Aged, Blind & Disabled Medi-Cal Program

Full-Scope Medi–Cal Health Benefits global

- See the My Medi Cal brochure for details & Benefits

- The Aged and/or Disabled Federal Poverty Level Program (See Income Chart) (A&D FPL) serves individuals aged 65 and older, and persons with disabilities.

- To qualify for this program, individuals Must meet all of the following three criteria:

- Be aged (65+) or

- disabled (meet Social Security’s definition of disability, even if your disability is blindness).

- If you are on SSI you get - Automatic Qualification for Medi Cal

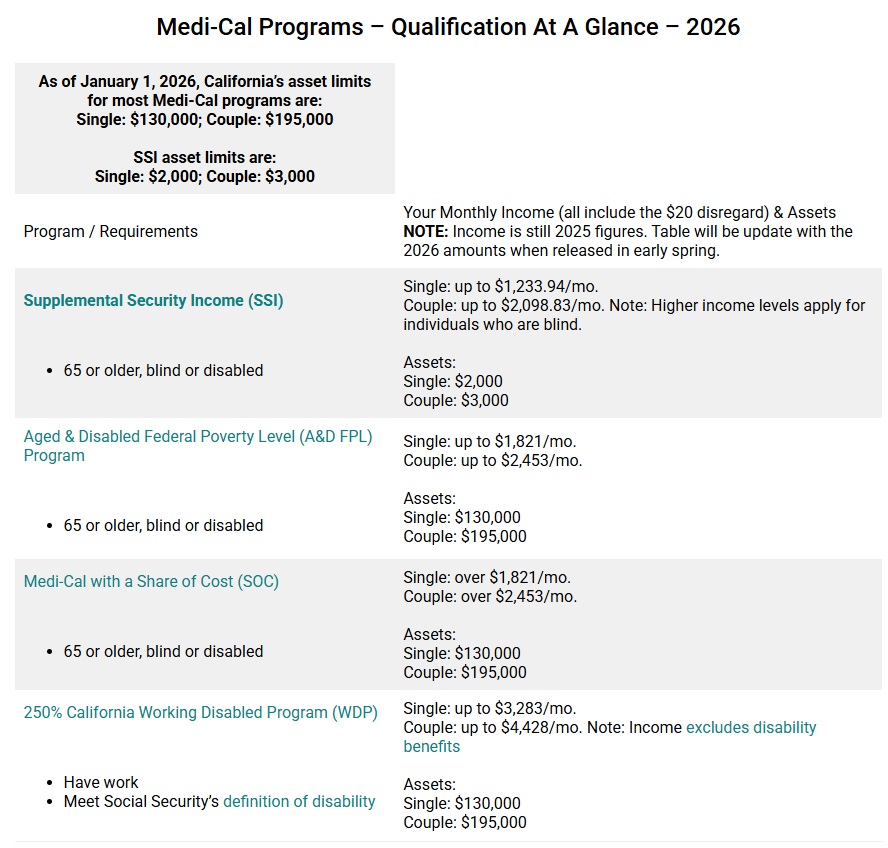

- 2026 Asset Limits are back Learn More our webpage

- Worksheets for Determining Eligibility Under the Aged & Disabled Federal Poverty Level (A&D FPL) Medi-Cal Program Disability Rights *

- Qualifications at a Glance 2026 Cal Health Care Advocates.com

Resources & Links

- CANHR.org - Fact Sheet

- CA Health Care Advocates

- Kaiser Foundation

- Does Integrating Medicare and Medicaid Improve Care for Dual Eligibles?

- DHCS.CA.Gov

- Disability Benefits 101

- BenefitsCal online enrollment

-

Medicare And Disabilities

Visit our webpage on the Working Disabled Program and lowering your share of cost

#My Medi-Cal

How to get the Health Care

You Need

24 pages

Smart Phones - try turning sideways to view pdf better

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

FAQ’s

FAQ’s

Question

My tax person informed me that claiming my 81 year old father-in-law as a dependent on my taxes would not affect his eligibility for A&D – Aged & Disabled FPL Full Scope – Federal Poverty Level Medical-cal. Is this true?

Similar situation in regards to claiming my mother. She receives SSI/SSDI and receives medical Medi-Cal . Would claiming her as a dependent affect her eligibility for medi-cal

Answer

See Chapter 3 – Western Poverty Law Center on Health Insurance for Low Income. See also Social Security’s website on SSI

Does your Mom get SSI or SSDI, it makes a difference. SSI is dealt with here. See also Social Security’s website on SSI for income & resource information.

SSI

Eligibility![]() Benefits

Benefits![]() Resources

Resources![]() Income

Income![]() Living Arrangements

Living Arrangements

SSDI gives one Medicare after two years.

We don’t get paid to help people with Medi-Cal, SSI or SSDI. When you read the manual, be sure to read it 3x and when you think you understand it, read it again. We’ve only skimmed the material

Question

I am 70 years of age and have been on medi cal due to low income. I recently applied for my ex husbands social security and my income increased to $1,379.10. Can I still qualify for medi cal?

***Sorry, it looks like you are now over the income limit. See excerpt below. Losing Medi-Cal would give you a Special Enrollment Period into a Medicare Advantage Plan where there are generally no premiums and very little co-pays that we can help you with. You might also qualify for low income subsidies for your prescriptions.

****

Question

What if one qualified for Medi-Cal because of a disability, but wants to opt out and get subsidies in Covered CA or just pay full price during Open Enrollment?

Excerpt of email…

[Covered CA] was advised that since member has disability even if he doesn’t want to be on Medi-cal, he will still be referred to them. … Medi-cal caters for people with disability. The member should ask Medi-cal for possibility of releasing him, unfortunately, it’s not under our control .

Maybe shouldn’t argue with Medi-Cal to say not disabled – could hurt Medicare and Social Security Disability Claim

#Understanding Medicare Advantage Plans (PDF) #12026

- Set a Zoom Meeting

- We can now do SOC Scope of Appointment, before the Meeting via a 3 minute recorded meeting 2 days before. AHIP Training Module 4 Page 14 *

- #Intake Form - Please email us [email protected] for the form - That way we can better analyze your situation to give you the answers to your needs and questions.

- Get Quotes, Full Information and Enroll

- MANDATED wording!: Think Advisor * ‘‘We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1–800–MEDICARE to get information on all of your options.’’

- We disagree with the above wording, as we can use the same tools on Medicare.gov as they do!

- Visit our general webpage on Medicare Advantage for much more detail and information.

Medi Cal & Seniors

- Medi-Cal is California’s Medicaid program, which provides health insurance to individuals and families who earn low incomes, including 40% of the state’s children, half of Californians with disabilities, and over a million seniors. In total, the program covers more than 12 million people, or nearly one in three Californians.

- Medi-Cal also covers a large number of working Californians, many of whom became eligible for the program because of the Affordable Care Act’s Medicaid expansion. Working Californians may be one of the least recognized or understood populations served by the program. In a 2018 poll, 42% of Californians said that they believed that most working-age adults without a disability enrolled in Medi-Cal are unemployed. Twenty percent said they didn’t know. This report combines key findings from survey data with insights from 19 in-depth interviews with enrollees to paint a more accurate and complete picture of working Californians who rely on Medi-Cal, why they came to enroll in the program, and the role it plays in their lives.

- VIDEO

- Working Californians Enrolled in Medi-Cal Share Their Stories

- Chcf Policy at a Glance

Have Medi Cal pay Medicare Part B $185 Premium #Costs # 10126

Medi Cal * Part B Outpatient Premium Forgiveness

- 2026 Reporting Assets to Medicare and Medi Cal Insure Me Keving.com

- How the ‘Medicare Cliff’ is raising costs and worsening health for many older low-income adults

- Medicare.Gov MSP Medicare Savings Programs

- DUALLY ELIGIBLE BENEFICIARIES UNDER MEDICARE AND MEDICAID (Medi Cal) MLN Knowledge Booklet

- cms.gov/QMB Qualified Medicare Beneficiary Programs

- CA Health Care Advocates on MSP

- Minimum Federal Eligibility Requirements for Medicare Savings Programs in 2024

- Save money on your Medicare costs

- CA Department of Aging 1-800-434-0222 -

- Medicare Counseling HICAP State Health Insurance Assistance Programs SHIP

- FACT Sheet Low Income Assistance: Medicare Savings Programs CA Health Care Advocates HI CAP

- Medicare Savings Programs in California

- health care rights.org Serving Los Angeles County

- dpss.lacounty.gov/savings

- Disability Benefits 101

- National Council on Aging MSP

- MSP Medicare Savings Plan CA Health Care Advocates

- khn.org/billions-of-dollars-in-benefits-go-unused

- Our webpage on Part D Rx Extra Help - LIS Low Income Subsidy

- Explanation of countable Income Insure Me Kevin.com

- FAQ

- Will the Aged & Disabled program pay for Medicare Part B Outpatient & Doctor Visits premium of $174?

- See brochure above.

.

- See brochure above.

- Medicare I need help with choosing what my options are.

- Take a look at our webpage on Original Medicare A & B plus Part D Rx and Medi Gap vs Medicare Advantage

- Set up a Zoom Meeting and we can discuss. www.SteveShorr.com/Meeting

- Will the Aged & Disabled program pay for Medicare Part B Outpatient & Doctor Visits premium of $174?

- dhcs.ca.gov/Medicare-Savings-Programs-in-California

- SCAN BROKER ONLY

- medicare.gov/medicare-savings-programs

- Prescription Drug Discount Program for Medicare Recipients Pharmacy.ca.gov *

- kff health news.org/the-pill-club-reaches-18-3-million-medicaid-fraud-settlement-with-california

- Mexican pharmacies sell fentanyl-, meth-tainted pills Fake medications are passed off as legitimate in tourist areas LA Times *

Links & Resources

- Main Webpage on Medicare & Enrollment

- Publication 524 (2023), Credit for the Elderly or the Disabled IRS.Gov *

- Publication 907 (2024), Tax Highlights for Persons With Disabilities IRS.gov *

- Publication 554 (2024), Tax Guide for Seniors IRS.Gov

- Negative MAGI Income Carry Forward Loss Our website

- The Health Consumer Alliance (HCA) is a statewide partnership that offers Free Over the Phone or In-Person Assistance to help California residents struggling to get or maintain health coverage and resolve problems with their plans.

- Disability Rights California (DRC) defends and improves the rights of Californians who have disabilities.

Links – Resources

- Big change in Medi-Cal rules opens the door to more seniors

- CA Health Advocates – Medi-Cal for People who have Medicare

- CANHR.org * Aged & Disabled

- Disability Benefits 101

- Orange County Social Services Agency

- Chart – MAGI and NON-MAGI Qualification for Medi-Cal

- See also our site on Medi-Medi – both Medi-Cal and Medicare

- Insure Me Kevin.com – Friendly Competitor

- How to Report Income Change

- MC 239 Denial of Benefits

- Medi-Cal Eligibilty Procedures Manual Article 22 Disability 179 pages

- Medically Needy Program

- Program for All Inclusive Care For The Elderly

- Welfare & Instituions Code General Provisions [14000 – 14042]

Child & Sibling Pages

- Share of Cost – Eliminate with Dental, Vision Medi Gap Insurance Premiums

- “How to Eliminate Medi-Cal Share of Cost with the 250% Working Disabled Program”

- Appeals Medi Cal

- Calculate Instantly Medi Cal Share of Cost and Zero it out!

- FAQ’s Share of Cost

- How to use medical expenses to lower share of cost

- Medi Gap to lower share of cost Medi Cal IHSS

- proof needed for Medi Cal

- Timing & Redetermination Medi Cal Share of Cost

- SSI – Supplemental Security Benefits – Automatic Medi Cal

- Aged and Disabled Federal Poverty Level Program

- Share of Cost – Eliminate with Dental, Vision Medi Gap Insurance Premiums

- “How to Eliminate Medi-Cal Share of Cost with the 250% Working Disabled Program”

- Appeals Medi Cal

- Calculate Instantly Medi Cal Share of Cost and Zero it out!

- FAQ’s Share of Cost

- How to use medical expenses to lower share of cost

- Medi Gap to lower share of cost Medi Cal IHSS

- proof needed for Medi Cal

- Timing & Redetermination Medi Cal Share of Cost

- SSI – Supplemental Security Benefits – Automatic Medi Cal

- Share of Cost – Eliminate with Dental, Vision Medi Gap Insurance Premiums

- Denti Cal Medi Cal Dental & Vision

- Dual Coverage? Medi Cal?

- MAGI Medi Cal Income Limits

- Medi Cal Report Changes

- Medi Cal Contact Help

- Medi Cal Resources Asset Limits