Married Filing Jointly and Covered California Subsidies

The general rule is straightforward: If you are legally married at the end of the tax year, you and your spouse generally must file a joint federal income tax return to qualify for a Covered California premium tax credit.

Filing as Married Filing Separately normally means you cannot claim the premium tax credit. Limited exceptions may apply when:

- You qualify to be treated as unmarried under federal tax rules and file as Single or Head of Household.

- You are living apart and cannot file jointly because of domestic abuse.

- You are living apart and cannot locate your spouse after reasonable efforts, which the IRS calls spousal abandonment.

The short questionnaire below provides a general direction. It does not calculate your taxes or replace advice from a qualified tax professional.

When Might the Joint-Filing Rule Not Apply?

The exceptions are limited. Living separately, having separate finances, or being estranged does not automatically make someone eligible for a Covered California premium tax credit while filing separately.

1. You are not considered married for federal tax purposes

- You were divorced by the end of the tax year.

- You were legally separated under a decree that is recognized for federal income-tax filing purposes.

2. You qualify to be treated as unmarried

Certain married people living apart may qualify to file as Single or Head of Household under federal tax rules. Requirements concerning the home, living arrangements, expenses, and a qualifying person may apply.

3. Domestic abuse or spousal abandonment applies

A person filing Married Filing Separately may still qualify for the premium tax credit when all applicable IRS requirements are satisfied. These generally include:

- You are living apart from your spouse when you file the tax return.

- You cannot file jointly because of domestic abuse or spousal abandonment.

- You certify the exception on IRS Form 8962.

- You have not exceeded the three-consecutive-year limit for using this exception.

Read the current IRS Publication 974 explanation of the Premium Tax Credit and the Instructions for IRS Form 8962.

Domestic Abuse and Spousal Abandonment

Domestic abuse can include more than physical violence

For purposes of this premium tax credit exception, the IRS explanation includes physical, psychological, sexual, and emotional abuse. It can include attempts to control, isolate, humiliate, intimidate, or undermine a person’s ability to reason independently.

What is spousal abandonment?

The IRS generally describes spousal abandonment as being unable to locate your spouse after reasonable diligence. Merely having little contact, disagreeing with your spouse, or living at different addresses may not be enough.

Keep records with your tax files

Do not attach private records to the tax return unless instructed to do so. Depending on the circumstances, useful records might include:

- A protective or restraining order.

- A police report.

- A doctor’s report or letter.

- A statement from someone familiar with the abuse or its effects.

- A statement from someone familiar with the abandonment or efforts to locate the spouse.

Review the current IRS Form 8962 instructions before claiming an exception.

What if Covered California Already Paid a Subsidy?

Covered California may have paid advance premium tax credits directly to your insurance company during the year. The final credit is determined when the federal tax return and IRS Form 8962 are completed.

If you file Married Filing Separately and do not qualify for an exception, you generally cannot claim the premium tax credit. Some or all of the advance credit may have to be repaid. The exact tax result depends on the applicable tax-year rules and how the policy and advance credit are allocated.

- Review our page explaining Covered California subsidy reconciliation and IRS Form 8962.

- Review the official IRS Form 8962 instructions.

- Ask a qualified tax professional to determine the correct filing status and repayment calculation.

Steve Shorr Insurance can help with Covered California plans and enrollment, but does not prepare tax returns or determine your federal filing status.

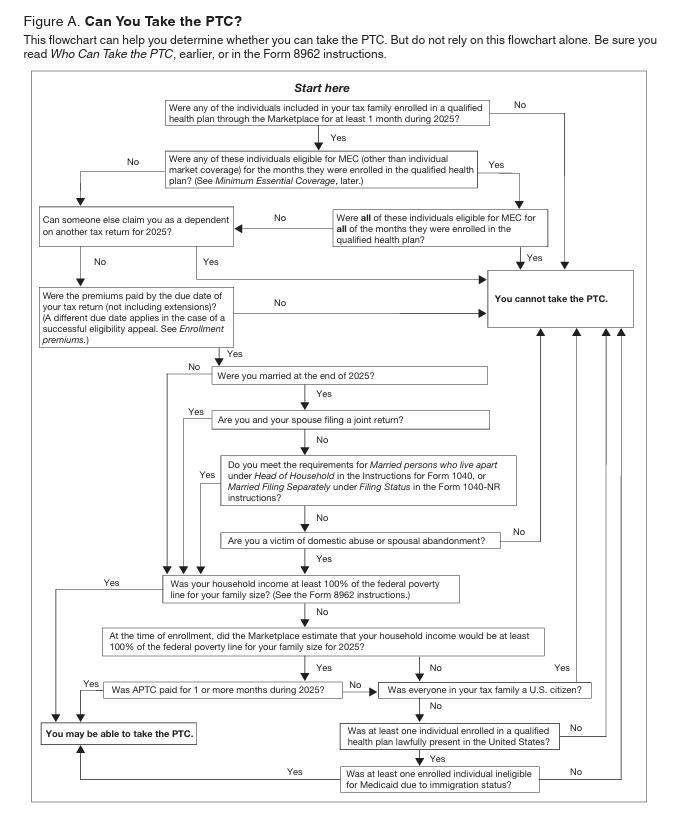

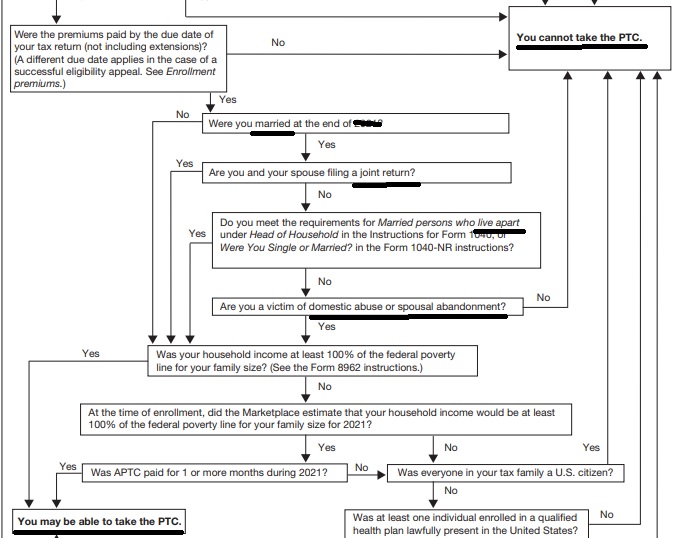

Prefer the Official IRS Flowchart?

The IRS flowchart below shows the broader process for determining who may claim the Premium Tax Credit. It contains more technical language than the explanation above, but it is useful for readers who want to follow the official decision process.

Need Help With Covered California Coverage?

Steve Shorr Insurance can help California residents review health plan choices and Covered California enrollment options. There is generally no additional charge to have Steve assist as your Covered California agent.

- Compare available health plans and premiums.

- Estimate premiums using your expected household information.

- Review how to appoint Steve as your Covered California agent.

- Get help reporting insurance-related household or coverage changes.

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

Married Couples must file Jointly to get ACA Subsidies

See below for exceptions

|

health care.gov who to include on your application (2) Married taxpayers must file joint return. A taxpayer who is married (within the meaning of section 7703) at the close of the taxable year is an applicable taxpayer only if the taxpayer and the taxpayer’s spouse file a joint return for the taxable year. GPO.Gov Final Regulations Page 11 * Turbo Tax Calculator Tax Policy Center….. Joint or separate? Married Filing Separately.If you file as married filing separately and are not a victim of domestic abuse or spousal abandonment (see Exception 2—Victim of domestic abuse or spousal abandonment under Married taxpayers above), then you are not an applicable taxpayer and you cannot get the subsidy. * IRS Publication 974 Page 7 * Instructions 8962 *

Not Considered MarriedYou are not considered married for federal income tax purposes if you are divorced or legally separated –Divorce * CA Courts * Definition San Francisco Court * attorney Website * according to your state law under a decree of divorce or separate maintenance. In that case, you cannot file a joint return but may be able to take the PTC on your separate return. See Pub. 501, Exemptions, Standard Deduction, and Filing Information.

Single. Normally this status is for taxpayers who aren’t married, or who are divorced or legally separated under state law. Head of Household. In most cases, this status applies to a taxpayer who is not married, but there are some special rules.

For example, the taxpayer must have paid more than half the cost of keeping up a home for themselves and a qualifying person. Qualifying Widow(er) with Dependent Child This status may apply to a taxpayer if their spouse died and they have a dependent child. Other conditions also apply. The “Filing” tab on IRS.gov can help with many taxpayers’ federal income tax filing needs. The Interactive Tax Assistant tool can help taxpayers choose the right filing status.

Scroll down for more details on the exceptions. |

|

|

|

What if I don’t have contact with my #estranged spouse,

do we still have to file jointly to get the tax subsidies?

Exception 1—Certain married persons living apart.

You may file your return as if you are unmarried and take the PTC if one of the following applies to you.

- You file a separate return from your spouse on Form 1040 or Form 1040A because you meet the requirements for Married persons who live apart under Head of Household in the instructions for Form 1040 or Form 1040A.

- You file as single on your Form 1040NR because you meet the requirements for Married persons who live apart under Were You Single or Married? in the instructions for Form 1040NR..

- Exception 1—Certain married persons living apart.

Exception 2—Victim of domestic abuse or spousal abandonment.

If you are a victim of domestic abuse or spousal abandonment, you can file a return as married filing separately and take the PTC if all of the following apply to you.

- You are living apart from your spouse at the time you file your 2016 tax return.

- You are unable to file a joint return because you are a victim of domestic abuse (described next) or spousal abandonment (described below).

- You check the box on your Form 8962 to certify that you are a victim of domestic abuse or spousal abandonment.

- Exception 2—Victim of domestic abuse or spousal abandonment.

- Domestic abuse.

-

Insurance Companies cannot discriminate against

victims of #domestic abuse, regardless of sex. (Woods v Horton * Woods v Sherry pdf ) npr.orgCA Insurance Code § 10144.2

(a) No disability insurer covering hospital, medical, or surgical expenses shall deny, refuse to insure, refuse to renew, cancel, restrict, or otherwise terminate, exclude, or limit coverage or charge a different rate for the same coverage, on the basis that the applicant or insured person is, has been, or may be a victim of domestic violence.

(c) As used in this section, “domestic violence” means domestic violence, as defined in Section 6211 of the Family Code. Abuse 6203 Definition

See also Health & Safety Code 1374.75

CA Insurance Code 676.9.

-

Spousal abandonment.

Records of domestic abuse and spousal abandonment.

If you checked the box in the upper right corner of Form 8962 indicating that you are eligible for the PTC despite having a filing status of married filing separately, you should keep records relating to your situation, like with all aspects of your tax return. What you have available may depend on your circumstances. However, the following list provides some examples of records that may be useful. (Do not attach these records to your tax return.)

- Protective and/or restraining order.

- Police report.

- Doctor’s report or letter.

- A statement from someone who was aware of, or who witnessed, the abuse or the results of the abuse. The statement should be notarized if possible.

- A statement from someone who knows of the abandonment. The statement should be notarized if possible.

- Records of domestic abuse and spousal abandonment.

This all goes beyond our pay grade. Click on the link for VITA.

- Example.

- Rules for the Married Taxpayers Not Filing a Joint Return and Also Allocating With Another Taxpayer.

- Health Care.gov says you don’t have to include a legally separated spouse!.

- Publication 974 Premium Tax Credit pdf HTML.

- Modified Adjusted Gross Income Definition – Line 37* 1040

- 1040 Instructions

- VITA free-tax-return-preparation-for-you-by-volunteers

IRS Publication # 504

#Divorced or Separated Individuals

pdf * (HTML)

- Community Property – Publication 555

- QDROs The Division of Retirement Benefits Through Qualified Domestic Relations Orders Dol.gov pdf

- Publications Dol.gov

- CA Court Self Help Website – Divorce

-

Dependent Care Benefits Publication # 503

- Nolo - Child Support & Custody

- Automatic Restraining Orders prohibiting changing insurance once divorce is filed fl 110

- AB 1297 Automatic temporary restraining orders Effective 1/1/2026

- Existing law blocks both parties from canceling or changing insurance policies, cashing in or borrowing against insurance or changing beneficiaries on insurance that benefits either party or their children.

- Effective Jan. 1, 2027, the law will also prohibit either party from letting insurance expire by not paying the premiums or failing to renew the policy. Sacramento Observer *

- Frequently Asked Questions for Declarations of Disclosure in California Wilkinson Esq *

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

Jump to section on:

| Estranged Spouse |

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

California Tax Information Registered Domestic Partners

#737

Federal IRS

- Q1. Can registered domestic partners file federal tax returns using a married filing jointly or married filing separately status?

- A1. No. Registered domestic partners may not file a federal return using a married filing separately or jointly filing status. Registered domestic partners are not married under state law. Therefore, these taxpayers are not married for federal tax purposes. IRS.gov *

- More Federal IRS FAQ's

- Our webpage on Registered Domestic Partners – Spousal Health Coverage?

- ftb.ca.gov/registered-domestic-partner

- Section 106 Deduction for Group Health Plans