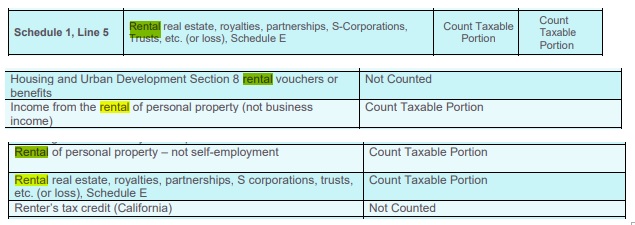

Schedule E Supplemental Income & Loss→ Schedule 1 Line 5 → Form 1040. → 8962 Premium Tax Credit

Schedule E Supplemental Income & Loss→ Schedule 1 Line 5 → Form 1040. → 8962 Premium Tax Credit

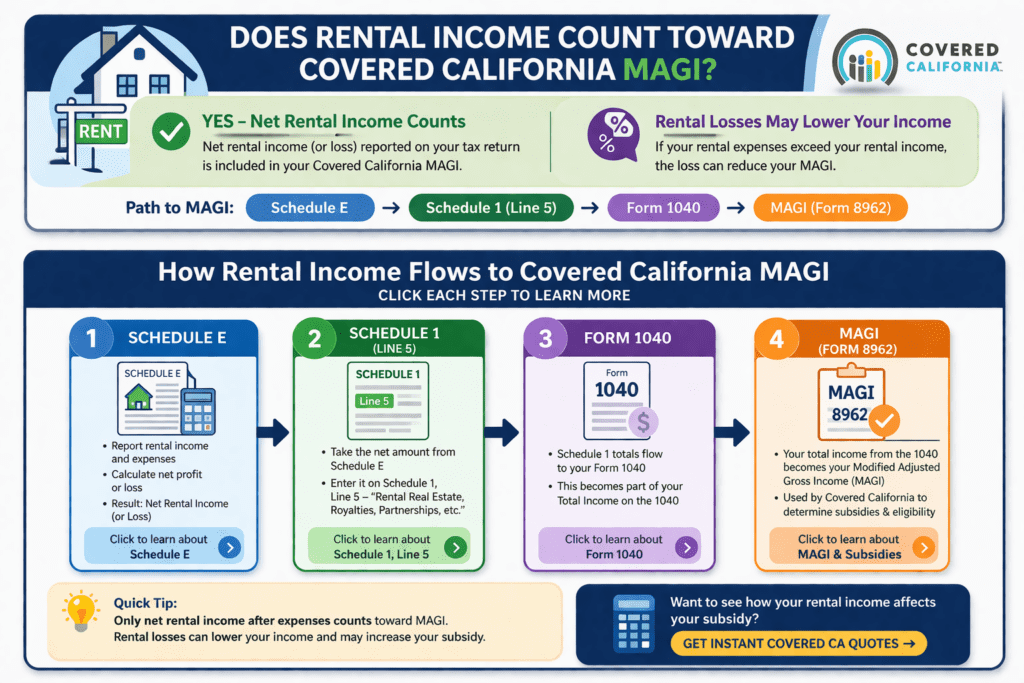

Does Rental Income Count for Covered California MAGI?

✅ YES — Net rental income (after expenses) counts toward MAGI

❌ Rental losses may reduce your income

Can Rental Losses Lower Your Covered CA Income?

- Rental losses from Schedule E may reduce your taxable income

- This can lower your MAGI for Covered California

- Depreciation and expenses can create a paper loss

- IRS Publication 527 #Residential Rental Property

⚠️ Passive loss rules may apply (consult a tax professional)

Estimate Your Covered California MAGI Income

Include your rental income (after expenses) to see your subsidy eligibility.

👉 Get Instant Covered CA & Direct Quotes

Common Questions About Rental Income and Covered CA

- Do I count gross rent? → No, only net after expenses

- Do rental losses count? → Yes, they may reduce income

- Do Airbnb / vacation rentals count? → Yes, if reported on Schedule E

- What about Section 8 income? → Generally counted as rental income

Covered CA MAGI Income #Rental Income & Losses

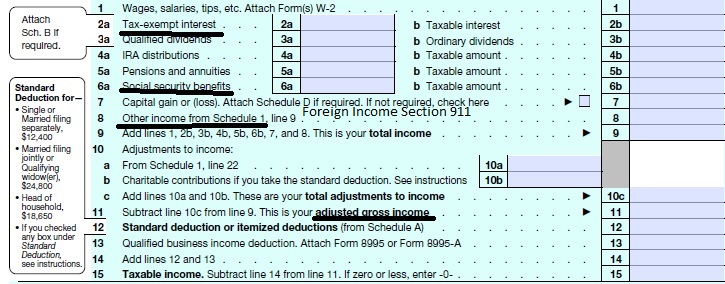

#Adjustments to Income - Schedule 1

#Schedule1 1040

- Part I Additional Income

- 2a Alimony received

- 3 Business income or (loss). Attach Schedule C

- Get Health Quote for your business

- 5 Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E

- 7 Unemployment compensation

- 8 Other income:

- a Net operating loss

- b Gambling income

- c Cancellation of debt

- d Foreign earned income exclusion from Form 2555

- e Taxable Health Savings Account distribution

- Part II Adjustments to Income

- 11 Educator expenses

- 13 Health savings account deduction. Attach Form 8889

- 15 Deductible part of self-employment tax. Attach Schedule SE

- Learn more about your Social Security Benefits

- 16 Self-employed SEP, SIMPLE, and qualified plans -

- 17 Self-employed health insurance deduction

- 19a Alimony paid

- 20 IRA Individual Retirement Account deduction

- 21 Student loan interest deduction

- Instant Business Health Insurance Proposals

Calculate your Covered CA MAGI Income

Take #Line8b 11 or your projected IRS 1040 Adjusted Gross income for the upcoming year then

add line 2a tax exempt interest

6a Social Security &

-

-

IMPORTANT!!!

The upcoming year – the future for what you tell Covered CA!

Sure, many people think it’s the past as Covered CA may ask for last years paperwork, but that’s BS! You might have to give back all the subsidies when you file Subsidy Reconciliation form #8962!

- Visit our MAIN webpage on MAGI Income

-

Rental income or a vacation home counts as taxable Covered California MAGI Income

- Rental Income net after losses, shows up on your 1040 tax return, Schedule E, Schedule 1 and is counted towards MAGI Modified Adjusted Gross income.

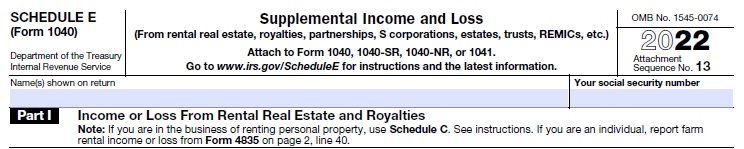

- Rental Property Income and Losses get calculated on Schedule E Supplemental Income & Loss

- Take the profit or loss from Schedule e and put it on Schedule 1 Line 5

- Put your income or loss from Schedule 1 on of your 1040.

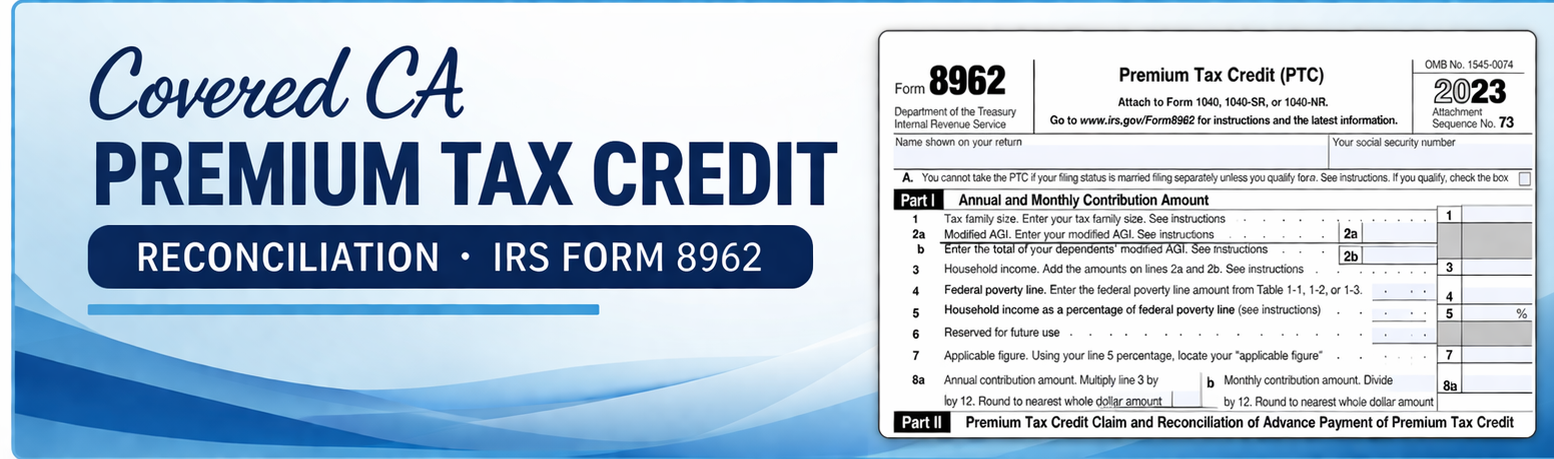

- Put your MAGI Modified Adjusted Gross income from your 1040 on line 2a of 8962 Premium Tax Credit

- Schedule E Supplemental Income & Loss

What rights do your Tenant’s Have?

How to #Estimate MAGI Income for Covered CA?

- From the AGI above, Add back in any

- foreign income,

- Social Security benefits and

- interest that are tax-exempt.

- View our main webpage on estimating income

-

Covered CA Premium Tax Credit Reconciliation IRS Form 8962

|

Vacation Homes

Tax Cut & Jobs Act

IRS Tips

Dwelling Unit.

This may be a house, an apartment, condominium, mobile home, boat, vacation home or similar property. It’s possible to use more than one dwelling unit as a residence during the year.

Used as a Home.

The dwelling unit is considered to be used as a residence if the taxpayer uses it for personal purposes during the tax year for more than the greater of: 14 days or 10% of the total days rented to others at a fair rental price. Rental expenses cannot be more than the rent received.

Personal Use.

Personal use means use by the owner, owner’s family, friends, other property owners and their families. Personal use includes anyone paying less than a fair rental price.

Divide Expenses.

Special rules generally apply to the rental of a home, apartment or other dwelling unit that is used by the taxpayer as a residence during the taxable year. Usually, rental income must be reported in full, and any expenses need to be divided between personal and business purposes. Special deduction limits apply.

How to Report.

Use Schedule E to report rental income and rental expenses on Supplemental Income and Loss. Rental income may also be subject to Net Investment Income Tax. Use Schedule A to report deductible expenses for personal use on Itemized Deductions. This includes such costs as mortgage interest, property taxes and casualty losses.

Special Rules.

If the dwelling unit is rented out fewer than 15 days during the year, none of the rental income is reportable and none of the rental expenses are deductible. Find out more about these rules; see Publication 527, Residential Rental Property (Including Rental of Vacation Homes).

Additional IRS Resources:

- Tax Topic 415 – Renting Residential and Vacation Property

- irs.gov/know-the-tax-facts-about-renting-out-residential-property

- Rental Income and Expenses – Real Estate Tax Tips

- Is My Residential Rental Income Taxable and/or Are My Expenses Deductible? IRS

IRS Topic 414 Rental Income & Expenses

Tips

IRS Rental Income Publication #527 pdf

Form 1040, Schedule E (PDF), Supplemental Income and Loss, to report income and expenses related to real estate rentals

Turbo Tax Summary

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

Covered CA

#Vacation Homes MAGI Income?

Renting out a vacation property to others can be profitable. If you do this, you must normally report the rental income on your tax return. You may not have to report the rent, however, if the rental period is short and you also use the property as your home. Here are some tips that you should know:

- Vacation Home. A vacation home can be a house, apartment, condominium, mobile home, boat or similar property.

- Schedule E. You usually report rental income and rental expenses on Schedule E, Supplemental Income and Loss. Your rental income may also be subject to Net Investment Income Tax.

- Used as a Home. If the property is “used as a home,” your rental expense deduction is limited. This means your deduction for rental expenses can’t be more than the rent you received. For more about these rules, see Publication 527, Residential Rental Property (Including Rental of Vacation Homes).

- Divide Expenses. If you personally use your property and also rent it to others, special rules apply. You must divide your expenses between rental use and personal use. To figure how to divide your costs, you must compare the number of days for each type of use with the total days of use.

- Personal Use. Personal use may include use by your family. It may also include use by any other property owners or their family. Use by anyone who pays less than a fair rental price is also considered personal use.

- Schedule A. Report deductible expenses for personal use on Schedule A, Itemized Deductions. These may include costs such as mortgage interest, property taxes and casualty losses.

- Rented Less than 15 Days. If the property is “used as a home” and you rent it out fewer than 15 days per year, you do not have to report the rental income. In this case you deduct your qualified expenses on Schedule A.

- Use IRS Free File. If you still need to file your 2015 tax return, you can use IRS Free File to make filing easier. Free File is available until Oct. 17. Free File is available only through the IRS.gov website.

IRS Tax Tips provide valuable information throughout the year. IRS.gov offers tax help and info on various topics including common tax scams, taxpayer rights and more.

Additional IRS Resources:

- Tax Topic 415 – Renting Residential and Vacation Property

- Rental Income and Expenses – Real Estate Tax Tips

- IRS Tax Tip 2018-79, May 22, 2018

- Publication 527 Residential Rental Property including VACATION HOMES

Instant Term Life Insurance Quote #naaipquote

- Schedule Zoom consultation

- Tools - Calculator to help you figure out how much you should get

- How much life insurance you really need?

Life Insurance Buyers Guide

#Covered CA Certified Agent

No extra charge for complementary assistance

You’ve been a tremendous help in providing this published documentation and I appreciate you.