What are the Legal California Residency Requirements to

Qualify for

Medicare, Medicare Advantage Plan or Medi Gap – Supplemental,

Part D Rx and under 65 Covered CA – Obama Care?

Medicare #Advantage

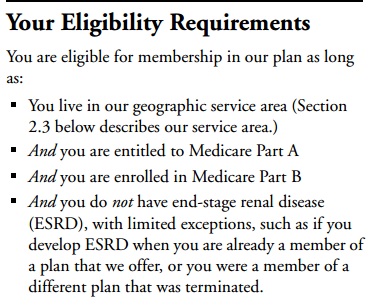

You are eligible to enroll in an Medicare Advantage plan if you permanently reside in the service area (where the plan has doctors and hospitals signed up) of the plan. Vacations or temporary moves do not count. (CMS 20.3) blue shield EOC CMS allows each State to determine the rules for residency in their state.

Definition Residency

- to dwell permanently or continuously : occupy a place as one's legal domicile Webster *

- the act or fact of dwelling in a place for some time

- the place where one actually lives as distinguished from one's domicile or a place of temporary sojourn Webster *

- When the plain meaning of a word lends itself to only one reasonable interpretation, that interpretation controls Guide to Contract Interpretation *

- Be sure to check your ACTUAL EOC Evidence of Coverage Value and how to find

Links & Resources

- Our Webpage on complex Medicare Rules Enrollment Dates, Residency

- Income Tax & Medicare if you live out of country 26 USC 911

- CA Residency Guidelines Publication 1031 pdf

Potential Cancellation if not a CA Resident

Medicare Advantage Plans or Supplement may cancel you when you move out of their service area for more than six months. (Freedom Blue EOC) Check out the rules to keep your current coverage for up to one year. §20.3

See our FAQ’s or ask Questions?

Members Who Change Residence

MA organizations may offer (or continue to offer) extended “visitor” or “traveler” programs to members of coordinated care plans who have been out of the service area for up to 12 months. The MA organizations that offer such programs do not have to disenroll members in these extended programs who remain out of the service area for more than 6 months but less than 12 months. …Organizations offering MA-PFFS plans may allow continued enrollment of individuals absent from the plan service area for up to 12 months,…50.2.1

MA organizations offering plans without these programs must disenroll members who have been out of the service area for more than 6 months.

- A geographic area where a health insurance plan accepts members if it limits membership based on where people live. For plans that limit which doctors and hospitals you may use, it’s also generally the area where you can get routine (non-emergency) services. The plan may disenroll you if you move out of the plan’s service area. Medicare.Gov

- When you move within a state, state to state or return to USA, you are entitled to a SEP (Special Enrollment Period) where you may choose another Medi Gap or Advantage plan, with NO MEDICAL QUESTIONS. 50.2.1 MAPD Rules * Medi Gap * Covered CA & Direct Quotes * Individual & Family Enrollment Periods *

- Enrollment Periods Publication # 11219 Page 7

- Individual & Covered CA Special Enrollment

- Email us [email protected] or navigate this website with your specific questions & proposals if moving to or from CA.

- Jump to section on:

CA Residency Guidelines #FTB1031 2023

- See our webpage on lawful presence & public charge

- A California resident is one who is in California for other than a temporary or transitory purpose; or Domiciled in California, but outside California for a temporary or transitory purpose. (ftb.ca.gov).

- Amount of time you spend in California versus amount of time you spend outside California;

- Location of your spouse and children;

- Location of your principal residence;

- Where your driver's license was issued;

- Where your vehicles are registered;

- Where you maintain your professional licenses;

- Where you are registered to vote;

- Location of the banks where you maintain accounts;

- Location of your doctors, dentists, accountants, and attorneys;

- Location of the church, temple or mosque, professional associations, or social and country clubs of which you are a member;

- Location of your real property and investments;

- Permanence of your work assignments in California; and

- Location of your social ties.

-

In using these factors, it is the strength of your ties and closest connections not just the number of ties, that determines your residency (ftb.ca.gov/)

- Sanjiv Gupta CPA reviews rules related to residency in California

Individual & Covered CA

Covered CA & Individual Residency Requirements

Blue Shield – Covered CA Individual & Family

EOC Evidence of Coverage

|

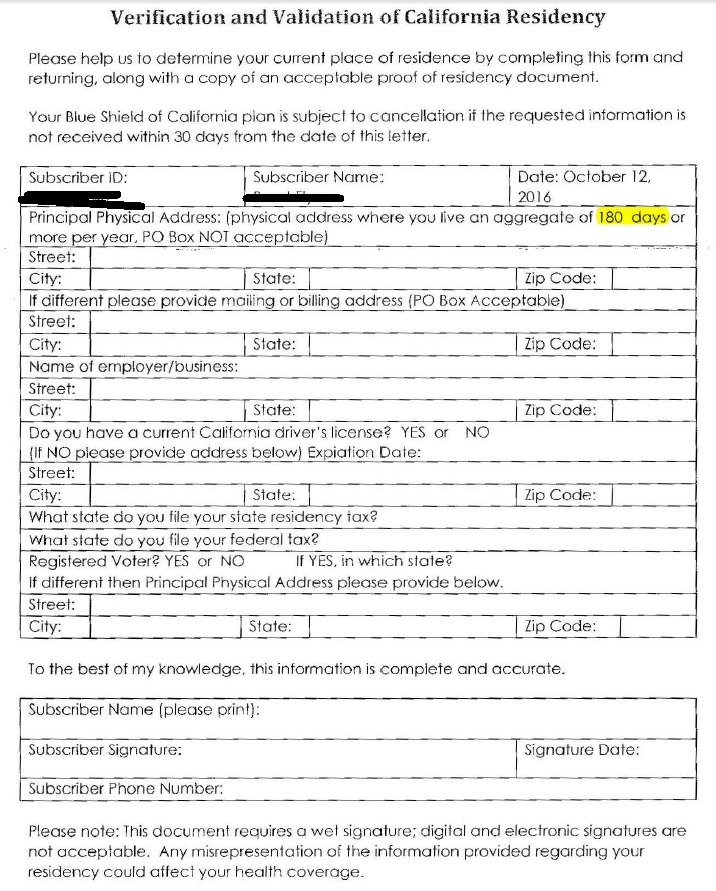

Blue Shield under 65 residency verification

|

Must Reside in the Service Area

|

#Insubuy Travel Health Insurance

Instant Quotes, Details and ONLINE Enrollment

Steve talks about International Travel Insurance VIDEO

US State Department - Travel - Insurance

Our webpage on Travel Insurance

Medicare A & B if you don't #live in USA

Publication 11871

Medicare just visiting Out of County Publication # 11037

- Medicare Abroad: Travel and Living Coverage Explained The Street.com

- medicare.gov/travel-outside-the-u.s.

- Our webpage on Medicare Coverage outside of USA

- FAQ - Buying Medi Gap if you live outside USA

- Get Travel Quotes & Information

*********Social Security*****

Payments if you are living outside of USA # 10137

- What if you work in two or more different Countries?

- International Social Security agreements, “Totalization agreements,” have two main purposes.

-

- First, they eliminate dual Social Security taxation, the situation that occurs when a worker from one country works in another country and is required to pay Social Security taxes to both countries on the same earnings.

- Second, the agreements help fill gaps in benefit protection for workers who have divided their careers between the United States and another country.

- Payments Abroad Screening Tool

- Learn More

Our Webpages on:

FAQ’s

Residency FAQ’s #a41

- Question – Is it legal to be with Covered CA since I am traveling for about 4 months and also not working for rest of the year?

- Background

- I am visiting India at the moment. Because of my current situation wanted your guidance regarding continuation of my Covered CA health insurance.

- I worked in LA , this year, 2023, till Feb 10th.

- Due to personal reasons, I may have to stay back here in India for another 2-3 months and after that I will be going to Michigan in June-July 2023 to help my daughter for the rest of the 2023.

- My income this year may be $ 10,000 + my husband’s Social security of $14000. for 2023.

- I am visiting India at the moment. Because of my current situation wanted your guidance regarding continuation of my Covered CA health insurance.

- Background

- Answer

- If you can earn say $28k or more, for the year, then you would earn enough to stay in Covered CA – See the Income Chart

- When you report lower income 138% of FPL Federal Poverty Level to Covered CA, they would put you in Medi Cal.

- Medi Cal and Covered CA only cover Urgent Care and Emergencies outside of CA – Service Area – Check your EOC Evidence of Coverage

- If you don’t have Medi Cal or Covered CA, you’re not outside the USA long enough to get an exemption from the CA Tax Penalty.

- You might want to consider Travel Coverage while you are in India, better service, not have to pay upfront and cover non emergencies.

- We really need to double check your actual EOC

- When you are in Michigan you can check with Medicaid if under $28k and their version of Covered CA and get coverage there, so that you are not limited to emergencies and urgent care.

- Read over the residency requirements… it shouldn’t be a problem.

- I’ll be in CA next week and can research more thoroughly then.

FAQ

Puerto Rico

- Question What is the status of Puerto Rico for Medi-Gap and Prescription Coverage?

.

. - Answer The “U.S.” includes the 50 states, the District of Columbia, Puerto Rico, the U.S. Virgin Islands, Guam, the Northern Mariana Islands, and American Samoa Medicare & You Page 57

- I like to document everything I say. So, I know that a Medi-Gap policy simply pays based on what Medicare Pays, let’s find that in the policy. Blue Shield “N.” Table of contents is on page 6. Page 12 is benefits

- 1. Blue Shield will pay the following:

- a) Coverage of Part A Medicare Eligible Expenses for hospitalization to the extent not covered by Medicare from the 61st day through the 90th day in any Medicare Benefit Period;

- b) Coverage of Part A Medicare Eligible Expenses incurred for hospitalization to the extent not covered by Medicare for each Medicare lifetime inpatient reserve day used. Each Medicare beneficiary is given sixty (60) lifetime reserve days which begin from the 91st day and after;

- c) Upon exhaustion of the Medicare hospital inpatient coverage including the sixty (60) lifetime reserve days, coverage for the Medicare Part A Eligible Expenses for hospitalization will be paid at the appropriate standard of payment which has been approved by Medicare, subject to a lifetime maximum benefit of an additional 365 days (except that psychiatric care in a psychiatric hospital participating in the Medicare program is limited to 190 days during the Subscriber’s lifetime);

- d) Room and board charges shall be no more than the charge for a semi-private accommodation in the Hospital of confinement, unless confinement in a subacute skilled nursing facility or private room is certified as medically necessary by an attending Physician.

- 1. Blue Shield will pay the following:

- Thus, Medi-Gap pays based on Medicare. Medicare covers Puerto Rico, so will Medi-Gap. Let me see if I can find another expert who agrees with me.

- Medicare.Gov agrees: If you have Original Medicare and you buy a Medigap policy, Medicare will pay its share of the Medicare-approved amount for covered health care costs. Then your Medigap policy pays its share.

- You can buy a Medigap policy from any insurance company that’s licensed in your state to sell one.

- I know I’ve been told that once you have a Medi-Gap plan you can keep it anywhere in the USA. I don’t see any residence requirements in the policy, nor agent guide, which does state you must live in the service area to get a Medicare Advantage plan. Thus, one can keep their Medi-Gap plan, anywhere, anytime.

- You can check with Medicare.gov to check what PDP Rx plans are available. Please verify your zip code.

- In the Blue Shield confidential agent guide, PDP Rx can only be sold in the service area – State. Thus, you would need to get coverage for Puerto Rico from a local agent or Medicare.Gov. You can do that at open enrollment or when you move. That would be a special enrollment period.

- Check out publication # 10521 Medicare in Puerto Rico

- I like to document everything I say. So, I know that a Medi-Gap policy simply pays based on what Medicare Pays, let’s find that in the policy. Blue Shield “N.” Table of contents is on page 6. Page 12 is benefits

FAQ’s

Out of Country Residence

- I live in Italy. I would like to buy and maintain guaranteed issue Medi gap (probably F – high deductible).

- However, if I read your other pages on your website, that will not be possible because I don’t have CA residency.

- And even if I managed to buy such a policy, it would probably not be maintainable without an ongoing CA address.

- Am I right so far?

- Let’s review the Blue Shield HI F Evidence of Coverage to take an example. I don’t see any mention of residency there.

- I don’t see residency mentioned in the application.

- At “EVERY” seminar I’ve ever been to, Medi Gap is touted as the solution to those who have grandchildren out of state for when they visit or those who travel in an RV Recreational Vehicle. PBS.org states that once you have a Medi Gap Plan, you can keep it, no matter where you live.

- I don’t see any mention of residency in Publication Medicare Medi Gap Guide

- The AARP 2017 Confidential Producer handbook page 10 states one must be a resident of the state in which they are applying. If they are going to cancel you for moving… it would have to be in their evidence of coverage. It’s not in Blue Shields.

- Blue Cross Agent Support per email says you must be a resident when you purchase coverage. Blue Shield said the same thing. BS did suggest contacting Medicare for ideas… I don’t know anyone at Medicare. I’ll try HICAP

- A Medi Gap wholesaler said the Insurance Companies go by the address on file with Medicare. They also point out, that Medicare is VERY limited outside USA. You might want to check out travel policies

- Reply from CA HICAP:

- Thanks for contacting California Health Advocates.

- A Medigap company can’t issue coverage out of the country, they aren’t licensed to do that outside the U.S. A Medigap can’t be used out of the country, except for the Medigap emergency benefit and that is not available to someone who lives outside the country.

- It sounds like he is trying to preserve his open enrollment opportunities and I don’t see a way for him to do that. If he has no serious health care conditions when he returns to the U.S., assuming he intends to return, he won’t have a guaranteed issue option but many insurers will sell him coverage at an underwritten rate.

- If he intends to ever return to the U.S., or visit frequently, he needs to apply for, and keep Medicare to ensure he has coverage when he returns, and that he will not be subject to any later premium penalties. If he is eligible for premium free Part A there are no premiums or late enrollment penalties for that part of Medicare, but there are for Part B, and even for Part C, the prescription drug benefit. Although this means he will pay premiums, even though Medicare will not pay for his care outside the U.S., these are serious premium penalties for delaying enrollment.

- He needs to consider what health care options he will have where he lives now if he intends to stay there, and whether that benefit will cover any care he might receive in the U.S. The consult or embassy where he lives may have some helpful information.

I hope this information is helpful.

- —

- Bonnie Burns

Training and Policy Specialist

California Health Advocates

- Bonnie Burns

My husband and I are thinking about moving to Washington State for 6 months (maybe longer) in June .

We are currently insured through Blue Shield of CA. BS of CA considers provider visits, in other states, out of network.

Should we change our coverage to Washington State – or – should we keep the coverage in CA and buy some sort of supplement (if one exists) to cover any “out of network” expenses while living in Washington?

If one exists – what sort of policy would that be?

Do you offer such policies?

I can’t define for you, where your residency is. The most authoritative thing I’ve ever seen is the FTB Guide # 1031

If you make a permanent move to Washington, that would give you a special enrollment period there, for making a move.

Subscribers must reside in the Plan Service Area for this plan within California to be eligible to enroll in coverage. Sample Blue Shield EOC

I’m not licensed in Washington. Check the NAHU Agent finder for someone licensed there.

A travel policy “might” work, but most of them, I understand won’t cover USA citizens as the plans don’t comply with ACA/Obamacare essential benefits.

Get Travel Quotes here Be sure to read all the caveats

Please read your EOC very carefully, it may be that doctor visits other than emergency or urgent care are not covered at all out of state, not even as out of network! Here’s our webpage on Blue Shield out of state.

When you go on Medicare – Medicare & Medi Gap are nationwide, you won’t have this problem in USA, it’s foreign travel that’s a problem.

We are moving from Texas to California, and my husband is on Medicare.

I’m wondering how to make sure he has continued coverage during the relocation process, and what I should do first.

So he has Medicare A Hospital & B Dr. Visits right? Here’s instructions to change your address with Medicare. You can do it online, visit them or call. Personally, I would do online.

What about Medi-Gap, Medicare Advantage or Part D Rx? What Insurance Companies are you with now? We can help you transfer that coverage. Check the menu above or site map for the plans that we have. What County in CA are you moving to?