“How to Eliminate Medi-Cal Share of Cost with the 250% Working Disabled Program”

Eligibility subject to county Medi-Cal determination. Must meet disability, income, and program requirements.

Eligibility subject to county Medi-Cal determination. Must meet disability, income, and program requirements.

“There are no minimum hours or amount you must earn”

250% Working disabled flyer from DHCS.Gov

How to Eliminate Medi-Cal Share of Cost

Using the 250% Working Disabled Program

A Little-Known Strategy

-

There is a Medi-Cal program that may allow you to:

-

Work (even part-time)

-

Keep full Medi-Cal coverage

-

Eliminate your Share of Cost (SOC)

-

-

This program is called the 250% Working Disabled Program (WDP)

👉 Eligibility subject to county Medi-Cal determination. Must meet disability, income, and program requirements.

🚨 You May Qualify with Very Small Income

-

There is no minimum number of hours required to work (DHCS guidance)

-

Even:

-

Part-time work

-

Self-employment

-

Very small income

-

may qualify as “working” (DHCS Working Disabled Program page)

👉 This is one of the most overlooked Medi-Cal strategies

- Email us [email protected]

What This Means for You

-

Instead of:

-

Paying a high monthly share of cost

-

-

You may qualify for:

-

Full Medi-Cal coverage

-

With a $0 or low monthly premium (DHCS WDP program updates)

-

👉Email us [email protected]

Why the Working Disabled Program Works

-

Disability-based income (such as SSDI) is not counted the same way as earned income (program methodology explained in WDP materials)

-

Earned income is:

-

Partially excluded

-

Not counted dollar-for-dollar (SSI income rules applied to Medi-Cal)

-

-

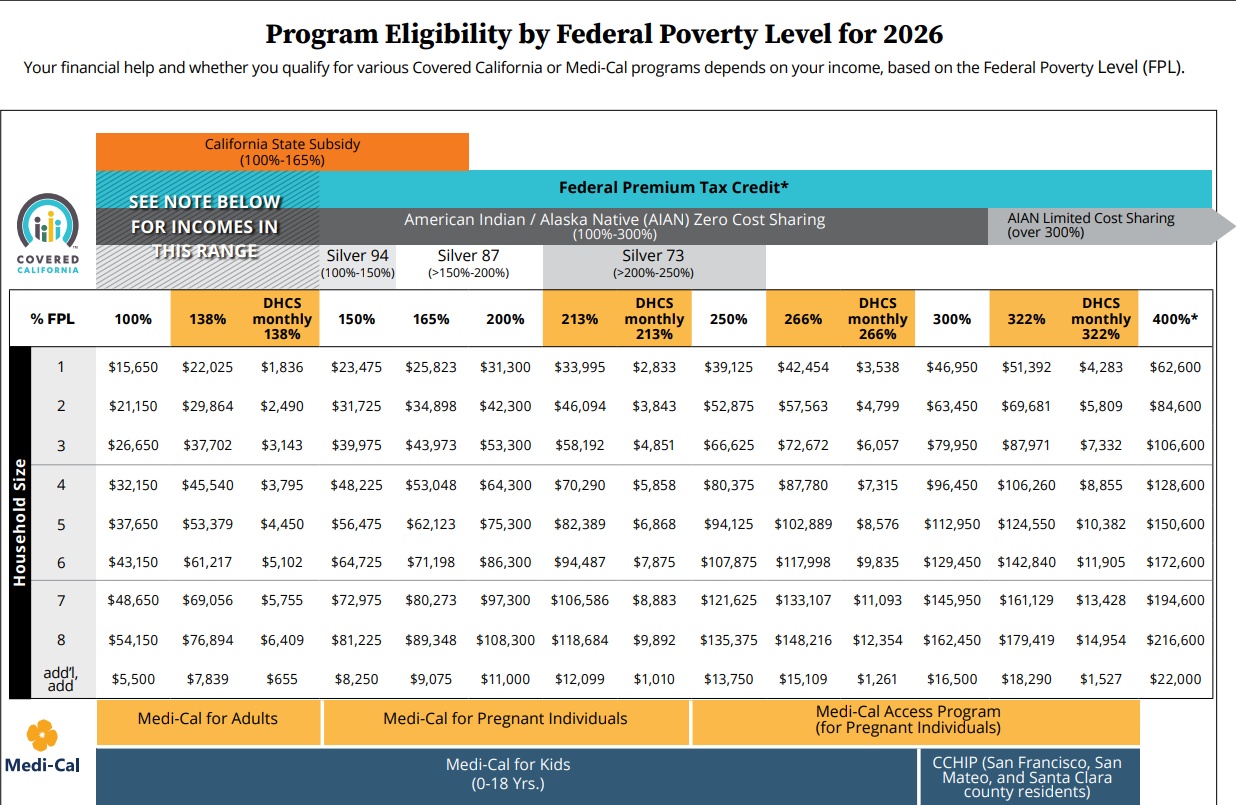

Eligibility is based on income up to:

-

250% of the Federal Poverty Level (DHCS program description)

-

👉Example (Simplified)

-

SSDI income: $2,500/month

-

Small part-time work: $300/month

Result:

-

Only part of the $300 is counted

-

SSDI may not disqualify eligibility

👉 The person may qualify for:

-

Full Medi-Cal

-

No Share of Cost

(Eligibility determined by county based on full rules)

Share of Cost vs Working Disabled Program

-

Share of Cost Medi-Cal

-

Pay large medical expenses before coverage begins

-

-

Working Disabled Program

-

Coverage starts immediately

-

May have:

-

$0 premium

-

Or a small monthly premium

-

-

👉 This is why many people switch when eligible

- Email us [email protected]

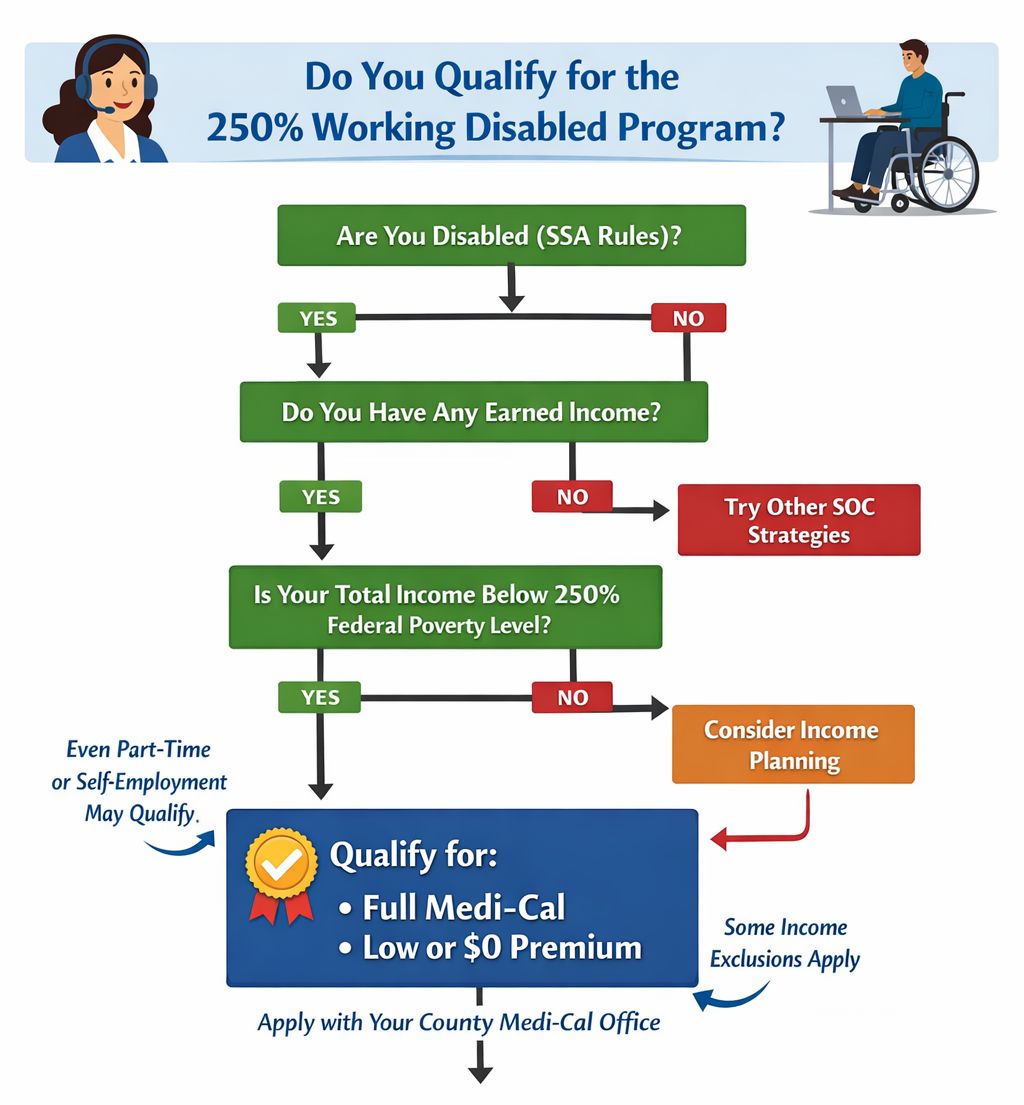

Quick Eligibility Check

-

Are you considered disabled under Social Security rules?

-

Yes / No

-

-

Do you have ANY earned income (even small)? DHCS.Gov

-

Yes / No

-

-

Is your income likely under about 250% of the Federal Poverty Level?

-

Yes / No / Not sure

-

If You Answered YES to All 3:

👉 You may qualify for the Working Disabled Program

👉 You may be able to eliminate your Share of Cost

- Email us [email protected]

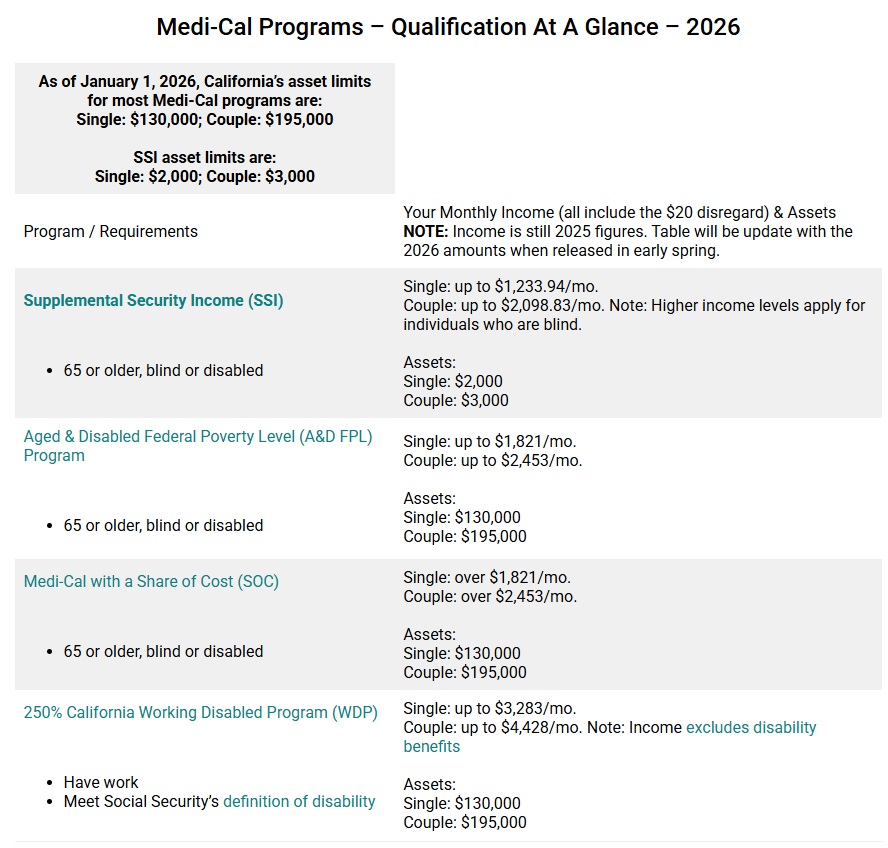

Asset Rules (Important Update for 2026+)

-

California previously eliminated asset limits

-

Asset limits are reinstated as of 2026

-

Current limits:

-

$130,000 (individual)

-

+$65,000 per additional household member

-

👉Some assets may still be excluded (home, vehicle, etc.)

- Email us [email protected]

Important: County Approval Required

-

The Working Disabled Program is:

-

Administered by your county Medi-Cal office

-

-

You must:

-

Apply through the county

-

Documentation required (work + disability)

-

Provide documentation of:

-

Disability

-

Earned income

-

-

👉When This Strategy Works Best

-

You currently have a high share of cost

-

You can perform any level of work

-

You want predictable coverage instead of monthly spend-down

Most Agents Don’t Tell You This – it’s rather technical..

-

There are ways to reduce or eliminate Share of Cost that:

-

Do not involve spending thousands on medical bills

-

Do not require giving up income

-

👉 The Working Disabled Program is one of those strategies

- Email us [email protected]

Not Sure If You Qualify?

We can help you evaluate:

-

Your income

-

Your work situation

-

Your current share of cost

👉 Request a Share of Cost Review

👉 Schedule a Zoom Consultation

- Email us [email protected]

-

- Medi Cal working while disabled dhcs.gov

- pdf flyer 250 percent working while disabled dhcs.gov

- Email us [email protected]

Can You Eliminate Your Medi-Cal Share of Cost?

You May Qualify Even If You Only Earn $50–$100 Per Month

Start Here:

-

Do you currently have a Medi-Cal Share of Cost (SOC)?

-

No → You may already qualify for full Medi-Cal

-

Yes → Continue below

-

Step 1: Do You Have Any Earned Income?

-

Yes → Go to Step 2

-

No → Go to Step 4

Step 2: Are You Disabled (SSDI or Similar Criteria)?

-

Yes → You may qualify for the Working Disabled 250% FPL Program (WDP)

-

Replace SOC with a zero premium

-

Keep full Medi-Cal coverage

(42 U.S.C. § 1396a(a)(10)(A)(ii)(XIII))

-

-

No → Go to Step 3

Step 3: Can You Work Even a Small Amount?

-

Yes → Consider creating earned income

-

Even part-time work may qualify you for WDP

(DHCS Medi-Cal Eligibility Procedures Manual § 5H)

-

-

No → Go to Step 4

Step 4: Do You Have Medical or Dental Expenses?

-

Yes → Consider the Dental or other Insurance Expense Strategy

-

Use dental premiums or Medical expenses like adult diapers to meet or reduce SOC

-

-

No → Go to Step 5

Step 5: Can Your Income Be Adjusted?

-

Yes → Consider Income Structuring

-

Reduce countable income

- Qualifying Health & Dental Coverage our webpage

-

Lower or eliminate SOC

-

-

No → SOC may still apply, but strategies may reduce impact

Step 6: Asset Check (2026 and Beyond)

-

Do your assets exceed:

-

$130,000 (individual)

-

+$65,000 per additional person

-

-

Yes → Planning may be needed before qualifying

-

No → Continue with strategy above

(California asset limits reinstated effective 2026 – DHCS / CANHR / CA Health Advocates)

- Email us [email protected]

- Share of Cost vs

- Working Disabled Program vs

- Dental, Vision, Insurance Premium Strategy

| Feature | Share of Cost Medi-Cal | Working Disabled Program | Insurance Expense Strategy |

|---|---|---|---|

| Monthly Cost | High / unpredictable | Low fixed premium | Variable |

| Requires Work | No | Yes (any level) | No |

| Income Treatment | Strict | Favorable exclusions | No change |

| Asset Rules (2026+) | Yes | Yes | Yes |

| Coverage | Full Medi-Cal after SOC met | Full Medi-Cal | Full Medi-Cal after SOC |

| Best Use | No other options | Working individuals | Temporary SOC reduction |

Share of Cost vs Working Disabled Program

-

Share of Cost:

-

Pay thousands before coverage starts

-

-

Working Disabled Program:

-

Full Medi-Cal immediately

-

Possibly $0 cost

-

Income & Asset Limits

Medi-Cal #Asset & Income Limits (2026)

For programs with an asset test (Aged/Blind/Disabled, Share-of-Cost, long-term care, Medicare Savings Programs):

- $130,000 for one person

- $195,000 for a couple

- +$65,000 for each additional household member (up to 10 people) (CalHealth Services)

These limits apply to countable assets, such as:

- Cash

- Bank accounts

- Stocks or brokerage accounts

- Certificates of deposit

- Additional real estate or second homes

- Extra vehicles (CalHealth Services)

Assets That Do NOT Count

Several assets are exempt, including:

- Your primary residence

- One vehicle

- Household goods and personal property

- Some retirement accounts if you are taking distributions our webpage

- Burial plots and certain prepaid funeral plans (CANHR)

This is why many people technically have more wealth than the limit but still qualify.

What If You’re Over the Asset Limit?

Yes — normally you must spend down assets until you fall below the limit.

Typical “spend-down” methods include:

Allowed spending

- Paying off debts (mortgage, credit cards, car loan)

- Home repairs or improvements

- Buying furniture or appliances

- Paying medical bills

- Prepaying rent or care costs

- Purchasing exempt assets (car, burial plan)

If your assets are still over $130,000 (or $195k for couples) when you apply or at renewal, Medi-Cal eligibility will be denied or terminated. (Justice in Aging)

Important Rule: Look-Back Period

For long-term-care Medi-Cal, our webpage California can review up to 30 months of financial history.

If someone gave away assets or transferred them for less than fair value, it can create a penalty period where Medi-Cal will not pay for care. (CunninghamLegal)

This is why planning is often done carefully with attorneys.

Example

Let’s say a single person has:

- $200,000 in savings

- A home they live in (not counted)

Since the limit is $130,000, they must spend down about $70,000 before Medi-Cal eligibility.

They could do that by:

- Paying off debts

- Home improvements

- Medical expenses our webpage

- Buying exempt items

The asset test only applies to “non-MAGI” Medi-Cal (mostly seniors, disabled, and long-term care).

MAGI Medi-Cal (Affordable Care Act expansion) has no asset test at all — eligibility is based on income only. (Justice in Aging)

✅ Bottom line:

- Asset limit in 2026: $130k single / $195k couple

- If you exceed it, you generally must spend down assets before qualifying.

- Some assets (home, car, personal property) don’t count.

- Improper transfers can trigger penalties.

- Email us [email protected]

If you want, Chat GBT can also explain three little-known strategies people use to qualify without just burning through their savings (these come up a lot in Medi-Cal planning and many agents don’t know them).

SSI #Resources & Income Limits

- Medi-Cal section of the

- Countable resources are the things you own that count toward the resource limit. Many things you own do not count.

CA Health Care Advocates * DHCS *

-

- asset questionnaire

- CANHR Fact Sheet

- Understanding Medi-Cal’s Asset Test for Seniors and People With Disabilities

- Western Poverty Law

- Nolo - SSI Income & Asset Limits

- Income SSA.Gov

- Will my settlement affect my government benefits? VIDEO

- dhcs.ca.gov/Asset-Limit-Changes-for-Non-MAGI-Medi-Cal

- california healthline.org/sset-test-elimination

- FAQ's

- Our webpage on SSI Resources & Income

- Have less than... of FPL in countable monthly income for an individual ... for a couple). ca health advocates.org ADFPL * AB 715 Fact Sheet * Western Poverty Law *

- Share of Cost if income is too high, but you qualify on asset test?

Resources & Links

- Insure Me Kevin.com *

- DHCS.CA.Gov *

- How to report assets Insure Me Kevin.com

Aged, Blind & Disabled Medi-Cal Program

Full-Scope Medi–Cal Health Benefits global

- See the My Medi Cal brochure for details & Benefits

- The Aged and/or Disabled Federal Poverty Level Program (See Income Chart) (A&D FPL) serves individuals aged 65 and older, and persons with disabilities.

- To qualify for this program, individuals Must meet all of the following three criteria:

- Be aged (65+) or

- disabled (meet Social Security’s definition of disability, even if your disability is blindness).

- If you are on SSI you get - Automatic Qualification for Medi Cal

- 2026 Asset Limits are back Learn More our webpage

- Worksheets for Determining Eligibility Under the Aged & Disabled Federal Poverty Level (A&D FPL) Medi-Cal Program Disability Rights *

- Qualifications at a Glance 2026 Cal Health Care Advocates.com

Resources & Links

- CANHR.org - Fact Sheet

- CA Health Care Advocates

- Kaiser Foundation

- Does Integrating Medicare and Medicaid Improve Care for Dual Eligibles?

- DHCS.CA.Gov

- Disability Benefits 101

- BenefitsCal online enrollment

-

Medicare And Disabilities

#Contact Us - Ask Questions - Get More Information - Schedule a Zoom Meeting

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

#My Medi-Cal

How to get the Health Care

You Need

24 pages

Smart Phones - try turning sideways to view pdf better

Working Disabled Program 250% of FPL (WDP)

“There are no minimum hours or wages required”

“Replace Share of Cost with $0 Medi-Cal”

Most Agents Don’t Tell You This

-

This program –

-

Allows you to work

-

Eliminates share of cost

-

May cost $0

-

eligibility is conditional:

-

Must meet disability + income 250% of FPL + SSI test – You would qualify for SSI if not that you were earning $$$

-

-

👉 And many people qualify without realizing it

What Is the Working Disabled Program?

-

The Working Disabled Program allows individuals with disabilities to work and still qualify for full-scope Medi-Cal. (42 U.S.C. § 1396a(a)(10)(A)(ii)(XIII))

- Email us [email protected]

Why This Matters for Share of Cost

-

Many individuals placed into Medi-Cal with a Share of Cost (SOC) may instead qualify for:

-

$0 share of cost Medi-Cal

-

-

This works because WDP uses more favorable income rules, especially for earned income. (DHCS Medi-Cal Eligibility Procedures Manual § 5H)

How WDP Lowers Countable Income

-

Earned income is not counted dollar-for-dollar. (20 CFR § 416.1112)

-

Additional deductions may apply, including:

-

Impairment-related work expenses (IRWE) (20 CFR § 416.976)

-

-

These rules can reduce income enough to:

-

Eliminate share of cost entirely

-

Or significantly reduce it

-

#Basic Eligibility Requirements

To qualify, an individual must generally:

-

Meet the definition of disabled under Social Security rules (Social Security Act § 1614(a))

- without regard to ability to perform substantial gainful activity. DHCS.Gov

-

Have earned income (even part-time work qualifies) (42 U.S.C. § 1396a(a)(10)(A)(ii)(XIII))

-

Meet Medi-Cal income requirements after exclusions (DHCS Manual § 5H)

Asset Rules (IMPORTANT – UPDATED FOR 2026)

-

California previously eliminated the Medi-Cal asset test in 2024–2025.

-

As of January 1, 2026, asset limits are reinstated, including for:

-

Working Disabled Program

-

Share of Cost Medi-Cal our webpage

-

Aged & Disabled programs our webpage

-

-

Current limits:

-

$130,000 for an individual

-

+$65,000 per additional household member

-

- More on 2026 Asset Limits

When WDP Is a Strong Strategy

-

You currently have a high share of cost

-

You can do any level of work (even minimal income)

-

You want predictable, affordable coverage instead of SOC

Key Planning Insight

-

Even a small amount of earned income can unlock eligibility

-

This creates a powerful strategy:

-

Shift from “spend down every month”

- Email us [email protected]

-

DHCS is clear:

-

You must apply through county office

👉 Add:

Important

-

Must be approved by your county apply through BenefitsCal.com

-

Documentation required (work + disability)

Bottom Line

-

If you have Medi-Cal with a share of cost:

-

The Working Disabled Program may eliminate it entirely

-

While allowing you to earn income and keep coverage

-

-

Not sure if you qualify?”

-

We’ll review:

-

Income

-

Work situation

-

Share of cost

-

👉 Request a Share of Cost Review Email us [email protected]

- Please include all relevant documents.

-

-

- Medi Cal working while disabled dhcs.gov

- pdf flyer 250 percent working while disabled dhcs.gov

- Email us [email protected]

#Social Security Disability

Factors in Evaluating

Parents & Care Givers

Check out our webpage on getting your own private disability coverage, in addition to Social Security Disability or SDI State Disability Coverage

- Disability Income – Pay Check Protection

- SSI – Supplemental Security Benefits – Automatic Medi Cal – SSDI

FAQ's

- Deafness?

- Mental Health – ACA/Health Reform Mandated Essential Benefit

- nolo.com/guide-to-social-security-disability

- c:/medi-gap/Social Security/disability