Narrow Networks - Myths & Facts

Chat GBT Summary of Narrow Networks and Inaccurate Directories

February 2026

I’ve had this page up for years… Not that many people are asking questions about narrow networks, like back when Covered CA ACA/Obamacare started in 2014.

Here’s where things stand as of February 16, 2026 for narrow networks + “ghost networks” + inaccurate directories in California—broken out by Covered California (ACA/QHPs) and Medicare Advantage (MA), with clickable citations.

Covered California and ACA plan directories in California

What’s improved (real structural change)

- Covered California moved to a centralized provider-directory data source (IHA “Symphony”) that is now live. The goal is to reduce the classic “plan says Dr. X is in-network, but office says no” problem by using a statewide “single source” directory platform while shoppers compare plans. (Integrated Healthcare Association)

- Instant Quotes, enrollment and comparing plan directories Quotit.com

What’s still the reality on the ground

- California already has statewide “directory accuracy” law + standards (SB 137), including requirements for plans/insurers to maintain accurate directories and update online information (and uniform standards issued by regulators). Those rules have been in place for years, but inaccuracies have persisted—especially for specialties, mental health, and “accepting new patients” status. (dmhc.ca.gov)

- Regulatory activity is ongoing, suggesting the state still considers this an active problem. For example, DMHC issued a 2025 “Provider Directory Annual Filing” instruction tied to Health & Safety Code 1367.27, which is basically the state tightening the reporting/attestation loop. (dmhc.ca.gov)

- News reporting in late 2025 still described consumers getting stranded by directory errors and “ghost networks,” with the observation that penalties/enforcement have been limited and some rules were still being completed/operationalized. (CalMatters) July 2024 Cal Matters.org

Where California may be headed next (if enacted/implemented)

- AB 280 (2025–26 session) is designed to add measurable accuracy benchmarks (e.g., ratcheting up toward 95% accuracy by July 1, 2029) and attach clearer penalties for missing those benchmarks—an explicit acknowledgment that “rules exist” hasn’t been enough. (LegiScan)

Bottom line for Covered California today:

Even with SB 137 on the books and a major infrastructure improvement (Symphony now live), California is still treating directory accuracy as an active compliance and access issue—especially because directories are the “front door” for narrow-network shopping. (Integrated Healthcare Association)

Medicare Advantage provider directory accuracy (and narrow networks)

What’s happening right now at the federal/CMS level

- CMS is integrating MA provider directory data into Medicare Plan Finder for Contract Year 2026, specifically because beneficiaries historically had to bounce between plan sites to figure out networks. CMS frames this as a “critical knowledge gap” it’s trying to close. (CMS)

- CMS also published implementation guidance for how MA plans must submit directory data for Plan Finder (tech specs), and the rulemaking pipeline continued into January 2026 (CMS-10906 on Regulations.gov). (CMS)

- CMS finalized a CY 2026 rule (separate from the broader MA/Part D rulemaking) focused on format/availability of MA provider directory data for Medicare Plan Finder—i.e., CMS is standardizing the “plumbing” for directories rather than relying only on each plan’s website presentation. (CMS)

The uncomfortable truth: accuracy problems are still very real

- CMS’s own “secret shopper / directory review” work has historically found very high error rates (wrong location, wrong phone, not accepting new patients, etc.). One CMS industry report found 48.74% of locations had at least one inaccuracy (that report is older, but it’s widely cited as evidence of the scale of the problem). (CMS)

- And importantly: even CMS’s newer Medicare.gov directory experience has had publicized accuracy issues. Investigations during October 2025 open enrollment described conflicting “in-network/out-of-network” results and other inconsistencies; CMS acknowledged errors and said it was working fixes (and pointed to special enrollment remedies for people misled). (The Washington Post)

Bottom line for Medicare Advantage today:

CMS is actively trying to centralize/standardize MA directory data inside Medicare Plan Finder (CY 2026), but the ecosystem still struggles with accuracy—especially when narrow networks make “is this doctor really in-network, at this location, taking new patients” the make-or-break question. (CMS)

Practical “field” advice (what actually works when directories lie)

- Verify provider status two ways: plan directory and the provider office’s billing/contracting staff (and ask “which TIN / which location address” is contracted—many mismatches are location/TIN-level).

- Google name of doctor or hospital and say “insurance accepted.” See our webpage on the major hospitals and IPA in South Bay Los Angeles.

- Screenshot/save the directory result the day they enrolled (useful for appeals/complaints).

- Escalate to regulators when access fails: DMHC (most managed-care plans) or CDI (some PPO/insurance products), depending on which regulator oversees the product. (SB 137 standards apply across regulators.) (dmhc.ca.gov)

- For MA, also use Medicare’s complaint/grievance pathways and document that the plan directory/Plan Finder information was a deciding factor (especially if CMS offers a special enrollment remedy tied to misinformation). (The Washington Post)

Quotit - #Find Provider - ALL Companies

Get Quotes:

How to see MD list when using our quote engine

- Which plan is right for you?

- Covered CA Provider VIDEO - How to use it Steve's video

- Can’t Find A Doctor? Look at Low Star Rated Docs InsureMeKevin.com

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

Why narrow Networks?

#Contact Us - Ask Questions - Get More Information - Schedule a Zoom Meeting

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

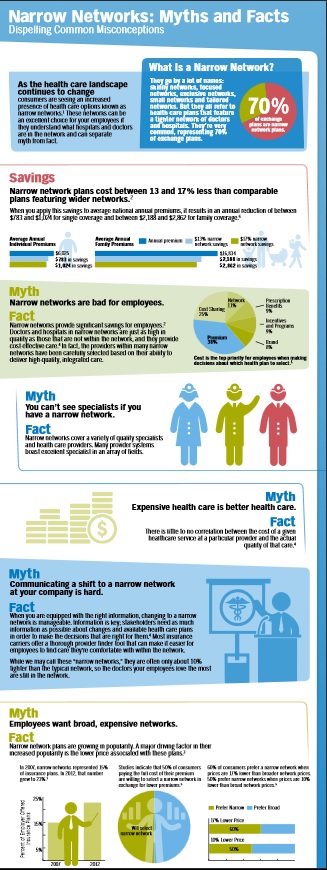

Narrow Networks keep premiums down

How do doctors get paid?

Imagine going to your favorite restaurant. You are greeted at the door by the hostess, who seats you and takes your drink order. You order through your favorite waiter, Andrew, who recommends the special of the day: prime rib with a dinner salad and a chocolate torte for dessert.

Soon after, the food is brought out and it is delicious! You have time to enjoy your food. You then receive the bill and pay for your meal, returning to your home satisfied, all your dining needs met. Let’s say, for simplicity’s sake, you paid $75 for this meal: $50 for the steak, $10 for the salad and $15 for the dessert.

A change then occurs in the restaurant industry. A new form of eating out has been adopted. Your favorite restaurant has now contracted with over 30 different ”restaurant insurance companies.” Read the rest of the article

**************************************

Aetna illegally secured contracts with Pennsylvania’s Medicaid program by misrepresenting the number of pediatric providers in its network, according to a federal whistleblower lawsuit unsealed Tuesday.

One Union keeps costs and deductibles down, by giving up access to some of their city’s best known, and most expensive, hospitals. Workers not only kept their insurance premiums under control, they saved so much money that housekeepers saw their hourly pay increase from $16.98 to $23.60 in five years, a 39% jump.

The price problem has been most acute in communities with dominant hospital systems, studies show.

In California, for example, hospitals that were part of Sutter Health and Dignity Health, the state’s largest hospital systems, increased prices almost 50% faster than other hospitals in the state between 2004 and 2013, researchers found.

Massachusetts General and Brigham and Women’s charged two or in some cases even three times as much as other academic medical centers in Boston.

For example, a hip replacement at the Beth Israel Deaconess Medical Center — which, like Massachusetts General and Brigham and Women’s is a teaching hospital for Harvard Medical School — cost $28,359, according to federal data.

Massachusetts General charged $55,362 for the same procedure, and Brigham and Women’s charged $65,073. LA Times 12.17.2019 *

- Out-of-network health care doesn’t have to mean out-of-control cost

- 2017 Directories are still lousy

- Patients scrambling for Network MD’s due to flawed directories Penny Gentieu did not intend to phone 308 physicians in six different insurance plans when she started shopping for 2017 health coverage. CA Health Line 12.13.2016

- How narrow are the new lists (See the Provider Finder Page) under Health Care Reform – Covered CA?

- Is there a difference in the Covered CA list vs if one buys coverage outside – direct from the Insurance Company or an Agent (at no additional charge)?

- Officially no, due to mirroring requirements

- Why do so many MD’s say they accept direct business from an Insurance Company – but not Covered CA?

- If your MD is not on the list and of course no one was told… is that a Material Provision and would allow one to change to a better list, with a new company under the rules for Special Enrollment?

- SB 137 effective 1.1.2016 hopefully will make things easier.

- Does this lawsuit filed against Blue Cross and Does 1-50 show a material violation?

- What about 2015 lists? Will the be better? ♦ LA Times 9.29.2014 ♦ No 10.17.2014 CA Health Line ♦ InsureMeKevin Health Net PPO EPO Comparison ♦ CA Healthline 12.8.2015 – Fewer PCP’s and Clients having trouble locating them

- Are consumers showing a preference for narrow networks to save $$$?

- Out of Network Costs…vary by Insurance Company Blog InsureMeKevin.com

- CMS Rule 9929 F leaves Network Adequacy to the States not the Feds. Modern Health Care 4.13.2017 * CMS.Gov 4.13.2017 * Amazonaws.com

- View LATEST news articles on Narrow Provider Lists

- View actual Evidence of Coverage page 14 and check out the definitions and explanations of the role of the PCP Primary Care Physician and IPA Independent Practise Assoc.

“If you’re competing on price and you can’t vary co-payment structure or deductibles, the only thing you can do is try and keep your networks as affordable as possible,” which means eliminating providers unwilling or unable to meet insurers’ cost expectations. (CA Healthline.org 2.17.2015)

Here’s the letter from a client of ours that prompted today’s 4.18.2014 update to this website:

Dear Steve I was planning to get in touch with you because as sson as I had coverage it sems that I started to need my insurance… I found a great general doctor and all went smooth with him. My test and Xray had a charge and I paid it but my leg specialist first said that he was participating with Blue Shield but later when he discovered that it was Covered California he said he was not and I had to pay his visit and the MRI ( $500) A second specialist that I contacted to check on my lungs upon suggestion of my GD, called afer I made the reservation to say the same thing and I had to find an other one, Does Blue Shield have two different PPO one for general public ad one for CC?

***Here’s a screen shot from Blue Shield’s provider search. It shows that the MD list for PPO and EPO is the same for 2014 Health Reform Compliant Plans in and out of Covered CA. More Explanation.I dont’ thing it is fair. What do you know about it? Amelia – See laws & Regulations on “code” page.

Blue Cross Explanation of Provider Networks – PDF on this website Benefit Snapshot – Brochure In an email dated 4.22.2014 I rec’d confirmation that networks are the same on and off the exchange.

I think it’s a real shame that the “authoritative” answers seem to be Facebook. Nothing with actual proof or citations.

#MAPD Medicare Advantage

Narrow Networks

Senate bill addresses inaccurate Medicare Advantage directories AMA.org

MAPD customers, are usually restricted to getting care from doctors and organizations included in their plan’s provider network. Most MAPD plans are HMOs, or health maintenance organizations, that have what are called narrow networks – relatively small groups of providers located only in the plan’s home market. PBS *

Health Care Dive.com Narrow Networks can cut costs

One can’t easily or accurately observe plan networks. The surest way to know if a physician is covered by a plan is to scrutinize the contracts between plans and providers. But these are closely held by the organizations, so are unavailable to researchers. Plans do publish provider directories, but there are no validated, comprehensive, historical archives of directories. Those that are available are not uniformly machine readable and are known to contain errors and omissions, such as listing physicians not in networks or failing to list those that are.

“secret shoppers” were able to schedule an appointment with a selected in-network provider in fewer than 30% of cases

on average, Medicare Advantage networks included 46% of all physicians in a county. There is considerable variation by specialty, with psychiatrists being least the likely to be included in plan networks (on average, a plan covered care by 23% of psychiatrists in a county) and ophthalmologists the most likely (59%). 16% of Medicare Advantage plans in 20 counties covered care at less than 30% of hospitals.) As for costs, the October study found that broader-network plans tend to charge higher premiums than narrow-network plans. Jama Network.com *

narrow network plans, insurers that offer these work with a smaller pool of doctors, hospitals, and treatment centers, who agree to a lower price for services with the expectation that they will get greater patient volume.

narrow networks are not strictly defined, the plans often have 25 percent or less of the physicians in the local area participating. The most restrictive plans have less than 10 percent of local doctors signed on.

One in 10 insured Americans say that within the past two years, they have been surprised to find that a doctor, lab, or facility that they thought was in their provider’s network actually wasn’t,

Identifying a plan as a narrow network can be very difficult.

Outdated directories are a problem

Even if you do everything you can to stay in network, sometimes needing out-of-network care is unavoidable, so you’ll want to take a close look at your out-of-network coverage. Some insurers will cover a portion of the cost of seeing a doctor who doesn’t take your insurance.

But an increasing number of plans have no out-of-network coverage at all. Consumer Reports *

KFF.org MAPD Robust Networks???

Urban.org Why MAPD plans have narrow networks

#Covered CA Certified Agent

No extra charge for complementary assistance

- Get Instant Health, Dental & Vision Quotes, Subsidy Calculation & Enroll

- Appoint us as your broker

- Get Instant Health Quotes, Subsidy Calculation & Enroll

Reliable Provider Directories - Study

Narrow Networks

ACA/Obamacare

- Montage of Obama saying Americans can keep their doctors current healthcare plan VIDEO

- many insurance companies offering policies through the healthcare law are quietly offering "narrow networks" to save money. VIDEO

- CBS News December 2014 Narrow Networks cause outrage VIDEO

- Provider Finder ALL Companies

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

Links, News & Resources

- Even Well-Intended Laws Can’t Protect Us From Inaccurate Provider Directories

- Covered CA – Marketplace plans deny in-network claims more than you might think

- Can’t Find A Doctor? Look at Low Star Rated Docs

- ‘A market failure’: High prices at Monterey County hospitals drive away many insured Californians

Mirrored Plans

Covered CA vs Direct must “mirror” each other

See prior versions of this page on Archive.org

- What are #Mirror ed Plans

- Mirrored means that plan benefits and provider networks must be exactly the same direct and with what is offered in Covered CA. (SB 639 * Cahba.com * Crosby * 2.7.2014 Email to Cedars Sinai *

- That is Any Insurance Company that offers a product on Covered California must also offer a “mirror” plan with identical benefits and networks. The ID cards of all consumers who purchased plans through Covered California display the logos of their respective health plan AND the logo of Covered California. The ID cards of patients who purchased mirror products do not display the Covered CA logo ACPonline.org * Exception to the rule on rates for Silver Plans, “Silver Loading” due to Supreme Court decision.

- More liberal Provider Networks are a big advantage to Grandfathered Plans

- Mirrored means that plan benefits and provider networks must be exactly the same direct and with what is offered in Covered CA. (SB 639 * Cahba.com * Crosby * 2.7.2014 Email to Cedars Sinai *

- Is there any difference in #practise the Provider Directory for the same plan be it direct with the Insurance Company or Covered CA?

- Briefly, NO!!! That’s what the law says. See above on Mirrored Plans.

Provider Network Access Standards

California Code of Regulations 10 CCR § 2240 et seq.

See also – Special Enrollment Periods

Department of Insurance Investigation – errors in lists

“It boggles my mind that insurers can’t keep their list up to date,” “There is no excuse for how messy it is. Health insurers are engaged in false advertising.” Fines coming… CA Health Line 2.10.2017 * Blog Insure Me Kevin.com 2.11.2017 DMHC fined: