Medicare High Income Penalty SURCHARGES “IRMAA”

for Part B Doctor Visits & Part D Rx Premiums

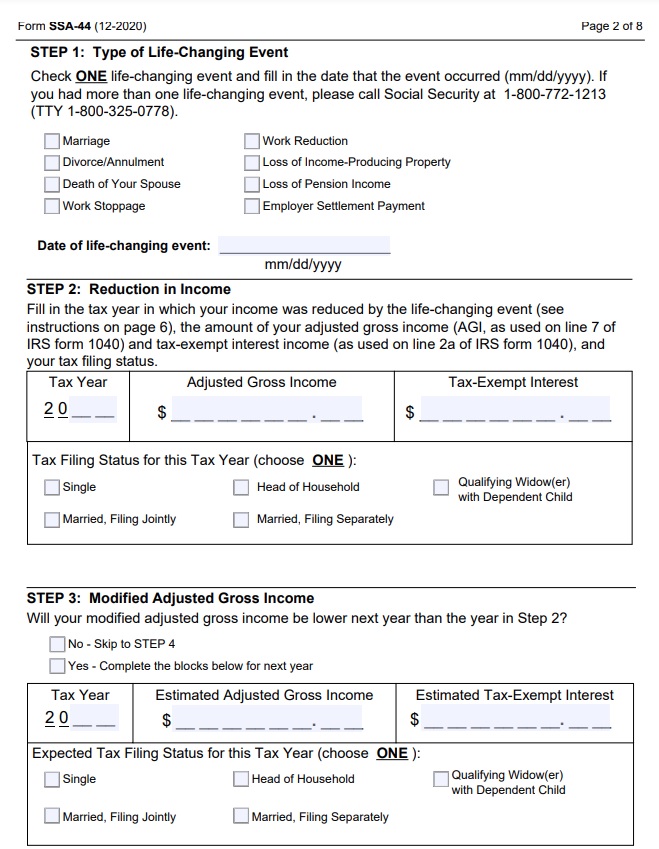

- What to do if you think your #income is incorrect Publication 10125

- Here’s or webpages on the penalty’s if

- you don’t sign up for Part A when you don’t get it “free” or

- for enrolling in Part B later than you’re supposed to, regardless of income

- Part D late enrollment penalty

- FAQ’s

Try turning your phone sideways to see the graphs & pdf's?

Waiver Form – Ask Medicare to Reconsider

How and when you get billed for the surcharge

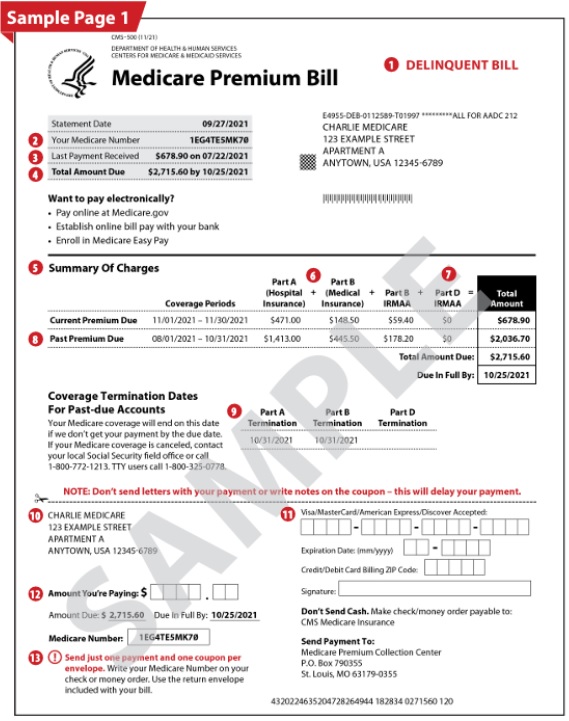

Understanding your Medicare Premium Bill

- Medicare has more detail on your billing statement at these links on the Internet:

- medicare.gov/11659-understanding-cms-500-trifold

- hhs.gov/11659-understanding-cms-500

- Medicare Premium Bill CMS 500

- cms.gov/cms 500

- medicare.gov/11659-understanding-cms-500-trifold

- Steve's YouTube VIDEO to explain late payments...

- What are the payment options to pay the Part B Premium?

- medicare.gov/How to pay Part B premiums and when

- What if you pay Medicare late?

- For Original Medicare (parts A and B), Medicare sends a person an initial bill. If you pay it late, you will get a second bill, which includes the past-due premium amount and the premium that is due the following month.

- If a person does not pay the second bill by the 25th day of the month, they will receive a Delinquent Bill. People who do not pay the Delinquent Bill by the 25th day of the next month will lose their Medicare coverage.

- Basically, you may get your first bill for 4 or 5 months. After that it's monthly if taken from your Social Security Check and quarterly if you get a bill via USPS mail.

- Coverage Termination Date: You’ll only see this notification if your payment is 90 days past due. If you don’t pay the full balance of the “Total Amount Due” by the “Due In Full By” date, your Medicare coverage will be terminated.

- Easy Pay Premium Statement CMS 20143

- Medicare Premium Bill CMS 500

- Why is my first bill higher than I expected?

- After you sign up for Medicare, your first bill might include premiums owed for previous months not already billed. That means the bill might be higher than you expected.For example:

- If you sign up for Medicare in February and your coverage begins February 1st, your premium will be billed quarterly, and your first bill will be dated March 28. It will arrive around April 10 and be due April 25. This bill will be for the upcoming 3 months and include any premiums you weren't previously billed for.

- That means your first bill would include the previous amount owed (for February, March, and April) and what you owe for the upcoming 3 months (May, June, and July). Moving forward, your future bills will only be for 3 months at a time. Learn More>>> Medicare.gov

- After you sign up for Medicare, your first bill might include premiums owed for previous months not already billed. That means the bill might be higher than you expected.For example:

- Why did the Part B premium go up to $170? in 2022 Los Angeles Times

- Live Chat with Medicare - Call 1 800 Medicare

- What if you don't pay...

-

1. How long before Medicare cancels Part B for non-payment

Medicare does not cancel immediately when premiums stop.

Typical sequence:

Month 1

- Premium not paid.

Month 2–3

- CMS sends delinquency notices.

Around Month 3

- CMS sends a termination warning notice.

About Month 4

- Part B terminates for non-payment.

Important detail:

- Termination is retroactive to the last month paid.

Example:

Month Event January last premium paid Feb–Apr no payments May termination processed Coverage ends January 31 That’s why people often suddenly get large premium bills.

- Scroll down to the bottom of our Medicare B page for more detail on reinstating...

#Medicare Related Pages

- Medicare – Introduction – Part A Hospital – B Outpatient – D Rx Medi Gap & MAPD

- Coverage in Part A Hospital & B Doctor Visits? Part D Rx

- Enroll ONLINE for Medicare Part A Hospital & B Doctor Visits

- Medi Gap – Supplement Plans – non conical

- Medicare Advantage Plans – Part C

- Part D Rx Prescriptions no index

Government Brochures on Part D Rx & Medi Gap

Introduction to #MediGap

Publication 02110

- 2025 Official Medicare Guide to choosing a Medi Gap Policy # 02110

- MORE Information and Links

- Matrix - Spreadsheet of what Medicare Pays, Medi Gap pays and what little you pay

Prescription Drug 2025 #RxGuide

PDF # 11109

*****************

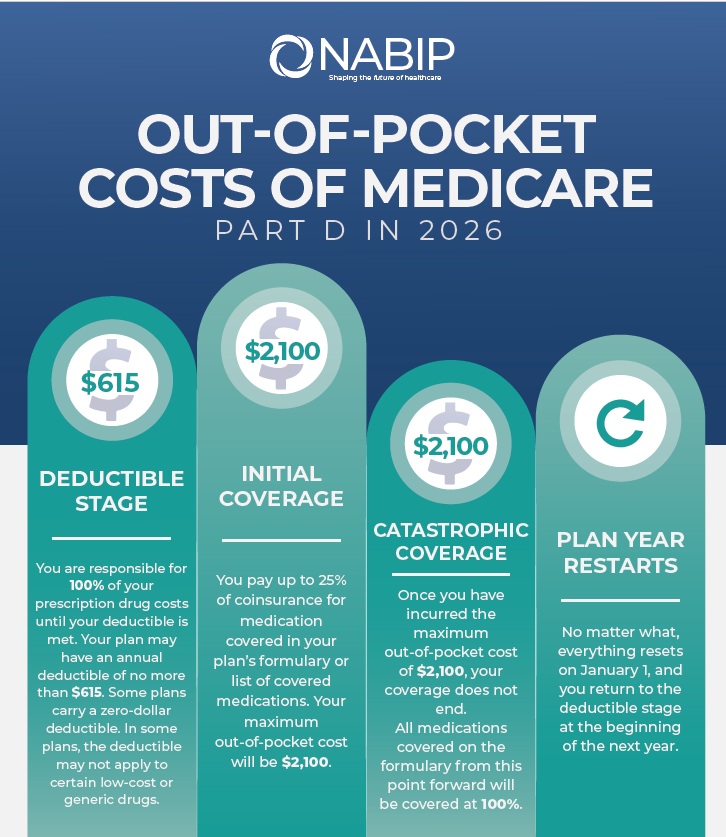

No more Coverage Gap - Donut Hole $2,100 Cap

******************

- Medicare Part D Rx premiums can be found on Medicare . Gov See instructions on how to shop premiums.

- Scope of appointment - permission to discuss Rx and MAPD Plans

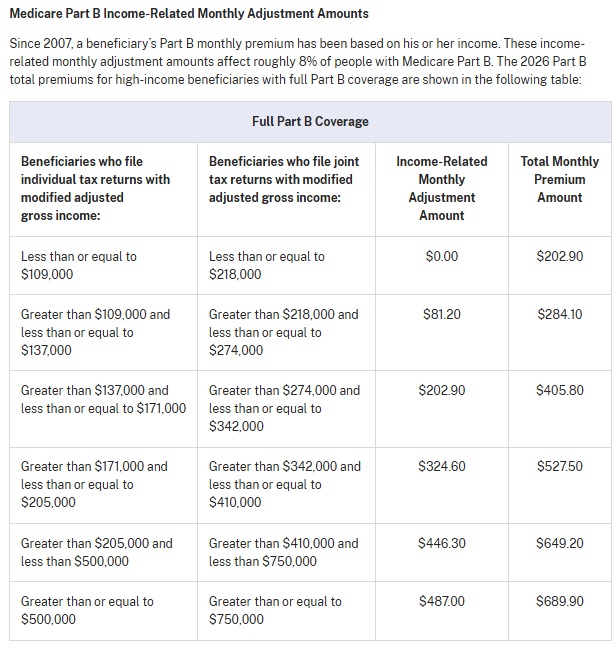

- Our Webpage Premiums for those with High Income Parts D Rx & B Doctor Visits

- Medicare Rules for High Income People Medicare Costs # 11579

- Our #High Income Surcharge Video Explanation

- Kaiser Foundation Introduction - Overview

- Fact Sheet Medicare Part D CA Health Care Advocates Hi Cap

-

. Prescription Drugs Hi Cap

- Medicare Part D: An Overview – 10-31-23

- Prescription Drug Resources – 11-07-22

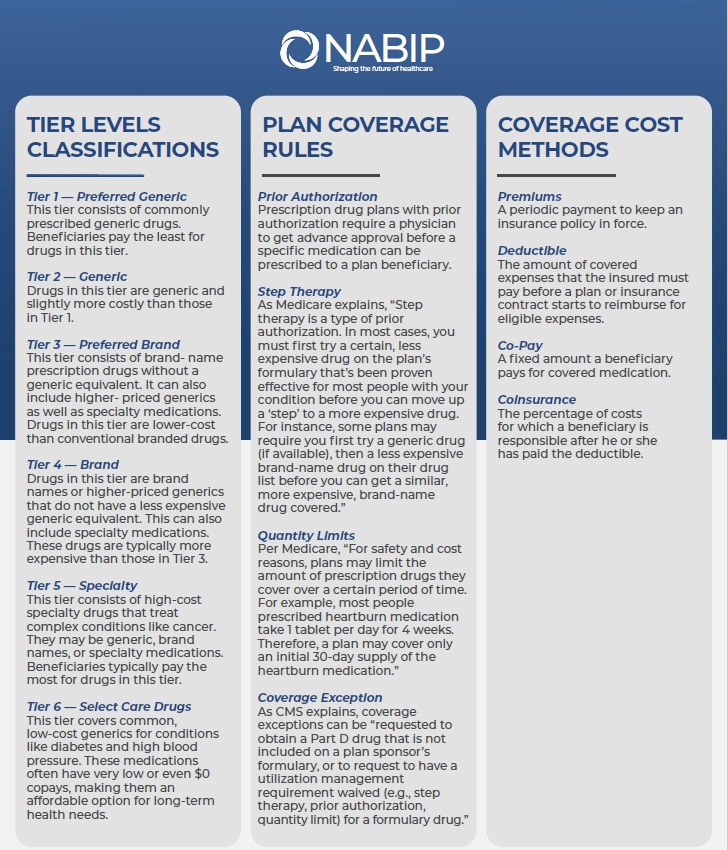

- When Your Part D Prescription is Denied– 11-22-22

- Shop & Compare Tools Part D Rx

- Get Instant Quotes, Information & Enroll online

- See our web page on Part D Shop & Compare for more information & FAQ's

- MANDATED wording!: ‘‘We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1–800–MEDICARE to get information on all of your options.’’ § 422.2267(e)(41).

- We disagree with the above wording, as we can use the same tools on Medicare.gov as they do!