California Employer Health Insurance Waiting Period Rules

If you are setting up a California employer group health plan, one of the most common questions is:

“How long can a new employee wait before becoming eligible for health insurance?”

The short answer is that group health coverage generally cannot be delayed indefinitely. Federal law limits waiting periods, and California employers must also follow carrier-specific enrollment rules. The actual effective date often depends on the employee’s hire date and the carrier’s enrollment procedures.

Quick Answer

Most California employer health plans offer waiting period choices such as:

- Coverage effective the 1st of the month following date of hire

- Coverage effective the 1st of the month following 30 days

- Coverage effective the 1st of the month following 60 days

- Other options that still comply with federal waiting-period limits

Because many carriers only begin coverage on the first day of a month, a “90-day probationary period” can sometimes create compliance issues if not calculated correctly.

Orientation Period vs Waiting Period

Many employers confuse an orientation period with a waiting period. They are not necessarily the same thing.

An employer may have an initial orientation period for a newly hired employee before the employee becomes eligible for health coverage. After that orientation period ends, the waiting period rules apply.

Always review your carrier’s current employer administrative guide because carrier implementation can vary.

Common Employer Questions

Can I make a new employee wait 90 days?

Possibly, but many carriers structure eligibility dates around the first day of a month. The actual effective date must still comply with applicable waiting-period rules.

What if the employee declines coverage?

Always obtain a signed waiver and keep it with your employee records.

What if HR forgets to enroll the employee?

Enrollment mistakes can become expensive. Employers should maintain enrollment forms, waiver forms, hire dates, eligibility records, and proof of coverage offers.

Can different employees have different waiting periods?

Generally, employers choose one eligibility approach that applies consistently to similarly situated employees.

Source: See carrier-specific employer rules and employer applications for available waiting-period option

Citations & Sources

- 42 U.S. Code § 300gg-7 – Prohibition on Excessive Waiting Periods

- California Senate Bill 1034 – Waiting Periods

- California Health & Safety Code §1357.51

- Employer Group Health Insurance Carriers – Check Each Carrier’s Current Rules

- Employer Applications – Choose Waiting Period Option

- Date Calculator – Add or Subtract Days

Related Employer Health Insurance Resources

- Employer Small Group Health Plans Introduction

- Employer Group Health Insurance Companies & Carriers

- Participation & Contribution Requirements

- 1099 Independent Contractor vs Employee Definition

- Late Enrollee & Special Enrollment Rules

- Dependent Definition & Adding Family Members

- COBRA & Cal-COBRA Rules

- Anthem Blue Cross Employer Plans

- Blue Shield Employer Group Plans

- Kaiser Permanente Employer Administration

- UnitedHealthcare Employer Plans

- Covered California SHOP Plans

Historical Research & Previous Versions

The Affordable Care Act generated significant confusion regarding waiting periods, probationary periods, orientation periods, and employer eligibility rules. If you would like to review older versions of this page, historical documents, or prior regulatory guidance:

View Historical Versions of This Page on Archive.org

Need Help Setting Up a California Employer Health Plan?

Steve Shorr Insurance has been helping California employers since 1981. We can help you compare carriers, understand waiting-period rules, add or terminate employees, review participation requirements, and obtain small-group health insurance quotes.

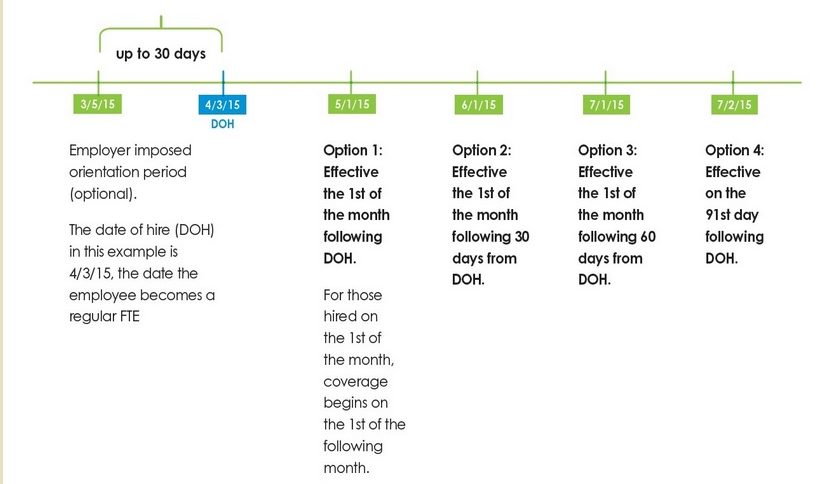

MAXIMUM 90 DAYS waiting period for

new employees to get on Group Health Plan

Maximum 90 Day Wait for New Employees

Example

Here’s other companies options check their Employer Application Quotit.

|

There is MAXIMUM of 90 DAYS waiting period for new employees to be enrolled on Employer Group Health Coverage 8.15.2014 SB 1034 * §2708 * Health & Safety Code 1357.51 (c) Anthem Explanation from their Administrative manual (scroll down) as an example. Check your own contracts, policies, paper work, Company Manuals, Employee Manuals, eoc, etc. Employer orientation and/or waiting periods Pursuant to SB 1034 (2014), Anthem will not impose a waiting period. Groups are responsible for providing Anthem with accurate member eligibility dates, taking into account any group-imposed orientation and/or waiting period. An employer may impose bona fide employment-based orientation (affiliation) period for new employees which cannot exceed 30 days. If the employer imposes an orientation period when completing the application the “date of hire” is the first day after completion of the orientation period. A waiting period may also be imposed before coverage becomes effective, beginning the first day after any orientation period however, cannot exceed 90 days. In accordance with SB 1034, groups are responsible for ensuring that any group-imposed waiting period is consistent with Section 2708 of the Federal Public Health Service Act(42 U.S.C. § 300gg-7). The following are the waiting period options:

You have the option to waive the waiting period for all new hires at the initial group enrollment only. You may only choose one waiting period for your employees; dual orientation and/or waiting periods aren’t allowed. Your group’s orientation and/or waiting period is applied to all employees in the group, with no exceptions for any eligible employee. Scroll down for a simplified chart of your options that comply with the law. Generally, 1st of the month after date of hire, 1st of month after 30 days, 60 days. |

Check the administration page for the company who have – want to check out or check all company Employer Enrollment applications. The interpretations and implementation can be quite confusing.

Insurance Company Bulletins

|