Sample Amendment

Health Coverage #Guide

Art Gallagher

Health Care Reform FAQ's

Understanding Health Reform

***********************************

Compliance #Assistance Guide from DOL.Gov Health Benefits under Federal Law

- Health Care Reform Explained Kaiser Foundation Cartoon VIDEO

- Choosing a Health Plan for Your Small Business VIDEO DOL.gov

- ACA Quick Reference Guide California Small Group Employers Revision 2020 Word & Brown

- kff.org/health-policy-101/

HISTORICAL

Simple explanation of AB 1672 (1993) & Rating Adjustment Factors (RAF) CHCF Site

Our business doesn’t have a physical address. How do we determine what region we are in?

We’ve answered that question above