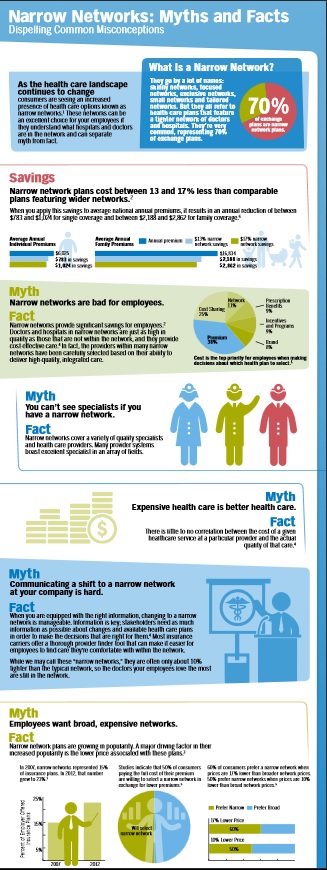

Narrow Networks to save money?

Narrow Networks - Myths & Facts

Click icon below to enlarge

Why narrow Networks?

Narrow Networks keep premiums down

How do doctors get paid?

Imagine going to your favorite restaurant. You are greeted at the door by the hostess, who seats you and takes your drink order. You order through your favorite waiter, Andrew, who recommends the special of the day: prime rib with a dinner salad and a chocolate torte for dessert.

Soon after, the food is brought out and it is delicious! You have time to enjoy your food. You then receive the bill and pay for your meal, returning to your home satisfied, all your dining needs met. Let’s say, for simplicity’s sake, you paid $75 for this meal: $50 for the steak, $10 for the salad and $15 for the dessert.

A change then occurs in the restaurant industry. A new form of eating out has been adopted. Your favorite restaurant has now contracted with over 30 different ”restaurant insurance companies.” Read the rest of the article

**************************************

Aetna illegally secured contracts with Pennsylvania’s Medicaid program by misrepresenting the number of pediatric providers in its network, according to a federal whistleblower lawsuit unsealed Tuesday.

One Union keeps costs and deductibles down, by giving up access to some of their city’s best known, and most expensive, hospitals. Workers not only kept their insurance premiums under control, they saved so much money that housekeepers saw their hourly pay increase from $16.98 to $23.60 in five years, a 39% jump.

The price problem has been most acute in communities with dominant hospital systems, studies show.

In California, for example, hospitals that were part of Sutter Health and Dignity Health, the state’s largest hospital systems, increased prices almost 50% faster than other hospitals in the state between 2004 and 2013, researchers found.

Massachusetts General and Brigham and Women’s charged two or in some cases even three times as much as other academic medical centers in Boston.

For example, a hip replacement at the Beth Israel Deaconess Medical Center — which, like Massachusetts General and Brigham and Women’s is a teaching hospital for Harvard Medical School — cost $28,359, according to federal data.

Massachusetts General charged $55,362 for the same procedure, and Brigham and Women’s charged $65,073. LA Times 12.17.2019 *

- Out-of-network health care doesn’t have to mean out-of-control cost

- 2017 Directories are still lousy

- Patients scrambling for Network MD’s due to flawed directories Penny Gentieu did not intend to phone 308 physicians in six different insurance plans when she started shopping for 2017 health coverage. CA Health Line 12.13.2016

- How narrow are the new lists (See the Provider Finder Page) under Health Care Reform – Covered CA?

- Is there a difference in the Covered CA list vs if one buys coverage outside – direct from the Insurance Company or an Agent (at no additional charge)?

- Officially no, due to mirroring requirements

- Why do so many MD’s say they accept direct business from an Insurance Company – but not Covered CA?

- If your MD is not on the list and of course no one was told… is that a Material Provision and would allow one to change to a better list, with a new company under the rules for Special Enrollment?

- SB 137 effective 1.1.2016 hopefully will make things easier.

- Does this lawsuit filed against Blue Cross and Does 1-50 show a material violation?

- What about 2015 lists? Will the be better? ♦ LA Times 9.29.2014 ♦ No 10.17.2014 CA Health Line ♦ InsureMeKevin Health Net PPO EPO Comparison ♦ CA Healthline 12.8.2015 – Fewer PCP’s and Clients having trouble locating them

- Are consumers showing a preference for narrow networks to save $$$?

- Out of Network Costs…vary by Insurance Company Blog InsureMeKevin.com

- CMS Rule 9929 F leaves Network Adequacy to the States not the Feds. Modern Health Care 4.13.2017 * CMS.Gov 4.13.2017 * Amazonaws.com

- View LATEST news articles on Narrow Provider Lists

- View actual Evidence of Coverage page 14 and check out the definitions and explanations of the role of the PCP Primary Care Physician and IPA Independent Practise Assoc.

“If you’re competing on price and you can’t vary co-payment structure or deductibles, the only thing you can do is try and keep your networks as affordable as possible,” which means eliminating providers unwilling or unable to meet insurers’ cost expectations. (CA Healthline.org 2.17.2015)

Here’s the letter from a client of ours that prompted today’s 4.18.2014 update to this website:

Dear Steve I was planning to get in touch with you because as sson as I had coverage it sems that I started to need my insurance… I found a great general doctor and all went smooth with him. My test and Xray had a charge and I paid it but my leg specialist first said that he was participating with Blue Shield but later when he discovered that it was Covered California he said he was not and I had to pay his visit and the MRI ( $500) A second specialist that I contacted to check on my lungs upon suggestion of my GD, called afer I made the reservation to say the same thing and I had to find an other one, Does Blue Shield have two different PPO one for general public ad one for CC?

***Here’s a screen shot from Blue Shield’s provider search. It shows that the MD list for PPO and EPO is the same for 2014 Health Reform Compliant Plans in and out of Covered CA. More Explanation.I dont’ thing it is fair. What do you know about it? Amelia – See laws & Regulations on “code” page.

Blue Cross Explanation of Provider Networks – PDF on this website Benefit Snapshot – Brochure In an email dated 4.22.2014 I rec’d confirmation that networks are the same on and off the exchange.

I think it’s a real shame that the “authoritative” answers seem to be Facebook. Nothing with actual proof or citations.

#MAPD Medicare Advantage

Narrow Networks

Senate bill addresses inaccurate Medicare Advantage directories AMA.org

MAPD customers, are usually restricted to getting care from doctors and organizations included in their plan’s provider network. Most MAPD plans are HMOs, or health maintenance organizations, that have what are called narrow networks – relatively small groups of providers located only in the plan’s home market. PBS *

Health Care Dive.com Narrow Networks can cut costs

One can’t easily or accurately observe plan networks. The surest way to know if a physician is covered by a plan is to scrutinize the contracts between plans and providers. But these are closely held by the organizations, so are unavailable to researchers. Plans do publish provider directories, but there are no validated, comprehensive, historical archives of directories. Those that are available are not uniformly machine readable and are known to contain errors and omissions, such as listing physicians not in networks or failing to list those that are.

“secret shoppers” were able to schedule an appointment with a selected in-network provider in fewer than 30% of cases

on average, Medicare Advantage networks included 46% of all physicians in a county. There is considerable variation by specialty, with psychiatrists being least the likely to be included in plan networks (on average, a plan covered care by 23% of psychiatrists in a county) and ophthalmologists the most likely (59%). 16% of Medicare Advantage plans in 20 counties covered care at less than 30% of hospitals.) As for costs, the October study found that broader-network plans tend to charge higher premiums than narrow-network plans. Jama Network.com *

narrow network plans, insurers that offer these work with a smaller pool of doctors, hospitals, and treatment centers, who agree to a lower price for services with the expectation that they will get greater patient volume.

narrow networks are not strictly defined, the plans often have 25 percent or less of the physicians in the local area participating. The most restrictive plans have less than 10 percent of local doctors signed on.

One in 10 insured Americans say that within the past two years, they have been surprised to find that a doctor, lab, or facility that they thought was in their provider’s network actually wasn’t,

Identifying a plan as a narrow network can be very difficult.

Outdated directories are a problem

Even if you do everything you can to stay in network, sometimes needing out-of-network care is unavoidable, so you’ll want to take a close look at your out-of-network coverage. Some insurers will cover a portion of the cost of seeing a doctor who doesn’t take your insurance.

But an increasing number of plans have no out-of-network coverage at all. Consumer Reports *

KFF.org MAPD Robust Networks???

Urban.org Why MAPD plans have narrow networks

Blue Cross Removes UC Hospitals From EPO Health Plans

UC Davis Medical Center, UC San Francisco Medical Center and Children’s Hospital, along with Benioff Children’s Hospital in Oakland are no longer part of their Pathway EPO network as January 1, 2022 Learn More – Insure Me Kevin.com

![]()

#Covered CA Certified Agent

No extra charge for complementary assistance

- Appoint us as your broker

- Get Instant Health Quotes, Subsidy Calculation & Enroll

- Videos on how great agents are

Reliable Provider Directories - Study

Narrow Networks

ACA/Obamacare

- Montage of Obama saying Americans can keep their doctors current healthcare plan VIDEO

- many insurance companies offering policies through the healthcare law are quietly offering "narrow networks" to save money. VIDEO

- CBS News December 2014 Narrow Networks cause outrage VIDEO

- Provider Finder ALL Companies

All our plans are Guaranteed Issue with No Pre X Clause

Quote & Subsidy #Calculation

There is No charge for our complementary services

Watch our 10 minute VIDEO

that explains everything about getting a quote

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- Get more detail on the Individual & Family Carriers available in CA

Links, News & Resources

- Even Well-Intended Laws Can’t Protect Us From Inaccurate Provider Directories

- Covered CA – Marketplace plans deny in-network claims more than you might think

- Can’t Find A Doctor? Look at Low Star Rated Docs

- ‘A market failure’: High prices at Monterey County hospitals drive away many insured Californians

Mirrored Plans

Covered CA vs Direct must “mirror” each other

- What are #Mirror ed Plans

- Mirrored means that plan benefits and provider networks must be exactly the same direct and with what is offered in Covered CA. (SB 639 * Cahba.com * Crosby * 2.7.2014 Email to Cedars Sinai *

- That is Any Insurance Company that offers a product on Covered California must also offer a “mirror” plan with identical benefits and networks. The ID cards of all consumers who purchased plans through Covered California display the logos of their respective health plan AND the logo of Covered California. The ID cards of patients who purchased mirror products do not display the Covered CA logo ACPonline.org * Exception to the rule on rates for Silver Plans, “Silver Loading” due to Supreme Court decision.

- More liberal Provider Networks are a big advantage to Grandfathered Plans

- Mirrored means that plan benefits and provider networks must be exactly the same direct and with what is offered in Covered CA. (SB 639 * Cahba.com * Crosby * 2.7.2014 Email to Cedars Sinai *

- Is there any difference in #practise the Provider Directory for the same plan be it direct with the Insurance Company or Covered CA?

- Briefly, NO!!! That’s what the law says. See above on Mirrored Plans.

§156.235 Essential community providers.

Link to an amendment published at 80 FR 10873, Feb. 27, 2015.

(a) General requirement.

(1) A QHP issuer must have a sufficient number and geographic distribution of essential community providers, where available, to ensure reasonable and timely access to a broad range of such providers for low-income, medically underserved individuals in the QHP’s service area, in accordance with the Exchange’s network adequacy standards.

(2) A QHP issuer that provides a majority of covered professional services through physicians employed by the issuer or through a single contracted medical group may instead comply with the alternate standard described in paragraph (b) of this section.

(3) Nothing in this requirement shall be construed to require any QHP to provide coverage for any specific medical procedure provided by the essential community provider.

(b) Alternate standard. A QHP issuer described in paragraph (a)(2) of this section must have a sufficient number and geographic distribution of employed providers and hospital facilities, or providers of its contracted medical group and hospital facilities to ensure reasonable and timely access for low-income, medically underserved individuals in the QHP’s service area, in accordance with the Exchange’s network adequacy standards.

(c) Definition. Essential community providers are providers that serve predominantly low-income, medically underserved individuals, including providers that meet the criteria of paragraph (c)(1) or (2) of this section, and providers that met the criteria under paragraph (c)(1) or (2) of this section on the publication date of this regulation unless the provider lost its status under paragraph (c)(1) or (2) of this section thereafter as a result of violating Federal law:

(1) Health care providers defined in section 340B(a)(4) of the PHS Act; and

(2) Providers described in section 1927(c)(1)(D)(i)(IV) of the Act as set forth by section 221 of Public Law 111-8.

(d) Payment rates. Nothing in paragraph (a) of this section shall be construed to require a QHP issuer to contract with an essential community provider if such provider refuses to accept the generally applicable payment rates of such issuer.

(e) Payment of federally-qualified health centers. If an item or service covered by a QHP is provided by a federally-qualified health center (as defined in section 1905(l)(2)(B) of the Act) to an enrollee of a QHP, the QHP issuer must pay the federally-qualified health center for the item or service an amount that is not less than the amount of payment that would have been paid to the center under section 1902(bb) of the Act for such item or service. Nothing in this paragraph (e) would preclude a QHP issuer and federally-qualified health center from mutually agreeing upon payment rates other than those that would have been paid to the center under section 1902(bb) of the Act, as long as such mutually agreed upon rates are at least equal to the generally applicable payment rates of the issuer indicated in paragraph (d) of this section.

New rules for Federal Exchanges about “Narrow” networks.

Plans generally would have to contract with at least 30% of essential community providers in their market, including community health centers, HIV/AIDS clinics, and children’s hospitals.

Rules PDF

modernhealthcare.com

Article

modernhealthcare.com/

Covered CA & Direct Plans must be the same

3.04 Offerings Outside of Exchange.

(a) Contractor [Insurance Company] acknowledges and agrees that QHPs [Qualified Health Plan] and substantially similar plans offered by Contractor outside the Exchange must be offered at the same rate whether offered inside the Exchange or whether the plan is offered outside the Exchange directly from the issuer or through an agent as required under applicable laws, rules and regulations, including those required under 45 C.F.R. § 156.255(b), 42 U.S.C. § 18021, 42 U.S.C. § 18032. In accordance with Government Code Section 100503(f), Insurance Code Section 10112.3(c), and Health and Safety Code Section 1366.6(c), and other applicable State and Federal laws, regulations or guidance in the event that Contractor sells products outside the Exchange, Contractor shall fairly and affirmatively offer, market and sell all products made available to individuals [Free Quotes] and small employers [Free Quotes] in the Exchange to individuals and small businesses purchasing coverage outside the Exchange. …

Network adequacy standards. §156.230

The law appears to require that plans are exactly the same in and out of the Exchange – Covered CA

PPACA Qualified Health Plan Defined 42 U.S. Code § 18021 Section 1301 Covered CA & Insurance Company Contract §3.04

(B) provides the essential health benefits package described in section 1302(a);

(iii) agrees to charge the same premium rate for each qualified health plan of the issuer without regard to whether the plan is offered through an Exchange [Covered CA] or whether the plan is offered directly from the issuer or through an agent; and

From another well informed agent, who is also setting up training for TX navigators

the statute does not use the term “mirror”, but how would a plan off the exchange have the same premium if it did not provide the same benefit [including networks] structure?

Section 1301 PPACA Qualified Health Plan Defined Page 44 steveshorr.com

(B) provides the essential health benefits package described in section 1302(a);

(iii) agrees to charge the same premium rate for each qualified health plan of the issuer without regard to whether the plan is offered through an Exchange [Covered CA] or whether the plan is offered directly from the issuer or through an agent; an

Covered CA Board Meeting

6.15.2017

3.2.2 Standard Benefit Designs and Off-Exchange Silver Plan

a) During the term of this Agreement, Contractor shall offer the QHPs identified in Attachment 1 and provide the benefits and services at the cost-sharing and actuarial cost levels described in the Benefit Plan Design summarized at Attachment 2 (“Benefit Plan Designs”), and as may be amended from time to time under applicable laws, rules and regulations or as otherwise authorized under this Agreement.

b) During the term of this Agreement, for any plan year that the cost of the cost-sharing reduction program (Our webpage on the court case that ruled the subsidy for CSR’s was illegal as it wasn’t authorized by Congress * House v Burwell) is built into the premium for Contractor’s Silver-level QHPs, Contractor shall offer a non-mirrored, Silver-level plan, that is not a QHP, outside of Covered California that complies with the benefits and services at the cost-sharing and actuarial cost level described in the plan design at Attachment 3 (“Off-Exchange, Non-Mirrored Silver Plan Design”). This plan must not have any rate increase or cost attributable to the cost of the cost-sharing reduction program.

3.2.3 Offerings Outside of the Exchange

a) Contractor acknowledges and agrees that as required under State and Federal law, QHPs and substantially similar plans that are identical in benefits, service area and cost sharing structure offered by Contractor outside the Exchange must be offered at the same premium rate whether offered inside the Exchange or outside the Exchange directly from the issuer or through an Agent. Covered CA Board Meeting 6.15.2017 *

Provider Network Access Standards

California Code of Regulations 10 CCR § 2240 et seq.

- § 2240. Definitions.

- § 2240.1. Adequacy and Accessibility of Provider Services.

- § 2240.15. Network Access Appointment Waiting Time Standards; Quality Assurance; Disclosure and Education.

- § 2240.16. Access Standards for Pediatric Vision and Oral Essential Health Benefits and Specialized Policies that Cover Dental Benefits Only.

- § 2240.2. Insurance Contract Provisions.

- § 2240.3. Provisions of Policies and Certificates.

- § 2240.4. Contracts with Network Providers.

- § 2240.5. Filing and Reporting Requirements.

- § 2240.6. Notice and Information to Covered Persons.

- § 2240.7. Discretionary Waiver of Network Access Standards.

See also – Special Enrollment Periods

Department of Insurance Investigation – errors in lists

“It boggles my mind that insurers can’t keep their list up to date,” “There is no excuse for how messy it is. Health insurers are engaged in false advertising.” Fines coming… CA Health Line 2.10.2017 * Blog Insure Me Kevin.com 2.11.2017 DMHC fined:

- Anthem $250,000; and

- Felser Settlement 5.5.2016

- Blue Shield (BS) $350,000.

- Letters to be sent to members about resubmitting claims by 12.31.2015. BS asked us not to post, so email us or call BS @(888) 256-3650 to discuss. FAQ’s

State officials said that Blue Shield faced a higher fine because it was less cooperative with regulators. In addition to the fines, DMHC has ordered both insurers to:

- Improve the accuracy of their provider directories; and

- Reimburse enrollees who have been negatively affected by the inaccurate information.

According to the Times, Blue Shield already has reimbursed more than $38 million to consumers who had been charged out-of-network costs. Officials said they do not yet have a reimbursement estimate for Anthem. Learn More CA Health Line 11.4.2015

1.5.2015 DOI Emergency Regulations! Rules Approved CA Health Line 2.3.2015 SB 137 Hernandez Los Angeles Times

The emergency regulation requires insurers to:

- Adhere to new standards for appointment wait times (DOI release, 1/5);

- Offer an adequate number of physicians, clinics and hospitals to patients who live in certain areas;

- Provide an accurate list of in-network providers (“KXJZ News,” Capital Public Radio, 1/5);

- Provide out-of-network care options for the same price as in-network care when the number of in-network providers is insufficient; and

- Report to DOI information about their networks and any changes. CA Health Line 1.5.2015

CA Health Line 2.17.2015 Sutter – Blue Shield could affect 280k patients – CA Health Line 1.6.2015

12.12.2014 – Health Net Sued – Narrow Lists – Alleged Actual Harm

11.18.2014 CA Healthline Errors Found by DMHC – Both Blue Shield and Anthem said the investigation’s methodology was flawed. For example, providers who responded to the survey with “no answer” were recorded as not accepting exchange patients.

12.9.2014 CA Health Line 1/2 of Medicaid MD’s on list, not really available.

So far, complaints have included:

•Failure to receive health plan identification cards and enrollment information; •Inaccurate provider lists; and •Narrow networks.

State regulators mostly are hearing complaints about the difficulty of determining physicians who are included in provider networks. For example, the Humboldt-Del Norte County Medical Society last month analyzed one insurer’s provider lists and found that only about 33% of area physicians were accurately listed (californiahealthline.org)

Open Letter to regulators from Concerned Consumer 10.14.2014

Must MD accept you, if directory is wrong?

My MD #said they that they are a participating provider with Blue Shield.

Turns out they are for some plans, but not the plan that I have.

Must the MD accept Blue Shield’s rate and not make me pay the difference.

It was their mistake!

This is beyond the scope of my duties as an Insurance Agent.

Please check with legal counsel and/or our appeals page.

Did the doctor make a binding contract with you, guaranteeing that they would accept Blue Shield’s payment as payment in full?

The Blue Shield policy – says it’s the members responsibility to make sure a provider is on the list

Choice of Providers

This Blue Shield health plan is designed for Members to obtain services from Blue Shield Participating Providers and MHSA Participating Providers. However, Members may choose to seek services from Non-Participating Providers for most services. Covered Services obtained from Non-Participating Providers will usually result in a higher share of cost for the Member. Some services are not covered unless rendered by a Participating Provider or MHSA Participating Provider.

Please be aware that a provider’s status as a Participating Provider or an MHSA Participating Provider may change. It is the Member’s obligation to verify whether the provider chosen is a Participating Provider or an MHSA Participating Provider prior to obtaining coverage.

Call Customer Service or visit www.blueshieldca.com to determine whether a provider is a Participating Provider. Call the MHSA to determine if a provider is an MHSA Participating Provider. See the sections below and the Summary of Benefits for more details. See the Out-of-Area Services section for services outside of California Blue Shield Evidence of Coverage Page 14 *

Blue Shield Participating Providers

Blue Shield Participating Providers include primary care Physicians, specialists, Hospitals, and Alternate Care Services Providers that have a contractual relationship with Blue Shield to provide services to Members of this Plan. Participating Providers are listed in the Participating Provider directory.

Participating Providers agree to accept Blue Shield’s payment, plus the Member’s payment of any applicable Deductibles, Copayments, and Coinsurance or amounts in excess of specified Benefit maximums as payment-in-full for Covered Services, except as provided under the Exception for Other Coverage and the Reductions-Third Party Liability sections. This is not true of NonParticipating Providers.

If a Member receives services from a Non Participating Provider, Blue Shield’s payment for that service may be substantially less than the amount billed. The Subscriber is responsible for the difference between the amount Blue Shield pays and the amount billed by the Non Participating Provider.

If a Member receives services at a facility that is a Participating Provider, Blue Shield’s payment for Covered Services provided by a health professional at the Participating Provider facility will be paid at the Participating Provider level of Benefits, whether the health professional is a Participating Provider or Non-Participating Provider. The Member’s share of cost will not exceed the Copayment or Coinsurance due to a Participating Provider under similar circumstances.

Some services are covered only if rendered by a Participating Provider. In these instances, using a Non-Participating Provider could result in a higher share of cost to the Member or no payment by Blue Shield for services received

Payment for Emergency Services rendered by a Physician or Hospital that is not a Participating Provider will be based on Blue Shield’s Allowable Amount and will be paid at the Participating level of Benefits. The Member is responsible for notifying Blue Shield within 24 hours, or as soon as reasonably possible following medical stabilization of the emergency condition.

The Member should contact Member Services if the Member needs assistance locating a provider. The Plan will review and consider a Member’s request for services that cannot be reasonably obtained in network. If a Member’s request for services from a Non-Participating Provider or MHSA Non-Participating Provider is approved at an in-network benefit level, the Plan will pay for Covered Services at a Participating Provider level.

Please call Customer Service or visit www.blueshieldca.com to determine whether a provider is a Participating Provider Blue Shield Evidence of Coverage Page 15

-

Have your MD click here to visit Blue Shield’s new provider sign up page.

Bibliography

A breach of contract is the failure of a party to the contract to do what he or she agreed to do under the contract. A party’s breach of contract gives rise to certain remedies in the non-breaching party, in particular

(1) an action for money damages, and

(2) in certain circumstances, a suit for specific performance of the contract.

CA Jury Instructions – Breach of Contract

.justia.com/trials-litigation/

Blue Shield Provider Finder – Shows detailed instructions

plainfield dental.com/does-do-you-take-my-insurance-equal-are-you-in-network/

See page 24 of Blue Shield PPO Evidence of Coverage – Choice of Providers

Blue Shield of California

![]()

Provider #Finder -

Dentists, Doctors & Hospitals

All Plans - Medicare Advantage, Employer Group, Under 65 - Covered CA

Find a doctor near you

VIDEOS

- Blue Shield Exclusive PPO Your new ppo * PPO Primary MD FAQ’s * has 50k+ doctors and 320 hospitals statewide, plus Blue Card benefits out of state & country. 2020 Agent Guide * Member Outreach Bulletin *

- Providence Issues 2024

- How to use the Finding a provider tool above VIDEO

- Understanding Your Plan pdf

- Nurse Help 24/7, Heal and Teladoc save on prescriptions ER vs. urgent care.

- Use your online account to review claims, copays or deductibles and take advantage of other member benefits.

- Explanatory VIDEOS on everything... from Blue Shield

- chcf.org/primary-care-matters * More readable summary * Health care systems with strong levels of primary care investment have better and more equitable health outcomes, lower care costs, and better care quality. We can build a healthier future for all Californians by focusing resources back to patients and their relationship with primary care providers.

- Medicare Advantage Provider Print Directories BROKER ONLY

- Email us [email protected] if you want a pdf print directory

- Enroll and get full details on our

- What do I have to do to see a specialist if I'm in an HMO or Medicare Advantage Plan?

- Generally, just ask your PCP Primary Doctor.

- Check your Evidence of Coverage for details. Email us, [email protected] if you want a copy of it.

- What if my PCP won't give a referral.

- Check the procedure in your Evidence of Coverage, email us and see our webpage on appeals & IMR Independent Medical Review.

- Generally, just ask your PCP Primary Doctor.

Historical

Felser & Scarpo Lawsuits

Class Action Felser Lawsuit against Blue Cross

- Felser Settlement 5.5.2016

- Specifically, the lawsuit alleges that Anthem:

- Delayed giving its customers complete information until it was too late for them to switch their coverage choice;

- •Did not inform its customers that it no longer offered out-of-network coverage in four of state’s largest counties — Los Angeles, Orange, San Diego and San Francisco; and

- •Misled or did not inform its customers about which doctors and hospitals were participating in the insurer’s new plans. “intentionally misrepresented and concealed the limitations of their plans because it wanted a big market share.”

As a result of those alleged failures, the lawsuit states that many members received thousands of dollars in unexpected medical bills and were unable to see their preferred physician. (californiahealthline.org)

55 page complaint – brief (with my personal ONLY opinions, links and research)

If you have a similar problem, Mr. Biedart Esq (Website & Contact Info) would be happy to talk to you. / I happen to know him socially. Here’s a comment from one of our Insurance Clients:Michael Bidart and his firm represented me in a bad faith claim against my home owners insurer some 13 years ago. As a lawyer myself, I can tell you that they are top notch in the field. Jay Gov. Jerry Brown (D) has signed a bill (SB 964) to increase oversight of insurers’ provider networks, the Sacramento Business Journal reports (Robertson, Sacramento Business Journal, 10/2). bizjournals.com/ Consumer Watchdog – files against CIGNA & Blue Shield californiahealthline.org/ 2nd Lawsuit latimes.com/

News Briefs

HHS ruling to urge insurers to be liberal in Provider Lists and Premium Payment Date (CA HealthLine) actual regulation & will coverage really start 1.1.2014 Right to change plans if Provider Finder doesn’t work – Special Enrollment???

Nationally 1/2 of exchange programs have narrow networks modern health care.com

Covered CA urges insurers to expand network california health line.org

12.12.2013 Covered CA claims 80% of CA MD’s are in their networks 10.15.2013 Covered CA apologies for releasing inaccurate provider list too early.

AIS Health Explanation Los Angeles Times 9.15.2013 on “Narrow Networks” to keep costs down on plans in Covered CA. Video about what networks are. Notice in MD office, not a provider. Blue Shield of California has said it will include just 50% of the physicians and 75% of the hospitals in 2014 that it did in this year’s individual plans. However, Blue Shield has said it will offer exclusive provider organization plans — or EPOs — to first-time buyers for a lower cost than other plans on the exchange CA HealthLine.org NPR

Kevin Knauss Post on if there are fewer MD’s in Covered CA then out of Covered CA? Confusing Provider Finders insuremekevin.com

For more information – View the Comments Section of the Provider Finder Page

Myth of MD Shortage – Modern Health Care.com 11.11.2013

Covered CA Contract with Insurance Companies – Provider List Requirements… See Page 9, et seq.

2.23.2014 A Sonora mechanic is in so much pain that he can barely walk, but he can’t seem to find a doctor to fix his ailing back after he and his wife switched their insurance coverage through Covered California. Chris Dunn reached out to CBS13 hoping we could get answers. He needs his surgery yesterday. But instead of scheduling his date, he and his wife are navigating a confusing maze of doctors and insurance plans. sacramento.cbslocal.com/ 2.23.2014 San Jose Mercury News Lowering costs by forcing doctors and insurers to compete for millions of new patients is a primary goal of the nation’s new health care law, but a group of gastroenterologists in the East Bay and internists near Chico are exposing a fissure in that plan. mercurynews.com/

Lori Scarpo sued Blue Shield,

alleging they knowingly posted

bogus provider lists

and made it a class action lawsuit. The case was consolidated – see links below for more detail.

Here’s relevant links:

Settlement Website harrington talon aca settlement.com

FAQ’s

Court Documents

Contact Information

Appoint us as your Broker No extra charge. Blue Shield pays us.

https://natlawreview.com/article/win-out-network-providers

https://jhmhp.amegroups.org/article/view/8976/pdf

https://www.dmhc.ca.gov/HealthCareinCalifornia/YourHealthCareRights/TimelyAccesstoCare.aspx

https://calmatters.org/health/2024/07/ghost-network-doctor-referrals/

https://calmatters.org/health/2024/01/california-hospital-salinas-cost/

https://insuremekevin.com/cant-find-a-doctor-look-at-low-star-rated-docs/

https://www.beckershospitalreview.com/finance/13-top-reasons-for-claims-denials.html

https://indianapublicmedia.org/news/marketplace-plans-deny-in-network-claims-more-than-you-might-think.php

https://www.news-medical.net/news/20220726/Even-well-intended-laws-cane28099t-protect-us-from-inaccurate-provider-directories.aspx

https://californiahealthline.org/news/article/even-well-intended-laws-cant-protect-us-from-inaccurate-provider-directories/

A top California hospital says it’s the target of retaliation by a giant Catholic healthcare chain

https://www.latimes.com/business/story/2021-02-19/providence-hoag-retaliation

I received your letter and I would like to go forward this case (No.CJC-14-004800)

Reply

steve says:

February 13, 2018 at 9:15 PM

This website is not the place to opt in or out of the lawsuit

Please double check any correspondence that you have received or the links above to make your election as to what you want to do