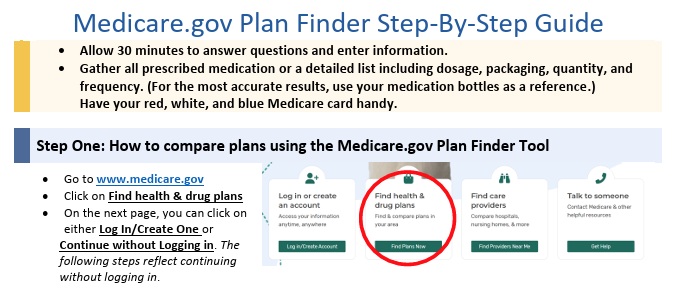

Instructions to Use Medicare.Gov Plan Finder

If you are using Part D premiums for Medi Cal Share of Cost Spend down, email us [email protected]

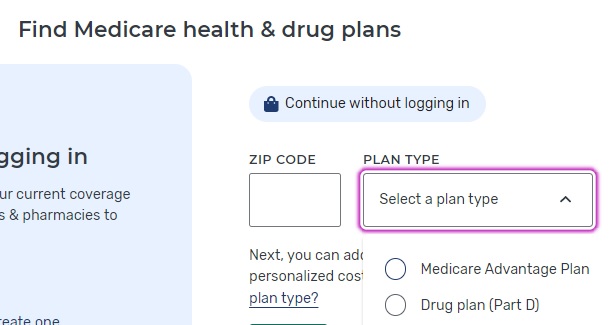

Medicare.Gov How to use the Shop & Compare Tool

Part D Rx Prescription plans?

- Medicare.Gov Plan Finder Instructions

- Scroll down for FAQ's, instructions and how we can help you navigate Medicare. It's better to create an account and log in. That way your Rx gets saved and/or automatically listed.

How to use the Rx & Plan Finder

- How to Create a My Medicare.Gov Account

- That way your Prescriptions Rx are automatically populated

- Our email is encrypted sending & receiving by Paubox.com

Prescription Drug 2025 #RxGuide

PDF # 11109

*****************

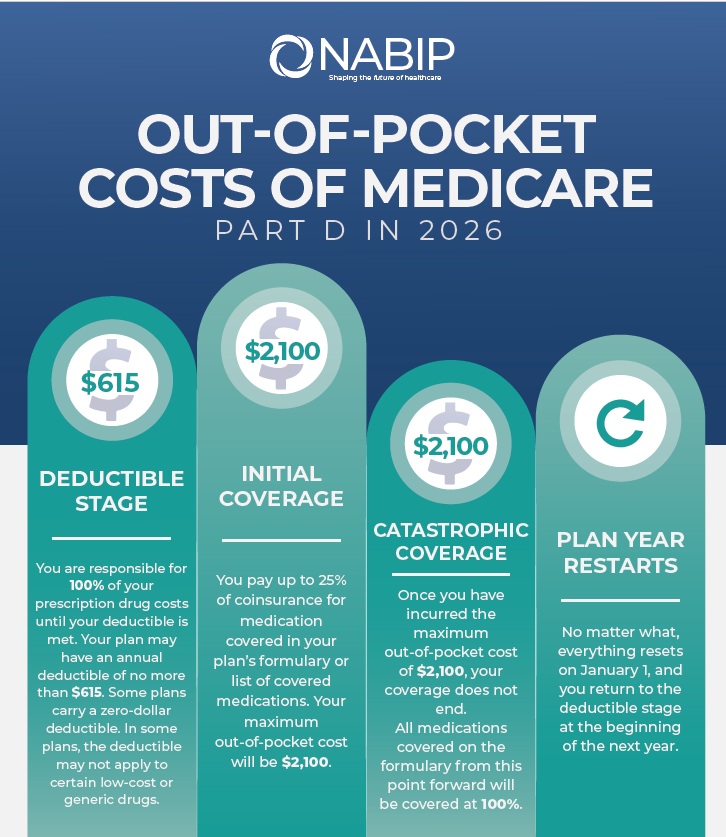

No more Coverage Gap - Donut Hole $2,100 Cap

******************

- Medicare Part D Rx premiums can be found on Medicare . Gov See instructions on how to shop premiums.

- Scope of appointment - permission to discuss Rx and MAPD Plans

- Our Webpage Premiums for those with High Income Parts D Rx & B Doctor Visits

- Medicare Rules for High Income People Medicare Costs # 11579

- Our #High Income Surcharge Video Explanation

- Kaiser Foundation Introduction - Overview

- Fact Sheet Medicare Part D CA Health Care Advocates Hi Cap

-

. Prescription Drugs Hi Cap

- Medicare Part D: An Overview – 10-31-23

- Prescription Drug Resources – 11-07-22

- When Your Part D Prescription is Denied– 11-22-22

- Shop & Compare Tools Part D Rx

- Get Instant Quotes, Information & Enroll online

- See our web page on Part D Shop & Compare for more information & FAQ's

- MANDATED wording!: ‘‘We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1–800–MEDICARE to get information on all of your options.’’ § 422.2267(e)(41).

- We disagree with the above wording, as we can use the same tools on Medicare.gov as they do!

AI Generated

Key reasons for the commission cuts

- Reclassifying “compensation”: In an effort to curb deceptive marketing practices, CMS issued new rules that went into effect in 2024, redefining what counts as agent compensation. The changes eliminated supplemental payments, sometimes referred to as “administrative fees” or “overrides,” that insurers previously paid to third-party marketing organizations (TPMOs) for additional services beyond a base commission.

- Centralizing control: The rule aimed to create a fixed compensation structure for agents, regardless of which plan a beneficiary enrolls in. This would prevent financial incentives that could lead agents to steer beneficiaries toward one plan over another based on higher payouts. [8, 9, 10, 11, 12]

- Limiting growth: Some insurers are cutting commissions to slow down their enrollment numbers. This typically happens when a company has enrolled a large number of people in a plan and becomes concerned that rising medical costs will hurt profitability.

- Managing costs: As medical utilization and costs increase, many insurers are prioritizing profit margins over enrollment growth. Cutting agent commissions is one way for companies to reduce their overall expenses.

- Responding to inflation: Regulations like the Inflation Reduction Act have also placed cost pressure on carriers, prompting many to find ways to restrict sales of certain products. [3, 6, 13, 14, 15]

- Legal setbacks: The CMS rule that sought to limit compensation was challenged in court, and enforcement of the rule was paused in mid-2024. However, this legal uncertainty has led some carriers to continue reducing or eliminating commissions on their own. [16, 17, 18]

How this impacts agents

- Financial instability: Independent agents who rely on commissions are experiencing significant financial strain. Many have spoken out, arguing that the cuts devalue their expertise and threaten their ability to provide year-round service to beneficiaries.

- Reduced incentive for Part D: Historically, Part D plans have offered lower commissions than Medicare Advantage plans. The elimination of commissions makes it even less appealing for agents to assist with these plans, which are already complex for consumers to navigate.

- Negative effect on consumers: Without agent compensation, many agents are no longer able to assist with Part D enrollments. Critics argue that this leaves seniors, especially those needing expert guidance on complex prescription drug options, confused and underserved. [1, 19, 20, 21, 22]

Resources for agents

. You can learn more about their efforts and resources on the

.

Links & Resources

- medicare.gov/prescription-drugs-outpatient

- ritterim.com/2026-medicare-part-d-redesign-updates-agents-should-know

- Final CY 2026 Part D Redesign Program Instructions

- Fact Sheet: President Donald J. Trump Announces Actions to Lower Prescription Drug Prices

- Why Part D Rx Premiums are likely to increase in 2026

- increased use of some higher-cost prescription drugs;

- a law that capped out-of-pocket spending for enrollees; and

- changes in a program aimed at stabilizing price increases that the Trump administration has continued but made less generous. Learn More >>> Kff.org *

- What to know about Medicare’s true out-of-pocket (TrOOP) costs

- Ask us about Medicare Advantage, where Part D Rx is usually included! [email protected]

- 3 million will be greatly helped with $2k cap

- Guidance on Inflation Reduction Act’s Medicare Prescription Payment Plan Released July 2024 Medicare Rights

- Key Facts About Medicare Part D Enrollment, Premiums, and Cost Sharing in 2024 KFF

- Goodbye Medicare Part D Donut Hole; Hello $2,000 Cap Forbes

- insurance news net.com/no more part-d-commissions?

New 2025 Medicare Payment Plan

#Monthly vs $2k at one time or as needed

- ritter im.com/preparing-clients-for-the-new-medicare-prescription-payment-plan-program/

- In 2025 you will have the option to pay out-of-pocket prescription drug costs in the form of capped monthly payments instead of all at once at the pharmacy.

- cms.gov/medicare-prescription-payment-plan

- cms.gov/fact-sheet-medicare-prescription-payment-plan-final-part-one-guidance

- cms.gov/medicare-prescription-payment-plan-fact-sheet

More information & FAQ’s on Medicare Rx Plans

- Scope of appointment – permission to discuss Rx and MAPD Plans

- Our Webpage Premiums for those with High Income Parts D Rx & B Doctor Visits

- Medicare Rules for High Income People Medicare Costs # 11579

- Our #High Income Surcharge Video Explanation

- Kaiser Foundation Introduction – Overview

- Fact Sheet Medicare Part D CA Health Care Advocates Hi Cap

-

. Prescription Drugs Hi Cap

- Medicare Part D: An Overview – 10-31-23

- Prescription Drug Resources – 11-07-22

- When Your Part D Prescription is Denied– 11-22-22

- Medicare Rx Benefit Manual Rev 1.2016 83 pages

- Resources: Medicare Drug Coverage (Part D) Mini-Course & Podcast Series CMS

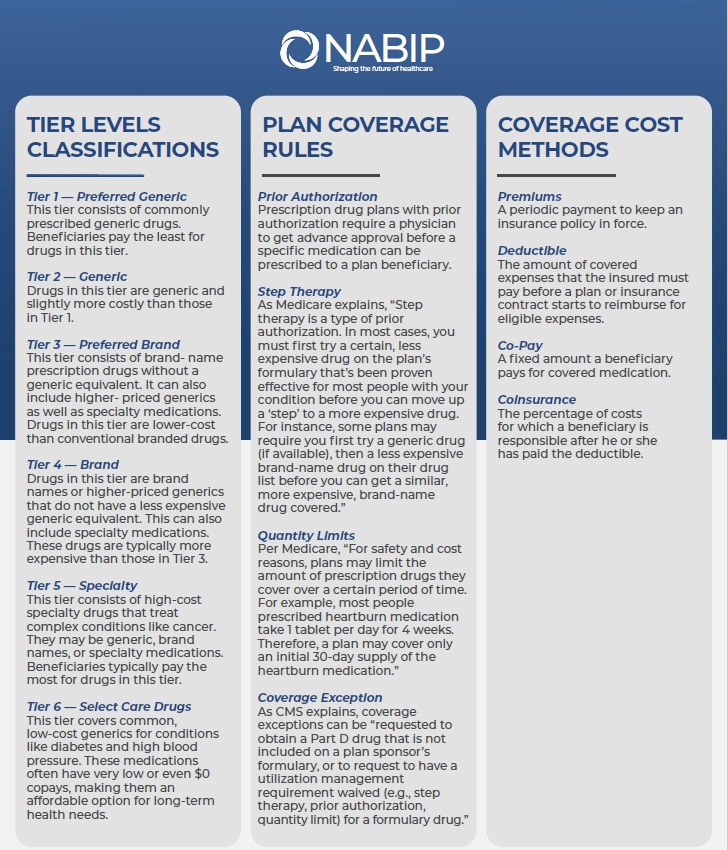

- Network Pharmacies, Formularies & Common Coverage Rules # 11136

- Insulin Maximum Co Pay $35

- Graphic on Part D Premium Increases & Why?

- Our webpage on Maximus Appeals LEP Late Enrollment Penalty

- Shop & Compare Tools Part D Rx

- Get Instant Quotes, Information & Enroll online

- MANDATED wording!: ‘‘We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1–800–MEDICARE to get information on all of your options.’’ § 422.2267(e)(41).

- We disagree with the above wording, as we can use the same tools on Medicare.gov as they do!

You’re reading the situation correctly: once someone enrolls in a PDP/MA-PD plan you’re not appointed with, you generally should not be acting as that plan’s “agent/broker” for ongoing plan-specific service—especially anything that involves member-specific information (PHI), contacting the plan on their behalf, coverage determinations, exceptions/appeals, billing, disenrollment/reinstatement, etc.

Why it’s a problem (the “compliance” logic in plain English)

-

“Representing” a Part D sponsor is broader than just enrolling someone. CMS’s Part D agent/broker rule treats “representation” as including selling and also outreach and answering (or potentially answering) questions from existing/potential beneficiaries. (Legal Information Institute)

Practical takeaway: if you keep troubleshooting their plan and advising them on that plan’s specifics, you can drift into “representation” without the sponsor appointment/training/oversight that normally goes with it. -

Role clarity matters. CMS marketing guidance emphasizes beneficiaries shouldn’t be confused about whether someone is acting in a sales/marketing role vs. customer service, and the agent/broker must be clear when roles change. (cms.gov)

Practical takeaway: you don’t want a member thinking you’re their plan’s servicing agent when you’re not authorized by that sponsor. -

You also can’t “solve it” by charging a service fee. CMS rules place guardrails around beneficiaries being charged “marketing/consulting fees” when considering enrollment (and related guidance in the market has been very clear that beneficiary-paid “consultation/service/admin fees” tied to MA/PDP enrollment activity are not allowed). (eCFR)

What you can still do safely (high-value, but bounded)

You can offer general education that doesn’t require plan authorization or member data, for example:

-

How to contact the plan, what to ask for, how to request a supervisor/case number.

-

General explanation of formulary/tiers, pharmacy networks, prior auth vs. exception vs. appeal (without telling them what the plan will do).

-

Help them assemble their info (med list, NDC, pharmacy, prescriber) and draft questions.

-

Refer them to 1-800-MEDICARE or SHIP for unbiased help if they want ongoing assistance outside a servicing agent relationship. (That’s a standard consumer-safe direction; CMS regularly points beneficiaries to these channels.)

A script you can say (phone/Zoom)

Here are a few versions you can use—pick the tone that fits you.

Version A (friendly + firm):

“I’m glad to help at the enrollment stage, but I’m not appointed/contracted with your current Part D plan. That means I can’t access your account, speak to the plan for you, or provide plan-specific service after enrollment. The fastest path is to call the plan’s member services number on your card (or 1-800-MEDICARE). If you’d like, I can help you write down the exact questions to ask before you call.”

Version B (short + boundary):

“Because I’m not the servicing agent for that plan, I can’t provide ongoing plan-specific support. Please contact your plan’s member services or 1-800-MEDICARE.”

Version C (offers a path forward):

“I can’t do ongoing service on a plan I’m not authorized to represent. If you want me to be your long-term Medicare person, during the next election period we can review options and enroll you in a plan I’m contracted with so I can properly support you going forward.”

A message you can copy/paste (text or email)

Thanks for reaching out. I’m happy to point you in the right direction, but I’m not appointed/contracted with your current Part D plan, so I’m not able to provide plan-specific service (account access, calling the plan on your behalf, coverage disputes, exceptions/appeals, billing issues, etc.).

Next step: Please call Member Services using the number on your ID card (or call 1-800-MEDICARE) and ask for a reference/case number.

If you want, reply with (1) the medication name + dosage, (2) the pharmacy name, and (3) what the plan told you, and I’ll help you organize questions to ask the plan—without accessing your account or acting as the plan’s representative.

For ongoing support in the future, we can schedule a review during the next election period and choose a plan I’m authorized to service.

A practical workflow that saves you time (and feels helpful)

-

One free “handoff”: “Here’s who to call + what to ask.”

-

One optional “prep” assist: You help them write questions and understand the terms (no PHI access, no calling as their agent).

-

After that, repeat the boundary and stop the loop unless they’re willing to switch into a plan you can properly service (when allowed by election rules).

If you tell me the main plans you keep seeing (e.g., big PDP brands your clients pick), I can tailor the copy so it references exactly what you will/won’t do (pharmacy change, formulary exception, LIS/Extra Help questions, IRMAA, etc.) while staying clean on CMS language.

Here’s a clearer, research-backed breakdown of the commission situation you’re describing — especially regarding WellCare Part D versus a plan that does pay you (like Blue Shield) — and how you can explain it to clients in a way that’s professional, compliant, and sets clear expectations.

1. WellCare Part D Plans & Broker Commissions

-

WellCare (and some other carriers) have stopped paying broker commissions for standalone Part D plans in many markets. That means even though the carrier reports a CMS fair market value commission schedule, the insurer itself may choose to pay $0 or very minimal compensation on certain Part D plans. (Ritter Insurance Marketing)

-

The national CMS maximum allowable for 2026 Part D initial commissions is about $114 per enrollee (with ~$57 on renewals), but carriers can and do choose to pay less — or nothing at all. (Ritter Insurance Marketing)

-

Industry discussions and reports (including carrier forums) confirm that many standalone PDPs, including some WellCare plans, are effectively “non-commissionable” this plan year — i.e., no broker compensation due to business decisions even though CMS sets a maximum guideline. (Ritter Insurance Marketing)

Bottom line: You can enroll someone in a WellCare Part D plan, but if your contract with WellCare doesn’t currently pay a commission on that plan, you simply won’t be paid for that enrollment.

2. What This Means for Your Role After Enrollment

Even when you help someone enroll, be cautious:

-

You should not act as the servicing agent for a plan where you aren’t appointed and contracted, because that crosses from educational support into a role that CMS and many carriers define as “representation” of the plan. That can expose you and the plan to compliance issues. (cms.gov)

-

Examples of things you should avoid doing without proper contracting include:

• Contacting the carrier on the member’s behalf about claims or coverage decisions

• Accessing PHI/accounts to troubleshoot service issues

• Advocating in formal appeals or exceptions processes

(You can help them understand what to ask the plan, *but calling as their agent is different than helping them ask better questions.)

3. How to Explain This to Clients

Here are phrases you can use that are clear, compassionate, and compliant — both live on Zoom and in text:

Live or Zoom Script (friendly + professional)

“For the Part D plan you chose, I wasn’t contracted with that carrier for service, so I can help you understand how to contact them or what questions to ask — but I am not able to call on your behalf or provide ongoing support for that plan.

If you want help throughout the year, one option is to enroll in a plan that I’m appointed to service — like Blue Shield — so I can provide ongoing support.”

Text or Email Version

Thanks for reaching out!

For the WellCare Part D coverage you selected, I am not contracted or appointed to provide ongoing account support with that carrier. That means I cannot access your account or contact the plan on your behalf.

Here’s what you can do next:

Call your plan’s Member Services number on your ID card (or 1-800-MEDICARE).

Ask for a case/reference number so you can follow up.

If you’d like help drafting specific questions before you call, I’m happy to assist.

If you want someone who can support you year-round, we can review your options and see whether switching to a plan I’m appointed with (like Blue Shield) makes sense during the next enrollment period.

4. Comparing the Plans (Your Situation)

You mentioned two examples:

-

WellCare PDP at ~$5.70/month (likely non-commissionable) — This type of plan may not pay you anything for enrollment. (Ritter Insurance Marketing)

-

Blue Shield plan at ~$180/month (commissionable) — If you are appointed with Blue Shield for that plan, you will receive compensation for enrolling and can provide ongoing compliant support as their appointed agent.

This is a legitimate business consideration — not just about money — because if a carrier isn’t paying a commission, that often means you can’t justify spending ongoing time providing service for that plan if you’re doing it outside of contract.

5. Optional “Value-Driven” Explanation for Clients

If a client pushes back or wonders why they should consider a plan that you can service:

“You should choose a plan that works best for your needs. A plan’s price and drug coverage matter most. But there’s also value in having someone you trust who can answer questions and help manage issues through the year. Plans where I am appointed to service you allow me to be that resource — which is why some people choose those options even if the premium is slightly higher.”

If you’d like, I can help you generate a client-facing FAQ or brochure with these explanations that you can use in Zoom meetings and follow-up emails, tailored to your specific carriers and compliance requirements.

Perfect. I’ll draft this in a way that protects you, is CMS-safe, and still positions you professionally.

Below is a client-facing FAQ sheet you can use in Zoom, email, or post as a PDF on your site.

Medicare Part D Plan Support – What to Expect

Why can’t you help me with my WellCare Part D plan?

Some Medicare Part D plans do not compensate independent brokers for enrollment or ongoing service. In those cases, I am not contracted or appointed to provide account-level support for that carrier.

That means:

-

I cannot access your account

-

I cannot call the plan on your behalf

-

I cannot intervene in coverage disputes or appeals

-

I cannot act as the plan’s servicing agent

You can always contact:

• The Member Services number on your ID card

• 1-800-MEDICARE (1-800-633-4227)

• Your local SHIP program for unbiased assistance

What CAN you help me with?

Even if I am not contracted with your plan, I can:

✓ Help you understand Medicare Part D rules

✓ Explain how formularies and tiers work

✓ Help you prepare questions before you call the plan

✓ Review options during Annual Enrollment

✓ Compare plans for the upcoming year

I just cannot provide plan-specific account service if I am not the appointed agent for that carrier.

Why would I consider a plan you’re contracted with?

When I am contracted and appointed with a Medicare plan:

✓ I can provide year-round support

✓ I can contact the carrier on your behalf

✓ I can assist with coverage questions

✓ I can help with exceptions and appeals guidance

✓ I can track issues to resolution

There is value in having a licensed Medicare advisor who can provide ongoing service.

Isn’t the cheaper plan better?

Sometimes yes — sometimes no.

A low-premium plan (for example, some $5–$10/month Part D plans) may work very well for healthy individuals with minimal prescriptions.

However, higher-premium plans (for example, some $150–$200/month options) may offer:

• Broader formularies

• Lower copays for certain drugs

• Better pharmacy networks

• More predictable coverage

• Ongoing broker support

The right plan depends on your medications, pharmacy, and how much service support you want during the year.

Important Disclosure

I am a licensed insurance agent. I may receive compensation from Medicare plans when I am contracted and appointed with that carrier and you enroll through me.

If I am not contracted with a plan, I do not receive compensation and cannot provide ongoing account-level service for that carrier.

You are never required to enroll in a plan I represent.

A Short Version for Zoom (2-Minute Explanation)

You can say this:

“I want you in the plan that works best for your prescriptions. Just understand that if you choose a carrier I’m not contracted with, I won’t be able to provide ongoing service during the year. If you want me to be your Medicare resource, we’ll want to choose a plan I’m appointed to support.”

Optional: A More Direct Boundary Version (When They Keep Asking for Free Service)

“I’m happy to point you in the right direction, but because I’m not the servicing agent for that plan, I can’t provide ongoing account support. Please contact Member Services directly for resolution.”

Steve, this approach does three things for you:

-

Keeps you clean with CMS

-

Sets professional boundaries

-

Repositions your value without sounding commission-driven

If you’d like, I can next:

• Tighten this into a branded one-page PDF format

• Create a short script specifically mentioning WellCare vs Blue Shield

• Or draft a website page titled “Why Ongoing Medicare Support Matters”

Which direction would help you most?

The True Cost of Healthcare

A View of Healthcare Costs from the Inside

David Belk MD

Edited by Paul Belk PhD

- “The Great American Healthcare Scam” by Dr David Belk VIDEO

- More articles by David Belk on Huffpost

- Heal-CA.org big pharma exposed

- On the other hand – Dr. Belk lost his license?

- Gross Negligence in treatment of a patient

- Yelp.com – Big Farma got him

Medicare.Gov #Glossary

for Shopping Tool

Coinsurance

An amount you may be required to pay as your share of the cost for health care services or prescriptions after you pay any deductibles. Coinsurance is usually a percentage (for example, 20%).

Deductible

The amount you must pay for health care services or prescriptions each year, before your Medicare drug plan, your Medicare Health Plan, or your other insurance begins to pay. These amounts can change every year.

Dosage

The prescribed strength or amount of therapeutic ingredient(s) administered at prescribed intervals.

Drug Coverage

This tells you that a plan offers coverage of prescription drugs.

Drug Restrictions

The plan may have certain coverage restrictions (including quantity limits, prior authorization, and step therapy) on a prescription drug.

Example of Restrictions

Estimated Annual Drug Costs

This is an estimate of the average amount you might expect to pay each year for your prescription drug coverage. This estimate includes the following costs, as applicable:

- Monthly premiums

- Annual deductible

- Drug copayments/coinsurance

- Drug costs not covered by prescription drug insurance

If you entered your drugs into the Medicare Plan Finder, then this estimate includes the cost of those drugs.

If you selected “I don’t take any drugs,” then this amount includes only the cost of the monthly premiums that you would pay for the plan and it does not include any drug costs.

If you selected “I don’t want to add drugs now,” then this estimate includes the average drug costs for people with Medicare and may differ depending on your age and health status.

Your expenses may be lower if you have limited income and resources.

Formulary

A list of prescription drugs covered by a prescription drug plan offering prescription drug benefits.

Monthly Premium

The periodic payment to Medicare, an insurance company, or a health care plan for health or prescription drug coverage. In a few cases, a note will say “Under Review” instead of a premium amount. This means Medicare and the company are still discussing the amount.

MTM Program

Medication Therapy Management (MTM) Programs

offer free services to eligible members of Medicare drug plans. These services help make sure that medications are working to improve their members’ health. Members can talk with a pharmacist or other health professional and find out how to get the most benefit from their medications. Members can ask questions about costs, drug reactions, or other problems. Each member gets their own action plan and medication list after the discussion. These can be shared with their doctors or other health care providers. Members who take different medications for more than one health condition may contact their drug plan to see if they’re eligible. Humana * Medicare.gov *

What are Star Ratings – Medicare Advantage

Medicare Part B Out Patient

Rx Drugs Covered

What types of Rx Drugs are Covered under Part B Doctor visits and then a Medi Gap plan?

- Part B covers certain drugs, like injections you get in a doctor’s office, certain oral cancer drugs, and drugs used with some types of durable medical equipment—like a nebulizer or external infusion pump.

- Under very limited circumstances, Part B covers certain drugs you get in a hospital outpatient setting. You pay 20% of the Medicare-approved amount for these covered drugs. Part B also covers the flu and pneumococcal shots. Generally, Medicare drug plans PDP cover other vaccines, like the shingles vaccine, needed to prevent illness.

- Medicare Part A (Hospital Insurance) or Part B generally doesn’t cover self-administered drugs you get in an outpatient setting like in an emergency room, observation unit, surgery center, or pain clinic.

- Publication 11109 Your Gidee to Medicare Prescription Drug Coverage Page 12 – above right on this webpage

- medicare.gov/prescription-drugs-outpatient

- Your Medicare Benefits – Prescription Drugs – Outpatient

- How Medicare Covers Self-Administered Drugs Given in Hospital Outpatient Settings Publication 11333

- Medicare Part B Home Infusion Therapy Services With The Use of Durable Medical Equipment CMS.gov

- What about an infusion at my doctors office of remicade (Infliximab) for Crohn’s or IBS Irritable Bowel Syndrome?

- Medicare covers most physician-administered drugs like REMICADE® under Medicare Part B. There are comprehensive published Part B coverage policies specific to REMICADE®. Copies of coverage policies (for example, local coverage determinations, or LCDs) are available on your regional Medicare Administrative Contractor’s, or MAC’s website.

- Medicare typically places few restrictions on REMICADE® coverage. However, some Medicare policies may limit coverage of REMICADE® to certain diagnoses, such as:

- Crohn’s disease

- Ulcerative colitis

- Rheumatoid arthritis

- Ankylosing spondylitis

- Psoriatic arthritis

- Plaque psoriasis

- You can check your regional MAC website for coverage policies for REMICADE® noridianmedicare.com/biologicals-injections or call Janssen Care Path at 877-CarePath (877-227-3728) for more assistance. janssen care path.com/

- What about:

- platelet-rich plasma (PRP) injections for osteoarthritis?

- No, it’s experimental, investigative and medical necessity issues – References Plain English Dr. Prpusa.com * Healthline.Com * CMS.Gov * Blue Cross MA *

- Corticosteroid injections for osteoarthritis of the knee: Mayo Clinic

- Yes, if Medically Necessary. References:

- Some of the things Medicare may require for a back pain treatment to be covered include:

- The treatment must be medically necessary

- Your pain must be of a certain level and/or duration (i.e., if the pain is chronic – lasting 6 weeks or more)

- You have tried less-invasive interventional treatments first (i.e., physical therapy) and they’ve been unsuccessful

- The treatment you receive to be done a certain way Learn More: * Dayton Orthopedic Surgery.com

- Cost range $85 to $149 Medicare.Gov Cost Tool

- Some of the things Medicare may require for a back pain treatment to be covered include:

- Yes, if Medically Necessary. References:

- Hyaluronic Acid (Injection Route) Cleveland Clinic

- Yes, but it’s complicated! Plain English LA Times editorial * Synvisconehcp.com * CMS.Gov * * Part B Step Theraphy Programs * John Hopkins Jurisdiction Specific Medicare Part B *

- platelet-rich plasma (PRP) injections for osteoarthritis?

More Detail & Info

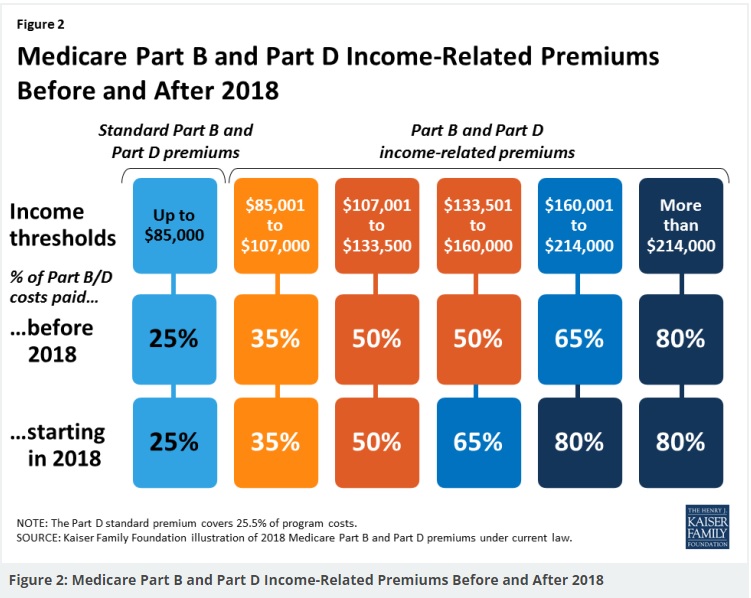

Source – Note the graph isn’t for 2024…

- Graphic courtesy of KFF – Read more

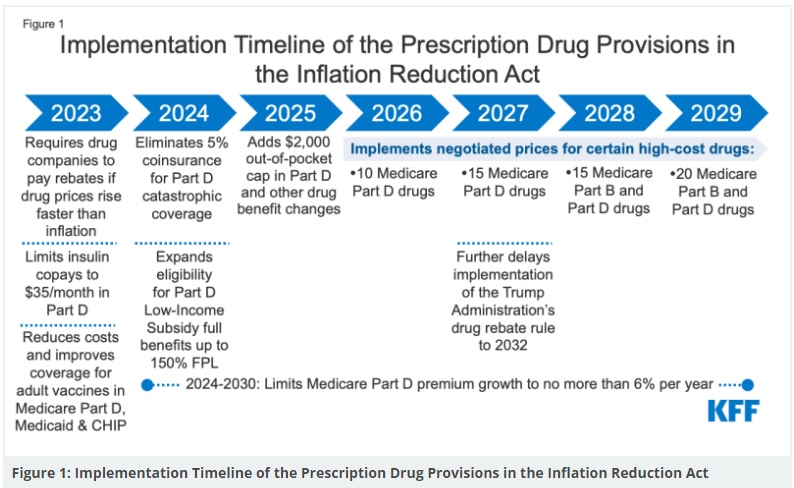

- CMS Finalizes Payment Updates for 2025 Medicare Advantage and Medicare Part D Programs

- Part D Redesign Program CMS.Gov

- 2025 Part D Redesign Program Instructions Fact Sheet

- Changes to Medicare Part D in 2024 and 2025 Under the Inflation Reduction Act and How Enrollees Will Benefitorg

- Guidance on Inflation Reduction Act’s Medicare Prescription Payment Plan Released Medicare Rights.org

- kff.org/key-facts-about-medicare-part-d-enrollment-and-costs-in-2022

- You enter the donut hole when you and your plan spend a total of $5,030 in 2024.

- In the donut hole, you pay up to 25% out of pocket for all covered medications.

- You leave the donut hole once you’ve spent $8,000 out of pocket for covered drugs in 2024.

- 2024 is the last year for the donut hole. A $2,000 out-of-pocket cap takes effect for Medicare Part D in 2025. Nerd Wallet *

- kff.org/key-facts-about-medicare-part-d-enrollment-and-costs-in-2022

- healthaffairs.org/understanding-drug-pricing-package

- Medicare negotiating drug prices? Prepare for a letdown LA Times

- Merck is suing the federal government over a plan to negotiate Medicare drug prices, calling the program a sham equivalent to extortion. LA Times

- nbcnews.com/drug-prices-might-not-help

- cnbc.com/medicare-historic-new-powers

- khn.org/drug-pricing-measures

- centralmaine.com much-needed-step-toward-lowering-prescription-drug-costs

- california healthline.org/300-billion-medicare-drug-price-negotiation

- usa today.com/lower-medicare-drug-costs-seniors

- cnet.com/important-medicare-changes

- Medicare negotiating drug prices? Prepare for a letdown LA Times

- reuters.com/newly-launched-us-drugs-head-toward-record-high-prices

- webmd.com/have-sex-now

- Medicare Part D beneficiaries projected to pay lower out-of-pocket costs A provision in the IRA would ameliorate the out-of-pocket spending increases when people transition from commercial insurance to Part D. READ MORE

- 9 ways the Inflation Reduction Act affects Medicare coverage, and what it means for you Nerdwallet 8/2022

- Here are 25 Medicare Part D drugs that have skyrocketed in price

- Regulations Take Aim At Misleading Medicare Ads As Enrollment Opens

- BLUE SHIELD OF CALIFORNIA UNVEILS FIRST-OF-ITS-KIND MODEL TO TRANSFORM PRESCRIPTION DRUG CARE; SAVE UP TO $500 MILLION ON MEDICATIONS ANNUALLY

- Key Facts About Medicare Part D Enrollment, Premiums, and Cost Sharing in 2024 Kff

Parent, Child & Related Pages

https://business.kaiserpermanente.org/california/healthy-employees/pharmacy/prescriptions-behavior-modification

https://www.facebook.com/WhiteHouse/posts/pfbid0oab6L3kkoVxf5bT1g3v1DswhyRwETiBbroHcD4pBwZDneSMv5fQ6MsFAGKwTfEzZl

https://www.medicarerights.org/medicare-watch/2025/09/25/final-rule-and-new-special-enrollment-period-will-aid-those-misled-by-provider-directories#:~:text=Important%20New%20Special%20Enrollment%20Period,that%20the%20directory%20was%20wrong.

https://www.cms.gov/files/document/application-medicare-part-part-b-special-enrollment-period-exceptional-conditions.pdf

https://www.cms.gov/files/document/cms-10797-application-medicare-part-and-part-b-special-enrollment-period-exceptional-conditions.pdf

https://youtu.be/uzBeYZh4BZc?si=hh0kipsDPLwOxDOO